Option Care Health SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

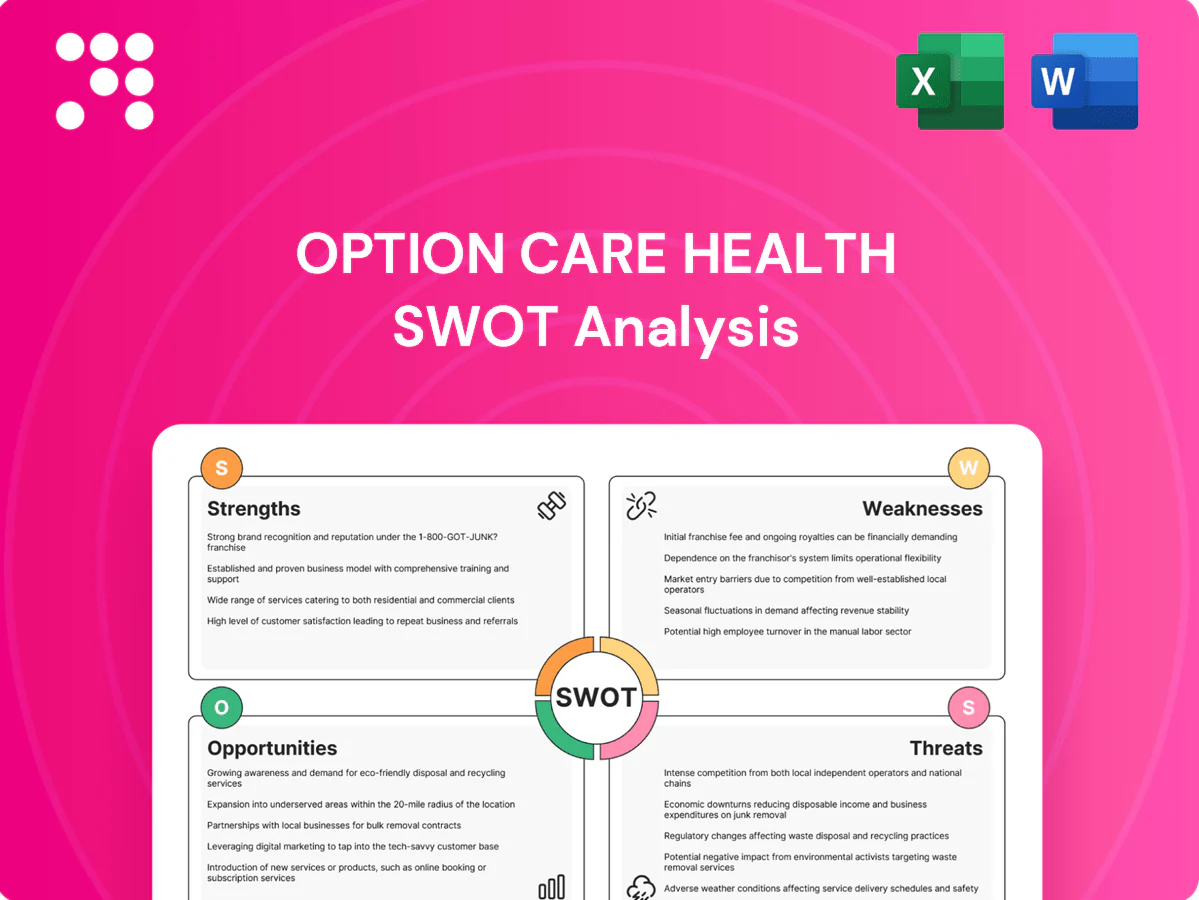

Option Care Health’s SWOT highlights strong home-infused medication capabilities and scale advantages, offset by reimbursement pressures and operational complexity; strategic partnerships and tech-enabled care pathways offer clear growth levers. Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Strengths

National scale in home and alternate-site infusion

Option Care Health operates nationally across all 50 states and Puerto Rico, enabling rapid referrals, standardized clinical protocols, and a consistent patient experience. Its scale underpins preferred-provider arrangements with major health systems and payors and allows fixed clinical, pharmacy, and logistics costs to be spread over a large patient base. This creates measurable cost and service reliability advantages versus smaller independents.

