Organon PESTLE Analysis

Skip the Research. Get the Strategy.

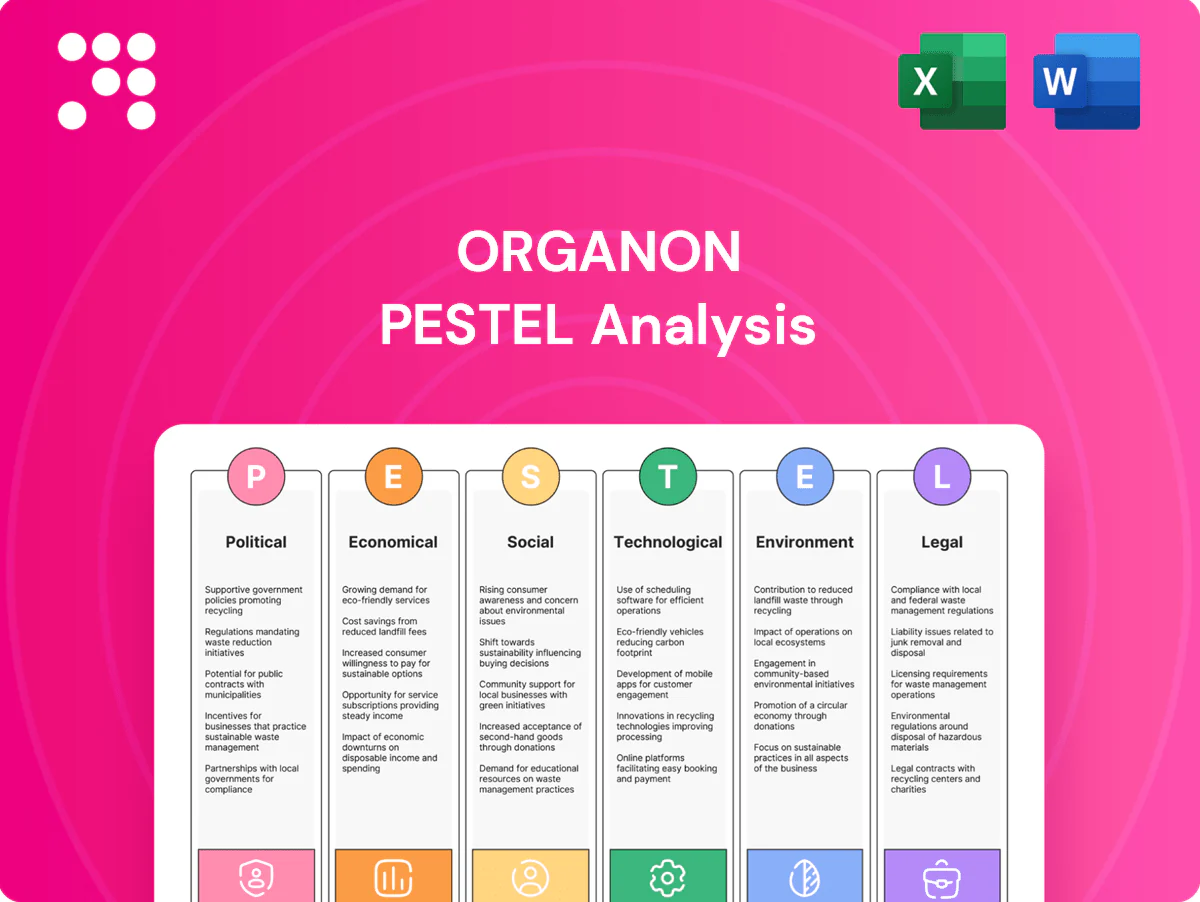

Discover how political, economic, social, technological, legal and environmental forces are shaping Organon's strategic outlook in our concise PESTLE snapshot. Ideal for investors and strategists, it highlights risks and opportunities you can't ignore. Purchase the full PESTLE analysis for the complete, actionable breakdown ready for immediate use.

Political factors

Women's health policy priorities

Government agendas that elevate women's health can unlock grants, reimbursement and public-private partnerships, improving market access for contraception, fertility and menopause therapies. UNFPA estimates 218 million women in developing regions have unmet need for modern contraception, so policy prioritization and election cycles materially influence pipeline focus and payer decisions. Organon can align advocacy to secure inclusion in national plans and consistent engagement with health ministries mitigates policy volatility.

