Orgill Porter's Five Forces Analysis

Don't Miss the Bigger Picture

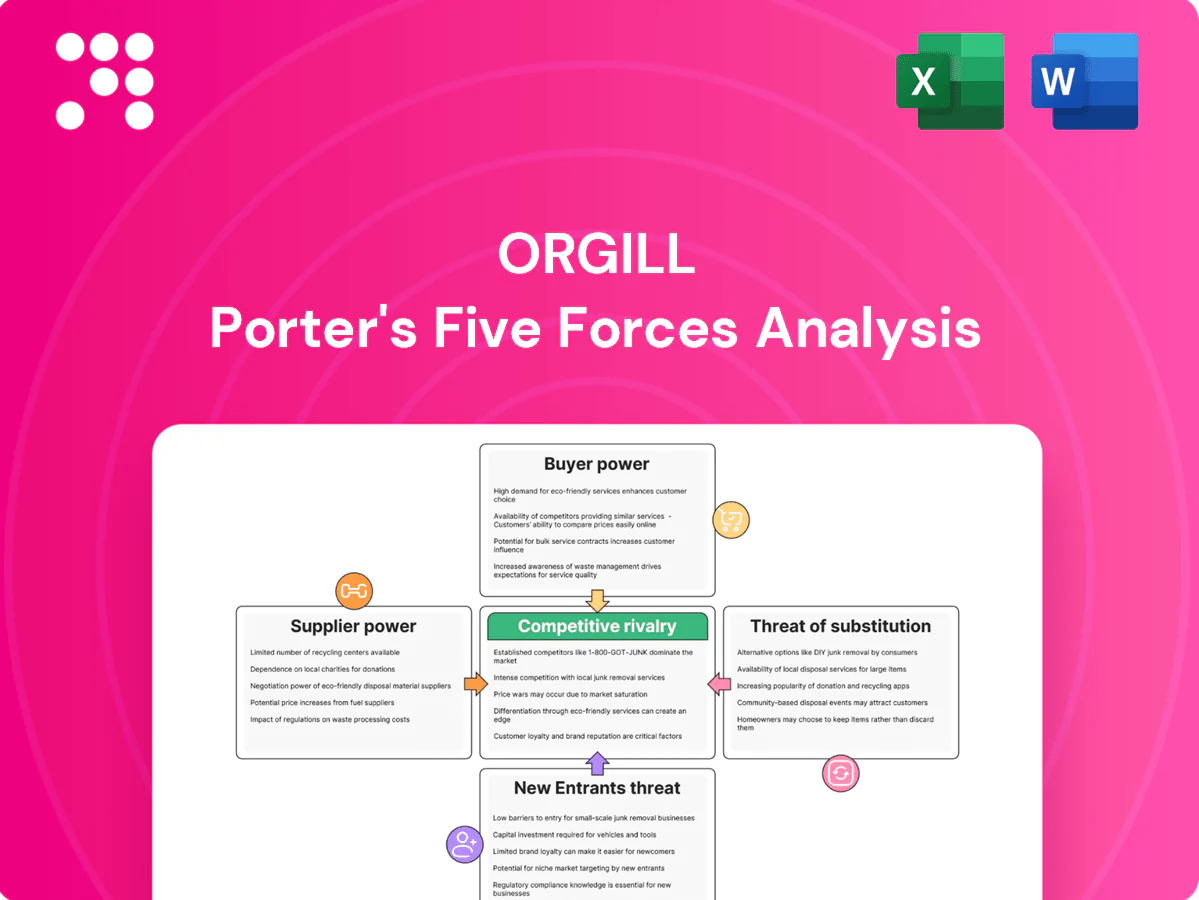

Orgill's Porter's Five Forces snapshot highlights supplier concentration, buyer bargaining, competitive rivalry, and threats from substitutes and new entrants—each shaping its distribution advantage and margin dynamics. The analysis shows how scale, supplier relationships, and retail fragmentation affect Orgill's pricing power. This brief preview points to strategic levers and risks. Unlock the full Porter's Five Forces Analysis to explore Orgill’s competitive dynamics in detail.