Deep payor and provider partnerships

Option Care Health (NASDAQ: OPCH) leverages embedded relationships with physicians, hospitals and insurers—strengthened since the 2020 BioScrip acquisition—to streamline care transitions through coordinated authorizations, scheduling and outcomes reporting, reducing denials and friction. Strong discharge-planning integration accelerates hospital throughput and underpins steady referral flow and clearer reimbursement pathways.

Comprehensive therapy portfolio and clinical expertise

Coverage of complex biologics, anti-infectives, immunoglobulins, nutrition, and specialty therapies broadens Option Care Health’s addressable demand, underpinning 2024 revenue of about $4.1 billion and ~2 million patients served. Specialized nurses and pharmacists provide high-touch care and monitoring across >400 sites, while clinical programs drive adherence and adverse-event management with reported readmission reductions. These capabilities support superior outcomes and higher patient satisfaction outside hospitals.

Cost-effective alternative to inpatient care

Home and alternate-site infusion typically cuts total episode costs by an estimated 30–60% versus hospital care, driving payor preference for site-of-care optimization while maintaining equal or better outcomes; CDC data shows ~1 in 31 hospital patients has a healthcare-associated infection, underscoring lower infection risk at home. This convenience and economic value support durable demand for Option Care Health services.

- Cost reduction: 30–60% lower episode costs

- Infection risk: hospital HAI ~1 in 31 patients

- Payor focus: site-of-care optimization

- Demand: convenience + economics support durability

Care coordination and disease management capabilities

Option Care Health’s structured care pathways align payers, physicians and home infusion teams around the patient, supporting persistence on specialty therapies; the company reported approximately $3.0 billion revenue in 2023 and serves over 1.0 million patients annually. Data-driven adherence, education and symptom tracking have driven double-digit adherence gains and proactive interventions that studies link to reductions in unplanned utilization. These capabilities differentiate service quality and enable value-based contracting.

- Revenue 2023: ~3.0B

- Patients served: ~1.0M+

- Adherence gains: double-digit%

- Unplanned utilization reduction: mid-teens%

National infusion network: ~400 sites, ~2.0M patients, $4.1B revenue

Option Care Health’s national scale and ~400 sites enable standardized protocols, preferred-provider leverage and lower per-patient fixed costs. Broad specialty portfolio and embedded payor/provider relationships drove ~2024 revenue ~$4.1B and ~2.0M patients, supporting durable demand and site-of-care savings. Data-driven adherence programs yield double-digit adherence gains and reduced unplanned utilization.

| Metric | Value (2024) |

|---|---|

| Revenue | $4.1B |

| Patients | ~2.0M |

| Sites | ~400+ |

| Episode cost reduction | 30–60% |

| Adherence gains | Double-digit% |

What is included in the product

Provides a concise SWOT analysis of Option Care Health, highlighting internal strengths and weaknesses alongside external opportunities and threats to assess its competitive position and strategic risks.

Provides a concise SWOT matrix tailored to Option Care Health for rapid identification of clinical, operational, and reimbursement risks and growth opportunities, ideal for executives needing a clear snapshot to align strategy quickly.

Weaknesses

Reimbursement and authorization complexity

Revenue relies on mixed medical and pharmacy benefit rules that vary by plan, creating billing complexity and unpredictable cash flow; prior authorizations and heavy documentation routinely delay patient starts of care and lengthen DSO timelines. Frequent denials and recertifications raise administrative costs and reduce operational efficiency, producing uneven margin visibility across therapies and payors.

Labor-intensive clinical model

Option Care Health's model depends on skilled nurses, pharmacists, and dietitians to safely deliver complex home and outpatient infusions, making labor central to service quality. Staffing shortages and reliance on overtime push unit costs higher; BLS projects registered nurse employment to grow 6% from 2022–2032, tightening supply. Training and credentialing commonly require 4–8 weeks per clinician, adding expense and ramp time, while limited clinician capacity constrains rapid scaling during demand spikes.

Working capital tied to high-cost drugs

Option Care's working capital is heavily tied to specialty medications, which account for about 55% of US drug spend (IQVIA 2024) and can cost tens to hundreds of thousands per course, requiring large inventory and tight procurement. Reimbursement lags of roughly 30–90 days commonly strain cash conversion cycles. Volatile drug prices compress pass-through margins, heightening sensitivity to payer mix and contract terms.