Reproductive rights and access

Legislative shifts on reproductive care directly reshape demand and distribution: Guttmacher estimates 26 US states enacted major post-Dobbs restrictions while WHO reports about 214 million women in low‑ and middle‑income countries have unmet need for contraception, altering channel dynamics. Restrictions fragment access, raise compliance costs, and shift product mix toward long‑acting or telehealth solutions. Liberalization expands addressable markets for contraception and maternal health, increasing TAM. Organon must map jurisdictional variability in labeling, distribution, and patient support to manage regulatory and commercial risk.

Drug pricing and reimbursement reforms

Value-based pricing, reference pricing and expanding government negotiation powers (eg US Medicare negotiation program rolling from 2026) compress margins across portfolios, often forcing price cuts of 5–20% at launch. Biosimilar uptake is policy-driven, with EU markets seeing biosimilar shares of 30–70% within 12 months post-entry, changing tender wins and penetration speed. Established brands face recurring price erosions under cost-containment mandates; robust health-economic evidence (eg NICE thresholds £20–30k/QALY) is critical to secure and sustain reimbursement.

Trade, tariffs, and localization

Supply chains for APIs and biologics face tariffs and local content rules across key markets, prompting Organon to weigh in-country manufacturing; India expanded production-linked incentives for bulk drugs in 2023, boosting localization for public tenders. Export controls and sanctions (eg Russia, Iran) constrain market access, so diversified sourcing and regional production reduce policy risk.

- Tariffs/local content: drive localization

- PLI expansions (India 2023): favor domestic plants

- Sanctions/export controls: limit markets, increase compliance costs

- Diversified sourcing/regional production: mitigates policy exposure

Public procurement dynamics

- Tender structures: national vs regional

- Single-winner auctions: rapid volume shifts

- Price impact: 15–35% compression (2024)

- Multi-year frameworks: demand stability

- RWE: boosts competitive positioning

Women's health prioritization, policy shifts and price pressure reshape access

Government prioritization of women’s health (UNFPA 218m unmet contraception need) opens grants, reimbursement and partnerships; election cycles materially shift pipeline focus. Post‑Dobbs/regulatory changes (26 US states with major restrictions) and expanding payer negotiation powers (US Medicare negotiation from 2026) reshape market access. Price pressure (5–20% launch cuts; tenders compress 15–35%) and biosimilar uptake (30–70% EU share) force localization and RWE-driven tendering.

| Indicator | Value |

|---|---|

| Unmet contraception need | 218m (UNFPA) |

| US restrictions | 26 states |

| Medicare negotiation | From 2026 |

| Price pressure | 5–20% launch; 15–35% tenders |

| Biosimilar uptake EU | 30–70% |

What is included in the product

Explores how macro-environmental factors uniquely affect Organon across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it offers forward-looking insights, scenario-ready findings, and insertion-ready formatting for plans and decks.

A concise, visually segmented PESTLE summary for Organon that’s easy to drop into presentations, shareable across teams, and editable for regional or portfolio-specific notes—ideal for quick alignment and risk discussions during strategic planning.

Economic factors

Macroeconomic volatility

Rising inflation and higher interest rates (US fed funds ~5.25–5.50% in mid‑2025) increase input costs, working capital carrying costs and constrain capital allocation for Organon. Economic slowdown (IMF world GDP ~3.2% in 2025) tightens healthcare budgets, pressuring prices and volumes. Currency volatility and USD strength in 2024–25 amplify reported FX swings and import costs. Active hedging and tight cost discipline are used to protect margins.

Payer mix and affordability

Out-of-pocket burdens strongly influence contraceptive and fertility product uptake, with WHO/UN estimates indicating about 218 million women in low- and middle-income countries have unmet need for contraception. US policy changes—notably ACA-mandated contraceptive coverage since 2013—have been linked to higher adherence and persistence. Tiering and copay structures steer product choice, while patient-assistance programs sustain volumes where affordability gaps persist.

