Orbit Garant Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

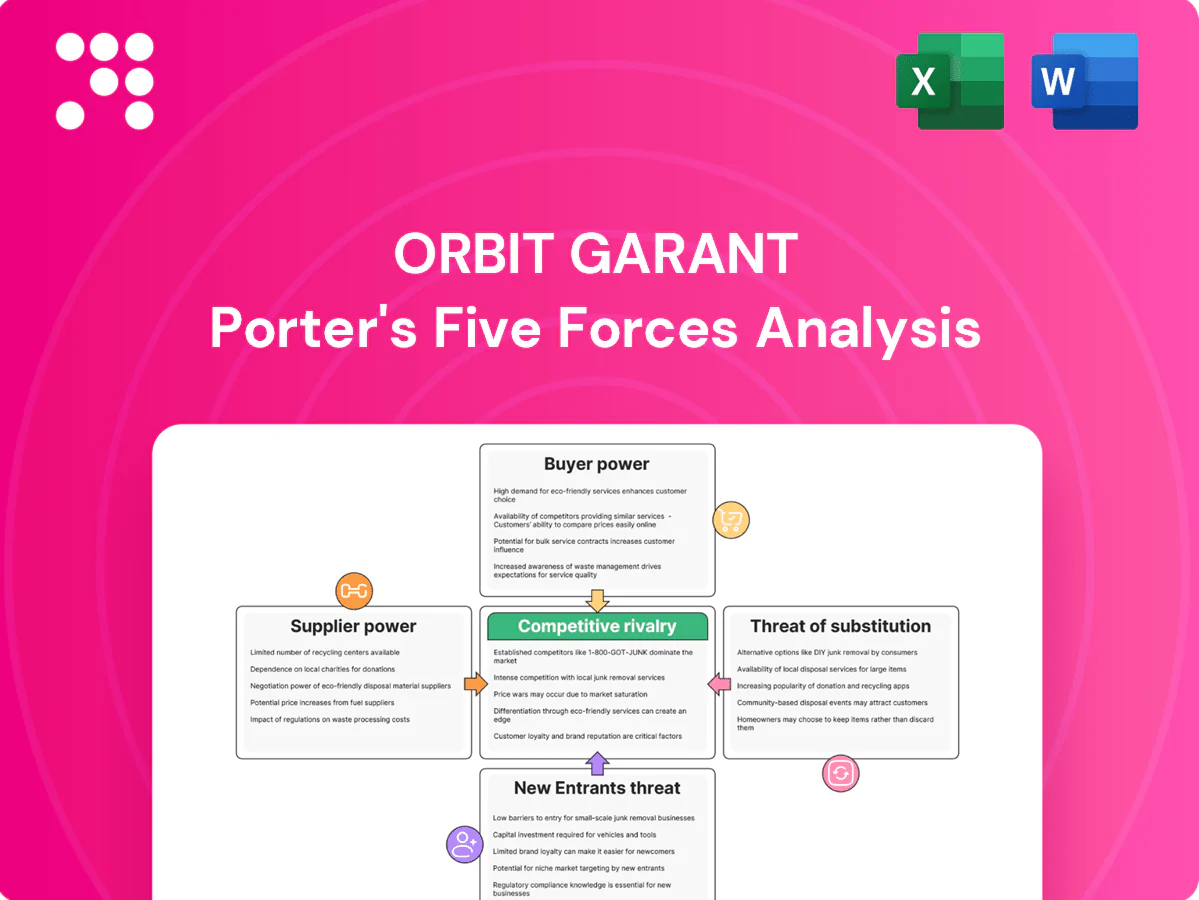

Orbit Garant’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer pressures, substitute threats, and entry barriers, offering a clear view of near‑term risks and advantages. This brief overview frames strategic priorities but omits detailed ratings, visuals, and scenario analysis. Unlock the full Porter's Five Forces Analysis to access force‑by‑force scores, data‑driven implications, and actionable recommendations for investment or strategy decisions.

