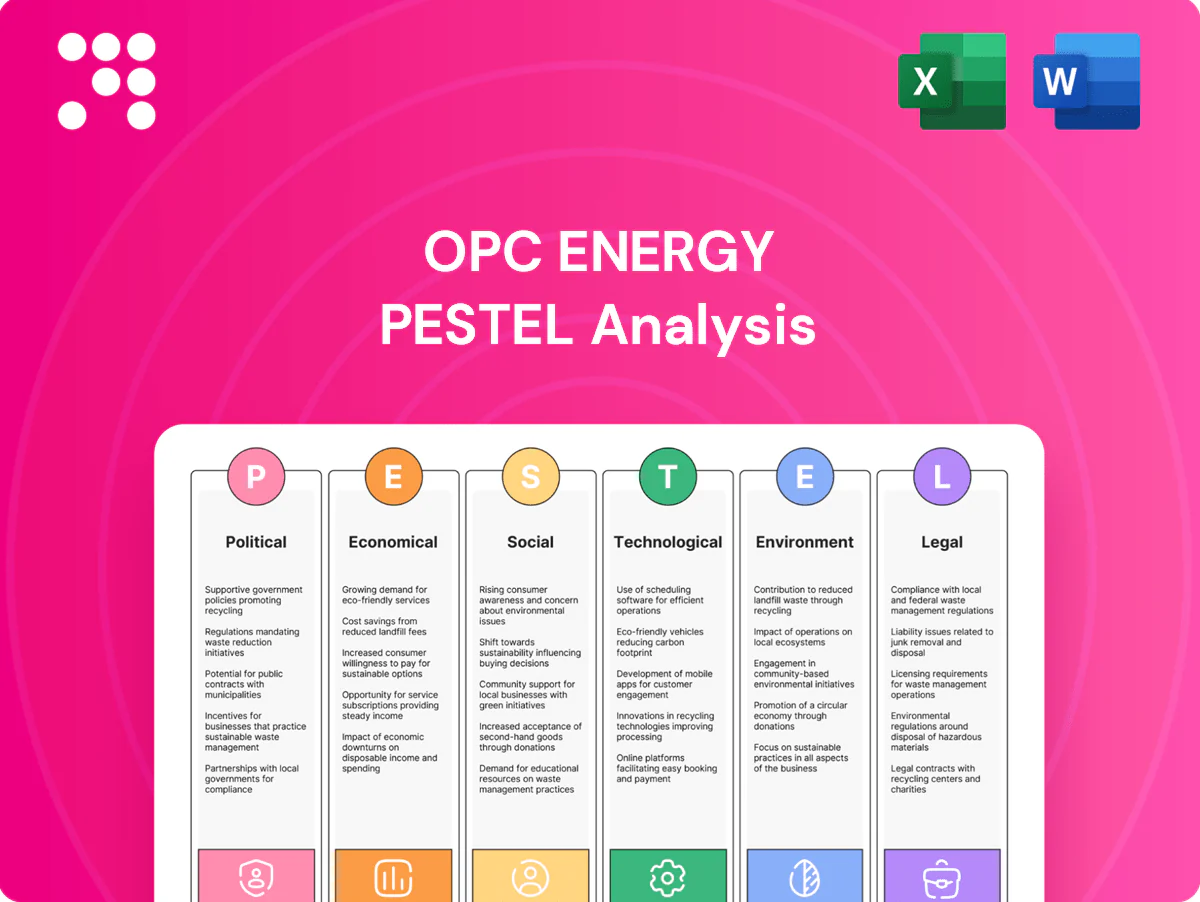

OPC Energy PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, social trends, tech advances, legal shifts, and environmental pressures are shaping OPC Energy’s outlook in our concise PESTLE snapshot—perfect for investors and strategists. Purchase the full analysis for detailed, actionable insights you can deploy immediately.

