Oportun Financial Business Model Canvas

Customer-centric credit blueprint: underwriting, partnerships, revenue & risk

Unlock the full strategic blueprint behind Oportun Financial’s Business Model Canvas: three to five concise sentences revealing how it creates customer-centric credit products, leverages proprietary underwriting and partnerships, and captures revenue while managing risk. Purchase the complete, editable Word/Excel canvas to benchmark strategy, support investor decks, and accelerate competitive planning.

Partnerships

Banking and credit card issuers

Partnerships with issuing banks and card networks enable Oportun to offer credit cards and scale card portfolios by leveraging partners' compliance, settlement, and co-branding infrastructure.

These partners provide fraud controls and dispute resolution capabilities that strengthen risk management and customer trust.

Collaboration reduces time-to-market and capital intensity, allowing Oportun to expand card offerings without large incremental balance-sheet investment.

Capital markets and warehouse lenders

Oportun relies on warehouse lines, securitizations and whole-loan buyers to fund originations, a structure it maintained through 2024 to lower cost of funds and diversify liquidity. These partners enable balance-sheet optimization and risk transfer, supporting capital efficiency and regulatory flexibility. Stable funding from these channels underpins consistent lending to underserved customers.

Credit bureaus and data providers

Oportun maintains secure data feeds to the three major US credit bureaus—Equifax, Experian and TransUnion—as of 2024 to support underwriting, fraud checks and credit reporting. Alternative data vendors augment thin-file risk assessment, improving approvals for underserved applicants. Timely bureau reporting helps customers build tradelines and credit histories while data partnerships boost decisioning precision and regulatory compliance.

Fintech and technology vendors

- cloud: >$600B public cloud spend 2024

- AI/analytics: ML credit scoring

- KYC/e-sign: faster onboarding

- payments: omnichannel repayments

Community groups and referral partners

Nonprofits, employers, and community organizations extend Oportun’s reach to low- and moderate-income consumers, improving access and cultural fit; referrals from these partners boost acquisition quality and trust while lowering CAC. Financial education partners improve repayment outcomes and lifetime value by increasing financial capability. Local partnerships reinforce brand credibility and align with Oportun’s mission to serve underserved communities.

- Partners: nonprofits, employers, community orgs

- Benefits: higher-quality referrals, lower CAC, better trust

- Outcomes: improved repayment, customer LTV, mission alignment

Partnerships power card issuance, diversified funding and data-driven underwriting

Partnerships with issuing banks and card networks enable card issuance, compliance and scaled portfolios.

Warehouse lines, securitizations and whole‑loan buyers funded originations through 2024, diversifying liquidity and lowering cost of funds.

Data ties to Equifax, Experian and TransUnion and alternative vendors support underwriting and reporting as of 2024.

Fintech/cloud vendors (public cloud >$600B 2024) and community partners accelerate product, acquisition and repayment outcomes.

