Ontex Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Ontex Group faces intense rivalry in mature personal-hygiene markets, moderate supplier and buyer power driven by private labels, and limited threat from new entrants and substitutes thanks to scale, brands and regulation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ontex Group’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated key inputs

Ontex relies on pulp, superabsorbent polymers, nonwovens, elastics and specialty chemicals sourced from a relatively concentrated global supplier base, which increases supplier leverage in tight 2024 markets.

Dual-sourcing strategies and centralized global procurement reduce but do not remove exposure to price spikes and supply interruption risks.

Any disruption or consolidation among top suppliers in 2024 can transmit higher input costs and margin pressure across Ontex’s product portfolio.

Commodity price volatility

In 2024 input costs for Ontex—pulp, oil-derivatives and energy—remained cyclical and volatile, materially influencing unit economics. Suppliers typically pass cost increases through quickly while downward adjustments lag, squeezing margins. Hedging and long-term contracts mitigate but do not eliminate short-term spikes. Persistent volatility forces pricing actions that can meet buyer resistance.

Switching costs and qualification

Material changes require qualification, line recalibration and quality audits that create moderate switching costs—approval cycles often span weeks and can delay supply changes; this technical specificity gave approved suppliers bargaining room in 2024, despite standardized specs enabling competitive bidding in parts of the category. Ontex’s ~€1.5bn scale in 2024 strengthens negotiation leverage but does not fully commoditize unique materials.

Sustainability and compliance constraints

Sustainability certifications like FSC and PEFC, strict chemical compliance and ESG traceability requirements narrow Ontexs eligible supplier pool, increasing reliance on certified sources.

Fewer compliant suppliers can heighten supplier bargaining power and raise input prices as eco-design goals push demand for newer, premium materials.

Long-term supplier collaboration and co-innovation can reduce cost-to-serve by improving yield, materials efficiency and joint process optimization.

- Certified supply constraints

- Higher supplier leverage

- Premium input necessity

- Co-innovation lowers costs

Logistics and regionalization

Logistics and regionalization drive supplier bargaining power for Ontex as transportation can add roughly 10-15% to landed costs and geopolitics (tariffs, border delays) raise unpredictability in 2024. Nearshoring improves reliability and cuts lead times, but regional supplier proximity reduces optionality and can increase supplier leverage when local capacity adjoins Ontex plants. Ontexs diversified footprint mitigates, but does not eliminate, regional shocks.

- Transport adds ~10-15% to landed cost

- Nearshoring shortens lead times but limits supplier choice

- Local plants near Ontex increase supplier leverage

- Geopolitical delays remain a 2024 risk; diversification only partially offsets shocks

Supplier concentration squeezes margins; logistics add 10-15%

Ontex faces elevated supplier bargaining power in 2024 due to a concentrated global supplier base for pulp, SAP, nonwovens and specialty chemicals, with input cost volatility materially squeezing margins. Dual sourcing, hedging and €1.5bn scale improve leverage but cannot eliminate price pass-through and certification-driven supplier constraints. Logistics add ~10-15% to landed cost, amplifying regional supplier power.

| Metric | 2024 value/note |

|---|---|

| Ontex revenue scale | ~€1.5bn |

| Transport add to landed cost | ~10-15% |

| Certification impact | Reduces eligible supplier pool (FSC/PEFC/ESG) |

What is included in the product

Tailored Porter's Five Forces analysis for Ontex Group uncovering competitive intensity, buyer/supplier leverage, substitution threats, and entry barriers specific to personal-care manufacturing. Identifies disruptive trends, pricing pressures, and strategic levers to protect market share and inform investor or management decisions.

A concise one-sheet Porter's Five Forces snapshot for Ontex Group that clarifies supplier/buyer power, private-label threats and regulatory pressure for quick strategic decisions. Ease customization of force levels and export-ready layout—drop straight into pitch decks or boardroom briefs.

Customers Bargaining Power

Retail private label leverage

Large retailers drive hard tenders for private label, forcing steep price concessions and compressing Ontex margins; their shelf control enforces strict delivery SLAs with penalties for non-compliance or delays. Multi-year private-label contracts secure volume but lock in low margins. Retailers’ ability to switch suppliers quickly—aided by category managers and centralized buying—keeps customer bargaining power high.