Political factors

Energy policy and subsidies

Government incentives, carbon pricing, and renewable targets shape OPC’s fuel mix and project pipeline: Israel targets roughly 30% renewable electricity by 2030, while the U.S. Inflation Reduction Act offers up to a 30% investment tax credit for qualifying solar and storage projects. EU ETS carbon prices averaged about €85/ton in 2024, affecting regional gas economics. Policy stability directly influences financing terms and contract tenor, while sudden subsidy or cap reforms can materially change project returns.

Geopolitical and security risk (Israel)

Regional tensions since October 2023 have disrupted supply chains and construction timelines in the Eastern Mediterranean, threatening grid reliability and project schedules. Heightened political-risk premiums have pushed insurers and lenders to tighten terms, increasing project financing costs and necessitating redundancy planning. Government emergency energy measures can reprioritize dispatch and capacity commitments, so continuity plans and site diversification are critical to mitigate operational exposure.

Permitting and siting approvals

National, state and municipal authorities control site licenses, interconnection and environmental clearances, often with separate application paths and criteria. Lengthy review cycles of 18–36 months delay COD and escalate capex; U.S. interconnection backlog exceeded 1,000 GW in 2024, creating queue-driven cost risk. Early stakeholder engagement and regulator alignment reduce objections and rework. Coordinated timelines with grid operators are critical to avoid stranded assets.

Market design and grid operator rules

Capacity payments, ancillary services and dispatch rules set by system operators define OPC Energy revenue stacks; ERCOT scarcity caps at 5,000/MWh (2024) and U.S. reserve margins ~20% (NERC 2024) materially shape realized revenues and volatility.

Changes to scarcity pricing, nodal tariffs or curtailment alter profitability; U.S. interconnection queues exceed 1,000 GW (FERC 2024) while Israel faces constrained queues and higher curtailment risk, so active rulemaking engagement is essential.

- Capacity payments: regional; affect base revenue

- Ancillary services: fast-response value rising

- Scarcity pricing: ERCOT 5,000/MWh cap (2024)

- Queues: U.S. >1,000 GW; Israel: constrained

- Action: participate in rulemaking

Public sector offtake and PPPs

Government entities as customers give creditworthy PPAs that lower commercial risk but raise compliance and procurement complexity; competitive tenders and localization rules increasingly dictate bid structure and supply-chain sourcing. Contract renegotiations or fiscal pressures can compress tariff trajectories and delay collections, while strong relationships with public buyers improve pipeline visibility and de-risk long-term project financing.

- Public offtakers: creditworthy but compliance-heavy

- Tenders/localization: shape bid and capex

- Renegotiation risk: affects tariff paths

- Strong public ties: enhance pipeline visibility

Policy, carbon & grid risk reshape economics: 30% ITC; EU ETS €85/t

Policy incentives, carbon pricing and geopolitical risk materially reshape OPC Energy’s project economics and financing terms. Key levers: Israel 30% renewables by 2030, U.S. IRA up to 30% ITC, EU ETS ~€85/t (2024). Interconnection backlogs (>1,000 GW U.S., FERC 2024) and ERCOT scarcity cap 5,000/MWh (2024) drive queue, curtailment and revenue risk.

| Policy | Metric | Impact |

|---|---|---|

| Renewable targets | Israel 30% by 2030 | Pipeline demand |

| Incentives | IRA up to 30% ITC | Capex reduction |

| Carbon price | EU ETS €85/t (2024) | Fuel shift |

| Queues/scarcity | US >1,000 GW; ERCOT 5,000/MWh | Revenue/curtailment risk |

What is included in the product

Explores how macro-environmental factors uniquely affect OPC Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific regulatory context.

A clean, summarized OPC Energy PESTLE that’s visually segmented by category for quick interpretation at a glance, making it easy to drop into presentations or planning sessions.