Suppliers Bargaining Power

Critical equipment OEM concentration

Core rigs and underground drill systems come from a few OEMs (notably Epiroc and Sandvik), concentrating pricing power and typical lead times of 3–12 months for bespoke units; supplier consolidation among specialist rig and tooling makers has tightened commercial terms. Multi-brand fleets and robust second-hand markets (used units often cost 30–50% less) partly offset dependence, while service agreements and stocked parts cut downtime but lock in recurring spend.

Consumables and parts volatility

Bits, rods, drilling fluids and wear parts drive recurring costs and track commodity and logistics swings — with Brent averaging about $85/bbl in 2024, base-oil linked mud costs rose materially. Bulk purchasing and standardization can secure discounts (commonly 5–15%) but switching specs mid-contract incurs requalification and downtime penalties. Vendor-managed inventory improves availability but typically reduces supplier margin capture. Global supply-chain shocks can temporarily elevate supplier leverage.

Fuel and energy dependence

Fuel dependence remains critical in 2024: diesel price volatility directly compresses job-level margins and forces surcharges, with many contracts indexing surcharges to published diesel indices. Remote site logistics concentrate buying power in local distributors, limiting alternatives. Hedging programs and contractual fuel escalators enable partial pass-through of spikes. Underground electrification can cut diesel exposure but needs significant capex and client alignment to implement.

Skilled labor as a quasi-supplier

Experienced drillers and maintenance technicians become scarce in upcycles, giving labor agencies and unions leverage; a 2024 industry survey found 68% of upstream firms reporting technician shortages, driving wage inflation and retention bonuses as utilization rises. Building in-house training pipelines mitigates dependence but requires 12–24 months to yield skilled crews. Strong safety culture and clear career paths reduce turnover-driven supplier power.

- Skilled shortage: 68% (2024 survey)

- Training lead time: 12–24 months

- Cost pressure: wage inflation + retention bonuses

- Mitigants: safety culture, career paths, internal training

Digital systems and telemetry lock-in

Proprietary data capture, rig telemetry, and software subscriptions create switching costs that entrench suppliers; integration into client reporting standards amplifies lock-in and bargaining power. Open APIs and in-house analytics implemented in 2024 are reducing dependency by enabling data portability and vendor comparison. Cybersecurity requirements and uptime SLAs add negotiation complexity and can raise total cost of ownership.

- Proprietary telemetry: increases switching costs

- Integration with client reporting: deepens vendor entrenchment

- Open APIs/internal analytics: lower dependency

- Cybersecurity & SLAs: escalate negotiation and costs

High supplier power: long OEM lead times, 68% tech shortage, used rigs 30-50% cheaper

Supplier power is high: core rigs concentrated with OEMs like Epiroc and Sandvik and 3–12 month lead times; specialist consolidation tightens terms. Recurring parts and fluids track commodity swings (Brent ~ $85/bbl in 2024); used rigs 30–50% cheaper and bulk discounts 5–15% mitigate. Technician shortage (68% 2024) and telemetry lock-in raise switching costs; open APIs reduce dependence.

| Item | Metric | 2024 |

|---|---|---|

| OEM concentration | Lead time | 3–12 months |

| Brent | Price | $85/bbl |

| Technician shortage | Survey | 68% |

| Used rigs | Price delta | 30–50% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, substitutes, and entry risks tailored exclusively to Orbit Garant. Detailed, data-supported evaluation of each Porter’s force highlighting disruptive threats, pricing levers, and protective market dynamics; delivered in fully editable Word format for use in investor materials, strategy decks, or academic projects.

Orbit Garant Porter's Five Forces delivers a clean one-sheet summary with customizable pressure levels and instant spider/radar visualization—ready to drop into decks, integrate into dashboards, and use without macros for fast, non-technical decision-making.

Customers Bargaining Power

Concentrated mining customer base

Large producers award multi-year, multi-site tenders—top five miners controlled roughly 40% of key seaborne ore/copper markets in 2024—consolidating customer leverage. Buyers extract price concessions and stricter KPIs, with many contracts spanning 3–5 years and often exceeding $100m. Diversification across commodities/geographies reduces single-buyer risk. Strong performance (eg 95% uptime, safety TRIFR targets) remains critical for renewal.

