ON24 Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

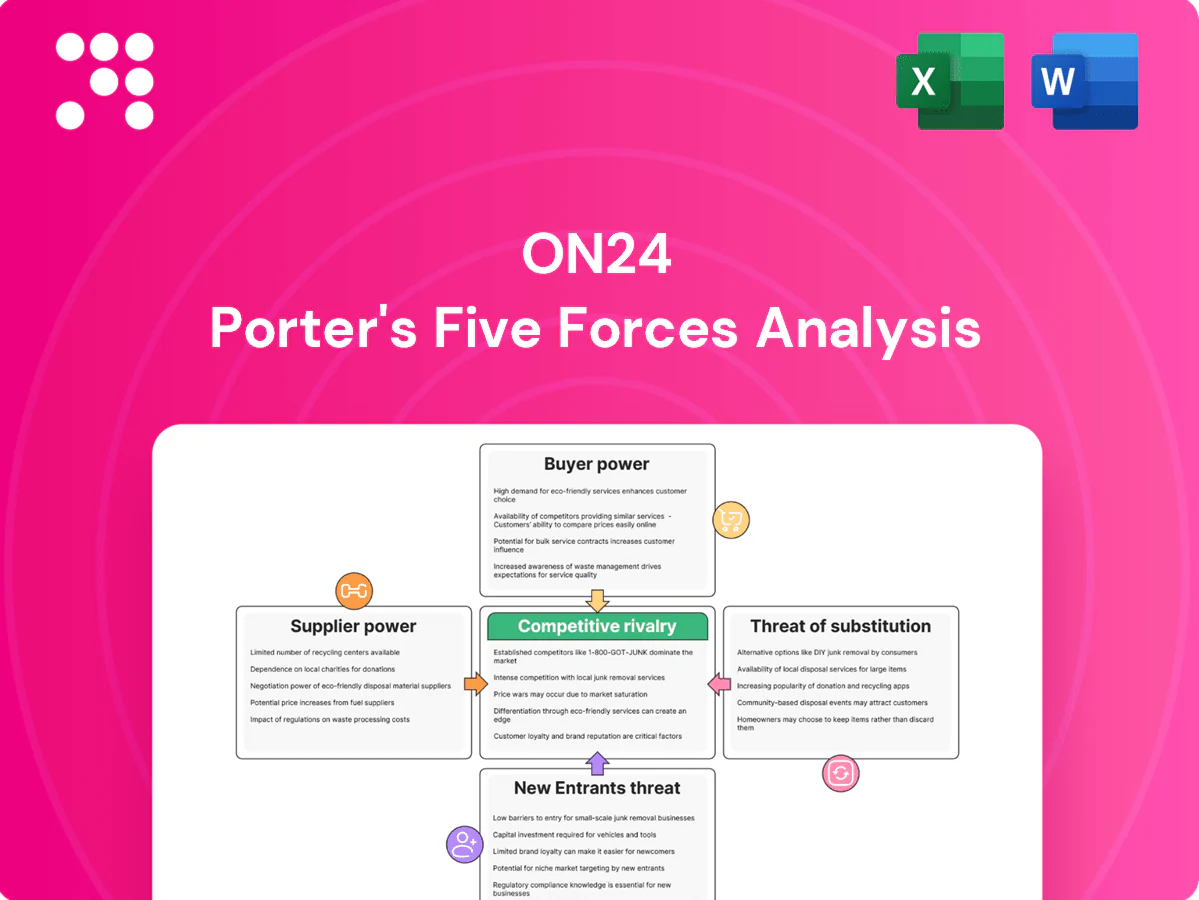

ON24 faces moderate supplier power, high buyer expectations for sophisticated digital event platforms, intense rivalry among webinar and virtual-event providers, low immediate substitute risk but growing pressure from free conferencing tools, and moderate barriers to entry. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ON24’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud and CDN concentration

ON24 depends on a small set of hyperscalers (AWS, Microsoft Azure, Google Cloud) and major CDNs (Akamai, Cloudflare) for compute, storage and delivery; the top three cloud providers held roughly 65% of the global IaaS/PaaS market in 2024 (Gartner). Multi‑cloud deployment and volume commitments can reduce supplier leverage, but major outages or abrupt price changes still risk materially harming margins and SLA delivery.