Suppliers Bargaining Power

Fragmented supplier base offsets power

As of 2024 Orgill sources from thousands of hardware and building-materials vendors, diluting any single supplier’s leverage and enabling multi-sourcing and rapid substitution when terms worsen. This supplier fragmentation supports competitive pricing across SKUs and allows procurement to pivot quickly, reducing disruption risk from any one manufacturer. The breadth of vendor relationships strengthens bargaining power in negotiations and supply continuity.

Concentrated brands hold leverage

In power tools, fasteners and paint, concentrated majors like Stanley Black & Decker, Bosch and Sherwin-Williams exert strong pull-through, constraining Orgill’s delisting options; global power tools market was valued around $35 billion in 2024, underscoring scale advantages. Orgill mitigates with private-labels and regional alternatives but cannot fully replace marquee SKUs. Co-marketing funds and volume rebates remain primary negotiation levers.

Scale and logistics give counterweight

Orgill, the world’s largest independent hardlines distributor, served over 6,000 independent retailers across 50+ countries and reported more than $3.2 billion in net sales in 2024, making it a preferred channel for suppliers. High fill-rate expectations and national promotions align supplier incentives with Orgill’s platform, while scale-based volume commitments secure better pricing and allocation in tight markets. Joint forecasting across Orgill’s DC network smooths production planning and reduces supplier uncertainty.

Commodity volatility pressures terms

- 10–30% 2024 commodity swings

- Index-linked pricing and cadence agreements

- Inventory buffering and hedging

- Private-label/spec flexibility

Switching and compliance costs curb power

Suppliers must integrate EDI, packaging, labeling, and Orgill service-level standards to win and keep business, and noncompliance chargebacks (often 1–3% of supplier sales in retail channels) plus performance scorecards sharply discipline negotiations. Orgill’s category management enforces shelf standards favoring reliable partners, and this operational rigor reduces supplier opportunism over time.

- EDI & standards: mandatory integration

- Chargebacks: commonly 1–3% of sales

- Category management: favors consistent partners

Distributor scale: $3.2B, 6,000+ retailers; 10-30% commodity swings, index-linked pricing

Orgill’s thousands of vendors dilute supplier leverage, enabling multi-sourcing and quick substitution; 2024 net sales ~$3.2B across 6,000+ retailers strengthen Orgill’s bargaining. Major suppliers in power tools/paint (global power tools market ~$35B in 2024) limit delisting options; Orgill offsets via private-labels, rebates and forecasting. Commodity input swings of 10–30% in 2024 drove index-linked pricing, buffering and selective hedging.

| Metric | 2024 Value |

|---|---|

| Net sales | $3.2B |

| Retailers served | 6,000+ |

| Commodity swings | 10–30% |

| Power tools market | $35B |

What is included in the product

Tailored Porter's Five Forces analysis for Orgill that uncovers competitive intensity, supplier and buyer power, substitute threats, and entry barriers, highlighting disruptive trends and strategic levers to protect market share and improve profitability.

Orgill Porter's Five Forces gives a one-sheet, customizable view of competitive pressure—instantly highlighting strategic risks and opportunities for quick, data-driven decisions and easy slide-ready summaries.

Customers Bargaining Power

Independent retailers are price sensitive

Independent hardware and lumber dealers operate on razor-thin net margins—about 3% on average in 2024 per industry reports—and press distributors hard on unit cost, dating, and payment terms. Volume tiers, rebates and promotional dating drive basket wins; suppliers must offer clear tiers and incentive math. Orgill, a leading distributor with roughly $5.1 billion in FY2023 sales, must justify total cost of ownership through superior fill rates and turns as online price transparency (e‑commerce ~18% of home improvement in 2024) intensifies buyer scrutiny.

Switching costs via programs

Orgill locks in over 6,000 independent retailers via integrated marketing, POS links, planograms and inventory-management services, creating significant switching costs. Converting assortments and migrating POS/data to another wholesaler is costly and risky, often disrupting sales and inventory flow. Orgill leverages these services to reduce churn, so high service quality directly weakens buyer bargaining power.