Cyclical demand and tendering pressure

Downcycles trigger aggressive rebids and shorter terms, amplifying buyer leverage as customers push renewals and spot bids; in offshore services this can compress contract lengths toward 6–12 months and force price cuts. Upcycles shift power back as capacity tightens, supporting dayrates—fuel and consumables, which can comprise up to 20% of OPEX, often drive escalators. Clients demand rate cards with input-linked escalators; flex clauses on mobilization/demobilization fees (commonly 3–10% of contract value) are key negotiation points.

Ability to insource drilling

Larger miners increasingly maintain internal drilling teams for core programs, creating a credible alternative that pressures external pricing and shifts procurement toward reliability and safety; industry estimates put the global contract drilling services market at about $18.5 billion in 2024, highlighting the scale of potential insourcing impact. Outsourcing stays attractive for directional, deep-hole work and peak loads, while hybrid models obscure Orbit Garant’s volume visibility and forecasting.

High switching ease between contractors

- Vendor rotation >40% in 2024 tenders

- Mobilization time: weeks–months

- HSE/productivity data raise retention

- Performance guarantees with penalties now common

Data and ESG reporting demands

Clients now demand granular productivity, environmental and safety reporting, raising compliance costs; the EU Corporate Sustainability Reporting Directive expanded scope in 2024. Meeting ESG targets is often decisive in awards, while buyers push technology adoption without full compensation. Measurable footprint and incident reductions enable premium pricing.

- Reporting: CSRD expansion 2024

- Costs: higher compliance burden

- Procurement: ESG can decide awards

- Pricing: proven reductions justify premiums

Buyers wield leverage; Top-5 ~40%; vendor rotation >40%

Buyers wield strong leverage—top five miners held ~40% seaborne ore/copper demand in 2024, driving multi-year tenders (3–5y, often >$100m) and strict KPIs. Downcycles shorten terms to 6–12m and force cuts; upcycles restore dayrates. Vendor rotation exceeded 40% in 2024; mobilization typically takes weeks–months. ESG/CSRD 2024 reporting now decisive in awards.

| Metric | 2024 |

|---|---|

| Top-5 market share | ~40% |

| Market size (contract drilling) | $18.5bn |

| Vendor rotation | >40% |

| Typical tender length | 3–5 years |

Full Version Awaits

Orbit Garant Porter's Five Forces Analysis

This preview shows the exact Orbit Garant Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is the final deliverable, exactly as provided to customers.

Go Beyond the Preview—Access the Full Strategic Report

Orbit Garant’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer pressures, substitute threats, and entry barriers, offering a clear view of near‑term risks and advantages. This brief overview frames strategic priorities but omits detailed ratings, visuals, and scenario analysis. Unlock the full Porter's Five Forces Analysis to access force‑by‑force scores, data‑driven implications, and actionable recommendations for investment or strategy decisions.

Suppliers Bargaining Power

Critical equipment OEM concentration

Core rigs and underground drill systems come from a few OEMs (notably Epiroc and Sandvik), concentrating pricing power and typical lead times of 3–12 months for bespoke units; supplier consolidation among specialist rig and tooling makers has tightened commercial terms. Multi-brand fleets and robust second-hand markets (used units often cost 30–50% less) partly offset dependence, while service agreements and stocked parts cut downtime but lock in recurring spend.

Consumables and parts volatility

Bits, rods, drilling fluids and wear parts drive recurring costs and track commodity and logistics swings — with Brent averaging about $85/bbl in 2024, base-oil linked mud costs rose materially. Bulk purchasing and standardization can secure discounts (commonly 5–15%) but switching specs mid-contract incurs requalification and downtime penalties. Vendor-managed inventory improves availability but typically reduces supplier margin capture. Global supply-chain shocks can temporarily elevate supplier leverage.

Fuel and energy dependence

Fuel dependence remains critical in 2024: diesel price volatility directly compresses job-level margins and forces surcharges, with many contracts indexing surcharges to published diesel indices. Remote site logistics concentrate buying power in local distributors, limiting alternatives. Hedging programs and contractual fuel escalators enable partial pass-through of spikes. Underground electrification can cut diesel exposure but needs significant capex and client alignment to implement.

