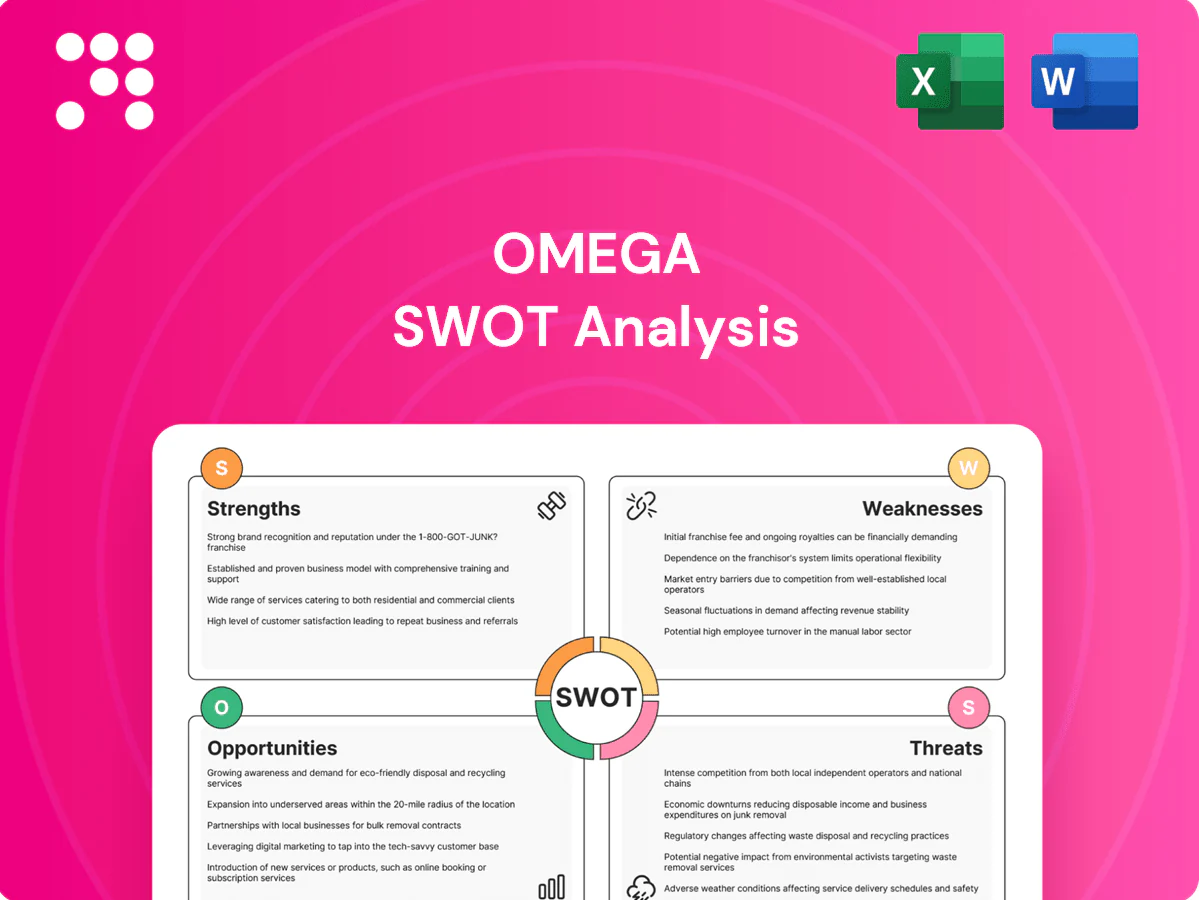

Omega SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Omega’s SWOT preview highlights key strengths, vulnerabilities, and market opportunities that shape its strategic outlook. For actionable guidance, purchase the full SWOT analysis to access a detailed, research-backed report. It includes editable Word and Excel deliverables perfect for planning, pitching, or investing. Unlock the complete insights and plan with confidence.

Strengths

Specialized healthcare REIT focus

Omega concentrates on skilled nursing and assisted living, owning approximately 800 facilities across more than 40 states (2024 reporting). This deep sector expertise supports informed underwriting and asset selection and fosters stronger operator and lender relationships. The niche focus historically yields more predictable, specialty-driven cash flows versus generic REIT strategies.

Predictable rental income

Long-term lease and mortgage structures generate recurring rental streams, and many agreements are triple-net, shifting property taxes, insurance and maintenance to tenants; this helps stabilize margins across cycles and underpins steady dividend capacity—FTSE Nareit All Equity REITs yield about 4.3% as of June 2025.