Alternative wholesalers raise leverage

Retailers can pit Orgill against three major peers—Ace, True Value and Do it Best—and regional distributors, leveraging alternative wholesalers to extract better terms.

Competitive bids on core assortments compress net pricing and freight margins, forcing Orgill to defend with service economics.

Differentiation shifts to fill rate, delivery frequency and promotional support, areas where Orgill’s network serving over 10,000 independents is tested.

Rebates and exclusive SKUs are used to defend share and stabilize retailer loyalty.

End-customer channel leakage

Retailers face intense channel leakage to big-box and online players—Home Depot and Lowe's together exceeded roughly 250 billion USD in 2024, forcing independent buyers to demand sharper wholesale economics, drop-ship, special orders and long-tail access.

- Orgill breadth captures special buys, reducing defection

- Data on local demand improves SKU-level margins

- Drop-ship support limits retailer margin squeeze

Buyer size heterogeneity

Larger chains and multi-store dealers negotiate stronger terms with Orgill by leveraging consolidated volumes, while small independents typically accept standard pricing in exchange for turnkey merchandising and support. Orgill’s tiered service model balances margin preservation with retention by differentiating fulfillment, marketing and credit terms. National accounts frequently trade higher discounts for scale and predictable replenishment.

- Buyer heterogeneity: chains vs independents

- Tiering: service for margin balance

- National accounts: margin for scale

Independent buyers squeeze margins; distributors must justify TCO with fill, turns, rebates

Independent buyers exert strong price pressure—industry net margins ~3% in 2024—while Orgill must justify TCO through fill rates and turns; e‑commerce transparency (home improvement ~18% in 2024) raises scrutiny. Orgill’s services lock >6,000 independents, lowering switching but chains use scale to extract deeper discounts. Rebates, exclusive SKUs and fill/delivery are decisive.

| Metric | Value |

|---|---|

| Orgill sales (FY2023) | $5.1B |

| Industry net margin (2024) | ~3% |

| Home improvement e‑commerce (2024) | ~18% |

| Independents served | >6,000 |

| HD+Lowe's 2024 sales | ~$250B |

Preview Before You Purchase

Orgill Porter's Five Forces Analysis

This Orgill Porter's Five Forces Analysis preview is the exact document you'll receive after purchase—no placeholders or samples. It delivers a professionally formatted, ready-to-use assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution. Purchase grants instant access to this same file for immediate download and application.

Don't Miss the Bigger Picture

Orgill's Porter's Five Forces snapshot highlights supplier concentration, buyer bargaining, competitive rivalry, and threats from substitutes and new entrants—each shaping its distribution advantage and margin dynamics. The analysis shows how scale, supplier relationships, and retail fragmentation affect Orgill's pricing power. This brief preview points to strategic levers and risks. Unlock the full Porter's Five Forces Analysis to explore Orgill’s competitive dynamics in detail.

Suppliers Bargaining Power

Fragmented supplier base offsets power

As of 2024 Orgill sources from thousands of hardware and building-materials vendors, diluting any single supplier’s leverage and enabling multi-sourcing and rapid substitution when terms worsen. This supplier fragmentation supports competitive pricing across SKUs and allows procurement to pivot quickly, reducing disruption risk from any one manufacturer. The breadth of vendor relationships strengthens bargaining power in negotiations and supply continuity.

Concentrated brands hold leverage

In power tools, fasteners and paint, concentrated majors like Stanley Black & Decker, Bosch and Sherwin-Williams exert strong pull-through, constraining Orgill’s delisting options; global power tools market was valued around $35 billion in 2024, underscoring scale advantages. Orgill mitigates with private-labels and regional alternatives but cannot fully replace marquee SKUs. Co-marketing funds and volume rebates remain primary negotiation levers.

Scale and logistics give counterweight

Orgill, the world’s largest independent hardlines distributor, served over 6,000 independent retailers across 50+ countries and reported more than $3.2 billion in net sales in 2024, making it a preferred channel for suppliers. High fill-rate expectations and national promotions align supplier incentives with Orgill’s platform, while scale-based volume commitments secure better pricing and allocation in tight markets. Joint forecasting across Orgill’s DC network smooths production planning and reduces supplier uncertainty.