Operational complexity in home logistics

Coordinating compounding, cold-chain distribution and in-home scheduling raises operational complexity for Option Care Health (NASDAQ: OPCH), increasing route-planning inefficiencies, cancellations and supply variability that strain margins. Navigating 50-state licensure and home-care regulations adds administrative overhead and risk. Service incidents can erode patient trust and reduce referral volume.

- Nationwide operations: 50-state licensure burden

- Logistics: cold-chain + compounding increases costs

- Scheduling: route planning, cancellations drive inefficiency

- Reputation risk: incidents reduce referrals

Limited diversification beyond infusion

Concentration in infusion care heightens exposure to therapy and policy shifts; Option Care Health reported $5.13 billion revenue in 2023 with infusion services comprising the majority of net sales, leaving results sensitive to drug mix and Medicare policy changes. Cross-selling outside core services is constrained by limited adjacent offerings, reducing revenue optionality versus diversified post-acute peers. Geographic and service-line concentration amplifies risk from local reimbursement pressure and clinic closures, narrowing strategic flexibility.

- High reliance: 2023 revenue $5.13B — majority from infusion

- Cross-sell limited: fewer non-infusion services

- Concentration risk: local reimbursement exposure

- Lower optionality vs broader post-acute platforms

Care delivery under strain: specialty drug exposure, payment lags and workforce bottlenecks

Revenue and cash flow are pressured by mixed benefit rules, prior‑auth delays and 30–90 day reimbursement lags; 2023 revenue $5.13B with specialty drugs driving exposure (IQVIA 2024 ~55% of US drug spend). Labor dependence raises costs amid a projected 6% RN supply growth (BLS 2022–32) and 4–8 week credentialing. Cold‑chain, compounding and 50‑state licensure heighten cancellations, route inefficiency and reputational risk.

| Metric | Value |

|---|---|

| 2023 revenue | $5.13B |

| Specialty drug exposure | ~55% (IQVIA 2024) |

| Reimbursement lag | 30–90 days |

| RN supply growth | 6% (BLS 2022–32) |

| Credentialing time | 4–8 weeks |

What You See Is What You Get

Option Care Health SWOT Analysis

This is the actual Option Care Health SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, with strengths, weaknesses, opportunities, and threats clearly outlined. Purchase unlocks the complete, editable version ready for download and immediate use.

Dive Deeper Into the Company’s Strategic Blueprint

Option Care Health’s SWOT highlights strong home-infused medication capabilities and scale advantages, offset by reimbursement pressures and operational complexity; strategic partnerships and tech-enabled care pathways offer clear growth levers. Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Strengths

National scale in home and alternate-site infusion

Option Care Health operates nationally across all 50 states and Puerto Rico, enabling rapid referrals, standardized clinical protocols, and a consistent patient experience. Its scale underpins preferred-provider arrangements with major health systems and payors and allows fixed clinical, pharmacy, and logistics costs to be spread over a large patient base. This creates measurable cost and service reliability advantages versus smaller independents.

Deep payor and provider partnerships

Option Care Health (NASDAQ: OPCH) leverages embedded relationships with physicians, hospitals and insurers—strengthened since the 2020 BioScrip acquisition—to streamline care transitions through coordinated authorizations, scheduling and outcomes reporting, reducing denials and friction. Strong discharge-planning integration accelerates hospital throughput and underpins steady referral flow and clearer reimbursement pathways.

Comprehensive therapy portfolio and clinical expertise

Coverage of complex biologics, anti-infectives, immunoglobulins, nutrition, and specialty therapies broadens Option Care Health’s addressable demand, underpinning 2024 revenue of about $4.1 billion and ~2 million patients served. Specialized nurses and pharmacists provide high-touch care and monitoring across >400 sites, while clinical programs drive adherence and adverse-event management with reported readmission reductions. These capabilities support superior outcomes and higher patient satisfaction outside hospitals.

Cost-effective alternative to inpatient care

Home and alternate-site infusion typically cuts total episode costs by an estimated 30–60% versus hospital care, driving payor preference for site-of-care optimization while maintaining equal or better outcomes; CDC data shows ~1 in 31 hospital patients has a healthcare-associated infection, underscoring lower infection risk at home. This convenience and economic value support durable demand for Option Care Health services.