Demographic tailwinds

Aging populations drive rising demand for long-term care as the US 65+ cohort is projected to reach about 20.6% of the population by 2030, with the 85+ group set to roughly double by 2050 per UN/Census forecasts. Higher-acuity needs among older cohorts support sustained skilled nursing occupancy and higher case-mix intensity. Secular demographic growth can underpin rent coverage and help offset short-term market volatility.

Portfolio diversification benefits

Exposure across multiple facilities and operators reduces single-asset risk, geographic spread lowers localized market shocks, and lease staggering mitigates renewal concentration; together these diversification levers materially strengthen portfolio durability.

Operator partnerships and scale

Established operator partnerships enable superior underwriting and hands‑on asset management, improving lease-up and NOI stability; scale lowers blended cost of capital and expands proprietary transaction flow; larger platforms can recycle capital across portfolios swiftly, directing proceeds into higher‑return assets and steadily enhancing portfolio quality over time.

- Partnerships: better underwriting & operations

- Scale: lower cost of capital, broader sourcing

- Capital recycling: boosts portfolio quality

~800 skilled-nursing/assisted-living facilities, triple-net leases, 4.3% REIT yield

Omega owns ~800 skilled-nursing/assisted-living facilities across >40 states (2024), concentrating sector expertise and operator relationships. Long-term, often triple-net leases drive recurring, stable cashflows; FTSE Nareit All Equity REIT yield ~4.3% (Jun 2025). US 65+ cohort ~20.6% by 2030 supporting demand; geographic/lease diversification reduces single-asset and renewal risk.

| Metric | Value |

|---|---|

| Facilities | ~800 (2024) |

| States | >40 |

| Lease type | Many triple-net |

| REIT yield | 4.3% (Jun 2025) |

| 65+ pop | 20.6% by 2030 |

What is included in the product

Delivers a strategic overview of Omega’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to inform decision-making and sharpen competitive strategy.

Provides a compact, visual SWOT dashboard to quickly identify and address strategic pain points; editable layout enables rapid updates to align actions with changing priorities.

Weaknesses

Operator credit dependence

Rent coverage for Omega is directly tied to tenant financial health: skilled nursing occupancy averaged about 79% in 2024 (NIC) and many operators reported median operating margins near 3% in 2024, leaving little cushion. Thin margins and rising labor/supply costs increase risk that tenant distress will force rent deferrals or restructurings, introducing measurable volatility to cash flows.

Regulatory reimbursement exposure

Revenue for tenants relies heavily on Medicare and Medicaid, with Medicaid covering roughly 50% of nursing home revenue and Medicare about 15% (industry averages 2023–24). Policy or rate changes can compress operator margins, reducing profitability and rent coverage. Reduced reimbursements can impair operators' ability to pay rent, leaving the REIT indirectly exposed to public funding risk.

Interest rate sensitivity

REIT valuations and financing costs move with interest rates: with the U.S. 10-year near 4.4% and the federal funds rate at 5.25–5.50% (mid‑2025), rising rates can compress cap‑rate spreads and dividend yields, make debt refinancing materially more expensive, and constrain Omega’s ability to fund growth investments and maintain payouts.

Asset and sector concentration

Heavy weighting to skilled nursing concentrates Omega’s operational and reimbursement risk in a single care model; shifts toward home- and community-based care or value-based payment reforms can reduce demand for facility-based SNF services. Limited exposure to hospitals, outpatient, or post-acute alternatives reduces portfolio diversification and can amplify revenue declines during sector downturns.

- Skilled nursing concentration raises reimbursement and census sensitivity

- Shift to alternative care settings threatens demand

- Low diversification limits revenue resilience

- Concentration can magnify downturn impacts

Capex and repositioning needs

Aging facilities may require upgrades to remain competitive, and while many tenants absorb routine capex, lease negotiations increasingly shift larger capital burdens back to owners. Repositioning assets can pause income streams and delay cash flows during transitions; documented operator changes carry execution risk that can extend downtime and increase costs.