Critical video and data tooling

Encoding, streaming SDKs, and analytics for ON24 are sourced from specialized vendors, creating high switching costs given limited high-quality alternatives and proprietary features. Open-source WebRTC and analytics libraries exist and in 2024 serve 1B+ monthly users but require significant integration and support resources. This supplier dependence strengthens vendor negotiation power, especially during contract renewals and price resets.

Integration partners and platforms

Deep integrations with CRM/MA platforms like Salesforce and Marketo are essential for ON24; ON24 lists native connectors to both on its integrations page. Salesforce held roughly 24% of the global CRM market in 2023 (IDC), making it a key gatekeeper. Platform policies, APIs and marketplace economics (e.g., listing and integration requirements) shift margins, and certification/co-sell programs add compliance costs, so gatekeepers wield moderate power.

Security, compliance, and privacy vendors

Enterprise deals force ON24 to embed third-party security tools and identity/compliance frameworks; certifications like SOC 2 (readiness plus audit commonly $50,000–200,000) and ISO audits ($20,000–100,000) require external auditors and services, while GDPR carries fines up to €20 million or 4% of global turnover; these costs and mandatory status reduce flexibility and increase supplier leverage.

- Third-party tooling: must-have for enterprise sales

- Certification costs: SOC 2 $50k–200k; ISO $20k–100k

- Regulatory risk: GDPR fines up to €20M or 4% turnover

Specialized talent and services

Skilled cloud, data, and video engineers remain scarce, giving labor markets cyclic pricing power that can drive wage and contract cost volatility for ON24; event production partners provide scalable capacity but are largely substitutable, limiting long-term supplier leverage. Retention programs reduce attrition risk yet materially raise operating expenses and total cost of ownership.

- Skilled talent scarcity: high hiring competition

- Labor markets: cyclical pricing power

- Event partners: add capacity but substitutable

- Retention programs: lower risk, raise OPEX

Cloud and CRM concentration raise switching costs, outage risk and talent-driven wage pressure

ON24 faces concentrated supplier power from top hyperscalers (top three IaaS/PaaS ~65% global share in 2024, Gartner), CDNs and specialist streaming vendors, raising switching costs and outage/price-change risk; CRM gatekeepers (Salesforce ~24% CRM share, IDC 2023) and mandatory compliance/vendors (SOC 2, ISO) further constrain flexibility; skilled talent scarcity adds wage pressure and vendor leverage.

| Supplier | Metric | 2024/Latest |

|---|---|---|

| Top cloud providers | Top-3 IaaS/PaaS share | ~65% (Gartner 2024) |

| Salesforce | CRM market share | ~24% (IDC 2023) |

| Compliance | SOC 2 audit cost | $50k–$200k |

| Regulatory | GDPR fine | €20M or 4% turnover |

What is included in the product

Comprehensive Porter's Five Forces assessment tailored to ON24 that uncovers competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and highlights disruptive trends and strategic levers affecting pricing, market share, and profitability.

A concise Porter's Five Forces one-sheet for ON24 that highlights competitive pressures and relieves decision-making pain by visualizing threat levels and action priorities—easy to customize, copy into decks, and update as market conditions change.

Customers Bargaining Power

Enterprise procurement leverage

ON24 sells to marketing and sales organizations with formal procurement, where large buyers leverage volume to secure discounts typically in the 10–25% range and negotiated service-level terms; competitive RFPs and bids further intensify pricing pressure. Multi-year contracts are common, trading lower annual pricing for retention and reduced churn, aligning with enterprise procurement priorities in 2024.

Switching costs vary by integration depth

Light users can shift to rivals with minimal friction, keeping buyer power high for simple webinar use cases; 2024 surveys show about 54% of buyers favor low-cost, standalone tools. Deep integrations, data pipelines, and custom workflows raise switching costs and lower buyer power for embedded deployments. ON24’s analytics and content hubs increase stickiness, often reducing churn by roughly 20% in integrated accounts.