Economic factors

Natural gas price volatility

Fuel costs drive OPC’s spark spreads as US Henry Hub gas is roughly 60% below 2022 peaks and global LNG oversupply pushed spot LNG to multi-year lows in 2024, compressing input costs. Regional contracts and Israeli import dynamics still create basis differentials vs US prices. Hedging programs and pass-through clauses in OPC’s PPAs materially stabilize margins. Diversifying into renewables and storage reduces fuel exposure and volatility risk.

Interest rates and capital access

Rising policy rates (Fed funds ~5.25–5.50% through 2024–25) lift WACC and compress equity IRRs for long-lived OPC Energy assets, making returns sensitive to discount-rate shifts. Project finance availability now hinges on contracted cash flows and clear policy pathways for hydrogen/CCS; refinancing windows materially affect portfolio returns. Green bonds and sustainability-linked loans, with global green issuance above $500bn in 2024, can improve pricing.

Electricity demand and load shape

Economic growth, electrification and data center expansion lifted global electricity demand about 2.5% in 2023, with data centers now consuming roughly 1% of global power and hyperscaler buildouts driving local peaks.

Rapid EV and heat‑pump adoption shifts loads into evening and daytime peaks—EV charging could add 5–10% to peak demand in many grids by 2030—creating new dispatch and arbitrage opportunities.

Accurate short‑term and long‑term forecasting is critical: utility‑scale battery additions (tens of GW annually) and capacity procurement hinge on tight load-shape projections, while demand downturns expose merchant generators to revenue risk.

Exchange rate exposure (ILS/USD)

Multi-jurisdiction operations create FX mismatches across revenues, costs and debt for OPC Energy; Bank of Israel data shows USD/ILS averaged about 3.67 in 2024, amplifying translation risk and affecting reported earnings and covenant headroom. Natural hedges and derivatives have reduced P&L volatility historically, while financing in operating currencies aligns cash flows and lowers refinancing risk.

- FX mismatch across revenue, costs, debt

- USD/ILS avg 3.67 in 2024 (Bank of Israel)

- Derivatives and natural hedges cut P&L volatility

- Local-currency financing aligns cash flows, improves covenant headroom

Competition and market entry costs

Crowded interconnection queues (US ~800+ GW reported across RTO filings in 2023–24) and EPC inflation (tenders up ~10–20% vs 2020) raise entry barriers, while rival IPPs, utilities and infrastructure funds compress PPA pricing toward $20–40/MWh in prime US markets. Scale procurement and O&M synergies can recover 5–15% of margin; superior development optionality becomes a key differentiator.

- Interconnection: US ~800+ GW backlog (2023–24)

- EPC inflation: +10–20% vs 2020

- PPA pressure: ~$20–40/MWh in top US markets

- Synergy recovery: 5–15% margin uplift

Policy, carbon & grid risk reshape economics: 30% ITC; EU ETS €85/t

Fuel costs (Henry Hub ~60% below 2022 peaks) and LNG oversupply compress input costs while hedges/PPAs stabilize margins. Rates (Fed funds ~5.25–5.50% 2024–25) raise WACC and pressure returns; green debt market (> $500bn 2024) eases financing. FX (USD/ILS ~3.67 in 2024) and 800+ GW interconnection backlog increase execution risk; PPA pricing compresses to ~$20–40/MWh.

| Metric | Value |

|---|---|

| Henry Hub vs 2022 | -60% |

| Fed funds | 5.25–5.50% |

| Green issuance 2024 | >$500bn |

| USD/ILS 2024 | ~3.67 |

| Interconnection backlog | 800+ GW |

| PPA range | $20–40/MWh |

Same Document Delivered

OPC Energy PESTLE Analysis

The preview shown here is the exact OPC Energy PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The layout, content, and insights visible now are the final file you’ll download immediately after payment. No placeholders, no teasers—this is the real document.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, social trends, tech advances, legal shifts, and environmental pressures are shaping OPC Energy’s outlook in our concise PESTLE snapshot—perfect for investors and strategists. Purchase the full analysis for detailed, actionable insights you can deploy immediately.