Consumer price sensitivity

Diapers, femcare and incontinence products are high-frequency buys with clear price visibility, and shoppers increasingly traded down during 2022–23 inflation waves, boosting private-label penetration (reaching roughly 40–45% in parts of Europe in 2023 per market reports).

Low end-user switching costs

Low end-user switching costs mean consumers swap brands with minimal effort in baby and femcare; online reviews and e-commerce comparisons (used by ~60% of shoppers in 2024) further lower friction. Performance parity among mid-tier products reduces differentiation, while subscription models can cut churn but are easily replicated, limiting long-term loyalty despite Ontex reporting ~€1.6bn revenue in 2024.

Retail consolidation and omnichannel

Consolidated modern trade in Europe concentrates buying power, with the top retailers accounting for roughly 50% of grocery retail sales in 2024, increasing negotiation leverage over suppliers like Ontex.

Discounters and marketplaces intensify price benchmarking; Western European discounters held about 20% market share in 2024, pressuring promo and margin dynamics.

Omnichannel fulfillment demands service-level excellence and data sharing, while OTIF failures and chargebacks—commonly 1–3% of invoice value in 2024—raise supplier compliance costs.

- Retail concentration ~50% (2024)

- Discounters ~20% share (2024)

- OTIF/chargebacks 1–3% of invoices (2024)

Institutional and B2B tenders

Healthcare and eldercare buyers route adult-care purchases through competitive institutional and B2B tenders that prioritize tight price bands alongside strict quality and specification compliance, concentrating buying power and pressuring supplier margins.

- Multi-year awards can create sudden volume swings for suppliers

- Compliance standards raise entry costs but enable apples-to-apples evaluation

- Win/loss outcomes drive rapid customer switching and strengthen buyer leverage

Retail consolidation, e-commerce and discounters drive private‑label surge and margin pressure

Large European retailers (≈50% market share in 2024) and 20% discounters force heavy private-label tenders, compressing Ontex margins and enforcing strict OTIF/chargebacks (~1–3% of invoice). Low consumer switching costs and ~60% e-commerce influence in 2024 raise price sensitivity and private-label penetration (~40–45%). Healthcare B2B tenders further centralize buying and pressure pricing.