| Partner | Role | 2024 metric |

|---|---|---|

| Issuers/networks | Card issuance, compliance | Scaled portfolios |

| Funding buyers | Liquidity, risk transfer | Securitizations maintained 2024 |

| Credit bureaus | Underwriting/reporting | Equifax/Experian/TransUnion |

What is included in the product

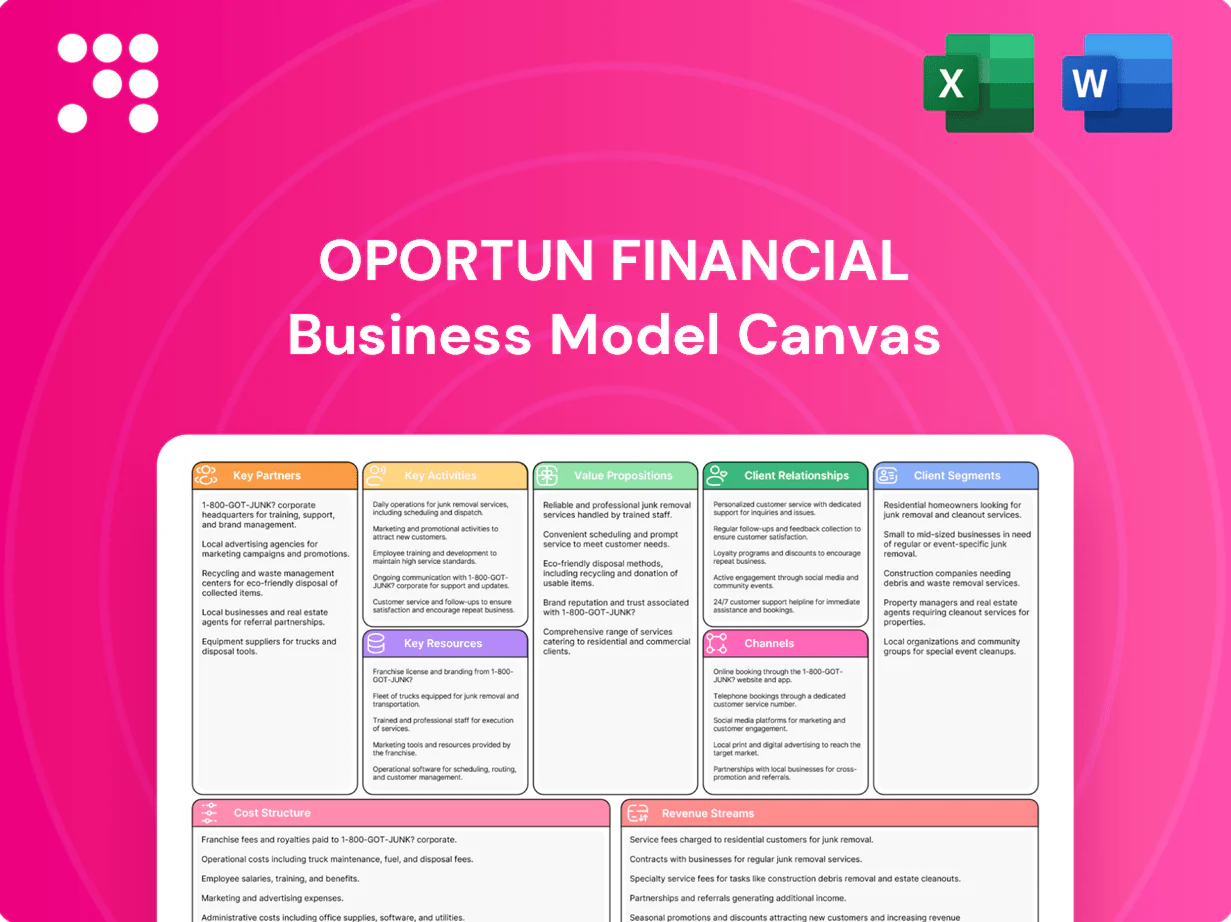

A comprehensive Business Model Canvas for Oportun Financial outlining customer segments, channels, value propositions, revenue streams, and key activities tied to its mission of providing responsible, data-driven lending to underserved consumers; organized into 9 BMC blocks with competitive analysis and SWOT insights for presentations and strategic decisions.

Condenses Oportun’s lending platform into an editable one-page Business Model Canvas, quickly relieving pain from fragmented strategy and documentation by clarifying customer segments, revenue streams, risk controls, and distribution channels for fast team alignment and decision-making.

Activities

Responsible credit underwriting

Responsible underwriting uses traditional bureau data plus alternative sources (bank transactions and income verification) to design and refine risk models. Teams balance approval rates with expected losses and borrower ability-to-pay while complying with ECOA and FCRA requirements. Decisioning is enforced across product lines and scorecards undergo continuous testing, monitoring, and weekly/monthly recalibration.

