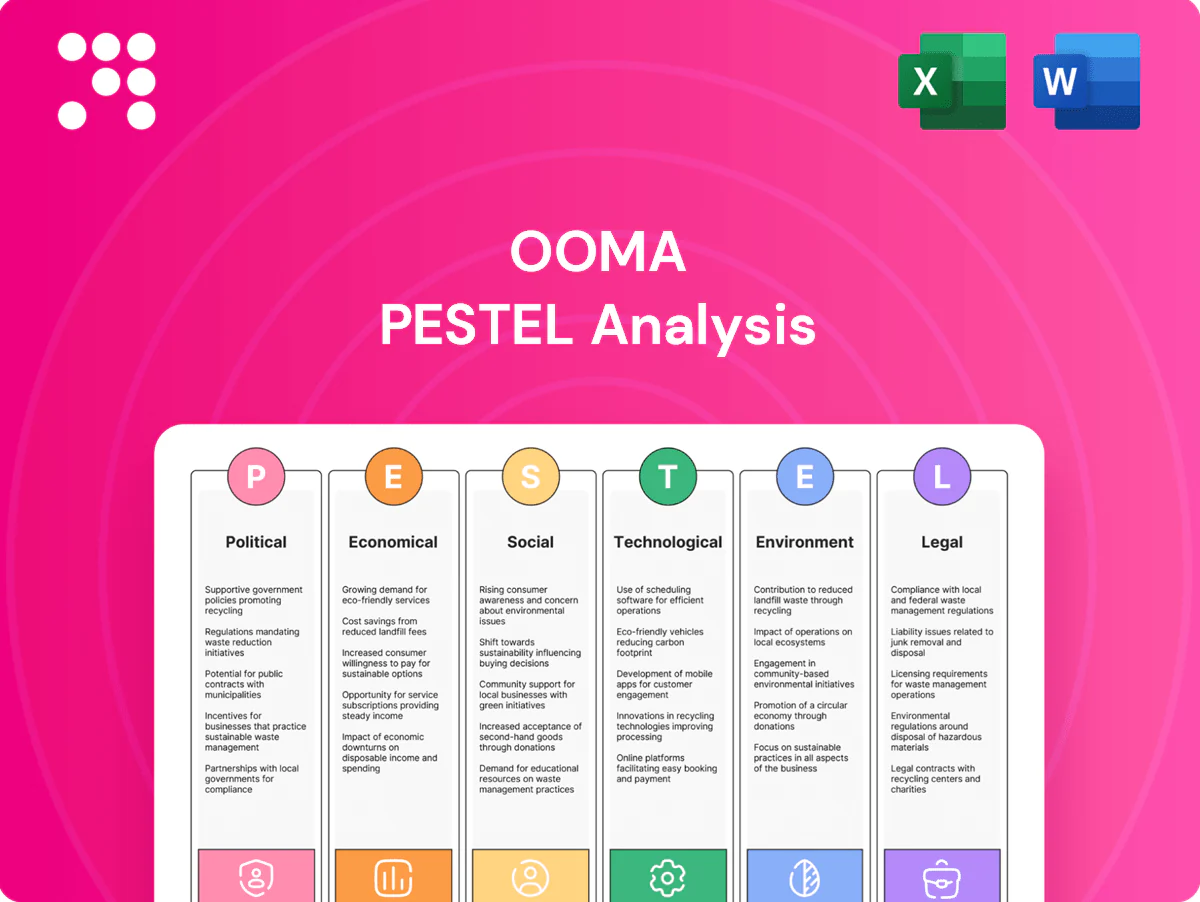

Ooma PESTLE Analysis

Skip the Research. Get the Strategy.

Gain a strategic edge with our PESTLE Analysis of Ooma. We map political, economic, social, technological, legal and environmental forces shaping its outlook. Ideal for investors, consultants and planners seeking actionable insights. Purchase the full report for the complete, ready-to-use breakdown.

Political factors

Telecom and broadband policy

Regulatory stances on VoIP, net neutrality and broadband access directly shape Ooma’s service quality and costs, affecting interconnect and peering expenses and potential liability exposure. The $42.45 billion BEAD program expanding rural broadband can increase Ooma’s addressable market by millions of households (FCC estimated ~14.5M unserved in 2020). Throttling or prioritization rules would alter QoS economics and CAPEX for edge capacity. Continuous monitoring of FCC and global telecom directives is essential.