Abundant alternatives and price sensitivity

Buyers routinely compare ON24 with Zoom, Teams, Webex and dedicated event platforms, intensifying switching options. Economic cycles increase scrutiny on ROI and seat utilization, tightening procurement. Freemium tiers and bundled UCaaS offerings anchor lower price expectations; Zoom reported 300 million daily meeting participants in 2020, highlighting alternative scale and elevating buyer bargaining power.

Demand for measurable ROI

Customers demand conversion lift, attribution, and sales acceleration; Gartner 2024 found 64% of B2B buyers require clear ROI proof, so ON24s strong analytics that drive measurable lift justify premium pricing and lower churn, while weak outcomes trigger renegotiation or switching; value proof therefore directly reduces buyer power.

- ROI focus: 64% (Gartner 2024)

- Price leverage: analytics = premium retention

- Risk: poor outcomes → churn/renegotiation

Global support and reliability expectations

Enterprises typically demand uptime SLAs of 99.9% or higher, global delivery and compliance assurances; failures commonly trigger service credits or contract terminations. Buyers leverage SLAs to extract price or support concessions, while demonstrable superior reliability reduces the need for such concessions and lowers churn risk.

- 99.9%+ uptime standard

- Service credits or exits on breach

- SLAs used as negotiation levers

- Higher reliability = fewer concessions

Buyers leverage: 10-25% cuts; 64% need ROI; 99.9%+ SLA

Buyers hold strong leverage: large deals secure 10–25% discounts and SLAs drive concessions; 54% favored low-cost tools in 2024. Integrations, analytics and content hubs cut churn ~20% and support premium pricing; 64% require clear ROI (Gartner 2024). 99.9%+ uptime expectations lower buyer power.

| Metric | Value |

|---|---|

| ROI requirement | 64% |

| Low-cost preference | 54% |

| Churn reduction (integrated) | ~20% |

| Uptime SLA | 99.9%+ |

Full Version Awaits

ON24 Porter's Five Forces Analysis

This ON24 Porter's Five Forces Analysis preview is the exact, fully formatted document you’ll receive instantly after purchase—no mockups, no placeholders. It contains the complete competitive assessment, strategic implications, and actionable insights ready for download and use. What you see here is precisely the deliverable you’ll get upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

ON24 faces moderate supplier power, high buyer expectations for sophisticated digital event platforms, intense rivalry among webinar and virtual-event providers, low immediate substitute risk but growing pressure from free conferencing tools, and moderate barriers to entry. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ON24’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud and CDN concentration

ON24 depends on a small set of hyperscalers (AWS, Microsoft Azure, Google Cloud) and major CDNs (Akamai, Cloudflare) for compute, storage and delivery; the top three cloud providers held roughly 65% of the global IaaS/PaaS market in 2024 (Gartner). Multi‑cloud deployment and volume commitments can reduce supplier leverage, but major outages or abrupt price changes still risk materially harming margins and SLA delivery.

Critical video and data tooling

Encoding, streaming SDKs, and analytics for ON24 are sourced from specialized vendors, creating high switching costs given limited high-quality alternatives and proprietary features. Open-source WebRTC and analytics libraries exist and in 2024 serve 1B+ monthly users but require significant integration and support resources. This supplier dependence strengthens vendor negotiation power, especially during contract renewals and price resets.

Integration partners and platforms

Deep integrations with CRM/MA platforms like Salesforce and Marketo are essential for ON24; ON24 lists native connectors to both on its integrations page. Salesforce held roughly 24% of the global CRM market in 2023 (IDC), making it a key gatekeeper. Platform policies, APIs and marketplace economics (e.g., listing and integration requirements) shift margins, and certification/co-sell programs add compliance costs, so gatekeepers wield moderate power.