- Cost reduction: 30–60% lower episode costs

- Infection risk: hospital HAI ~1 in 31 patients

- Payor focus: site-of-care optimization

- Demand: convenience + economics support durability

Care coordination and disease management capabilities

Option Care Health’s structured care pathways align payers, physicians and home infusion teams around the patient, supporting persistence on specialty therapies; the company reported approximately $3.0 billion revenue in 2023 and serves over 1.0 million patients annually. Data-driven adherence, education and symptom tracking have driven double-digit adherence gains and proactive interventions that studies link to reductions in unplanned utilization. These capabilities differentiate service quality and enable value-based contracting.

- Revenue 2023: ~3.0B

- Patients served: ~1.0M+

- Adherence gains: double-digit%

- Unplanned utilization reduction: mid-teens%

National infusion network: ~400 sites, ~2.0M patients, $4.1B revenue

Option Care Health’s national scale and ~400 sites enable standardized protocols, preferred-provider leverage and lower per-patient fixed costs. Broad specialty portfolio and embedded payor/provider relationships drove ~2024 revenue ~$4.1B and ~2.0M patients, supporting durable demand and site-of-care savings. Data-driven adherence programs yield double-digit adherence gains and reduced unplanned utilization.

| Metric | Value (2024) |

|---|---|

| Revenue | $4.1B |

| Patients | ~2.0M |

| Sites | ~400+ |

| Episode cost reduction | 30–60% |

| Adherence gains | Double-digit% |

What is included in the product

Provides a concise SWOT analysis of Option Care Health, highlighting internal strengths and weaknesses alongside external opportunities and threats to assess its competitive position and strategic risks.

Provides a concise SWOT matrix tailored to Option Care Health for rapid identification of clinical, operational, and reimbursement risks and growth opportunities, ideal for executives needing a clear snapshot to align strategy quickly.

Weaknesses

Reimbursement and authorization complexity

Revenue relies on mixed medical and pharmacy benefit rules that vary by plan, creating billing complexity and unpredictable cash flow; prior authorizations and heavy documentation routinely delay patient starts of care and lengthen DSO timelines. Frequent denials and recertifications raise administrative costs and reduce operational efficiency, producing uneven margin visibility across therapies and payors.

Labor-intensive clinical model

Option Care Health's model depends on skilled nurses, pharmacists, and dietitians to safely deliver complex home and outpatient infusions, making labor central to service quality. Staffing shortages and reliance on overtime push unit costs higher; BLS projects registered nurse employment to grow 6% from 2022–2032, tightening supply. Training and credentialing commonly require 4–8 weeks per clinician, adding expense and ramp time, while limited clinician capacity constrains rapid scaling during demand spikes.

Working capital tied to high-cost drugs

Option Care's working capital is heavily tied to specialty medications, which account for about 55% of US drug spend (IQVIA 2024) and can cost tens to hundreds of thousands per course, requiring large inventory and tight procurement. Reimbursement lags of roughly 30–90 days commonly strain cash conversion cycles. Volatile drug prices compress pass-through margins, heightening sensitivity to payer mix and contract terms.

Operational complexity in home logistics

Coordinating compounding, cold-chain distribution and in-home scheduling raises operational complexity for Option Care Health (NASDAQ: OPCH), increasing route-planning inefficiencies, cancellations and supply variability that strain margins. Navigating 50-state licensure and home-care regulations adds administrative overhead and risk. Service incidents can erode patient trust and reduce referral volume.

- Nationwide operations: 50-state licensure burden

- Logistics: cold-chain + compounding increases costs

- Scheduling: route planning, cancellations drive inefficiency

- Reputation risk: incidents reduce referrals

Limited diversification beyond infusion

Concentration in infusion care heightens exposure to therapy and policy shifts; Option Care Health reported $5.13 billion revenue in 2023 with infusion services comprising the majority of net sales, leaving results sensitive to drug mix and Medicare policy changes. Cross-selling outside core services is constrained by limited adjacent offerings, reducing revenue optionality versus diversified post-acute peers. Geographic and service-line concentration amplifies risk from local reimbursement pressure and clinic closures, narrowing strategic flexibility.