Biosimilar price competition

Biosimilar entry has driven price erosion—European tenders commonly yield discounts of 30–70% versus originators and hospital/tender wins can push net prices 50–90% lower, enabling rapid switching; IQVIA and health-system analyses cite cumulative biosimilar savings in the tens of billions by 2023–24. Scale manufacturing and lean commercialization are decisive to protect margins, while bundled service offerings and patient-support programs can blunt pure price competition.

Portfolio lifecycle and LOE

Established brands typically lose 50–90% of sales within 12–24 months after loss of exclusivity (LOE), compressing cash flows; lifecycle management and line extensions commonly extend commercial relevance by 1–3 years, while disciplined SKU rationalization can boost margins by 100–300 basis points. Capital should rotate toward women's health and biosimilars as the biosimilars market is projected near $80 billion by 2028.

- LOE impact: 50–90% sales drop in 12–24 months

- Lifecycle lift: +1–3 years by line extensions

- Margin upside: SKU rationalization +100–300 bps

- Strategic capital: prioritize women's health, biosimilars (~$80B by 2028)

Emerging market growth

Rising incomes and urbanization in emerging markets (IMF 2024 EM growth ~4.1%; urban population ~56% in 2024) expand demand for women's health solutions, while currency volatility and payment delays (DSO often 60–90 days) strain cash conversion. Local partnerships speed registration and market access, but pricing must balance affordability with sustainable margins to protect profitability.

- IMF 2024 EM growth ~4.1%

- Urban population ~56% (2024)

- Typical DSO 60–90 days

- Local partnerships accelerate access

Women's health prioritization, policy shifts and price pressure reshape access

Higher inflation and US policy rates (~5.25–5.50% mid‑2025) raise input and capital costs while IMF projects world GDP ~3.2% (2025) constraining budgets; USD strength increases FX swings. 218M women in LMICs have unmet contraceptive need; biosimilars market ~$80B by 2028. LOE typically cuts sales 50–90%; DSO often 60–90 days.

| Metric | Value |

|---|---|

| US policy rate | 5.25–5.50% (mid‑2025) |

| World GDP (IMF) | ~3.2% (2025) |

| Unmet contraception | 218M women |

| Biosimilars | ~$80B by 2028 |

| LOE impact | 50–90% sales drop |

| DSO | 60–90 days |

Same Document Delivered

Organon PESTLE Analysis

The preview shown here is the exact Organon PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure are identical to the downloadable file. No placeholders or surprises.

Skip the Research. Get the Strategy.

Discover how political, economic, social, technological, legal and environmental forces are shaping Organon's strategic outlook in our concise PESTLE snapshot. Ideal for investors and strategists, it highlights risks and opportunities you can't ignore. Purchase the full PESTLE analysis for the complete, actionable breakdown ready for immediate use.

Political factors

Women's health policy priorities

Government agendas that elevate women's health can unlock grants, reimbursement and public-private partnerships, improving market access for contraception, fertility and menopause therapies. UNFPA estimates 218 million women in developing regions have unmet need for modern contraception, so policy prioritization and election cycles materially influence pipeline focus and payer decisions. Organon can align advocacy to secure inclusion in national plans and consistent engagement with health ministries mitigates policy volatility.

Reproductive rights and access

Legislative shifts on reproductive care directly reshape demand and distribution: Guttmacher estimates 26 US states enacted major post-Dobbs restrictions while WHO reports about 214 million women in low‑ and middle‑income countries have unmet need for contraception, altering channel dynamics. Restrictions fragment access, raise compliance costs, and shift product mix toward long‑acting or telehealth solutions. Liberalization expands addressable markets for contraception and maternal health, increasing TAM. Organon must map jurisdictional variability in labeling, distribution, and patient support to manage regulatory and commercial risk.

Drug pricing and reimbursement reforms

Value-based pricing, reference pricing and expanding government negotiation powers (eg US Medicare negotiation program rolling from 2026) compress margins across portfolios, often forcing price cuts of 5–20% at launch. Biosimilar uptake is policy-driven, with EU markets seeing biosimilar shares of 30–70% within 12 months post-entry, changing tender wins and penetration speed. Established brands face recurring price erosions under cost-containment mandates; robust health-economic evidence (eg NICE thresholds £20–30k/QALY) is critical to secure and sustain reimbursement.