Loan and card origination

Streamline applications across digital and in-person channels to serve over 2 million customers, unifying web, mobile, and branch intake. Verify identity, income, and employment efficiently using automated KYC and data-enriched checks to reduce manual review times and fraud. Deliver transparent terms and quick funding—many approvals fund in under 24 hours—while optimizing conversion with a frictionless UX and clear disclosures that can lift conversion by roughly 20%.

Servicing and collections

Oportun provides omnichannel servicing—mobile, web, and contact center—for payments, hardship requests, and account support, serving over 1.2 million customers and a loan portfolio exceeding $1.3 billion in 2024. Empathetic, compliant collections focus on maximizing recoveries while preserving customer relationships through tailored payment plans and hardship options. Portfolio health is tracked continuously with early-warning indicators to reduce loss severity and inform remediation strategies.

Risk, compliance, and reporting

Maintain robust controls for fair lending, UDAAP, AML, and privacy; conduct model governance, independent audits and stress tests; report to Equifax, Experian and TransUnion to help customers build credit; and manage vendor risk and regulatory relationships to sustain compliance and operational resilience.

- Fair lending, UDAAP, AML, privacy controls

- Model governance, audits, stress tests

- Credit bureau reporting (Equifax, Experian, TransUnion)

- Vendor risk & regulatory engagement

Capital and liquidity management

Structure warehouse lines and ABS programs to fund growth, while actively hedging interest rate exposure and aligning pricing with funding costs and credit risk.

Optimize capital allocation across personal-loan, auto-refinance and banking-like products to maximize risk-adjusted returns, supported by rigorous performance reporting.

Maintain strong investor relations with transparent quarterly disclosures and investor presentations to sustain access to institutional funding.

- NASDAQ: OPRT public access to capital

- ABS/warehouse funding for scale

- Interest-rate hedging and dynamic pricing

- Product-level capital optimization

- Quarterly investor reporting

Responsible underwriting funds 2M, $1.3B portfolio; 20% conversion lift

Responsible underwriting uses bureau plus alternative data to manage risk for over 2 million customers and a $1.3B loan portfolio (2024). Omnichannel origination and automated verification enable many approvals and sub-24hr funding, boosting conversion ~20%. Robust compliance, model governance, ABS/warehouse funding and quarterly investor reporting sustain liquidity and scale (NASDAQ: OPRT).

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual Oportun Financial Business Model Canvas you will receive after purchase. It is not a mockup—this same ready-to-edit file includes all sections and formatting as shown. Upon payment you’ll instantly download the complete document in Word and Excel, ready to present and customize.

Customer-centric credit blueprint: underwriting, partnerships, revenue & risk

Unlock the full strategic blueprint behind Oportun Financial’s Business Model Canvas: three to five concise sentences revealing how it creates customer-centric credit products, leverages proprietary underwriting and partnerships, and captures revenue while managing risk. Purchase the complete, editable Word/Excel canvas to benchmark strategy, support investor decks, and accelerate competitive planning.

Partnerships

Banking and credit card issuers

Partnerships with issuing banks and card networks enable Oportun to offer credit cards and scale card portfolios by leveraging partners' compliance, settlement, and co-branding infrastructure.

These partners provide fraud controls and dispute resolution capabilities that strengthen risk management and customer trust.

Collaboration reduces time-to-market and capital intensity, allowing Oportun to expand card offerings without large incremental balance-sheet investment.

Capital markets and warehouse lenders

Oportun relies on warehouse lines, securitizations and whole-loan buyers to fund originations, a structure it maintained through 2024 to lower cost of funds and diversify liquidity. These partners enable balance-sheet optimization and risk transfer, supporting capital efficiency and regulatory flexibility. Stable funding from these channels underpins consistent lending to underserved customers.

Credit bureaus and data providers

Oportun maintains secure data feeds to the three major US credit bureaus—Equifax, Experian and TransUnion—as of 2024 to support underwriting, fraud checks and credit reporting. Alternative data vendors augment thin-file risk assessment, improving approvals for underserved applicants. Timely bureau reporting helps customers build tradelines and credit histories while data partnerships boost decisioning precision and regulatory compliance.