Political factors

Energy policy and subsidies

Government incentives, carbon pricing, and renewable targets shape OPC’s fuel mix and project pipeline: Israel targets roughly 30% renewable electricity by 2030, while the U.S. Inflation Reduction Act offers up to a 30% investment tax credit for qualifying solar and storage projects. EU ETS carbon prices averaged about €85/ton in 2024, affecting regional gas economics. Policy stability directly influences financing terms and contract tenor, while sudden subsidy or cap reforms can materially change project returns.

Geopolitical and security risk (Israel)

Regional tensions since October 2023 have disrupted supply chains and construction timelines in the Eastern Mediterranean, threatening grid reliability and project schedules. Heightened political-risk premiums have pushed insurers and lenders to tighten terms, increasing project financing costs and necessitating redundancy planning. Government emergency energy measures can reprioritize dispatch and capacity commitments, so continuity plans and site diversification are critical to mitigate operational exposure.

Permitting and siting approvals

National, state and municipal authorities control site licenses, interconnection and environmental clearances, often with separate application paths and criteria. Lengthy review cycles of 18–36 months delay COD and escalate capex; U.S. interconnection backlog exceeded 1,000 GW in 2024, creating queue-driven cost risk. Early stakeholder engagement and regulator alignment reduce objections and rework. Coordinated timelines with grid operators are critical to avoid stranded assets.

Market design and grid operator rules

Capacity payments, ancillary services and dispatch rules set by system operators define OPC Energy revenue stacks; ERCOT scarcity caps at 5,000/MWh (2024) and U.S. reserve margins ~20% (NERC 2024) materially shape realized revenues and volatility.

Changes to scarcity pricing, nodal tariffs or curtailment alter profitability; U.S. interconnection queues exceed 1,000 GW (FERC 2024) while Israel faces constrained queues and higher curtailment risk, so active rulemaking engagement is essential.

- Capacity payments: regional; affect base revenue

- Ancillary services: fast-response value rising

- Scarcity pricing: ERCOT 5,000/MWh cap (2024)

- Queues: U.S. >1,000 GW; Israel: constrained

- Action: participate in rulemaking

Public sector offtake and PPPs

Government entities as customers give creditworthy PPAs that lower commercial risk but raise compliance and procurement complexity; competitive tenders and localization rules increasingly dictate bid structure and supply-chain sourcing. Contract renegotiations or fiscal pressures can compress tariff trajectories and delay collections, while strong relationships with public buyers improve pipeline visibility and de-risk long-term project financing.

- Public offtakers: creditworthy but compliance-heavy

- Tenders/localization: shape bid and capex

- Renegotiation risk: affects tariff paths

- Strong public ties: enhance pipeline visibility

Policy, carbon & grid risk reshape economics: 30% ITC; EU ETS €85/t

Policy incentives, carbon pricing and geopolitical risk materially reshape OPC Energy’s project economics and financing terms. Key levers: Israel 30% renewables by 2030, U.S. IRA up to 30% ITC, EU ETS ~€85/t (2024). Interconnection backlogs (>1,000 GW U.S., FERC 2024) and ERCOT scarcity cap 5,000/MWh (2024) drive queue, curtailment and revenue risk.

| Policy | Metric | Impact |

|---|---|---|

| Renewable targets | Israel 30% by 2030 | Pipeline demand |

| Incentives | IRA up to 30% ITC | Capex reduction |

| Carbon price | EU ETS €85/t (2024) | Fuel shift |

| Queues/scarcity | US >1,000 GW; ERCOT 5,000/MWh | Revenue/curtailment risk |

What is included in the product

Explores how macro-environmental factors uniquely affect OPC Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific regulatory context.

A clean, summarized OPC Energy PESTLE that’s visually segmented by category for quick interpretation at a glance, making it easy to drop into presentations or planning sessions.