Data sovereignty and localization

Governments increasingly require local data storage and routing, with over 60 countries having localization rules by 2024, forcing changes to Ooma’s cloud architecture. Compliance can raise infrastructure spend by millions annually and increase operational complexity across regions. Non-compliance risks fines up to 4% of global turnover (GDPR) and possible service restrictions. Strategic regional hosting partnerships can mitigate deployment friction and regulatory risk.

Geopolitical risk and supply chain

Tariffs and export controls, including US Section 301 measures that impose duties up to 25%, raise costs for hardware components used in Ooma devices and can restrict access to key parts. Lead times and procurement costs can spike during geopolitical tensions, squeezing device margins and availability. Diversifying suppliers and nearshoring assembly reduces exposure and shortens replenishment cycles. Rigorous scenario planning preserves service continuity amid supply disruptions.

Public sector procurement

Winning government and education UCaaS deals requires meeting strict security, compliance and procurement standards; accreditation such as FedRAMP and state contract vehicles unlock sticky, multi-year agreements. Ooma reported FY2024 revenue of $183.8M and is targeting public-sector expansion to capture recurring revenue. Budget cycles and political shifts influence timing and size of awards, while dedicated compliance roadmaps measurably improve win rates and shorten sales cycles.

- Security: FedRAMP/state accreditations

- Revenue: Ooma FY2024 $183.8M

- Timing: tied to annual/biannual budget cycles

- Strategy: dedicated compliance roadmap raises win rate

Digital infrastructure investments

National investments in 5G and fiber — supported by the US BEAD program's $42.45 billion broadband funding — strengthen VoIP reliability and video performance, while global 5G connections surpassed 1 billion by end-2023, improving latency and throughput for cloud communications. Improved last-mile connectivity accelerates enterprise and SMB adoption of cloud PBX; policy-driven buildouts can open regions faster and let Ooma align go-to-market with funded rollouts.

- Policy funding: BEAD $42.45B unlocks new markets for Ooma

- Infrastructure impact: 5G >1B connections by 2023 boosts VoIP/video QoS

- Go-to-market: align sales/partner launches with funded buildout timelines

Regulation, localization and tariffs squeeze margins; BEAD $42.45B

Regulatory, trade and procurement policies (BEAD $42.45B, GDPR fines up to 4% revenue) materially affect Ooma’s costs, market access and compliance spend; >60 countries had data localization rules by 2024. US tariffs and export controls raise device costs and lead times, squeezing margins. FedRAMP/state accreditations unlock public-sector revenue (Ooma FY2024 $183.8M).

| Factor | Metric |

|---|---|

| BEAD | $42.45B |

| Localization rules | >60 countries (2024) |

| GDPR fine | Up to 4% global turnover |

| Ooma FY2024 | $183.8M |

What is included in the product

Explores how macro-environmental factors uniquely impact Ooma across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and trend-backed examples tailored to its telecom and cloud-comm markets. Designed for executives and investors, it reflects current regional dynamics and provides forward-looking insights for strategy and risk planning.

A concise, visually segmented PESTLE summary of Ooma that highlights external risks and opportunities for quick reference, easily dropped into presentations or shared across teams to streamline strategic planning.

Economic factors

SMB IT spending cycles

Ooma’s growth is tightly linked to SMB communications budgets given small businesses represent 99.9% of US firms (SBA, 2024). Economic slowdowns historically raise churn and lengthen sales cycles, squeezing 2024 buying windows. Cost-saving pressures push SMBs toward VoIP over legacy PBX, and flexible pricing bundles improve win rates across varied spending cycles.

Inflation and interest rates

Federal Reserve policy rates of roughly 5.25–5.50% (2024–mid‑2025) raise Ooma’s capital costs and compress telecom valuations, while US CPI running near 3–4% in 2024 lifts wages and cloud/hosting expenses. Price increases must balance ARPU gains against churn risk; long‑term customer and vendor contracts hedge cost volatility, and efficiency gains plus renegotiated supplier terms preserve margins.