Skilled labor as a quasi-supplier

Experienced drillers and maintenance technicians become scarce in upcycles, giving labor agencies and unions leverage; a 2024 industry survey found 68% of upstream firms reporting technician shortages, driving wage inflation and retention bonuses as utilization rises. Building in-house training pipelines mitigates dependence but requires 12–24 months to yield skilled crews. Strong safety culture and clear career paths reduce turnover-driven supplier power.

- Skilled shortage: 68% (2024 survey)

- Training lead time: 12–24 months

- Cost pressure: wage inflation + retention bonuses

- Mitigants: safety culture, career paths, internal training

Digital systems and telemetry lock-in

Proprietary data capture, rig telemetry, and software subscriptions create switching costs that entrench suppliers; integration into client reporting standards amplifies lock-in and bargaining power. Open APIs and in-house analytics implemented in 2024 are reducing dependency by enabling data portability and vendor comparison. Cybersecurity requirements and uptime SLAs add negotiation complexity and can raise total cost of ownership.

- Proprietary telemetry: increases switching costs

- Integration with client reporting: deepens vendor entrenchment

- Open APIs/internal analytics: lower dependency

- Cybersecurity & SLAs: escalate negotiation and costs

High supplier power: long OEM lead times, 68% tech shortage, used rigs 30-50% cheaper

Supplier power is high: core rigs concentrated with OEMs like Epiroc and Sandvik and 3–12 month lead times; specialist consolidation tightens terms. Recurring parts and fluids track commodity swings (Brent ~ $85/bbl in 2024); used rigs 30–50% cheaper and bulk discounts 5–15% mitigate. Technician shortage (68% 2024) and telemetry lock-in raise switching costs; open APIs reduce dependence.

| Item | Metric | 2024 |

|---|---|---|

| OEM concentration | Lead time | 3–12 months |

| Brent | Price | $85/bbl |

| Technician shortage | Survey | 68% |

| Used rigs | Price delta | 30–50% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, substitutes, and entry risks tailored exclusively to Orbit Garant. Detailed, data-supported evaluation of each Porter’s force highlighting disruptive threats, pricing levers, and protective market dynamics; delivered in fully editable Word format for use in investor materials, strategy decks, or academic projects.

Orbit Garant Porter's Five Forces delivers a clean one-sheet summary with customizable pressure levels and instant spider/radar visualization—ready to drop into decks, integrate into dashboards, and use without macros for fast, non-technical decision-making.

Customers Bargaining Power

Concentrated mining customer base

Large producers award multi-year, multi-site tenders—top five miners controlled roughly 40% of key seaborne ore/copper markets in 2024—consolidating customer leverage. Buyers extract price concessions and stricter KPIs, with many contracts spanning 3–5 years and often exceeding $100m. Diversification across commodities/geographies reduces single-buyer risk. Strong performance (eg 95% uptime, safety TRIFR targets) remains critical for renewal.

Cyclical demand and tendering pressure

Downcycles trigger aggressive rebids and shorter terms, amplifying buyer leverage as customers push renewals and spot bids; in offshore services this can compress contract lengths toward 6–12 months and force price cuts. Upcycles shift power back as capacity tightens, supporting dayrates—fuel and consumables, which can comprise up to 20% of OPEX, often drive escalators. Clients demand rate cards with input-linked escalators; flex clauses on mobilization/demobilization fees (commonly 3–10% of contract value) are key negotiation points.

Ability to insource drilling

Larger miners increasingly maintain internal drilling teams for core programs, creating a credible alternative that pressures external pricing and shifts procurement toward reliability and safety; industry estimates put the global contract drilling services market at about $18.5 billion in 2024, highlighting the scale of potential insourcing impact. Outsourcing stays attractive for directional, deep-hole work and peak loads, while hybrid models obscure Orbit Garant’s volume visibility and forecasting.

High switching ease between contractors

- Vendor rotation >40% in 2024 tenders

- Mobilization time: weeks–months

- HSE/productivity data raise retention

- Performance guarantees with penalties now common

Data and ESG reporting demands

Clients now demand granular productivity, environmental and safety reporting, raising compliance costs; the EU Corporate Sustainability Reporting Directive expanded scope in 2024. Meeting ESG targets is often decisive in awards, while buyers push technology adoption without full compensation. Measurable footprint and incident reductions enable premium pricing.