Commodity volatility pressures terms

- 10–30% 2024 commodity swings

- Index-linked pricing and cadence agreements

- Inventory buffering and hedging

- Private-label/spec flexibility

Switching and compliance costs curb power

Suppliers must integrate EDI, packaging, labeling, and Orgill service-level standards to win and keep business, and noncompliance chargebacks (often 1–3% of supplier sales in retail channels) plus performance scorecards sharply discipline negotiations. Orgill’s category management enforces shelf standards favoring reliable partners, and this operational rigor reduces supplier opportunism over time.

- EDI & standards: mandatory integration

- Chargebacks: commonly 1–3% of sales

- Category management: favors consistent partners

Distributor scale: $3.2B, 6,000+ retailers; 10-30% commodity swings, index-linked pricing

Orgill’s thousands of vendors dilute supplier leverage, enabling multi-sourcing and quick substitution; 2024 net sales ~$3.2B across 6,000+ retailers strengthen Orgill’s bargaining. Major suppliers in power tools/paint (global power tools market ~$35B in 2024) limit delisting options; Orgill offsets via private-labels, rebates and forecasting. Commodity input swings of 10–30% in 2024 drove index-linked pricing, buffering and selective hedging.

| Metric | 2024 Value |

|---|---|

| Net sales | $3.2B |

| Retailers served | 6,000+ |

| Commodity swings | 10–30% |

| Power tools market | $35B |

What is included in the product

Tailored Porter's Five Forces analysis for Orgill that uncovers competitive intensity, supplier and buyer power, substitute threats, and entry barriers, highlighting disruptive trends and strategic levers to protect market share and improve profitability.

Orgill Porter's Five Forces gives a one-sheet, customizable view of competitive pressure—instantly highlighting strategic risks and opportunities for quick, data-driven decisions and easy slide-ready summaries.

Customers Bargaining Power

Independent retailers are price sensitive

Independent hardware and lumber dealers operate on razor-thin net margins—about 3% on average in 2024 per industry reports—and press distributors hard on unit cost, dating, and payment terms. Volume tiers, rebates and promotional dating drive basket wins; suppliers must offer clear tiers and incentive math. Orgill, a leading distributor with roughly $5.1 billion in FY2023 sales, must justify total cost of ownership through superior fill rates and turns as online price transparency (e‑commerce ~18% of home improvement in 2024) intensifies buyer scrutiny.

Switching costs via programs

Orgill locks in over 6,000 independent retailers via integrated marketing, POS links, planograms and inventory-management services, creating significant switching costs. Converting assortments and migrating POS/data to another wholesaler is costly and risky, often disrupting sales and inventory flow. Orgill leverages these services to reduce churn, so high service quality directly weakens buyer bargaining power.

Alternative wholesalers raise leverage

Retailers can pit Orgill against three major peers—Ace, True Value and Do it Best—and regional distributors, leveraging alternative wholesalers to extract better terms.

Competitive bids on core assortments compress net pricing and freight margins, forcing Orgill to defend with service economics.

Differentiation shifts to fill rate, delivery frequency and promotional support, areas where Orgill’s network serving over 10,000 independents is tested.

Rebates and exclusive SKUs are used to defend share and stabilize retailer loyalty.

End-customer channel leakage

Retailers face intense channel leakage to big-box and online players—Home Depot and Lowe's together exceeded roughly 250 billion USD in 2024, forcing independent buyers to demand sharper wholesale economics, drop-ship, special orders and long-tail access.

- Orgill breadth captures special buys, reducing defection

- Data on local demand improves SKU-level margins

- Drop-ship support limits retailer margin squeeze

Buyer size heterogeneity

Larger chains and multi-store dealers negotiate stronger terms with Orgill by leveraging consolidated volumes, while small independents typically accept standard pricing in exchange for turnkey merchandising and support. Orgill’s tiered service model balances margin preservation with retention by differentiating fulfillment, marketing and credit terms. National accounts frequently trade higher discounts for scale and predictable replenishment.