| Metric | 2024 |

|---|---|

| Retail concentration | ≈50% |

| Discounters | ≈20% |

| OTIF/chargebacks | 1–3% invoices |

| E‑commerce influence | ≈60% |

| Private‑label share | ≈40–45% |

What You See Is What You Get

Ontex Group Porter's Five Forces Analysis

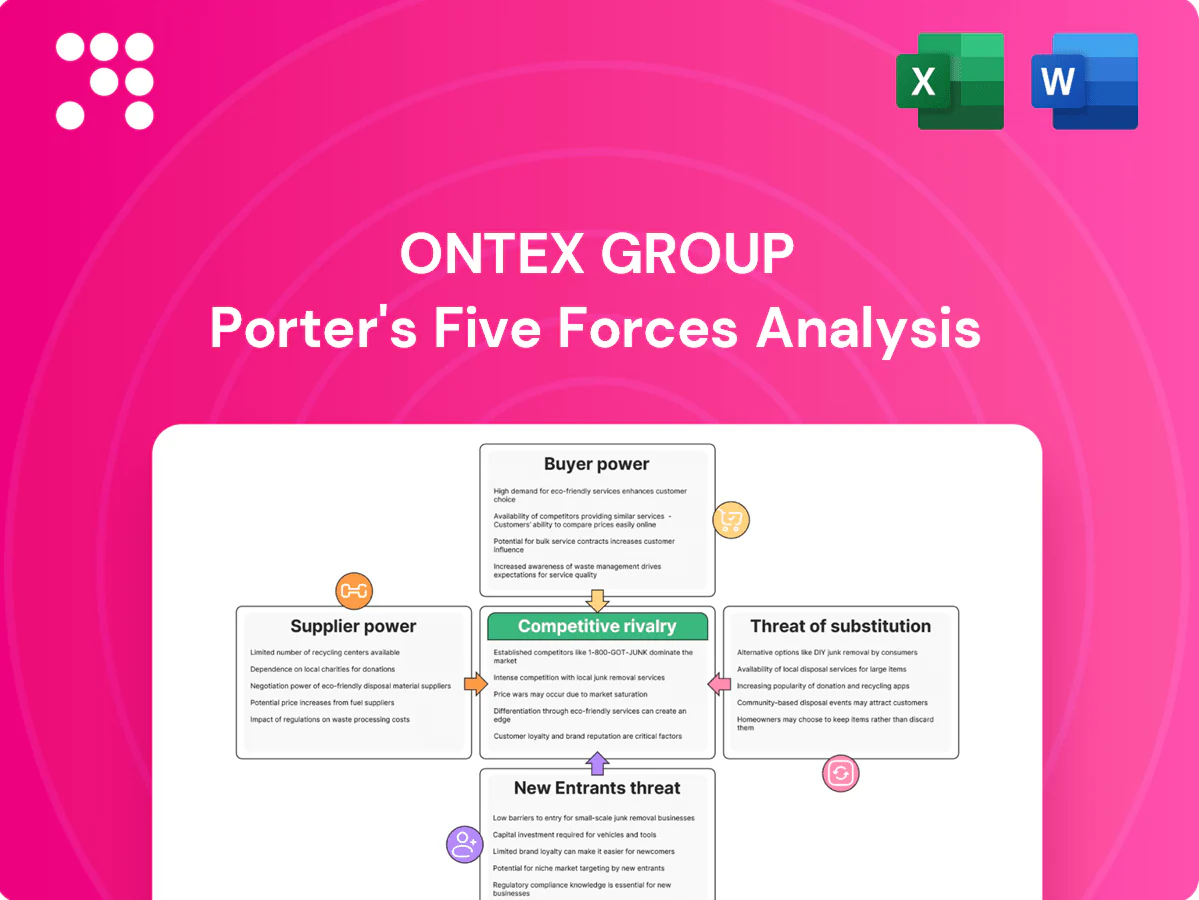

This Ontex Group Porter's Five Forces Analysis offers a concise assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to inform strategic decisions and valuation. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use. It’s the exact file available for immediate download after purchase.

Go Beyond the Preview—Access the Full Strategic Report

Ontex Group faces intense rivalry in mature personal-hygiene markets, moderate supplier and buyer power driven by private labels, and limited threat from new entrants and substitutes thanks to scale, brands and regulation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ontex Group’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated key inputs

Ontex relies on pulp, superabsorbent polymers, nonwovens, elastics and specialty chemicals sourced from a relatively concentrated global supplier base, which increases supplier leverage in tight 2024 markets.

Dual-sourcing strategies and centralized global procurement reduce but do not remove exposure to price spikes and supply interruption risks.

Any disruption or consolidation among top suppliers in 2024 can transmit higher input costs and margin pressure across Ontex’s product portfolio.

Commodity price volatility

In 2024 input costs for Ontex—pulp, oil-derivatives and energy—remained cyclical and volatile, materially influencing unit economics. Suppliers typically pass cost increases through quickly while downward adjustments lag, squeezing margins. Hedging and long-term contracts mitigate but do not eliminate short-term spikes. Persistent volatility forces pricing actions that can meet buyer resistance.

Switching costs and qualification

Material changes require qualification, line recalibration and quality audits that create moderate switching costs—approval cycles often span weeks and can delay supply changes; this technical specificity gave approved suppliers bargaining room in 2024, despite standardized specs enabling competitive bidding in parts of the category. Ontex’s ~€1.5bn scale in 2024 strengthens negotiation leverage but does not fully commoditize unique materials.

Sustainability and compliance constraints

Sustainability certifications like FSC and PEFC, strict chemical compliance and ESG traceability requirements narrow Ontexs eligible supplier pool, increasing reliance on certified sources.

Fewer compliant suppliers can heighten supplier bargaining power and raise input prices as eco-design goals push demand for newer, premium materials.