Trade, tariffs, and localization

Supply chains for APIs and biologics face tariffs and local content rules across key markets, prompting Organon to weigh in-country manufacturing; India expanded production-linked incentives for bulk drugs in 2023, boosting localization for public tenders. Export controls and sanctions (eg Russia, Iran) constrain market access, so diversified sourcing and regional production reduce policy risk.

- Tariffs/local content: drive localization

- PLI expansions (India 2023): favor domestic plants

- Sanctions/export controls: limit markets, increase compliance costs

- Diversified sourcing/regional production: mitigates policy exposure

Public procurement dynamics

- Tender structures: national vs regional

- Single-winner auctions: rapid volume shifts

- Price impact: 15–35% compression (2024)

- Multi-year frameworks: demand stability

- RWE: boosts competitive positioning

Women's health prioritization, policy shifts and price pressure reshape access

Government prioritization of women’s health (UNFPA 218m unmet contraception need) opens grants, reimbursement and partnerships; election cycles materially shift pipeline focus. Post‑Dobbs/regulatory changes (26 US states with major restrictions) and expanding payer negotiation powers (US Medicare negotiation from 2026) reshape market access. Price pressure (5–20% launch cuts; tenders compress 15–35%) and biosimilar uptake (30–70% EU share) force localization and RWE-driven tendering.

| Indicator | Value |

|---|---|

| Unmet contraception need | 218m (UNFPA) |

| US restrictions | 26 states |

| Medicare negotiation | From 2026 |

| Price pressure | 5–20% launch; 15–35% tenders |

| Biosimilar uptake EU | 30–70% |

What is included in the product

Explores how macro-environmental factors uniquely affect Organon across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it offers forward-looking insights, scenario-ready findings, and insertion-ready formatting for plans and decks.

A concise, visually segmented PESTLE summary for Organon that’s easy to drop into presentations, shareable across teams, and editable for regional or portfolio-specific notes—ideal for quick alignment and risk discussions during strategic planning.

Economic factors

Macroeconomic volatility

Rising inflation and higher interest rates (US fed funds ~5.25–5.50% in mid‑2025) increase input costs, working capital carrying costs and constrain capital allocation for Organon. Economic slowdown (IMF world GDP ~3.2% in 2025) tightens healthcare budgets, pressuring prices and volumes. Currency volatility and USD strength in 2024–25 amplify reported FX swings and import costs. Active hedging and tight cost discipline are used to protect margins.

Payer mix and affordability

Out-of-pocket burdens strongly influence contraceptive and fertility product uptake, with WHO/UN estimates indicating about 218 million women in low- and middle-income countries have unmet need for contraception. US policy changes—notably ACA-mandated contraceptive coverage since 2013—have been linked to higher adherence and persistence. Tiering and copay structures steer product choice, while patient-assistance programs sustain volumes where affordability gaps persist.

Biosimilar price competition

Biosimilar entry has driven price erosion—European tenders commonly yield discounts of 30–70% versus originators and hospital/tender wins can push net prices 50–90% lower, enabling rapid switching; IQVIA and health-system analyses cite cumulative biosimilar savings in the tens of billions by 2023–24. Scale manufacturing and lean commercialization are decisive to protect margins, while bundled service offerings and patient-support programs can blunt pure price competition.

Portfolio lifecycle and LOE

Established brands typically lose 50–90% of sales within 12–24 months after loss of exclusivity (LOE), compressing cash flows; lifecycle management and line extensions commonly extend commercial relevance by 1–3 years, while disciplined SKU rationalization can boost margins by 100–300 basis points. Capital should rotate toward women's health and biosimilars as the biosimilars market is projected near $80 billion by 2028.

- LOE impact: 50–90% sales drop in 12–24 months

- Lifecycle lift: +1–3 years by line extensions

- Margin upside: SKU rationalization +100–300 bps

- Strategic capital: prioritize women's health, biosimilars (~$80B by 2028)

Emerging market growth

Rising incomes and urbanization in emerging markets (IMF 2024 EM growth ~4.1%; urban population ~56% in 2024) expand demand for women's health solutions, while currency volatility and payment delays (DSO often 60–90 days) strain cash conversion. Local partnerships speed registration and market access, but pricing must balance affordability with sustainable margins to protect profitability.