- Reporting: CSRD expansion 2024

- Costs: higher compliance burden

- Procurement: ESG can decide awards

- Pricing: proven reductions justify premiums

Buyers wield leverage; Top-5 ~40%; vendor rotation >40%

Buyers wield strong leverage—top five miners held ~40% seaborne ore/copper demand in 2024, driving multi-year tenders (3–5y, often >$100m) and strict KPIs. Downcycles shorten terms to 6–12m and force cuts; upcycles restore dayrates. Vendor rotation exceeded 40% in 2024; mobilization typically takes weeks–months. ESG/CSRD 2024 reporting now decisive in awards.

| Metric | 2024 |

|---|---|

| Top-5 market share | ~40% |

| Market size (contract drilling) | $18.5bn |

| Vendor rotation | >40% |

| Typical tender length | 3–5 years |

Full Version Awaits

Orbit Garant Porter's Five Forces Analysis

This preview shows the exact Orbit Garant Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is the final deliverable, exactly as provided to customers.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Orbit Garant’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer pressures, substitute threats, and entry barriers, offering a clear view of near‑term risks and advantages. This brief overview frames strategic priorities but omits detailed ratings, visuals, and scenario analysis. Unlock the full Porter's Five Forces Analysis to access force‑by‑force scores, data‑driven implications, and actionable recommendations for investment or strategy decisions.

Suppliers Bargaining Power

Critical equipment OEM concentration

Core rigs and underground drill systems come from a few OEMs (notably Epiroc and Sandvik), concentrating pricing power and typical lead times of 3–12 months for bespoke units; supplier consolidation among specialist rig and tooling makers has tightened commercial terms. Multi-brand fleets and robust second-hand markets (used units often cost 30–50% less) partly offset dependence, while service agreements and stocked parts cut downtime but lock in recurring spend.

Consumables and parts volatility

Bits, rods, drilling fluids and wear parts drive recurring costs and track commodity and logistics swings — with Brent averaging about $85/bbl in 2024, base-oil linked mud costs rose materially. Bulk purchasing and standardization can secure discounts (commonly 5–15%) but switching specs mid-contract incurs requalification and downtime penalties. Vendor-managed inventory improves availability but typically reduces supplier margin capture. Global supply-chain shocks can temporarily elevate supplier leverage.

Fuel and energy dependence

Fuel dependence remains critical in 2024: diesel price volatility directly compresses job-level margins and forces surcharges, with many contracts indexing surcharges to published diesel indices. Remote site logistics concentrate buying power in local distributors, limiting alternatives. Hedging programs and contractual fuel escalators enable partial pass-through of spikes. Underground electrification can cut diesel exposure but needs significant capex and client alignment to implement.

Skilled labor as a quasi-supplier

Experienced drillers and maintenance technicians become scarce in upcycles, giving labor agencies and unions leverage; a 2024 industry survey found 68% of upstream firms reporting technician shortages, driving wage inflation and retention bonuses as utilization rises. Building in-house training pipelines mitigates dependence but requires 12–24 months to yield skilled crews. Strong safety culture and clear career paths reduce turnover-driven supplier power.

- Skilled shortage: 68% (2024 survey)

- Training lead time: 12–24 months

- Cost pressure: wage inflation + retention bonuses

- Mitigants: safety culture, career paths, internal training

Digital systems and telemetry lock-in

Proprietary data capture, rig telemetry, and software subscriptions create switching costs that entrench suppliers; integration into client reporting standards amplifies lock-in and bargaining power. Open APIs and in-house analytics implemented in 2024 are reducing dependency by enabling data portability and vendor comparison. Cybersecurity requirements and uptime SLAs add negotiation complexity and can raise total cost of ownership.