Long-term supplier collaboration and co-innovation can reduce cost-to-serve by improving yield, materials efficiency and joint process optimization.

- Certified supply constraints

- Higher supplier leverage

- Premium input necessity

- Co-innovation lowers costs

Logistics and regionalization

Logistics and regionalization drive supplier bargaining power for Ontex as transportation can add roughly 10-15% to landed costs and geopolitics (tariffs, border delays) raise unpredictability in 2024. Nearshoring improves reliability and cuts lead times, but regional supplier proximity reduces optionality and can increase supplier leverage when local capacity adjoins Ontex plants. Ontexs diversified footprint mitigates, but does not eliminate, regional shocks.

- Transport adds ~10-15% to landed cost

- Nearshoring shortens lead times but limits supplier choice

- Local plants near Ontex increase supplier leverage

- Geopolitical delays remain a 2024 risk; diversification only partially offsets shocks

Supplier concentration squeezes margins; logistics add 10-15%

Ontex faces elevated supplier bargaining power in 2024 due to a concentrated global supplier base for pulp, SAP, nonwovens and specialty chemicals, with input cost volatility materially squeezing margins. Dual sourcing, hedging and €1.5bn scale improve leverage but cannot eliminate price pass-through and certification-driven supplier constraints. Logistics add ~10-15% to landed cost, amplifying regional supplier power.

| Metric | 2024 value/note |

|---|---|

| Ontex revenue scale | ~€1.5bn |

| Transport add to landed cost | ~10-15% |

| Certification impact | Reduces eligible supplier pool (FSC/PEFC/ESG) |

What is included in the product

Tailored Porter's Five Forces analysis for Ontex Group uncovering competitive intensity, buyer/supplier leverage, substitution threats, and entry barriers specific to personal-care manufacturing. Identifies disruptive trends, pricing pressures, and strategic levers to protect market share and inform investor or management decisions.

A concise one-sheet Porter's Five Forces snapshot for Ontex Group that clarifies supplier/buyer power, private-label threats and regulatory pressure for quick strategic decisions. Ease customization of force levels and export-ready layout—drop straight into pitch decks or boardroom briefs.

Customers Bargaining Power

Retail private label leverage

Large retailers drive hard tenders for private label, forcing steep price concessions and compressing Ontex margins; their shelf control enforces strict delivery SLAs with penalties for non-compliance or delays. Multi-year private-label contracts secure volume but lock in low margins. Retailers’ ability to switch suppliers quickly—aided by category managers and centralized buying—keeps customer bargaining power high.

Consumer price sensitivity

Diapers, femcare and incontinence products are high-frequency buys with clear price visibility, and shoppers increasingly traded down during 2022–23 inflation waves, boosting private-label penetration (reaching roughly 40–45% in parts of Europe in 2023 per market reports).

Low end-user switching costs

Low end-user switching costs mean consumers swap brands with minimal effort in baby and femcare; online reviews and e-commerce comparisons (used by ~60% of shoppers in 2024) further lower friction. Performance parity among mid-tier products reduces differentiation, while subscription models can cut churn but are easily replicated, limiting long-term loyalty despite Ontex reporting ~€1.6bn revenue in 2024.

Retail consolidation and omnichannel

Consolidated modern trade in Europe concentrates buying power, with the top retailers accounting for roughly 50% of grocery retail sales in 2024, increasing negotiation leverage over suppliers like Ontex.

Discounters and marketplaces intensify price benchmarking; Western European discounters held about 20% market share in 2024, pressuring promo and margin dynamics.

Omnichannel fulfillment demands service-level excellence and data sharing, while OTIF failures and chargebacks—commonly 1–3% of invoice value in 2024—raise supplier compliance costs.

- Retail concentration ~50% (2024)

- Discounters ~20% share (2024)

- OTIF/chargebacks 1–3% of invoices (2024)

Institutional and B2B tenders

Healthcare and eldercare buyers route adult-care purchases through competitive institutional and B2B tenders that prioritize tight price bands alongside strict quality and specification compliance, concentrating buying power and pressuring supplier margins.