Broadband availability and pricing

VoIP QoS for Ooma hinges on customers’ internet cost and reliability; in the US the average monthly broadband bill was about $64 in 2023, constraining adoption where service is expensive or unstable. Markets with frequent outages show lower VoIP satisfaction and churn. Strategic ISP partnerships can guarantee QoS, enable bundled discounts and reduce support incidents by clarifying bandwidth requirements.

Currency and international expansion

As Ooma scales abroad, FX volatility—with the USD roughly 5–7% stronger on the trade-weighted DXY in mid-2024—can compress translated revenue and raise local input costs.

Local pricing strategies and hedging programs can stabilize margins, while regional GDP slowdowns or recoveries in 2024–25 reshape demand for business communications.

Phased market entry and distributor models limit capital exposure and operational risk during currency and macro swings.

- FX risk: DXY +5–7% (mid-2024)

- Local pricing/hedging: margin stabilizers

- Phased entry/distributors: risk containment

Competitive pricing pressure

UCaaS and VoIP markets are crowded with low-cost entrants; the global UCaaS market was about $40B in 2024, intensifying price competition. Price wars compress ARPU and force differentiation through richer features and premium support. Bundling video, AI and security helps defend pricing while proactive customer success lowers churn and acquisition costs.

- Market size: ~$40B (2024)

- ARPU pressure: drives feature/support differentiation

- Defense: video, AI, security bundles

- Retention: customer success reduces churn/acquisition spend

Regulation, localization and tariffs squeeze margins; BEAD $42.45B

Ooma’s revenue and churn track SMB budgets—US small firms = 99.9% (SBA, 2024)—so recessions tighten buying windows and lengthen sales cycles. Higher policy rates ~5.25–5.50% (2024–mid‑2025) and CPI ~3–4% raise capital and operating costs, pressuring ARPU. Intense UCaaS competition ($40B global 2024) plus FX swings (DXY +5–7% mid‑2024) force pricing, hedging and bundled feature strategies.

| Metric | Value |

|---|---|

| SMB share (US) | 99.9% (SBA 2024) |

| Fed rates | 5.25–5.50% (2024–mid‑2025) |

| CPI | ~3–4% (2024) |

| UCaaS market | $40B (2024) |

| DXY move | +5–7% (mid‑2024) |

| Avg broadband | $64/mo (US, 2023) |

Same Document Delivered

Ooma PESTLE Analysis

The Ooma PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It delivers a concise review of political, economic, sociocultural, technological, legal, and environmental factors affecting Ooma. The layout, content, and structure visible in this preview are exactly what you’ll download immediately after buying.

Skip the Research. Get the Strategy.

Gain a strategic edge with our PESTLE Analysis of Ooma. We map political, economic, social, technological, legal and environmental forces shaping its outlook. Ideal for investors, consultants and planners seeking actionable insights. Purchase the full report for the complete, ready-to-use breakdown.

Political factors

Telecom and broadband policy

Regulatory stances on VoIP, net neutrality and broadband access directly shape Ooma’s service quality and costs, affecting interconnect and peering expenses and potential liability exposure. The $42.45 billion BEAD program expanding rural broadband can increase Ooma’s addressable market by millions of households (FCC estimated ~14.5M unserved in 2020). Throttling or prioritization rules would alter QoS economics and CAPEX for edge capacity. Continuous monitoring of FCC and global telecom directives is essential.

Data sovereignty and localization

Governments increasingly require local data storage and routing, with over 60 countries having localization rules by 2024, forcing changes to Ooma’s cloud architecture. Compliance can raise infrastructure spend by millions annually and increase operational complexity across regions. Non-compliance risks fines up to 4% of global turnover (GDPR) and possible service restrictions. Strategic regional hosting partnerships can mitigate deployment friction and regulatory risk.

Geopolitical risk and supply chain

Tariffs and export controls, including US Section 301 measures that impose duties up to 25%, raise costs for hardware components used in Ooma devices and can restrict access to key parts. Lead times and procurement costs can spike during geopolitical tensions, squeezing device margins and availability. Diversifying suppliers and nearshoring assembly reduces exposure and shortens replenishment cycles. Rigorous scenario planning preserves service continuity amid supply disruptions.

Public sector procurement

Winning government and education UCaaS deals requires meeting strict security, compliance and procurement standards; accreditation such as FedRAMP and state contract vehicles unlock sticky, multi-year agreements. Ooma reported FY2024 revenue of $183.8M and is targeting public-sector expansion to capture recurring revenue. Budget cycles and political shifts influence timing and size of awards, while dedicated compliance roadmaps measurably improve win rates and shorten sales cycles.