Fintech and technology vendors

- cloud: >$600B public cloud spend 2024

- AI/analytics: ML credit scoring

- KYC/e-sign: faster onboarding

- payments: omnichannel repayments

Community groups and referral partners

Nonprofits, employers, and community organizations extend Oportun’s reach to low- and moderate-income consumers, improving access and cultural fit; referrals from these partners boost acquisition quality and trust while lowering CAC. Financial education partners improve repayment outcomes and lifetime value by increasing financial capability. Local partnerships reinforce brand credibility and align with Oportun’s mission to serve underserved communities.

- Partners: nonprofits, employers, community orgs

- Benefits: higher-quality referrals, lower CAC, better trust

- Outcomes: improved repayment, customer LTV, mission alignment

Partnerships power card issuance, diversified funding and data-driven underwriting

Partnerships with issuing banks and card networks enable card issuance, compliance and scaled portfolios.

Warehouse lines, securitizations and whole‑loan buyers funded originations through 2024, diversifying liquidity and lowering cost of funds.

Data ties to Equifax, Experian and TransUnion and alternative vendors support underwriting and reporting as of 2024.

Fintech/cloud vendors (public cloud >$600B 2024) and community partners accelerate product, acquisition and repayment outcomes.

| Partner | Role | 2024 metric |

|---|---|---|

| Issuers/networks | Card issuance, compliance | Scaled portfolios |

| Funding buyers | Liquidity, risk transfer | Securitizations maintained 2024 |

| Credit bureaus | Underwriting/reporting | Equifax/Experian/TransUnion |

What is included in the product

A comprehensive Business Model Canvas for Oportun Financial outlining customer segments, channels, value propositions, revenue streams, and key activities tied to its mission of providing responsible, data-driven lending to underserved consumers; organized into 9 BMC blocks with competitive analysis and SWOT insights for presentations and strategic decisions.

Condenses Oportun’s lending platform into an editable one-page Business Model Canvas, quickly relieving pain from fragmented strategy and documentation by clarifying customer segments, revenue streams, risk controls, and distribution channels for fast team alignment and decision-making.

Activities

Responsible credit underwriting

Responsible underwriting uses traditional bureau data plus alternative sources (bank transactions and income verification) to design and refine risk models. Teams balance approval rates with expected losses and borrower ability-to-pay while complying with ECOA and FCRA requirements. Decisioning is enforced across product lines and scorecards undergo continuous testing, monitoring, and weekly/monthly recalibration.

Loan and card origination

Streamline applications across digital and in-person channels to serve over 2 million customers, unifying web, mobile, and branch intake. Verify identity, income, and employment efficiently using automated KYC and data-enriched checks to reduce manual review times and fraud. Deliver transparent terms and quick funding—many approvals fund in under 24 hours—while optimizing conversion with a frictionless UX and clear disclosures that can lift conversion by roughly 20%.

Servicing and collections

Oportun provides omnichannel servicing—mobile, web, and contact center—for payments, hardship requests, and account support, serving over 1.2 million customers and a loan portfolio exceeding $1.3 billion in 2024. Empathetic, compliant collections focus on maximizing recoveries while preserving customer relationships through tailored payment plans and hardship options. Portfolio health is tracked continuously with early-warning indicators to reduce loss severity and inform remediation strategies.

Risk, compliance, and reporting

Maintain robust controls for fair lending, UDAAP, AML, and privacy; conduct model governance, independent audits and stress tests; report to Equifax, Experian and TransUnion to help customers build credit; and manage vendor risk and regulatory relationships to sustain compliance and operational resilience.

- Fair lending, UDAAP, AML, privacy controls

- Model governance, audits, stress tests

- Credit bureau reporting (Equifax, Experian, TransUnion)

- Vendor risk & regulatory engagement

Capital and liquidity management

Structure warehouse lines and ABS programs to fund growth, while actively hedging interest rate exposure and aligning pricing with funding costs and credit risk.

