Orion Engineered Carbons GmbH PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

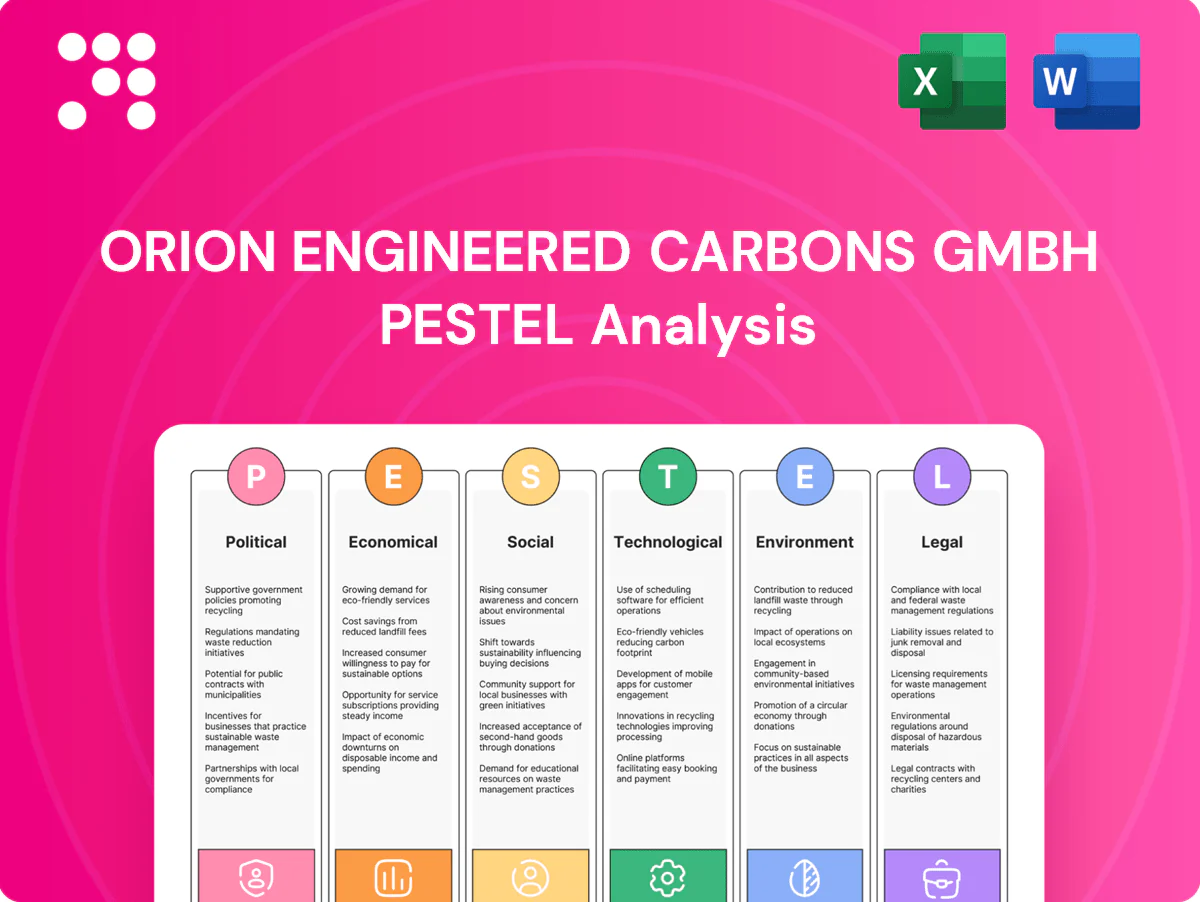

Gain a strategic advantage with our PESTLE Analysis of Orion Engineered Carbons GmbH—three concise insights reveal political, environmental, and technological forces shaping its trajectory. Ideal for investors and strategists, this brief highlights key risks and opportunities. Purchase the full report to access the complete, actionable breakdown and editable files now.

Political factors

Trade policy and tariffs

Carbon black crosses borders extensively, exposing Orion to tariff shifts and trade disputes that can rapidly alter landed costs and margin profiles. The EU Carbon Border Adjustment Mechanism enters full application in 2026 after a 2023–2025 transition, potentially increasing EU import costs for carbon-intensive grades. Favorable trade agreements reduce barriers for specialty grades, while sudden political shifts can change duty structures and quota regimes with little notice.