- Buyer heterogeneity: chains vs independents

- Tiering: service for margin balance

- National accounts: margin for scale

Independent buyers squeeze margins; distributors must justify TCO with fill, turns, rebates

Independent buyers exert strong price pressure—industry net margins ~3% in 2024—while Orgill must justify TCO through fill rates and turns; e‑commerce transparency (home improvement ~18% in 2024) raises scrutiny. Orgill’s services lock >6,000 independents, lowering switching but chains use scale to extract deeper discounts. Rebates, exclusive SKUs and fill/delivery are decisive.

| Metric | Value |

|---|---|

| Orgill sales (FY2023) | $5.1B |

| Industry net margin (2024) | ~3% |

| Home improvement e‑commerce (2024) | ~18% |

| Independents served | >6,000 |

| HD+Lowe's 2024 sales | ~$250B |

Preview Before You Purchase

Orgill Porter's Five Forces Analysis

This Orgill Porter's Five Forces Analysis preview is the exact document you'll receive after purchase—no placeholders or samples. It delivers a professionally formatted, ready-to-use assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution. Purchase grants instant access to this same file for immediate download and application.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Orgill's Porter's Five Forces snapshot highlights supplier concentration, buyer bargaining, competitive rivalry, and threats from substitutes and new entrants—each shaping its distribution advantage and margin dynamics. The analysis shows how scale, supplier relationships, and retail fragmentation affect Orgill's pricing power. This brief preview points to strategic levers and risks. Unlock the full Porter's Five Forces Analysis to explore Orgill’s competitive dynamics in detail.

Suppliers Bargaining Power

Fragmented supplier base offsets power

As of 2024 Orgill sources from thousands of hardware and building-materials vendors, diluting any single supplier’s leverage and enabling multi-sourcing and rapid substitution when terms worsen. This supplier fragmentation supports competitive pricing across SKUs and allows procurement to pivot quickly, reducing disruption risk from any one manufacturer. The breadth of vendor relationships strengthens bargaining power in negotiations and supply continuity.

Concentrated brands hold leverage

In power tools, fasteners and paint, concentrated majors like Stanley Black & Decker, Bosch and Sherwin-Williams exert strong pull-through, constraining Orgill’s delisting options; global power tools market was valued around $35 billion in 2024, underscoring scale advantages. Orgill mitigates with private-labels and regional alternatives but cannot fully replace marquee SKUs. Co-marketing funds and volume rebates remain primary negotiation levers.

Scale and logistics give counterweight

Orgill, the world’s largest independent hardlines distributor, served over 6,000 independent retailers across 50+ countries and reported more than $3.2 billion in net sales in 2024, making it a preferred channel for suppliers. High fill-rate expectations and national promotions align supplier incentives with Orgill’s platform, while scale-based volume commitments secure better pricing and allocation in tight markets. Joint forecasting across Orgill’s DC network smooths production planning and reduces supplier uncertainty.

Commodity volatility pressures terms

- 10–30% 2024 commodity swings

- Index-linked pricing and cadence agreements

- Inventory buffering and hedging

- Private-label/spec flexibility

Switching and compliance costs curb power

Suppliers must integrate EDI, packaging, labeling, and Orgill service-level standards to win and keep business, and noncompliance chargebacks (often 1–3% of supplier sales in retail channels) plus performance scorecards sharply discipline negotiations. Orgill’s category management enforces shelf standards favoring reliable partners, and this operational rigor reduces supplier opportunism over time.