Optimize capital allocation across personal-loan, auto-refinance and banking-like products to maximize risk-adjusted returns, supported by rigorous performance reporting.

Maintain strong investor relations with transparent quarterly disclosures and investor presentations to sustain access to institutional funding.

- NASDAQ: OPRT public access to capital

- ABS/warehouse funding for scale

- Interest-rate hedging and dynamic pricing

- Product-level capital optimization

- Quarterly investor reporting

Responsible underwriting funds 2M, $1.3B portfolio; 20% conversion lift

Responsible underwriting uses bureau plus alternative data to manage risk for over 2 million customers and a $1.3B loan portfolio (2024). Omnichannel origination and automated verification enable many approvals and sub-24hr funding, boosting conversion ~20%. Robust compliance, model governance, ABS/warehouse funding and quarterly investor reporting sustain liquidity and scale (NASDAQ: OPRT).

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual Oportun Financial Business Model Canvas you will receive after purchase. It is not a mockup—this same ready-to-edit file includes all sections and formatting as shown. Upon payment you’ll instantly download the complete document in Word and Excel, ready to present and customize.

Original: $10.00

-65%$10.00

$3.50Description

Customer-centric credit blueprint: underwriting, partnerships, revenue & risk

Unlock the full strategic blueprint behind Oportun Financial’s Business Model Canvas: three to five concise sentences revealing how it creates customer-centric credit products, leverages proprietary underwriting and partnerships, and captures revenue while managing risk. Purchase the complete, editable Word/Excel canvas to benchmark strategy, support investor decks, and accelerate competitive planning.

Partnerships

Banking and credit card issuers

Partnerships with issuing banks and card networks enable Oportun to offer credit cards and scale card portfolios by leveraging partners' compliance, settlement, and co-branding infrastructure.

These partners provide fraud controls and dispute resolution capabilities that strengthen risk management and customer trust.

Collaboration reduces time-to-market and capital intensity, allowing Oportun to expand card offerings without large incremental balance-sheet investment.

Capital markets and warehouse lenders

Oportun relies on warehouse lines, securitizations and whole-loan buyers to fund originations, a structure it maintained through 2024 to lower cost of funds and diversify liquidity. These partners enable balance-sheet optimization and risk transfer, supporting capital efficiency and regulatory flexibility. Stable funding from these channels underpins consistent lending to underserved customers.

Credit bureaus and data providers

Oportun maintains secure data feeds to the three major US credit bureaus—Equifax, Experian and TransUnion—as of 2024 to support underwriting, fraud checks and credit reporting. Alternative data vendors augment thin-file risk assessment, improving approvals for underserved applicants. Timely bureau reporting helps customers build tradelines and credit histories while data partnerships boost decisioning precision and regulatory compliance.

Fintech and technology vendors

- cloud: >$600B public cloud spend 2024

- AI/analytics: ML credit scoring

- KYC/e-sign: faster onboarding

- payments: omnichannel repayments

Community groups and referral partners

Nonprofits, employers, and community organizations extend Oportun’s reach to low- and moderate-income consumers, improving access and cultural fit; referrals from these partners boost acquisition quality and trust while lowering CAC. Financial education partners improve repayment outcomes and lifetime value by increasing financial capability. Local partnerships reinforce brand credibility and align with Oportun’s mission to serve underserved communities.

- Partners: nonprofits, employers, community orgs

- Benefits: higher-quality referrals, lower CAC, better trust

- Outcomes: improved repayment, customer LTV, mission alignment

Partnerships power card issuance, diversified funding and data-driven underwriting

Partnerships with issuing banks and card networks enable card issuance, compliance and scaled portfolios.

Warehouse lines, securitizations and whole‑loan buyers funded originations through 2024, diversifying liquidity and lowering cost of funds.

Data ties to Equifax, Experian and TransUnion and alternative vendors support underwriting and reporting as of 2024.