- Security: FedRAMP/state accreditations

- Revenue: Ooma FY2024 $183.8M

- Timing: tied to annual/biannual budget cycles

- Strategy: dedicated compliance roadmap raises win rate

Digital infrastructure investments

National investments in 5G and fiber — supported by the US BEAD program's $42.45 billion broadband funding — strengthen VoIP reliability and video performance, while global 5G connections surpassed 1 billion by end-2023, improving latency and throughput for cloud communications. Improved last-mile connectivity accelerates enterprise and SMB adoption of cloud PBX; policy-driven buildouts can open regions faster and let Ooma align go-to-market with funded rollouts.

- Policy funding: BEAD $42.45B unlocks new markets for Ooma

- Infrastructure impact: 5G >1B connections by 2023 boosts VoIP/video QoS

- Go-to-market: align sales/partner launches with funded buildout timelines

Regulation, localization and tariffs squeeze margins; BEAD $42.45B

Regulatory, trade and procurement policies (BEAD $42.45B, GDPR fines up to 4% revenue) materially affect Ooma’s costs, market access and compliance spend; >60 countries had data localization rules by 2024. US tariffs and export controls raise device costs and lead times, squeezing margins. FedRAMP/state accreditations unlock public-sector revenue (Ooma FY2024 $183.8M).

| Factor | Metric |

|---|---|

| BEAD | $42.45B |

| Localization rules | >60 countries (2024) |

| GDPR fine | Up to 4% global turnover |

| Ooma FY2024 | $183.8M |

What is included in the product

Explores how macro-environmental factors uniquely impact Ooma across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and trend-backed examples tailored to its telecom and cloud-comm markets. Designed for executives and investors, it reflects current regional dynamics and provides forward-looking insights for strategy and risk planning.

A concise, visually segmented PESTLE summary of Ooma that highlights external risks and opportunities for quick reference, easily dropped into presentations or shared across teams to streamline strategic planning.

Economic factors

SMB IT spending cycles

Ooma’s growth is tightly linked to SMB communications budgets given small businesses represent 99.9% of US firms (SBA, 2024). Economic slowdowns historically raise churn and lengthen sales cycles, squeezing 2024 buying windows. Cost-saving pressures push SMBs toward VoIP over legacy PBX, and flexible pricing bundles improve win rates across varied spending cycles.

Inflation and interest rates

Federal Reserve policy rates of roughly 5.25–5.50% (2024–mid‑2025) raise Ooma’s capital costs and compress telecom valuations, while US CPI running near 3–4% in 2024 lifts wages and cloud/hosting expenses. Price increases must balance ARPU gains against churn risk; long‑term customer and vendor contracts hedge cost volatility, and efficiency gains plus renegotiated supplier terms preserve margins.

Broadband availability and pricing

VoIP QoS for Ooma hinges on customers’ internet cost and reliability; in the US the average monthly broadband bill was about $64 in 2023, constraining adoption where service is expensive or unstable. Markets with frequent outages show lower VoIP satisfaction and churn. Strategic ISP partnerships can guarantee QoS, enable bundled discounts and reduce support incidents by clarifying bandwidth requirements.

Currency and international expansion

As Ooma scales abroad, FX volatility—with the USD roughly 5–7% stronger on the trade-weighted DXY in mid-2024—can compress translated revenue and raise local input costs.

Local pricing strategies and hedging programs can stabilize margins, while regional GDP slowdowns or recoveries in 2024–25 reshape demand for business communications.

Phased market entry and distributor models limit capital exposure and operational risk during currency and macro swings.

- FX risk: DXY +5–7% (mid-2024)

- Local pricing/hedging: margin stabilizers

- Phased entry/distributors: risk containment

Competitive pricing pressure

UCaaS and VoIP markets are crowded with low-cost entrants; the global UCaaS market was about $40B in 2024, intensifying price competition. Price wars compress ARPU and force differentiation through richer features and premium support. Bundling video, AI and security helps defend pricing while proactive customer success lowers churn and acquisition costs.