Geopolitical energy security

Geopolitical energy security drives policy responses that reshaped power and feedstock availability for Orion; European TTF gas fell from peaks >200 €/MWh in 2022 to roughly 30–40 €/MWh in 2024, while EU storage stayed >80% through 2024. Government interventions—price caps, strategic stockpiles and market rules—have compressed or distorted cost curves and can shift site utilization decisions across European plants.

Industrial policy and subsidies

National incentives for advanced materials and battery value chains — notably the EU NextGenerationEU €723.8bn package and the US Inflation Reduction Act ($369bn in clean energy investments) — can boost demand for conductive carbon black used in battery electrodes. Grants and tax credits tied to low‑emission upgrades and domestic content (IRA domestic sourcing rules) improve project economics. Conversely, subsidies for substitute materials and strict local‑content rules may erode share unless Orion aligns with policy priorities and supply‑chain requirements.

Sanctions and export controls

Sanctions on specific countries can constrain sales and sourcing of feedstocks for Orion Engineered Carbons, raising supply and price volatility. Export controls on advanced carbon materials may trigger licensing for specialty grades and limit market access. Evolving sanction and control lists increase compliance costs and operational risk, while diversified feedstock routes and a broad customer base help mitigate disruptions.

- Sanctions restrict feedstock trade

- Export licenses needed for specialty grades

- Compliance costs rising with list changes

- Diversification reduces disruption risk

Local permitting and political stability

Plant operations at Orion Engineered Carbons depend on municipal and regional approvals, with German and Brazilian permitting often requiring 12–18 months in 2024; political instability in some Latin American sites has caused expansion and turnaround delays of 6–24 months. Local council pressure tightened emission limits post-2023, raising compliance capex, while stable jurisdictions enable 3–5 year contract and capex planning horizons.

- Permitting timelines: 12–18 months (Germany, 2024)

- Delay range from instability: 6–24 months

- Planning horizon enabled by stability: 3–5 years

- Post-2023 emission tightening increased compliance capex

CBAM risk, lower TTF gas and policy funds spur battery demand by 2026

Carbon black trade exposure makes Orion sensitive to tariffs and CBAM (full 2026). European TTF gas fell from >200 €/MWh in 2022 to ~30–40 €/MWh in 2024; EU gas storage >80% in 2024 affecting feedstock costs. EU NextGenerationEU €723.8bn and US IRA $369bn lift battery-grade demand; permitting averages 12–18 months (Germany, 2024) with instability causing 6–24 month delays.

| Factor | Key 2024–25 Data |

|---|---|

| CBAM | Full 2026 |

| TTF gas | 30–40 €/MWh (2024) |

| Funding | EU €723.8bn; US $369bn |

| Permitting | 12–18 months; delays 6–24m |

What is included in the product

Explores how macro-environmental factors uniquely affect Orion Engineered Carbons GmbH across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region- and industry-specific insights. Designed for executives and investors, it highlights threats, opportunities and forward-looking scenarios ready for reports and pitch decks.

Condensed PESTLE summary for Orion Engineered Carbons GmbH that highlights regulatory, environmental, supply-chain and market risks for quick decision-making, editable for local context and presentation-ready to streamline team alignment and planning.

Economic factors

Cyclical demand in end markets

Rubber (tires), coatings, inks and polymer demand track industrial and auto cycles, so downturns compress volumes and shift mix toward lower-margin standard carbon blacks while specialty, high-performance grades show greater resilience; Orion’s geographic diversification across Europe, Americas and Asia helps smooth regional volatility and support stable cash flow.

Feedstock and energy price volatility

Carbon black production depends on carbonaceous oils and high energy input; crude (Brent ~80 USD/bbl mid-2025) and EU industrial power (~0.20 EUR/kWh) and gas (TTF ~25 EUR/MWh) swings drive margin variability for Orion. Crude oil spreads and electricity/gas moves cause short-term earnings pressure, partially offset by surcharges and index-linked pricing that pass costs with a 1–3 month lag. Active hedging programs and ongoing energy-efficiency projects reduce earnings volatility.