- Tenant-paid vs owner-paid capex: negotiation leverage

- Repositioning delays: cash-flow timing risk

- Operator change: execution and downtime risk

SNF risk: 79% occ, ~3% margins, Medicaid mix, rate shock

Omega faces tenant risk: 2024 skilled nursing occupancy ~79% and median operator margins near 3%, raising rent-deferral risk. Payer mix concentrates risk: Medicaid ~50% and Medicare ~15% of revenue (2023–24), so reimbursement cuts would hit rent coverage. Rising rates (U.S. 10‑yr ~4.4%, fed funds 5.25–5.50% mid‑2025) raise refinancing and cap‑rate pressure. Aging inventory and SNF concentration limit diversification.

| Metric | Value | Impact |

|---|---|---|

| SNF occupancy (2024) | 79% | Low cash flow cushion |

| Median operator margin (2024) | ~3% | High rent stress |

| Medicaid/Medicare | 50% / 15% | Reimbursement risk |

| Rates (mid‑2025) | 10‑yr 4.4%, fed 5.25–5.50% | Refi & cap‑rate pressure |

Preview the Actual Deliverable

Omega SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the complete, editable version becomes available after checkout. Buy now to unlock the entire detailed file, ready to use in presentations or strategy work.

Make Insightful Decisions Backed by Expert Research

Omega’s SWOT preview highlights key strengths, vulnerabilities, and market opportunities that shape its strategic outlook. For actionable guidance, purchase the full SWOT analysis to access a detailed, research-backed report. It includes editable Word and Excel deliverables perfect for planning, pitching, or investing. Unlock the complete insights and plan with confidence.

Strengths

Specialized healthcare REIT focus

Omega concentrates on skilled nursing and assisted living, owning approximately 800 facilities across more than 40 states (2024 reporting). This deep sector expertise supports informed underwriting and asset selection and fosters stronger operator and lender relationships. The niche focus historically yields more predictable, specialty-driven cash flows versus generic REIT strategies.

Predictable rental income

Long-term lease and mortgage structures generate recurring rental streams, and many agreements are triple-net, shifting property taxes, insurance and maintenance to tenants; this helps stabilize margins across cycles and underpins steady dividend capacity—FTSE Nareit All Equity REITs yield about 4.3% as of June 2025.

Demographic tailwinds

Aging populations drive rising demand for long-term care as the US 65+ cohort is projected to reach about 20.6% of the population by 2030, with the 85+ group set to roughly double by 2050 per UN/Census forecasts. Higher-acuity needs among older cohorts support sustained skilled nursing occupancy and higher case-mix intensity. Secular demographic growth can underpin rent coverage and help offset short-term market volatility.

Portfolio diversification benefits

Exposure across multiple facilities and operators reduces single-asset risk, geographic spread lowers localized market shocks, and lease staggering mitigates renewal concentration; together these diversification levers materially strengthen portfolio durability.

Operator partnerships and scale

Established operator partnerships enable superior underwriting and hands‑on asset management, improving lease-up and NOI stability; scale lowers blended cost of capital and expands proprietary transaction flow; larger platforms can recycle capital across portfolios swiftly, directing proceeds into higher‑return assets and steadily enhancing portfolio quality over time.

- Partnerships: better underwriting & operations

- Scale: lower cost of capital, broader sourcing

- Capital recycling: boosts portfolio quality

~800 skilled-nursing/assisted-living facilities, triple-net leases, 4.3% REIT yield

Omega owns ~800 skilled-nursing/assisted-living facilities across >40 states (2024), concentrating sector expertise and operator relationships. Long-term, often triple-net leases drive recurring, stable cashflows; FTSE Nareit All Equity REIT yield ~4.3% (Jun 2025). US 65+ cohort ~20.6% by 2030 supporting demand; geographic/lease diversification reduces single-asset and renewal risk.

| Metric | Value |

|---|---|

| Facilities | ~800 (2024) |

| States | >40 |

| Lease type | Many triple-net |

| REIT yield | 4.3% (Jun 2025) |

| 65+ pop | 20.6% by 2030 |

What is included in the product

Delivers a strategic overview of Omega’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to inform decision-making and sharpen competitive strategy.

Provides a compact, visual SWOT dashboard to quickly identify and address strategic pain points; editable layout enables rapid updates to align actions with changing priorities.

Weaknesses

Operator credit dependence

Rent coverage for Omega is directly tied to tenant financial health: skilled nursing occupancy averaged about 79% in 2024 (NIC) and many operators reported median operating margins near 3% in 2024, leaving little cushion. Thin margins and rising labor/supply costs increase risk that tenant distress will force rent deferrals or restructurings, introducing measurable volatility to cash flows.