- EDI & standards: mandatory integration

- Chargebacks: commonly 1–3% of sales

- Category management: favors consistent partners

Distributor scale: $3.2B, 6,000+ retailers; 10-30% commodity swings, index-linked pricing

Orgill’s thousands of vendors dilute supplier leverage, enabling multi-sourcing and quick substitution; 2024 net sales ~$3.2B across 6,000+ retailers strengthen Orgill’s bargaining. Major suppliers in power tools/paint (global power tools market ~$35B in 2024) limit delisting options; Orgill offsets via private-labels, rebates and forecasting. Commodity input swings of 10–30% in 2024 drove index-linked pricing, buffering and selective hedging.

| Metric | 2024 Value |

|---|---|

| Net sales | $3.2B |

| Retailers served | 6,000+ |

| Commodity swings | 10–30% |

| Power tools market | $35B |

What is included in the product

Tailored Porter's Five Forces analysis for Orgill that uncovers competitive intensity, supplier and buyer power, substitute threats, and entry barriers, highlighting disruptive trends and strategic levers to protect market share and improve profitability.

Orgill Porter's Five Forces gives a one-sheet, customizable view of competitive pressure—instantly highlighting strategic risks and opportunities for quick, data-driven decisions and easy slide-ready summaries.

Customers Bargaining Power

Independent retailers are price sensitive

Independent hardware and lumber dealers operate on razor-thin net margins—about 3% on average in 2024 per industry reports—and press distributors hard on unit cost, dating, and payment terms. Volume tiers, rebates and promotional dating drive basket wins; suppliers must offer clear tiers and incentive math. Orgill, a leading distributor with roughly $5.1 billion in FY2023 sales, must justify total cost of ownership through superior fill rates and turns as online price transparency (e‑commerce ~18% of home improvement in 2024) intensifies buyer scrutiny.

Switching costs via programs

Orgill locks in over 6,000 independent retailers via integrated marketing, POS links, planograms and inventory-management services, creating significant switching costs. Converting assortments and migrating POS/data to another wholesaler is costly and risky, often disrupting sales and inventory flow. Orgill leverages these services to reduce churn, so high service quality directly weakens buyer bargaining power.

Alternative wholesalers raise leverage

Retailers can pit Orgill against three major peers—Ace, True Value and Do it Best—and regional distributors, leveraging alternative wholesalers to extract better terms.

Competitive bids on core assortments compress net pricing and freight margins, forcing Orgill to defend with service economics.

Differentiation shifts to fill rate, delivery frequency and promotional support, areas where Orgill’s network serving over 10,000 independents is tested.

Rebates and exclusive SKUs are used to defend share and stabilize retailer loyalty.

End-customer channel leakage

Retailers face intense channel leakage to big-box and online players—Home Depot and Lowe's together exceeded roughly 250 billion USD in 2024, forcing independent buyers to demand sharper wholesale economics, drop-ship, special orders and long-tail access.

- Orgill breadth captures special buys, reducing defection

- Data on local demand improves SKU-level margins

- Drop-ship support limits retailer margin squeeze

Buyer size heterogeneity

Larger chains and multi-store dealers negotiate stronger terms with Orgill by leveraging consolidated volumes, while small independents typically accept standard pricing in exchange for turnkey merchandising and support. Orgill’s tiered service model balances margin preservation with retention by differentiating fulfillment, marketing and credit terms. National accounts frequently trade higher discounts for scale and predictable replenishment.

- Buyer heterogeneity: chains vs independents

- Tiering: service for margin balance

- National accounts: margin for scale

Independent buyers squeeze margins; distributors must justify TCO with fill, turns, rebates

Independent buyers exert strong price pressure—industry net margins ~3% in 2024—while Orgill must justify TCO through fill rates and turns; e‑commerce transparency (home improvement ~18% in 2024) raises scrutiny. Orgill’s services lock >6,000 independents, lowering switching but chains use scale to extract deeper discounts. Rebates, exclusive SKUs and fill/delivery are decisive.

| Metric | Value |

|---|---|

| Orgill sales (FY2023) | $5.1B |

| Industry net margin (2024) | ~3% |

| Home improvement e‑commerce (2024) | ~18% |

| Independents served | >6,000 |

| HD+Lowe's 2024 sales | ~$250B |

Preview Before You Purchase

Orgill Porter's Five Forces Analysis

This Orgill Porter's Five Forces Analysis preview is the exact document you'll receive after purchase—no placeholders or samples. It delivers a professionally formatted, ready-to-use assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution. Purchase grants instant access to this same file for immediate download and application.