Currency fluctuations

Orion Engineered Carbons records revenues and costs across USD, EUR and several emerging-market currencies, with EUR/USD trading roughly 1.05–1.12 through 2024, amplifying translation effects on reported earnings. FX moves affect price competitiveness in export markets and margin volatility; emerging-market currencies experienced up to ~15% volatility in 2023–24. Local sourcing and local-currency pricing provide natural hedges while financial hedging instruments are used to align cash flows with debt and capex obligations.

Scale, utilization, and pricing power

Capacity utilization drives fixed-cost absorption—moving utilization above 85% materially lowers unit fixed costs, while prolonged overcapacity depresses pricing for commoditized grades; tight markets allow Orion to enforce price discipline and capture premiums on specialty blacks. Network optimization across plants (scheduling, feedstock flow) sustains margins through cycles by shifting volumes to higher-margin sites.

- utilization >85%: better fixed-cost absorption

- tight markets: specialty price premiums

- overcapacity: commoditized price pressure

- network optimization: margin resilience

Capital intensity and financing

Orion faces high capital intensity as environmental upgrades and debottlenecking demand substantial capex, raising project hurdle rates when interest rates rose in 2024–25 and pushed WACC higher. Access to green or sustainability-linked financing can materially lower funding costs and improve payback timelines. Strong cash generation enables deleveraging and funds strategic M&A without diluting equity.

- Capex pressure: environmental upgrades required

- Rates impact: higher WACC, raised hurdle rates

- Green finance: lowers cost of capital

- Cash flow: supports deleveraging and M&A

CBAM risk, lower TTF gas and policy funds spur battery demand by 2026

Demand and mix follow auto/industrial cycles, pressuring volumes and favoring low-margin standard blacks in downturns while specialties hold better. Feedstock and energy costs drive margins (Brent ~80 USD/bbl mid-2025; EU power ~0.20 EUR/kWh; TTF ~25 EUR/MWh) mitigated by surcharges and hedging. FX (EUR/USD 1.05–1.12) and utilization (>85% breakeven) materially affect reported earnings and unit costs; higher 2024–25 rates raised WACC, boosting capex hurdle rates.

| Metric | Value |

|---|---|

| Brent | ~80 USD/bbl (mid-2025) |

| EU power | ~0.20 EUR/kWh |

| TTF gas | ~25 EUR/MWh |

| EUR/USD | 1.05–1.12 (2024) |

| Utilization | >85% (material margin tailwind) |

| EM FX vol | ~15% (2023–24) |

Preview Before You Purchase

Orion Engineered Carbons GmbH PESTLE Analysis

The preview shown here is the exact Orion Engineered Carbons GmbH PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It provides political, economic, social, technological, legal, and environmental insights tailored to Orion’s business context. No placeholders or teasers—this is the final downloadable file. You’ll get immediate access upon payment.

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic advantage with our PESTLE Analysis of Orion Engineered Carbons GmbH—three concise insights reveal political, environmental, and technological forces shaping its trajectory. Ideal for investors and strategists, this brief highlights key risks and opportunities. Purchase the full report to access the complete, actionable breakdown and editable files now.

Political factors

Trade policy and tariffs

Carbon black crosses borders extensively, exposing Orion to tariff shifts and trade disputes that can rapidly alter landed costs and margin profiles. The EU Carbon Border Adjustment Mechanism enters full application in 2026 after a 2023–2025 transition, potentially increasing EU import costs for carbon-intensive grades. Favorable trade agreements reduce barriers for specialty grades, while sudden political shifts can change duty structures and quota regimes with little notice.

Geopolitical energy security

Geopolitical energy security drives policy responses that reshaped power and feedstock availability for Orion; European TTF gas fell from peaks >200 €/MWh in 2022 to roughly 30–40 €/MWh in 2024, while EU storage stayed >80% through 2024. Government interventions—price caps, strategic stockpiles and market rules—have compressed or distorted cost curves and can shift site utilization decisions across European plants.

Industrial policy and subsidies

National incentives for advanced materials and battery value chains — notably the EU NextGenerationEU €723.8bn package and the US Inflation Reduction Act ($369bn in clean energy investments) — can boost demand for conductive carbon black used in battery electrodes. Grants and tax credits tied to low‑emission upgrades and domestic content (IRA domestic sourcing rules) improve project economics. Conversely, subsidies for substitute materials and strict local‑content rules may erode share unless Orion aligns with policy priorities and supply‑chain requirements.