- High reliance: 2023 revenue $5.13B — majority from infusion

- Cross-sell limited: fewer non-infusion services

- Concentration risk: local reimbursement exposure

- Lower optionality vs broader post-acute platforms

Care delivery under strain: specialty drug exposure, payment lags and workforce bottlenecks

Revenue and cash flow are pressured by mixed benefit rules, prior‑auth delays and 30–90 day reimbursement lags; 2023 revenue $5.13B with specialty drugs driving exposure (IQVIA 2024 ~55% of US drug spend). Labor dependence raises costs amid a projected 6% RN supply growth (BLS 2022–32) and 4–8 week credentialing. Cold‑chain, compounding and 50‑state licensure heighten cancellations, route inefficiency and reputational risk.

| Metric | Value |

|---|---|

| 2023 revenue | $5.13B |

| Specialty drug exposure | ~55% (IQVIA 2024) |

| Reimbursement lag | 30–90 days |

| RN supply growth | 6% (BLS 2022–32) |

| Credentialing time | 4–8 weeks |

What You See Is What You Get

Option Care Health SWOT Analysis

This is the actual Option Care Health SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, with strengths, weaknesses, opportunities, and threats clearly outlined. Purchase unlocks the complete, editable version ready for download and immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Option Care Health’s SWOT highlights strong home-infused medication capabilities and scale advantages, offset by reimbursement pressures and operational complexity; strategic partnerships and tech-enabled care pathways offer clear growth levers. Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Strengths

National scale in home and alternate-site infusion

Option Care Health operates nationally across all 50 states and Puerto Rico, enabling rapid referrals, standardized clinical protocols, and a consistent patient experience. Its scale underpins preferred-provider arrangements with major health systems and payors and allows fixed clinical, pharmacy, and logistics costs to be spread over a large patient base. This creates measurable cost and service reliability advantages versus smaller independents.

Deep payor and provider partnerships

Option Care Health (NASDAQ: OPCH) leverages embedded relationships with physicians, hospitals and insurers—strengthened since the 2020 BioScrip acquisition—to streamline care transitions through coordinated authorizations, scheduling and outcomes reporting, reducing denials and friction. Strong discharge-planning integration accelerates hospital throughput and underpins steady referral flow and clearer reimbursement pathways.

Comprehensive therapy portfolio and clinical expertise

Coverage of complex biologics, anti-infectives, immunoglobulins, nutrition, and specialty therapies broadens Option Care Health’s addressable demand, underpinning 2024 revenue of about $4.1 billion and ~2 million patients served. Specialized nurses and pharmacists provide high-touch care and monitoring across >400 sites, while clinical programs drive adherence and adverse-event management with reported readmission reductions. These capabilities support superior outcomes and higher patient satisfaction outside hospitals.

Cost-effective alternative to inpatient care

Home and alternate-site infusion typically cuts total episode costs by an estimated 30–60% versus hospital care, driving payor preference for site-of-care optimization while maintaining equal or better outcomes; CDC data shows ~1 in 31 hospital patients has a healthcare-associated infection, underscoring lower infection risk at home. This convenience and economic value support durable demand for Option Care Health services.

- Cost reduction: 30–60% lower episode costs

- Infection risk: hospital HAI ~1 in 31 patients

- Payor focus: site-of-care optimization

- Demand: convenience + economics support durability

Care coordination and disease management capabilities

Option Care Health’s structured care pathways align payers, physicians and home infusion teams around the patient, supporting persistence on specialty therapies; the company reported approximately $3.0 billion revenue in 2023 and serves over 1.0 million patients annually. Data-driven adherence, education and symptom tracking have driven double-digit adherence gains and proactive interventions that studies link to reductions in unplanned utilization. These capabilities differentiate service quality and enable value-based contracting.

- Revenue 2023: ~3.0B

- Patients served: ~1.0M+

- Adherence gains: double-digit%

- Unplanned utilization reduction: mid-teens%

National infusion network: ~400 sites, ~2.0M patients, $4.1B revenue

Option Care Health’s national scale and ~400 sites enable standardized protocols, preferred-provider leverage and lower per-patient fixed costs. Broad specialty portfolio and embedded payor/provider relationships drove ~2024 revenue ~$4.1B and ~2.0M patients, supporting durable demand and site-of-care savings. Data-driven adherence programs yield double-digit adherence gains and reduced unplanned utilization.

| Metric | Value (2024) |

|---|---|

| Revenue | $4.1B |

| Patients | ~2.0M |

| Sites | ~400+ |

| Episode cost reduction | 30–60% |

| Adherence gains | Double-digit% |

What is included in the product

Provides a concise SWOT analysis of Option Care Health, highlighting internal strengths and weaknesses alongside external opportunities and threats to assess its competitive position and strategic risks.