- IMF 2024 EM growth ~4.1%

- Urban population ~56% (2024)

- Typical DSO 60–90 days

- Local partnerships accelerate access

Women's health prioritization, policy shifts and price pressure reshape access

Higher inflation and US policy rates (~5.25–5.50% mid‑2025) raise input and capital costs while IMF projects world GDP ~3.2% (2025) constraining budgets; USD strength increases FX swings. 218M women in LMICs have unmet contraceptive need; biosimilars market ~$80B by 2028. LOE typically cuts sales 50–90%; DSO often 60–90 days.

| Metric | Value |

|---|---|

| US policy rate | 5.25–5.50% (mid‑2025) |

| World GDP (IMF) | ~3.2% (2025) |

| Unmet contraception | 218M women |

| Biosimilars | ~$80B by 2028 |

| LOE impact | 50–90% sales drop |

| DSO | 60–90 days |

Same Document Delivered

Organon PESTLE Analysis

The preview shown here is the exact Organon PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure are identical to the downloadable file. No placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Discover how political, economic, social, technological, legal and environmental forces are shaping Organon's strategic outlook in our concise PESTLE snapshot. Ideal for investors and strategists, it highlights risks and opportunities you can't ignore. Purchase the full PESTLE analysis for the complete, actionable breakdown ready for immediate use.

Political factors

Women's health policy priorities

Government agendas that elevate women's health can unlock grants, reimbursement and public-private partnerships, improving market access for contraception, fertility and menopause therapies. UNFPA estimates 218 million women in developing regions have unmet need for modern contraception, so policy prioritization and election cycles materially influence pipeline focus and payer decisions. Organon can align advocacy to secure inclusion in national plans and consistent engagement with health ministries mitigates policy volatility.

Reproductive rights and access

Legislative shifts on reproductive care directly reshape demand and distribution: Guttmacher estimates 26 US states enacted major post-Dobbs restrictions while WHO reports about 214 million women in low‑ and middle‑income countries have unmet need for contraception, altering channel dynamics. Restrictions fragment access, raise compliance costs, and shift product mix toward long‑acting or telehealth solutions. Liberalization expands addressable markets for contraception and maternal health, increasing TAM. Organon must map jurisdictional variability in labeling, distribution, and patient support to manage regulatory and commercial risk.

Drug pricing and reimbursement reforms

Value-based pricing, reference pricing and expanding government negotiation powers (eg US Medicare negotiation program rolling from 2026) compress margins across portfolios, often forcing price cuts of 5–20% at launch. Biosimilar uptake is policy-driven, with EU markets seeing biosimilar shares of 30–70% within 12 months post-entry, changing tender wins and penetration speed. Established brands face recurring price erosions under cost-containment mandates; robust health-economic evidence (eg NICE thresholds £20–30k/QALY) is critical to secure and sustain reimbursement.

Trade, tariffs, and localization

Supply chains for APIs and biologics face tariffs and local content rules across key markets, prompting Organon to weigh in-country manufacturing; India expanded production-linked incentives for bulk drugs in 2023, boosting localization for public tenders. Export controls and sanctions (eg Russia, Iran) constrain market access, so diversified sourcing and regional production reduce policy risk.

- Tariffs/local content: drive localization

- PLI expansions (India 2023): favor domestic plants

- Sanctions/export controls: limit markets, increase compliance costs

- Diversified sourcing/regional production: mitigates policy exposure

Public procurement dynamics

- Tender structures: national vs regional

- Single-winner auctions: rapid volume shifts

- Price impact: 15–35% compression (2024)

- Multi-year frameworks: demand stability

- RWE: boosts competitive positioning

Women's health prioritization, policy shifts and price pressure reshape access

Government prioritization of women’s health (UNFPA 218m unmet contraception need) opens grants, reimbursement and partnerships; election cycles materially shift pipeline focus. Post‑Dobbs/regulatory changes (26 US states with major restrictions) and expanding payer negotiation powers (US Medicare negotiation from 2026) reshape market access. Price pressure (5–20% launch cuts; tenders compress 15–35%) and biosimilar uptake (30–70% EU share) force localization and RWE-driven tendering.