Security, compliance, and privacy vendors

Enterprise deals force ON24 to embed third-party security tools and identity/compliance frameworks; certifications like SOC 2 (readiness plus audit commonly $50,000–200,000) and ISO audits ($20,000–100,000) require external auditors and services, while GDPR carries fines up to €20 million or 4% of global turnover; these costs and mandatory status reduce flexibility and increase supplier leverage.

- Third-party tooling: must-have for enterprise sales

- Certification costs: SOC 2 $50k–200k; ISO $20k–100k

- Regulatory risk: GDPR fines up to €20M or 4% turnover

Specialized talent and services

Skilled cloud, data, and video engineers remain scarce, giving labor markets cyclic pricing power that can drive wage and contract cost volatility for ON24; event production partners provide scalable capacity but are largely substitutable, limiting long-term supplier leverage. Retention programs reduce attrition risk yet materially raise operating expenses and total cost of ownership.

- Skilled talent scarcity: high hiring competition

- Labor markets: cyclical pricing power

- Event partners: add capacity but substitutable

- Retention programs: lower risk, raise OPEX

Cloud and CRM concentration raise switching costs, outage risk and talent-driven wage pressure

ON24 faces concentrated supplier power from top hyperscalers (top three IaaS/PaaS ~65% global share in 2024, Gartner), CDNs and specialist streaming vendors, raising switching costs and outage/price-change risk; CRM gatekeepers (Salesforce ~24% CRM share, IDC 2023) and mandatory compliance/vendors (SOC 2, ISO) further constrain flexibility; skilled talent scarcity adds wage pressure and vendor leverage.

| Supplier | Metric | 2024/Latest |

|---|---|---|

| Top cloud providers | Top-3 IaaS/PaaS share | ~65% (Gartner 2024) |

| Salesforce | CRM market share | ~24% (IDC 2023) |

| Compliance | SOC 2 audit cost | $50k–$200k |

| Regulatory | GDPR fine | €20M or 4% turnover |

What is included in the product

Comprehensive Porter's Five Forces assessment tailored to ON24 that uncovers competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and highlights disruptive trends and strategic levers affecting pricing, market share, and profitability.

A concise Porter's Five Forces one-sheet for ON24 that highlights competitive pressures and relieves decision-making pain by visualizing threat levels and action priorities—easy to customize, copy into decks, and update as market conditions change.

Customers Bargaining Power

Enterprise procurement leverage

ON24 sells to marketing and sales organizations with formal procurement, where large buyers leverage volume to secure discounts typically in the 10–25% range and negotiated service-level terms; competitive RFPs and bids further intensify pricing pressure. Multi-year contracts are common, trading lower annual pricing for retention and reduced churn, aligning with enterprise procurement priorities in 2024.

Switching costs vary by integration depth

Light users can shift to rivals with minimal friction, keeping buyer power high for simple webinar use cases; 2024 surveys show about 54% of buyers favor low-cost, standalone tools. Deep integrations, data pipelines, and custom workflows raise switching costs and lower buyer power for embedded deployments. ON24’s analytics and content hubs increase stickiness, often reducing churn by roughly 20% in integrated accounts.

Abundant alternatives and price sensitivity

Buyers routinely compare ON24 with Zoom, Teams, Webex and dedicated event platforms, intensifying switching options. Economic cycles increase scrutiny on ROI and seat utilization, tightening procurement. Freemium tiers and bundled UCaaS offerings anchor lower price expectations; Zoom reported 300 million daily meeting participants in 2020, highlighting alternative scale and elevating buyer bargaining power.

Demand for measurable ROI

Customers demand conversion lift, attribution, and sales acceleration; Gartner 2024 found 64% of B2B buyers require clear ROI proof, so ON24s strong analytics that drive measurable lift justify premium pricing and lower churn, while weak outcomes trigger renegotiation or switching; value proof therefore directly reduces buyer power.

- ROI focus: 64% (Gartner 2024)

- Price leverage: analytics = premium retention

- Risk: poor outcomes → churn/renegotiation

Global support and reliability expectations

Enterprises typically demand uptime SLAs of 99.9% or higher, global delivery and compliance assurances; failures commonly trigger service credits or contract terminations. Buyers leverage SLAs to extract price or support concessions, while demonstrable superior reliability reduces the need for such concessions and lowers churn risk.