Sanctions and export controls

Sanctions on specific countries can constrain sales and sourcing of feedstocks for Orion Engineered Carbons, raising supply and price volatility. Export controls on advanced carbon materials may trigger licensing for specialty grades and limit market access. Evolving sanction and control lists increase compliance costs and operational risk, while diversified feedstock routes and a broad customer base help mitigate disruptions.

- Sanctions restrict feedstock trade

- Export licenses needed for specialty grades

- Compliance costs rising with list changes

- Diversification reduces disruption risk

Local permitting and political stability

Plant operations at Orion Engineered Carbons depend on municipal and regional approvals, with German and Brazilian permitting often requiring 12–18 months in 2024; political instability in some Latin American sites has caused expansion and turnaround delays of 6–24 months. Local council pressure tightened emission limits post-2023, raising compliance capex, while stable jurisdictions enable 3–5 year contract and capex planning horizons.

- Permitting timelines: 12–18 months (Germany, 2024)

- Delay range from instability: 6–24 months

- Planning horizon enabled by stability: 3–5 years

- Post-2023 emission tightening increased compliance capex

CBAM risk, lower TTF gas and policy funds spur battery demand by 2026

Carbon black trade exposure makes Orion sensitive to tariffs and CBAM (full 2026). European TTF gas fell from >200 €/MWh in 2022 to ~30–40 €/MWh in 2024; EU gas storage >80% in 2024 affecting feedstock costs. EU NextGenerationEU €723.8bn and US IRA $369bn lift battery-grade demand; permitting averages 12–18 months (Germany, 2024) with instability causing 6–24 month delays.

| Factor | Key 2024–25 Data |

|---|---|

| CBAM | Full 2026 |

| TTF gas | 30–40 €/MWh (2024) |

| Funding | EU €723.8bn; US $369bn |

| Permitting | 12–18 months; delays 6–24m |

What is included in the product

Explores how macro-environmental factors uniquely affect Orion Engineered Carbons GmbH across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region- and industry-specific insights. Designed for executives and investors, it highlights threats, opportunities and forward-looking scenarios ready for reports and pitch decks.

Condensed PESTLE summary for Orion Engineered Carbons GmbH that highlights regulatory, environmental, supply-chain and market risks for quick decision-making, editable for local context and presentation-ready to streamline team alignment and planning.

Economic factors

Cyclical demand in end markets

Rubber (tires), coatings, inks and polymer demand track industrial and auto cycles, so downturns compress volumes and shift mix toward lower-margin standard carbon blacks while specialty, high-performance grades show greater resilience; Orion’s geographic diversification across Europe, Americas and Asia helps smooth regional volatility and support stable cash flow.

Feedstock and energy price volatility

Carbon black production depends on carbonaceous oils and high energy input; crude (Brent ~80 USD/bbl mid-2025) and EU industrial power (~0.20 EUR/kWh) and gas (TTF ~25 EUR/MWh) swings drive margin variability for Orion. Crude oil spreads and electricity/gas moves cause short-term earnings pressure, partially offset by surcharges and index-linked pricing that pass costs with a 1–3 month lag. Active hedging programs and ongoing energy-efficiency projects reduce earnings volatility.

Currency fluctuations

Orion Engineered Carbons records revenues and costs across USD, EUR and several emerging-market currencies, with EUR/USD trading roughly 1.05–1.12 through 2024, amplifying translation effects on reported earnings. FX moves affect price competitiveness in export markets and margin volatility; emerging-market currencies experienced up to ~15% volatility in 2023–24. Local sourcing and local-currency pricing provide natural hedges while financial hedging instruments are used to align cash flows with debt and capex obligations.

Scale, utilization, and pricing power

Capacity utilization drives fixed-cost absorption—moving utilization above 85% materially lowers unit fixed costs, while prolonged overcapacity depresses pricing for commoditized grades; tight markets allow Orion to enforce price discipline and capture premiums on specialty blacks. Network optimization across plants (scheduling, feedstock flow) sustains margins through cycles by shifting volumes to higher-margin sites.

- utilization >85%: better fixed-cost absorption

- tight markets: specialty price premiums

- overcapacity: commoditized price pressure

- network optimization: margin resilience

Capital intensity and financing

Orion faces high capital intensity as environmental upgrades and debottlenecking demand substantial capex, raising project hurdle rates when interest rates rose in 2024–25 and pushed WACC higher. Access to green or sustainability-linked financing can materially lower funding costs and improve payback timelines. Strong cash generation enables deleveraging and funds strategic M&A without diluting equity.