Fintech/cloud vendors (public cloud >$600B 2024) and community partners accelerate product, acquisition and repayment outcomes.

| Partner | Role | 2024 metric |

|---|---|---|

| Issuers/networks | Card issuance, compliance | Scaled portfolios |

| Funding buyers | Liquidity, risk transfer | Securitizations maintained 2024 |

| Credit bureaus | Underwriting/reporting | Equifax/Experian/TransUnion |

What is included in the product

A comprehensive Business Model Canvas for Oportun Financial outlining customer segments, channels, value propositions, revenue streams, and key activities tied to its mission of providing responsible, data-driven lending to underserved consumers; organized into 9 BMC blocks with competitive analysis and SWOT insights for presentations and strategic decisions.

Condenses Oportun’s lending platform into an editable one-page Business Model Canvas, quickly relieving pain from fragmented strategy and documentation by clarifying customer segments, revenue streams, risk controls, and distribution channels for fast team alignment and decision-making.

Activities

Responsible credit underwriting

Responsible underwriting uses traditional bureau data plus alternative sources (bank transactions and income verification) to design and refine risk models. Teams balance approval rates with expected losses and borrower ability-to-pay while complying with ECOA and FCRA requirements. Decisioning is enforced across product lines and scorecards undergo continuous testing, monitoring, and weekly/monthly recalibration.

Loan and card origination

Streamline applications across digital and in-person channels to serve over 2 million customers, unifying web, mobile, and branch intake. Verify identity, income, and employment efficiently using automated KYC and data-enriched checks to reduce manual review times and fraud. Deliver transparent terms and quick funding—many approvals fund in under 24 hours—while optimizing conversion with a frictionless UX and clear disclosures that can lift conversion by roughly 20%.

Servicing and collections

Oportun provides omnichannel servicing—mobile, web, and contact center—for payments, hardship requests, and account support, serving over 1.2 million customers and a loan portfolio exceeding $1.3 billion in 2024. Empathetic, compliant collections focus on maximizing recoveries while preserving customer relationships through tailored payment plans and hardship options. Portfolio health is tracked continuously with early-warning indicators to reduce loss severity and inform remediation strategies.

Risk, compliance, and reporting

Maintain robust controls for fair lending, UDAAP, AML, and privacy; conduct model governance, independent audits and stress tests; report to Equifax, Experian and TransUnion to help customers build credit; and manage vendor risk and regulatory relationships to sustain compliance and operational resilience.

- Fair lending, UDAAP, AML, privacy controls

- Model governance, audits, stress tests

- Credit bureau reporting (Equifax, Experian, TransUnion)

- Vendor risk & regulatory engagement

Capital and liquidity management

Structure warehouse lines and ABS programs to fund growth, while actively hedging interest rate exposure and aligning pricing with funding costs and credit risk.

Optimize capital allocation across personal-loan, auto-refinance and banking-like products to maximize risk-adjusted returns, supported by rigorous performance reporting.

Maintain strong investor relations with transparent quarterly disclosures and investor presentations to sustain access to institutional funding.

- NASDAQ: OPRT public access to capital

- ABS/warehouse funding for scale

- Interest-rate hedging and dynamic pricing

- Product-level capital optimization

- Quarterly investor reporting

Responsible underwriting funds 2M, $1.3B portfolio; 20% conversion lift

Responsible underwriting uses bureau plus alternative data to manage risk for over 2 million customers and a $1.3B loan portfolio (2024). Omnichannel origination and automated verification enable many approvals and sub-24hr funding, boosting conversion ~20%. Robust compliance, model governance, ABS/warehouse funding and quarterly investor reporting sustain liquidity and scale (NASDAQ: OPRT).

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual Oportun Financial Business Model Canvas you will receive after purchase. It is not a mockup—this same ready-to-edit file includes all sections and formatting as shown. Upon payment you’ll instantly download the complete document in Word and Excel, ready to present and customize.