- Multi-year awards can create sudden volume swings for suppliers

- Compliance standards raise entry costs but enable apples-to-apples evaluation

- Win/loss outcomes drive rapid customer switching and strengthen buyer leverage

Retail consolidation, e-commerce and discounters drive private‑label surge and margin pressure

Large European retailers (≈50% market share in 2024) and 20% discounters force heavy private-label tenders, compressing Ontex margins and enforcing strict OTIF/chargebacks (~1–3% of invoice). Low consumer switching costs and ~60% e-commerce influence in 2024 raise price sensitivity and private-label penetration (~40–45%). Healthcare B2B tenders further centralize buying and pressure pricing.

| Metric | 2024 |

|---|---|

| Retail concentration | ≈50% |

| Discounters | ≈20% |

| OTIF/chargebacks | 1–3% invoices |

| E‑commerce influence | ≈60% |

| Private‑label share | ≈40–45% |

What You See Is What You Get

Ontex Group Porter's Five Forces Analysis

This Ontex Group Porter's Five Forces Analysis offers a concise assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to inform strategic decisions and valuation. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use. It’s the exact file available for immediate download after purchase.

Description

Go Beyond the Preview—Access the Full Strategic Report

Ontex Group faces intense rivalry in mature personal-hygiene markets, moderate supplier and buyer power driven by private labels, and limited threat from new entrants and substitutes thanks to scale, brands and regulation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ontex Group’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated key inputs

Ontex relies on pulp, superabsorbent polymers, nonwovens, elastics and specialty chemicals sourced from a relatively concentrated global supplier base, which increases supplier leverage in tight 2024 markets.

Dual-sourcing strategies and centralized global procurement reduce but do not remove exposure to price spikes and supply interruption risks.

Any disruption or consolidation among top suppliers in 2024 can transmit higher input costs and margin pressure across Ontex’s product portfolio.

Commodity price volatility

In 2024 input costs for Ontex—pulp, oil-derivatives and energy—remained cyclical and volatile, materially influencing unit economics. Suppliers typically pass cost increases through quickly while downward adjustments lag, squeezing margins. Hedging and long-term contracts mitigate but do not eliminate short-term spikes. Persistent volatility forces pricing actions that can meet buyer resistance.

Switching costs and qualification

Material changes require qualification, line recalibration and quality audits that create moderate switching costs—approval cycles often span weeks and can delay supply changes; this technical specificity gave approved suppliers bargaining room in 2024, despite standardized specs enabling competitive bidding in parts of the category. Ontex’s ~€1.5bn scale in 2024 strengthens negotiation leverage but does not fully commoditize unique materials.

Sustainability and compliance constraints

Sustainability certifications like FSC and PEFC, strict chemical compliance and ESG traceability requirements narrow Ontexs eligible supplier pool, increasing reliance on certified sources.

Fewer compliant suppliers can heighten supplier bargaining power and raise input prices as eco-design goals push demand for newer, premium materials.

Long-term supplier collaboration and co-innovation can reduce cost-to-serve by improving yield, materials efficiency and joint process optimization.

- Certified supply constraints

- Higher supplier leverage

- Premium input necessity

- Co-innovation lowers costs

Logistics and regionalization

Logistics and regionalization drive supplier bargaining power for Ontex as transportation can add roughly 10-15% to landed costs and geopolitics (tariffs, border delays) raise unpredictability in 2024. Nearshoring improves reliability and cuts lead times, but regional supplier proximity reduces optionality and can increase supplier leverage when local capacity adjoins Ontex plants. Ontexs diversified footprint mitigates, but does not eliminate, regional shocks.