Economic factors

Natural gas price volatility

Fuel costs drive OPC’s spark spreads as US Henry Hub gas is roughly 60% below 2022 peaks and global LNG oversupply pushed spot LNG to multi-year lows in 2024, compressing input costs. Regional contracts and Israeli import dynamics still create basis differentials vs US prices. Hedging programs and pass-through clauses in OPC’s PPAs materially stabilize margins. Diversifying into renewables and storage reduces fuel exposure and volatility risk.

Interest rates and capital access

Rising policy rates (Fed funds ~5.25–5.50% through 2024–25) lift WACC and compress equity IRRs for long-lived OPC Energy assets, making returns sensitive to discount-rate shifts. Project finance availability now hinges on contracted cash flows and clear policy pathways for hydrogen/CCS; refinancing windows materially affect portfolio returns. Green bonds and sustainability-linked loans, with global green issuance above $500bn in 2024, can improve pricing.

Electricity demand and load shape

Economic growth, electrification and data center expansion lifted global electricity demand about 2.5% in 2023, with data centers now consuming roughly 1% of global power and hyperscaler buildouts driving local peaks.

Rapid EV and heat‑pump adoption shifts loads into evening and daytime peaks—EV charging could add 5–10% to peak demand in many grids by 2030—creating new dispatch and arbitrage opportunities.

Accurate short‑term and long‑term forecasting is critical: utility‑scale battery additions (tens of GW annually) and capacity procurement hinge on tight load-shape projections, while demand downturns expose merchant generators to revenue risk.

Exchange rate exposure (ILS/USD)

Multi-jurisdiction operations create FX mismatches across revenues, costs and debt for OPC Energy; Bank of Israel data shows USD/ILS averaged about 3.67 in 2024, amplifying translation risk and affecting reported earnings and covenant headroom. Natural hedges and derivatives have reduced P&L volatility historically, while financing in operating currencies aligns cash flows and lowers refinancing risk.

- FX mismatch across revenue, costs, debt

- USD/ILS avg 3.67 in 2024 (Bank of Israel)

- Derivatives and natural hedges cut P&L volatility

- Local-currency financing aligns cash flows, improves covenant headroom

Competition and market entry costs

Crowded interconnection queues (US ~800+ GW reported across RTO filings in 2023–24) and EPC inflation (tenders up ~10–20% vs 2020) raise entry barriers, while rival IPPs, utilities and infrastructure funds compress PPA pricing toward $20–40/MWh in prime US markets. Scale procurement and O&M synergies can recover 5–15% of margin; superior development optionality becomes a key differentiator.

- Interconnection: US ~800+ GW backlog (2023–24)

- EPC inflation: +10–20% vs 2020

- PPA pressure: ~$20–40/MWh in top US markets

- Synergy recovery: 5–15% margin uplift

Policy, carbon & grid risk reshape economics: 30% ITC; EU ETS €85/t

Fuel costs (Henry Hub ~60% below 2022 peaks) and LNG oversupply compress input costs while hedges/PPAs stabilize margins. Rates (Fed funds ~5.25–5.50% 2024–25) raise WACC and pressure returns; green debt market (> $500bn 2024) eases financing. FX (USD/ILS ~3.67 in 2024) and 800+ GW interconnection backlog increase execution risk; PPA pricing compresses to ~$20–40/MWh.

| Metric | Value |

|---|---|

| Henry Hub vs 2022 | -60% |

| Fed funds | 5.25–5.50% |

| Green issuance 2024 | >$500bn |

| USD/ILS 2024 | ~3.67 |

| Interconnection backlog | 800+ GW |

| PPA range | $20–40/MWh |

Same Document Delivered

OPC Energy PESTLE Analysis

The preview shown here is the exact OPC Energy PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The layout, content, and insights visible now are the final file you’ll download immediately after payment. No placeholders, no teasers—this is the real document.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, social trends, tech advances, legal shifts, and environmental pressures are shaping OPC Energy’s outlook in our concise PESTLE snapshot—perfect for investors and strategists. Purchase the full analysis for detailed, actionable insights you can deploy immediately.