- Proprietary telemetry: increases switching costs

- Integration with client reporting: deepens vendor entrenchment

- Open APIs/internal analytics: lower dependency

- Cybersecurity & SLAs: escalate negotiation and costs

High supplier power: long OEM lead times, 68% tech shortage, used rigs 30-50% cheaper

Supplier power is high: core rigs concentrated with OEMs like Epiroc and Sandvik and 3–12 month lead times; specialist consolidation tightens terms. Recurring parts and fluids track commodity swings (Brent ~ $85/bbl in 2024); used rigs 30–50% cheaper and bulk discounts 5–15% mitigate. Technician shortage (68% 2024) and telemetry lock-in raise switching costs; open APIs reduce dependence.

| Item | Metric | 2024 |

|---|---|---|

| OEM concentration | Lead time | 3–12 months |

| Brent | Price | $85/bbl |

| Technician shortage | Survey | 68% |

| Used rigs | Price delta | 30–50% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, substitutes, and entry risks tailored exclusively to Orbit Garant. Detailed, data-supported evaluation of each Porter’s force highlighting disruptive threats, pricing levers, and protective market dynamics; delivered in fully editable Word format for use in investor materials, strategy decks, or academic projects.

Orbit Garant Porter's Five Forces delivers a clean one-sheet summary with customizable pressure levels and instant spider/radar visualization—ready to drop into decks, integrate into dashboards, and use without macros for fast, non-technical decision-making.

Customers Bargaining Power

Concentrated mining customer base

Large producers award multi-year, multi-site tenders—top five miners controlled roughly 40% of key seaborne ore/copper markets in 2024—consolidating customer leverage. Buyers extract price concessions and stricter KPIs, with many contracts spanning 3–5 years and often exceeding $100m. Diversification across commodities/geographies reduces single-buyer risk. Strong performance (eg 95% uptime, safety TRIFR targets) remains critical for renewal.

Cyclical demand and tendering pressure

Downcycles trigger aggressive rebids and shorter terms, amplifying buyer leverage as customers push renewals and spot bids; in offshore services this can compress contract lengths toward 6–12 months and force price cuts. Upcycles shift power back as capacity tightens, supporting dayrates—fuel and consumables, which can comprise up to 20% of OPEX, often drive escalators. Clients demand rate cards with input-linked escalators; flex clauses on mobilization/demobilization fees (commonly 3–10% of contract value) are key negotiation points.

Ability to insource drilling

Larger miners increasingly maintain internal drilling teams for core programs, creating a credible alternative that pressures external pricing and shifts procurement toward reliability and safety; industry estimates put the global contract drilling services market at about $18.5 billion in 2024, highlighting the scale of potential insourcing impact. Outsourcing stays attractive for directional, deep-hole work and peak loads, while hybrid models obscure Orbit Garant’s volume visibility and forecasting.

High switching ease between contractors

- Vendor rotation >40% in 2024 tenders

- Mobilization time: weeks–months

- HSE/productivity data raise retention

- Performance guarantees with penalties now common

Data and ESG reporting demands

Clients now demand granular productivity, environmental and safety reporting, raising compliance costs; the EU Corporate Sustainability Reporting Directive expanded scope in 2024. Meeting ESG targets is often decisive in awards, while buyers push technology adoption without full compensation. Measurable footprint and incident reductions enable premium pricing.

- Reporting: CSRD expansion 2024

- Costs: higher compliance burden

- Procurement: ESG can decide awards

- Pricing: proven reductions justify premiums

Buyers wield leverage; Top-5 ~40%; vendor rotation >40%

Buyers wield strong leverage—top five miners held ~40% seaborne ore/copper demand in 2024, driving multi-year tenders (3–5y, often >$100m) and strict KPIs. Downcycles shorten terms to 6–12m and force cuts; upcycles restore dayrates. Vendor rotation exceeded 40% in 2024; mobilization typically takes weeks–months. ESG/CSRD 2024 reporting now decisive in awards.

| Metric | 2024 |

|---|---|

| Top-5 market share | ~40% |

| Market size (contract drilling) | $18.5bn |

| Vendor rotation | >40% |

| Typical tender length | 3–5 years |

Full Version Awaits

Orbit Garant Porter's Five Forces Analysis

This preview shows the exact Orbit Garant Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is the final deliverable, exactly as provided to customers.