Regulatory reimbursement exposure

Revenue for tenants relies heavily on Medicare and Medicaid, with Medicaid covering roughly 50% of nursing home revenue and Medicare about 15% (industry averages 2023–24). Policy or rate changes can compress operator margins, reducing profitability and rent coverage. Reduced reimbursements can impair operators' ability to pay rent, leaving the REIT indirectly exposed to public funding risk.

Interest rate sensitivity

REIT valuations and financing costs move with interest rates: with the U.S. 10-year near 4.4% and the federal funds rate at 5.25–5.50% (mid‑2025), rising rates can compress cap‑rate spreads and dividend yields, make debt refinancing materially more expensive, and constrain Omega’s ability to fund growth investments and maintain payouts.

Asset and sector concentration

Heavy weighting to skilled nursing concentrates Omega’s operational and reimbursement risk in a single care model; shifts toward home- and community-based care or value-based payment reforms can reduce demand for facility-based SNF services. Limited exposure to hospitals, outpatient, or post-acute alternatives reduces portfolio diversification and can amplify revenue declines during sector downturns.

- Skilled nursing concentration raises reimbursement and census sensitivity

- Shift to alternative care settings threatens demand

- Low diversification limits revenue resilience

- Concentration can magnify downturn impacts

Capex and repositioning needs

Aging facilities may require upgrades to remain competitive, and while many tenants absorb routine capex, lease negotiations increasingly shift larger capital burdens back to owners. Repositioning assets can pause income streams and delay cash flows during transitions; documented operator changes carry execution risk that can extend downtime and increase costs.

- Tenant-paid vs owner-paid capex: negotiation leverage

- Repositioning delays: cash-flow timing risk

- Operator change: execution and downtime risk

SNF risk: 79% occ, ~3% margins, Medicaid mix, rate shock

Omega faces tenant risk: 2024 skilled nursing occupancy ~79% and median operator margins near 3%, raising rent-deferral risk. Payer mix concentrates risk: Medicaid ~50% and Medicare ~15% of revenue (2023–24), so reimbursement cuts would hit rent coverage. Rising rates (U.S. 10‑yr ~4.4%, fed funds 5.25–5.50% mid‑2025) raise refinancing and cap‑rate pressure. Aging inventory and SNF concentration limit diversification.

| Metric | Value | Impact |

|---|---|---|

| SNF occupancy (2024) | 79% | Low cash flow cushion |

| Median operator margin (2024) | ~3% | High rent stress |

| Medicaid/Medicare | 50% / 15% | Reimbursement risk |

| Rates (mid‑2025) | 10‑yr 4.4%, fed 5.25–5.50% | Refi & cap‑rate pressure |

Preview the Actual Deliverable

Omega SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the complete, editable version becomes available after checkout. Buy now to unlock the entire detailed file, ready to use in presentations or strategy work.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Omega’s SWOT preview highlights key strengths, vulnerabilities, and market opportunities that shape its strategic outlook. For actionable guidance, purchase the full SWOT analysis to access a detailed, research-backed report. It includes editable Word and Excel deliverables perfect for planning, pitching, or investing. Unlock the complete insights and plan with confidence.

Strengths

Specialized healthcare REIT focus

Omega concentrates on skilled nursing and assisted living, owning approximately 800 facilities across more than 40 states (2024 reporting). This deep sector expertise supports informed underwriting and asset selection and fosters stronger operator and lender relationships. The niche focus historically yields more predictable, specialty-driven cash flows versus generic REIT strategies.

Predictable rental income

Long-term lease and mortgage structures generate recurring rental streams, and many agreements are triple-net, shifting property taxes, insurance and maintenance to tenants; this helps stabilize margins across cycles and underpins steady dividend capacity—FTSE Nareit All Equity REITs yield about 4.3% as of June 2025.

Demographic tailwinds

Aging populations drive rising demand for long-term care as the US 65+ cohort is projected to reach about 20.6% of the population by 2030, with the 85+ group set to roughly double by 2050 per UN/Census forecasts. Higher-acuity needs among older cohorts support sustained skilled nursing occupancy and higher case-mix intensity. Secular demographic growth can underpin rent coverage and help offset short-term market volatility.

Portfolio diversification benefits

Exposure across multiple facilities and operators reduces single-asset risk, geographic spread lowers localized market shocks, and lease staggering mitigates renewal concentration; together these diversification levers materially strengthen portfolio durability.

Operator partnerships and scale

Established operator partnerships enable superior underwriting and hands‑on asset management, improving lease-up and NOI stability; scale lowers blended cost of capital and expands proprietary transaction flow; larger platforms can recycle capital across portfolios swiftly, directing proceeds into higher‑return assets and steadily enhancing portfolio quality over time.