| Indicator | Value |

|---|---|

| Unmet contraception need | 218m (UNFPA) |

| US restrictions | 26 states |

| Medicare negotiation | From 2026 |

| Price pressure | 5–20% launch; 15–35% tenders |

| Biosimilar uptake EU | 30–70% |

What is included in the product

Explores how macro-environmental factors uniquely affect Organon across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it offers forward-looking insights, scenario-ready findings, and insertion-ready formatting for plans and decks.

A concise, visually segmented PESTLE summary for Organon that’s easy to drop into presentations, shareable across teams, and editable for regional or portfolio-specific notes—ideal for quick alignment and risk discussions during strategic planning.

Economic factors

Macroeconomic volatility

Rising inflation and higher interest rates (US fed funds ~5.25–5.50% in mid‑2025) increase input costs, working capital carrying costs and constrain capital allocation for Organon. Economic slowdown (IMF world GDP ~3.2% in 2025) tightens healthcare budgets, pressuring prices and volumes. Currency volatility and USD strength in 2024–25 amplify reported FX swings and import costs. Active hedging and tight cost discipline are used to protect margins.

Payer mix and affordability

Out-of-pocket burdens strongly influence contraceptive and fertility product uptake, with WHO/UN estimates indicating about 218 million women in low- and middle-income countries have unmet need for contraception. US policy changes—notably ACA-mandated contraceptive coverage since 2013—have been linked to higher adherence and persistence. Tiering and copay structures steer product choice, while patient-assistance programs sustain volumes where affordability gaps persist.

Biosimilar price competition

Biosimilar entry has driven price erosion—European tenders commonly yield discounts of 30–70% versus originators and hospital/tender wins can push net prices 50–90% lower, enabling rapid switching; IQVIA and health-system analyses cite cumulative biosimilar savings in the tens of billions by 2023–24. Scale manufacturing and lean commercialization are decisive to protect margins, while bundled service offerings and patient-support programs can blunt pure price competition.

Portfolio lifecycle and LOE

Established brands typically lose 50–90% of sales within 12–24 months after loss of exclusivity (LOE), compressing cash flows; lifecycle management and line extensions commonly extend commercial relevance by 1–3 years, while disciplined SKU rationalization can boost margins by 100–300 basis points. Capital should rotate toward women's health and biosimilars as the biosimilars market is projected near $80 billion by 2028.

- LOE impact: 50–90% sales drop in 12–24 months

- Lifecycle lift: +1–3 years by line extensions

- Margin upside: SKU rationalization +100–300 bps

- Strategic capital: prioritize women's health, biosimilars (~$80B by 2028)

Emerging market growth

Rising incomes and urbanization in emerging markets (IMF 2024 EM growth ~4.1%; urban population ~56% in 2024) expand demand for women's health solutions, while currency volatility and payment delays (DSO often 60–90 days) strain cash conversion. Local partnerships speed registration and market access, but pricing must balance affordability with sustainable margins to protect profitability.

- IMF 2024 EM growth ~4.1%

- Urban population ~56% (2024)

- Typical DSO 60–90 days

- Local partnerships accelerate access

Women's health prioritization, policy shifts and price pressure reshape access

Higher inflation and US policy rates (~5.25–5.50% mid‑2025) raise input and capital costs while IMF projects world GDP ~3.2% (2025) constraining budgets; USD strength increases FX swings. 218M women in LMICs have unmet contraceptive need; biosimilars market ~$80B by 2028. LOE typically cuts sales 50–90%; DSO often 60–90 days.

| Metric | Value |

|---|---|

| US policy rate | 5.25–5.50% (mid‑2025) |

| World GDP (IMF) | ~3.2% (2025) |

| Unmet contraception | 218M women |

| Biosimilars | ~$80B by 2028 |

| LOE impact | 50–90% sales drop |

| DSO | 60–90 days |

Same Document Delivered

Organon PESTLE Analysis

The preview shown here is the exact Organon PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure are identical to the downloadable file. No placeholders or surprises.