- 99.9%+ uptime standard

- Service credits or exits on breach

- SLAs used as negotiation levers

- Higher reliability = fewer concessions

Buyers leverage: 10-25% cuts; 64% need ROI; 99.9%+ SLA

Buyers hold strong leverage: large deals secure 10–25% discounts and SLAs drive concessions; 54% favored low-cost tools in 2024. Integrations, analytics and content hubs cut churn ~20% and support premium pricing; 64% require clear ROI (Gartner 2024). 99.9%+ uptime expectations lower buyer power.

| Metric | Value |

|---|---|

| ROI requirement | 64% |

| Low-cost preference | 54% |

| Churn reduction (integrated) | ~20% |

| Uptime SLA | 99.9%+ |

Full Version Awaits

ON24 Porter's Five Forces Analysis

This ON24 Porter's Five Forces Analysis preview is the exact, fully formatted document you’ll receive instantly after purchase—no mockups, no placeholders. It contains the complete competitive assessment, strategic implications, and actionable insights ready for download and use. What you see here is precisely the deliverable you’ll get upon payment.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

ON24 faces moderate supplier power, high buyer expectations for sophisticated digital event platforms, intense rivalry among webinar and virtual-event providers, low immediate substitute risk but growing pressure from free conferencing tools, and moderate barriers to entry. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ON24’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud and CDN concentration

ON24 depends on a small set of hyperscalers (AWS, Microsoft Azure, Google Cloud) and major CDNs (Akamai, Cloudflare) for compute, storage and delivery; the top three cloud providers held roughly 65% of the global IaaS/PaaS market in 2024 (Gartner). Multi‑cloud deployment and volume commitments can reduce supplier leverage, but major outages or abrupt price changes still risk materially harming margins and SLA delivery.

Critical video and data tooling

Encoding, streaming SDKs, and analytics for ON24 are sourced from specialized vendors, creating high switching costs given limited high-quality alternatives and proprietary features. Open-source WebRTC and analytics libraries exist and in 2024 serve 1B+ monthly users but require significant integration and support resources. This supplier dependence strengthens vendor negotiation power, especially during contract renewals and price resets.

Integration partners and platforms

Deep integrations with CRM/MA platforms like Salesforce and Marketo are essential for ON24; ON24 lists native connectors to both on its integrations page. Salesforce held roughly 24% of the global CRM market in 2023 (IDC), making it a key gatekeeper. Platform policies, APIs and marketplace economics (e.g., listing and integration requirements) shift margins, and certification/co-sell programs add compliance costs, so gatekeepers wield moderate power.

Security, compliance, and privacy vendors

Enterprise deals force ON24 to embed third-party security tools and identity/compliance frameworks; certifications like SOC 2 (readiness plus audit commonly $50,000–200,000) and ISO audits ($20,000–100,000) require external auditors and services, while GDPR carries fines up to €20 million or 4% of global turnover; these costs and mandatory status reduce flexibility and increase supplier leverage.

- Third-party tooling: must-have for enterprise sales

- Certification costs: SOC 2 $50k–200k; ISO $20k–100k

- Regulatory risk: GDPR fines up to €20M or 4% turnover

Specialized talent and services

Skilled cloud, data, and video engineers remain scarce, giving labor markets cyclic pricing power that can drive wage and contract cost volatility for ON24; event production partners provide scalable capacity but are largely substitutable, limiting long-term supplier leverage. Retention programs reduce attrition risk yet materially raise operating expenses and total cost of ownership.