- Partnerships: better underwriting & operations

- Scale: lower cost of capital, broader sourcing

- Capital recycling: boosts portfolio quality

~800 skilled-nursing/assisted-living facilities, triple-net leases, 4.3% REIT yield

Omega owns ~800 skilled-nursing/assisted-living facilities across >40 states (2024), concentrating sector expertise and operator relationships. Long-term, often triple-net leases drive recurring, stable cashflows; FTSE Nareit All Equity REIT yield ~4.3% (Jun 2025). US 65+ cohort ~20.6% by 2030 supporting demand; geographic/lease diversification reduces single-asset and renewal risk.

| Metric | Value |

|---|---|

| Facilities | ~800 (2024) |

| States | >40 |

| Lease type | Many triple-net |

| REIT yield | 4.3% (Jun 2025) |

| 65+ pop | 20.6% by 2030 |

What is included in the product

Delivers a strategic overview of Omega’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to inform decision-making and sharpen competitive strategy.

Provides a compact, visual SWOT dashboard to quickly identify and address strategic pain points; editable layout enables rapid updates to align actions with changing priorities.

Weaknesses

Operator credit dependence

Rent coverage for Omega is directly tied to tenant financial health: skilled nursing occupancy averaged about 79% in 2024 (NIC) and many operators reported median operating margins near 3% in 2024, leaving little cushion. Thin margins and rising labor/supply costs increase risk that tenant distress will force rent deferrals or restructurings, introducing measurable volatility to cash flows.

Regulatory reimbursement exposure

Revenue for tenants relies heavily on Medicare and Medicaid, with Medicaid covering roughly 50% of nursing home revenue and Medicare about 15% (industry averages 2023–24). Policy or rate changes can compress operator margins, reducing profitability and rent coverage. Reduced reimbursements can impair operators' ability to pay rent, leaving the REIT indirectly exposed to public funding risk.

Interest rate sensitivity

REIT valuations and financing costs move with interest rates: with the U.S. 10-year near 4.4% and the federal funds rate at 5.25–5.50% (mid‑2025), rising rates can compress cap‑rate spreads and dividend yields, make debt refinancing materially more expensive, and constrain Omega’s ability to fund growth investments and maintain payouts.

Asset and sector concentration

Heavy weighting to skilled nursing concentrates Omega’s operational and reimbursement risk in a single care model; shifts toward home- and community-based care or value-based payment reforms can reduce demand for facility-based SNF services. Limited exposure to hospitals, outpatient, or post-acute alternatives reduces portfolio diversification and can amplify revenue declines during sector downturns.

- Skilled nursing concentration raises reimbursement and census sensitivity

- Shift to alternative care settings threatens demand

- Low diversification limits revenue resilience

- Concentration can magnify downturn impacts

Capex and repositioning needs

Aging facilities may require upgrades to remain competitive, and while many tenants absorb routine capex, lease negotiations increasingly shift larger capital burdens back to owners. Repositioning assets can pause income streams and delay cash flows during transitions; documented operator changes carry execution risk that can extend downtime and increase costs.

- Tenant-paid vs owner-paid capex: negotiation leverage

- Repositioning delays: cash-flow timing risk

- Operator change: execution and downtime risk

SNF risk: 79% occ, ~3% margins, Medicaid mix, rate shock

Omega faces tenant risk: 2024 skilled nursing occupancy ~79% and median operator margins near 3%, raising rent-deferral risk. Payer mix concentrates risk: Medicaid ~50% and Medicare ~15% of revenue (2023–24), so reimbursement cuts would hit rent coverage. Rising rates (U.S. 10‑yr ~4.4%, fed funds 5.25–5.50% mid‑2025) raise refinancing and cap‑rate pressure. Aging inventory and SNF concentration limit diversification.

| Metric | Value | Impact |

|---|---|---|

| SNF occupancy (2024) | 79% | Low cash flow cushion |

| Median operator margin (2024) | ~3% | High rent stress |

| Medicaid/Medicare | 50% / 15% | Reimbursement risk |

| Rates (mid‑2025) | 10‑yr 4.4%, fed 5.25–5.50% | Refi & cap‑rate pressure |

Preview the Actual Deliverable

Omega SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the complete, editable version becomes available after checkout. Buy now to unlock the entire detailed file, ready to use in presentations or strategy work.