Political factors

Energy policy and subsidies

Government incentives, carbon pricing, and renewable targets shape OPC’s fuel mix and project pipeline: Israel targets roughly 30% renewable electricity by 2030, while the U.S. Inflation Reduction Act offers up to a 30% investment tax credit for qualifying solar and storage projects. EU ETS carbon prices averaged about €85/ton in 2024, affecting regional gas economics. Policy stability directly influences financing terms and contract tenor, while sudden subsidy or cap reforms can materially change project returns.

Geopolitical and security risk (Israel)

Regional tensions since October 2023 have disrupted supply chains and construction timelines in the Eastern Mediterranean, threatening grid reliability and project schedules. Heightened political-risk premiums have pushed insurers and lenders to tighten terms, increasing project financing costs and necessitating redundancy planning. Government emergency energy measures can reprioritize dispatch and capacity commitments, so continuity plans and site diversification are critical to mitigate operational exposure.

Permitting and siting approvals

National, state and municipal authorities control site licenses, interconnection and environmental clearances, often with separate application paths and criteria. Lengthy review cycles of 18–36 months delay COD and escalate capex; U.S. interconnection backlog exceeded 1,000 GW in 2024, creating queue-driven cost risk. Early stakeholder engagement and regulator alignment reduce objections and rework. Coordinated timelines with grid operators are critical to avoid stranded assets.

Market design and grid operator rules

Capacity payments, ancillary services and dispatch rules set by system operators define OPC Energy revenue stacks; ERCOT scarcity caps at 5,000/MWh (2024) and U.S. reserve margins ~20% (NERC 2024) materially shape realized revenues and volatility.

Changes to scarcity pricing, nodal tariffs or curtailment alter profitability; U.S. interconnection queues exceed 1,000 GW (FERC 2024) while Israel faces constrained queues and higher curtailment risk, so active rulemaking engagement is essential.

- Capacity payments: regional; affect base revenue

- Ancillary services: fast-response value rising

- Scarcity pricing: ERCOT 5,000/MWh cap (2024)

- Queues: U.S. >1,000 GW; Israel: constrained

- Action: participate in rulemaking

Public sector offtake and PPPs

Government entities as customers give creditworthy PPAs that lower commercial risk but raise compliance and procurement complexity; competitive tenders and localization rules increasingly dictate bid structure and supply-chain sourcing. Contract renegotiations or fiscal pressures can compress tariff trajectories and delay collections, while strong relationships with public buyers improve pipeline visibility and de-risk long-term project financing.

- Public offtakers: creditworthy but compliance-heavy

- Tenders/localization: shape bid and capex

- Renegotiation risk: affects tariff paths

- Strong public ties: enhance pipeline visibility

Policy, carbon & grid risk reshape economics: 30% ITC; EU ETS €85/t

Policy incentives, carbon pricing and geopolitical risk materially reshape OPC Energy’s project economics and financing terms. Key levers: Israel 30% renewables by 2030, U.S. IRA up to 30% ITC, EU ETS ~€85/t (2024). Interconnection backlogs (>1,000 GW U.S., FERC 2024) and ERCOT scarcity cap 5,000/MWh (2024) drive queue, curtailment and revenue risk.

| Policy | Metric | Impact |

|---|---|---|

| Renewable targets | Israel 30% by 2030 | Pipeline demand |

| Incentives | IRA up to 30% ITC | Capex reduction |

| Carbon price | EU ETS €85/t (2024) | Fuel shift |

| Queues/scarcity | US >1,000 GW; ERCOT 5,000/MWh | Revenue/curtailment risk |

What is included in the product

Explores how macro-environmental factors uniquely affect OPC Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific regulatory context.

A clean, summarized OPC Energy PESTLE that’s visually segmented by category for quick interpretation at a glance, making it easy to drop into presentations or planning sessions.