- Skilled talent scarcity: high hiring competition

- Labor markets: cyclical pricing power

- Event partners: add capacity but substitutable

- Retention programs: lower risk, raise OPEX

Cloud and CRM concentration raise switching costs, outage risk and talent-driven wage pressure

ON24 faces concentrated supplier power from top hyperscalers (top three IaaS/PaaS ~65% global share in 2024, Gartner), CDNs and specialist streaming vendors, raising switching costs and outage/price-change risk; CRM gatekeepers (Salesforce ~24% CRM share, IDC 2023) and mandatory compliance/vendors (SOC 2, ISO) further constrain flexibility; skilled talent scarcity adds wage pressure and vendor leverage.

| Supplier | Metric | 2024/Latest |

|---|---|---|

| Top cloud providers | Top-3 IaaS/PaaS share | ~65% (Gartner 2024) |

| Salesforce | CRM market share | ~24% (IDC 2023) |

| Compliance | SOC 2 audit cost | $50k–$200k |

| Regulatory | GDPR fine | €20M or 4% turnover |

What is included in the product

Comprehensive Porter's Five Forces assessment tailored to ON24 that uncovers competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and highlights disruptive trends and strategic levers affecting pricing, market share, and profitability.

A concise Porter's Five Forces one-sheet for ON24 that highlights competitive pressures and relieves decision-making pain by visualizing threat levels and action priorities—easy to customize, copy into decks, and update as market conditions change.

Customers Bargaining Power

Enterprise procurement leverage

ON24 sells to marketing and sales organizations with formal procurement, where large buyers leverage volume to secure discounts typically in the 10–25% range and negotiated service-level terms; competitive RFPs and bids further intensify pricing pressure. Multi-year contracts are common, trading lower annual pricing for retention and reduced churn, aligning with enterprise procurement priorities in 2024.

Switching costs vary by integration depth

Light users can shift to rivals with minimal friction, keeping buyer power high for simple webinar use cases; 2024 surveys show about 54% of buyers favor low-cost, standalone tools. Deep integrations, data pipelines, and custom workflows raise switching costs and lower buyer power for embedded deployments. ON24’s analytics and content hubs increase stickiness, often reducing churn by roughly 20% in integrated accounts.

Abundant alternatives and price sensitivity

Buyers routinely compare ON24 with Zoom, Teams, Webex and dedicated event platforms, intensifying switching options. Economic cycles increase scrutiny on ROI and seat utilization, tightening procurement. Freemium tiers and bundled UCaaS offerings anchor lower price expectations; Zoom reported 300 million daily meeting participants in 2020, highlighting alternative scale and elevating buyer bargaining power.

Demand for measurable ROI

Customers demand conversion lift, attribution, and sales acceleration; Gartner 2024 found 64% of B2B buyers require clear ROI proof, so ON24s strong analytics that drive measurable lift justify premium pricing and lower churn, while weak outcomes trigger renegotiation or switching; value proof therefore directly reduces buyer power.

- ROI focus: 64% (Gartner 2024)

- Price leverage: analytics = premium retention

- Risk: poor outcomes → churn/renegotiation

Global support and reliability expectations

Enterprises typically demand uptime SLAs of 99.9% or higher, global delivery and compliance assurances; failures commonly trigger service credits or contract terminations. Buyers leverage SLAs to extract price or support concessions, while demonstrable superior reliability reduces the need for such concessions and lowers churn risk.

- 99.9%+ uptime standard

- Service credits or exits on breach

- SLAs used as negotiation levers

- Higher reliability = fewer concessions

Buyers leverage: 10-25% cuts; 64% need ROI; 99.9%+ SLA

Buyers hold strong leverage: large deals secure 10–25% discounts and SLAs drive concessions; 54% favored low-cost tools in 2024. Integrations, analytics and content hubs cut churn ~20% and support premium pricing; 64% require clear ROI (Gartner 2024). 99.9%+ uptime expectations lower buyer power.

| Metric | Value |

|---|---|

| ROI requirement | 64% |

| Low-cost preference | 54% |

| Churn reduction (integrated) | ~20% |

| Uptime SLA | 99.9%+ |

Full Version Awaits

ON24 Porter's Five Forces Analysis

This ON24 Porter's Five Forces Analysis preview is the exact, fully formatted document you’ll receive instantly after purchase—no mockups, no placeholders. It contains the complete competitive assessment, strategic implications, and actionable insights ready for download and use. What you see here is precisely the deliverable you’ll get upon payment.