- Market size: ~$40B (2024)

- ARPU pressure: drives feature/support differentiation

- Defense: video, AI, security bundles

- Retention: customer success reduces churn/acquisition spend

Regulation, localization and tariffs squeeze margins; BEAD $42.45B

Ooma’s revenue and churn track SMB budgets—US small firms = 99.9% (SBA, 2024)—so recessions tighten buying windows and lengthen sales cycles. Higher policy rates ~5.25–5.50% (2024–mid‑2025) and CPI ~3–4% raise capital and operating costs, pressuring ARPU. Intense UCaaS competition ($40B global 2024) plus FX swings (DXY +5–7% mid‑2024) force pricing, hedging and bundled feature strategies.

| Metric | Value |

|---|---|

| SMB share (US) | 99.9% (SBA 2024) |

| Fed rates | 5.25–5.50% (2024–mid‑2025) |

| CPI | ~3–4% (2024) |

| UCaaS market | $40B (2024) |

| DXY move | +5–7% (mid‑2024) |

| Avg broadband | $64/mo (US, 2023) |

Same Document Delivered

Ooma PESTLE Analysis

The Ooma PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It delivers a concise review of political, economic, sociocultural, technological, legal, and environmental factors affecting Ooma. The layout, content, and structure visible in this preview are exactly what you’ll download immediately after buying.

Description

Skip the Research. Get the Strategy.

Gain a strategic edge with our PESTLE Analysis of Ooma. We map political, economic, social, technological, legal and environmental forces shaping its outlook. Ideal for investors, consultants and planners seeking actionable insights. Purchase the full report for the complete, ready-to-use breakdown.

Political factors

Telecom and broadband policy

Regulatory stances on VoIP, net neutrality and broadband access directly shape Ooma’s service quality and costs, affecting interconnect and peering expenses and potential liability exposure. The $42.45 billion BEAD program expanding rural broadband can increase Ooma’s addressable market by millions of households (FCC estimated ~14.5M unserved in 2020). Throttling or prioritization rules would alter QoS economics and CAPEX for edge capacity. Continuous monitoring of FCC and global telecom directives is essential.

Data sovereignty and localization

Governments increasingly require local data storage and routing, with over 60 countries having localization rules by 2024, forcing changes to Ooma’s cloud architecture. Compliance can raise infrastructure spend by millions annually and increase operational complexity across regions. Non-compliance risks fines up to 4% of global turnover (GDPR) and possible service restrictions. Strategic regional hosting partnerships can mitigate deployment friction and regulatory risk.

Geopolitical risk and supply chain

Tariffs and export controls, including US Section 301 measures that impose duties up to 25%, raise costs for hardware components used in Ooma devices and can restrict access to key parts. Lead times and procurement costs can spike during geopolitical tensions, squeezing device margins and availability. Diversifying suppliers and nearshoring assembly reduces exposure and shortens replenishment cycles. Rigorous scenario planning preserves service continuity amid supply disruptions.

Public sector procurement

Winning government and education UCaaS deals requires meeting strict security, compliance and procurement standards; accreditation such as FedRAMP and state contract vehicles unlock sticky, multi-year agreements. Ooma reported FY2024 revenue of $183.8M and is targeting public-sector expansion to capture recurring revenue. Budget cycles and political shifts influence timing and size of awards, while dedicated compliance roadmaps measurably improve win rates and shorten sales cycles.

- Security: FedRAMP/state accreditations

- Revenue: Ooma FY2024 $183.8M

- Timing: tied to annual/biannual budget cycles

- Strategy: dedicated compliance roadmap raises win rate

Digital infrastructure investments

National investments in 5G and fiber — supported by the US BEAD program's $42.45 billion broadband funding — strengthen VoIP reliability and video performance, while global 5G connections surpassed 1 billion by end-2023, improving latency and throughput for cloud communications. Improved last-mile connectivity accelerates enterprise and SMB adoption of cloud PBX; policy-driven buildouts can open regions faster and let Ooma align go-to-market with funded rollouts.