- Transport adds ~10-15% to landed cost

- Nearshoring shortens lead times but limits supplier choice

- Local plants near Ontex increase supplier leverage

- Geopolitical delays remain a 2024 risk; diversification only partially offsets shocks

Supplier concentration squeezes margins; logistics add 10-15%

Ontex faces elevated supplier bargaining power in 2024 due to a concentrated global supplier base for pulp, SAP, nonwovens and specialty chemicals, with input cost volatility materially squeezing margins. Dual sourcing, hedging and €1.5bn scale improve leverage but cannot eliminate price pass-through and certification-driven supplier constraints. Logistics add ~10-15% to landed cost, amplifying regional supplier power.

| Metric | 2024 value/note |

|---|---|

| Ontex revenue scale | ~€1.5bn |

| Transport add to landed cost | ~10-15% |

| Certification impact | Reduces eligible supplier pool (FSC/PEFC/ESG) |

What is included in the product

Tailored Porter's Five Forces analysis for Ontex Group uncovering competitive intensity, buyer/supplier leverage, substitution threats, and entry barriers specific to personal-care manufacturing. Identifies disruptive trends, pricing pressures, and strategic levers to protect market share and inform investor or management decisions.

A concise one-sheet Porter's Five Forces snapshot for Ontex Group that clarifies supplier/buyer power, private-label threats and regulatory pressure for quick strategic decisions. Ease customization of force levels and export-ready layout—drop straight into pitch decks or boardroom briefs.

Customers Bargaining Power

Retail private label leverage

Large retailers drive hard tenders for private label, forcing steep price concessions and compressing Ontex margins; their shelf control enforces strict delivery SLAs with penalties for non-compliance or delays. Multi-year private-label contracts secure volume but lock in low margins. Retailers’ ability to switch suppliers quickly—aided by category managers and centralized buying—keeps customer bargaining power high.

Consumer price sensitivity

Diapers, femcare and incontinence products are high-frequency buys with clear price visibility, and shoppers increasingly traded down during 2022–23 inflation waves, boosting private-label penetration (reaching roughly 40–45% in parts of Europe in 2023 per market reports).

Low end-user switching costs

Low end-user switching costs mean consumers swap brands with minimal effort in baby and femcare; online reviews and e-commerce comparisons (used by ~60% of shoppers in 2024) further lower friction. Performance parity among mid-tier products reduces differentiation, while subscription models can cut churn but are easily replicated, limiting long-term loyalty despite Ontex reporting ~€1.6bn revenue in 2024.

Retail consolidation and omnichannel

Consolidated modern trade in Europe concentrates buying power, with the top retailers accounting for roughly 50% of grocery retail sales in 2024, increasing negotiation leverage over suppliers like Ontex.

Discounters and marketplaces intensify price benchmarking; Western European discounters held about 20% market share in 2024, pressuring promo and margin dynamics.

Omnichannel fulfillment demands service-level excellence and data sharing, while OTIF failures and chargebacks—commonly 1–3% of invoice value in 2024—raise supplier compliance costs.

- Retail concentration ~50% (2024)

- Discounters ~20% share (2024)

- OTIF/chargebacks 1–3% of invoices (2024)

Institutional and B2B tenders

Healthcare and eldercare buyers route adult-care purchases through competitive institutional and B2B tenders that prioritize tight price bands alongside strict quality and specification compliance, concentrating buying power and pressuring supplier margins.

- Multi-year awards can create sudden volume swings for suppliers

- Compliance standards raise entry costs but enable apples-to-apples evaluation

- Win/loss outcomes drive rapid customer switching and strengthen buyer leverage

Retail consolidation, e-commerce and discounters drive private‑label surge and margin pressure

Large European retailers (≈50% market share in 2024) and 20% discounters force heavy private-label tenders, compressing Ontex margins and enforcing strict OTIF/chargebacks (~1–3% of invoice). Low consumer switching costs and ~60% e-commerce influence in 2024 raise price sensitivity and private-label penetration (~40–45%). Healthcare B2B tenders further centralize buying and pressure pricing.

| Metric | 2024 |

|---|---|

| Retail concentration | ≈50% |

| Discounters | ≈20% |

| OTIF/chargebacks | 1–3% invoices |

| E‑commerce influence | ≈60% |

| Private‑label share | ≈40–45% |

What You See Is What You Get

Ontex Group Porter's Five Forces Analysis

This Ontex Group Porter's Five Forces Analysis offers a concise assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to inform strategic decisions and valuation. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use. It’s the exact file available for immediate download after purchase.