Economic factors

Natural gas price volatility

Fuel costs drive OPC’s spark spreads as US Henry Hub gas is roughly 60% below 2022 peaks and global LNG oversupply pushed spot LNG to multi-year lows in 2024, compressing input costs. Regional contracts and Israeli import dynamics still create basis differentials vs US prices. Hedging programs and pass-through clauses in OPC’s PPAs materially stabilize margins. Diversifying into renewables and storage reduces fuel exposure and volatility risk.

Interest rates and capital access

Rising policy rates (Fed funds ~5.25–5.50% through 2024–25) lift WACC and compress equity IRRs for long-lived OPC Energy assets, making returns sensitive to discount-rate shifts. Project finance availability now hinges on contracted cash flows and clear policy pathways for hydrogen/CCS; refinancing windows materially affect portfolio returns. Green bonds and sustainability-linked loans, with global green issuance above $500bn in 2024, can improve pricing.

Electricity demand and load shape

Economic growth, electrification and data center expansion lifted global electricity demand about 2.5% in 2023, with data centers now consuming roughly 1% of global power and hyperscaler buildouts driving local peaks.

Rapid EV and heat‑pump adoption shifts loads into evening and daytime peaks—EV charging could add 5–10% to peak demand in many grids by 2030—creating new dispatch and arbitrage opportunities.

Accurate short‑term and long‑term forecasting is critical: utility‑scale battery additions (tens of GW annually) and capacity procurement hinge on tight load-shape projections, while demand downturns expose merchant generators to revenue risk.

Exchange rate exposure (ILS/USD)

Multi-jurisdiction operations create FX mismatches across revenues, costs and debt for OPC Energy; Bank of Israel data shows USD/ILS averaged about 3.67 in 2024, amplifying translation risk and affecting reported earnings and covenant headroom. Natural hedges and derivatives have reduced P&L volatility historically, while financing in operating currencies aligns cash flows and lowers refinancing risk.

- FX mismatch across revenue, costs, debt

- USD/ILS avg 3.67 in 2024 (Bank of Israel)

- Derivatives and natural hedges cut P&L volatility

- Local-currency financing aligns cash flows, improves covenant headroom

Competition and market entry costs

Crowded interconnection queues (US ~800+ GW reported across RTO filings in 2023–24) and EPC inflation (tenders up ~10–20% vs 2020) raise entry barriers, while rival IPPs, utilities and infrastructure funds compress PPA pricing toward $20–40/MWh in prime US markets. Scale procurement and O&M synergies can recover 5–15% of margin; superior development optionality becomes a key differentiator.

- Interconnection: US ~800+ GW backlog (2023–24)

- EPC inflation: +10–20% vs 2020

- PPA pressure: ~$20–40/MWh in top US markets

- Synergy recovery: 5–15% margin uplift

Policy, carbon & grid risk reshape economics: 30% ITC; EU ETS €85/t

Fuel costs (Henry Hub ~60% below 2022 peaks) and LNG oversupply compress input costs while hedges/PPAs stabilize margins. Rates (Fed funds ~5.25–5.50% 2024–25) raise WACC and pressure returns; green debt market (> $500bn 2024) eases financing. FX (USD/ILS ~3.67 in 2024) and 800+ GW interconnection backlog increase execution risk; PPA pricing compresses to ~$20–40/MWh.

| Metric | Value |

|---|---|

| Henry Hub vs 2022 | -60% |

| Fed funds | 5.25–5.50% |

| Green issuance 2024 | >$500bn |

| USD/ILS 2024 | ~3.67 |

| Interconnection backlog | 800+ GW |

| PPA range | $20–40/MWh |

Same Document Delivered

OPC Energy PESTLE Analysis

The preview shown here is the exact OPC Energy PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The layout, content, and insights visible now are the final file you’ll download immediately after payment. No placeholders, no teasers—this is the real document.