Provides a concise SWOT matrix tailored to Option Care Health for rapid identification of clinical, operational, and reimbursement risks and growth opportunities, ideal for executives needing a clear snapshot to align strategy quickly.

Weaknesses

Reimbursement and authorization complexity

Revenue relies on mixed medical and pharmacy benefit rules that vary by plan, creating billing complexity and unpredictable cash flow; prior authorizations and heavy documentation routinely delay patient starts of care and lengthen DSO timelines. Frequent denials and recertifications raise administrative costs and reduce operational efficiency, producing uneven margin visibility across therapies and payors.

Labor-intensive clinical model

Option Care Health's model depends on skilled nurses, pharmacists, and dietitians to safely deliver complex home and outpatient infusions, making labor central to service quality. Staffing shortages and reliance on overtime push unit costs higher; BLS projects registered nurse employment to grow 6% from 2022–2032, tightening supply. Training and credentialing commonly require 4–8 weeks per clinician, adding expense and ramp time, while limited clinician capacity constrains rapid scaling during demand spikes.

Working capital tied to high-cost drugs

Option Care's working capital is heavily tied to specialty medications, which account for about 55% of US drug spend (IQVIA 2024) and can cost tens to hundreds of thousands per course, requiring large inventory and tight procurement. Reimbursement lags of roughly 30–90 days commonly strain cash conversion cycles. Volatile drug prices compress pass-through margins, heightening sensitivity to payer mix and contract terms.

Operational complexity in home logistics

Coordinating compounding, cold-chain distribution and in-home scheduling raises operational complexity for Option Care Health (NASDAQ: OPCH), increasing route-planning inefficiencies, cancellations and supply variability that strain margins. Navigating 50-state licensure and home-care regulations adds administrative overhead and risk. Service incidents can erode patient trust and reduce referral volume.

- Nationwide operations: 50-state licensure burden

- Logistics: cold-chain + compounding increases costs

- Scheduling: route planning, cancellations drive inefficiency

- Reputation risk: incidents reduce referrals

Limited diversification beyond infusion

Concentration in infusion care heightens exposure to therapy and policy shifts; Option Care Health reported $5.13 billion revenue in 2023 with infusion services comprising the majority of net sales, leaving results sensitive to drug mix and Medicare policy changes. Cross-selling outside core services is constrained by limited adjacent offerings, reducing revenue optionality versus diversified post-acute peers. Geographic and service-line concentration amplifies risk from local reimbursement pressure and clinic closures, narrowing strategic flexibility.

- High reliance: 2023 revenue $5.13B — majority from infusion

- Cross-sell limited: fewer non-infusion services

- Concentration risk: local reimbursement exposure

- Lower optionality vs broader post-acute platforms

Care delivery under strain: specialty drug exposure, payment lags and workforce bottlenecks

Revenue and cash flow are pressured by mixed benefit rules, prior‑auth delays and 30–90 day reimbursement lags; 2023 revenue $5.13B with specialty drugs driving exposure (IQVIA 2024 ~55% of US drug spend). Labor dependence raises costs amid a projected 6% RN supply growth (BLS 2022–32) and 4–8 week credentialing. Cold‑chain, compounding and 50‑state licensure heighten cancellations, route inefficiency and reputational risk.

| Metric | Value |

|---|---|

| 2023 revenue | $5.13B |

| Specialty drug exposure | ~55% (IQVIA 2024) |

| Reimbursement lag | 30–90 days |

| RN supply growth | 6% (BLS 2022–32) |

| Credentialing time | 4–8 weeks |

What You See Is What You Get

Option Care Health SWOT Analysis

This is the actual Option Care Health SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, with strengths, weaknesses, opportunities, and threats clearly outlined. Purchase unlocks the complete, editable version ready for download and immediate use.