- Policy funding: BEAD $42.45B unlocks new markets for Ooma

- Infrastructure impact: 5G >1B connections by 2023 boosts VoIP/video QoS

- Go-to-market: align sales/partner launches with funded buildout timelines

Regulation, localization and tariffs squeeze margins; BEAD $42.45B

Regulatory, trade and procurement policies (BEAD $42.45B, GDPR fines up to 4% revenue) materially affect Ooma’s costs, market access and compliance spend; >60 countries had data localization rules by 2024. US tariffs and export controls raise device costs and lead times, squeezing margins. FedRAMP/state accreditations unlock public-sector revenue (Ooma FY2024 $183.8M).

| Factor | Metric |

|---|---|

| BEAD | $42.45B |

| Localization rules | >60 countries (2024) |

| GDPR fine | Up to 4% global turnover |

| Ooma FY2024 | $183.8M |

What is included in the product

Explores how macro-environmental factors uniquely impact Ooma across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and trend-backed examples tailored to its telecom and cloud-comm markets. Designed for executives and investors, it reflects current regional dynamics and provides forward-looking insights for strategy and risk planning.

A concise, visually segmented PESTLE summary of Ooma that highlights external risks and opportunities for quick reference, easily dropped into presentations or shared across teams to streamline strategic planning.

Economic factors

SMB IT spending cycles

Ooma’s growth is tightly linked to SMB communications budgets given small businesses represent 99.9% of US firms (SBA, 2024). Economic slowdowns historically raise churn and lengthen sales cycles, squeezing 2024 buying windows. Cost-saving pressures push SMBs toward VoIP over legacy PBX, and flexible pricing bundles improve win rates across varied spending cycles.

Inflation and interest rates

Federal Reserve policy rates of roughly 5.25–5.50% (2024–mid‑2025) raise Ooma’s capital costs and compress telecom valuations, while US CPI running near 3–4% in 2024 lifts wages and cloud/hosting expenses. Price increases must balance ARPU gains against churn risk; long‑term customer and vendor contracts hedge cost volatility, and efficiency gains plus renegotiated supplier terms preserve margins.

Broadband availability and pricing

VoIP QoS for Ooma hinges on customers’ internet cost and reliability; in the US the average monthly broadband bill was about $64 in 2023, constraining adoption where service is expensive or unstable. Markets with frequent outages show lower VoIP satisfaction and churn. Strategic ISP partnerships can guarantee QoS, enable bundled discounts and reduce support incidents by clarifying bandwidth requirements.

Currency and international expansion

As Ooma scales abroad, FX volatility—with the USD roughly 5–7% stronger on the trade-weighted DXY in mid-2024—can compress translated revenue and raise local input costs.

Local pricing strategies and hedging programs can stabilize margins, while regional GDP slowdowns or recoveries in 2024–25 reshape demand for business communications.

Phased market entry and distributor models limit capital exposure and operational risk during currency and macro swings.

- FX risk: DXY +5–7% (mid-2024)

- Local pricing/hedging: margin stabilizers

- Phased entry/distributors: risk containment

Competitive pricing pressure

UCaaS and VoIP markets are crowded with low-cost entrants; the global UCaaS market was about $40B in 2024, intensifying price competition. Price wars compress ARPU and force differentiation through richer features and premium support. Bundling video, AI and security helps defend pricing while proactive customer success lowers churn and acquisition costs.

- Market size: ~$40B (2024)

- ARPU pressure: drives feature/support differentiation

- Defense: video, AI, security bundles

- Retention: customer success reduces churn/acquisition spend

Regulation, localization and tariffs squeeze margins; BEAD $42.45B

Ooma’s revenue and churn track SMB budgets—US small firms = 99.9% (SBA, 2024)—so recessions tighten buying windows and lengthen sales cycles. Higher policy rates ~5.25–5.50% (2024–mid‑2025) and CPI ~3–4% raise capital and operating costs, pressuring ARPU. Intense UCaaS competition ($40B global 2024) plus FX swings (DXY +5–7% mid‑2024) force pricing, hedging and bundled feature strategies.

| Metric | Value |

|---|---|

| SMB share (US) | 99.9% (SBA 2024) |

| Fed rates | 5.25–5.50% (2024–mid‑2025) |

| CPI | ~3–4% (2024) |

| UCaaS market | $40B (2024) |

| DXY move | +5–7% (mid‑2024) |

| Avg broadband | $64/mo (US, 2023) |

Same Document Delivered

Ooma PESTLE Analysis

The Ooma PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It delivers a concise review of political, economic, sociocultural, technological, legal, and environmental factors affecting Ooma. The layout, content, and structure visible in this preview are exactly what you’ll download immediately after buying.