- Capex pressure: environmental upgrades required

- Rates impact: higher WACC, raised hurdle rates

- Green finance: lowers cost of capital

- Cash flow: supports deleveraging and M&A

CBAM risk, lower TTF gas and policy funds spur battery demand by 2026

Demand and mix follow auto/industrial cycles, pressuring volumes and favoring low-margin standard blacks in downturns while specialties hold better. Feedstock and energy costs drive margins (Brent ~80 USD/bbl mid-2025; EU power ~0.20 EUR/kWh; TTF ~25 EUR/MWh) mitigated by surcharges and hedging. FX (EUR/USD 1.05–1.12) and utilization (>85% breakeven) materially affect reported earnings and unit costs; higher 2024–25 rates raised WACC, boosting capex hurdle rates.

| Metric | Value |

|---|---|

| Brent | ~80 USD/bbl (mid-2025) |

| EU power | ~0.20 EUR/kWh |

| TTF gas | ~25 EUR/MWh |

| EUR/USD | 1.05–1.12 (2024) |

| Utilization | >85% (material margin tailwind) |

| EM FX vol | ~15% (2023–24) |

Preview Before You Purchase

Orion Engineered Carbons GmbH PESTLE Analysis

The preview shown here is the exact Orion Engineered Carbons GmbH PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It provides political, economic, social, technological, legal, and environmental insights tailored to Orion’s business context. No placeholders or teasers—this is the final downloadable file. You’ll get immediate access upon payment.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic advantage with our PESTLE Analysis of Orion Engineered Carbons GmbH—three concise insights reveal political, environmental, and technological forces shaping its trajectory. Ideal for investors and strategists, this brief highlights key risks and opportunities. Purchase the full report to access the complete, actionable breakdown and editable files now.

Political factors

Trade policy and tariffs

Carbon black crosses borders extensively, exposing Orion to tariff shifts and trade disputes that can rapidly alter landed costs and margin profiles. The EU Carbon Border Adjustment Mechanism enters full application in 2026 after a 2023–2025 transition, potentially increasing EU import costs for carbon-intensive grades. Favorable trade agreements reduce barriers for specialty grades, while sudden political shifts can change duty structures and quota regimes with little notice.

Geopolitical energy security

Geopolitical energy security drives policy responses that reshaped power and feedstock availability for Orion; European TTF gas fell from peaks >200 €/MWh in 2022 to roughly 30–40 €/MWh in 2024, while EU storage stayed >80% through 2024. Government interventions—price caps, strategic stockpiles and market rules—have compressed or distorted cost curves and can shift site utilization decisions across European plants.

Industrial policy and subsidies

National incentives for advanced materials and battery value chains — notably the EU NextGenerationEU €723.8bn package and the US Inflation Reduction Act ($369bn in clean energy investments) — can boost demand for conductive carbon black used in battery electrodes. Grants and tax credits tied to low‑emission upgrades and domestic content (IRA domestic sourcing rules) improve project economics. Conversely, subsidies for substitute materials and strict local‑content rules may erode share unless Orion aligns with policy priorities and supply‑chain requirements.

Sanctions and export controls

Sanctions on specific countries can constrain sales and sourcing of feedstocks for Orion Engineered Carbons, raising supply and price volatility. Export controls on advanced carbon materials may trigger licensing for specialty grades and limit market access. Evolving sanction and control lists increase compliance costs and operational risk, while diversified feedstock routes and a broad customer base help mitigate disruptions.

- Sanctions restrict feedstock trade

- Export licenses needed for specialty grades

- Compliance costs rising with list changes

- Diversification reduces disruption risk

Local permitting and political stability

Plant operations at Orion Engineered Carbons depend on municipal and regional approvals, with German and Brazilian permitting often requiring 12–18 months in 2024; political instability in some Latin American sites has caused expansion and turnaround delays of 6–24 months. Local council pressure tightened emission limits post-2023, raising compliance capex, while stable jurisdictions enable 3–5 year contract and capex planning horizons.

- Permitting timelines: 12–18 months (Germany, 2024)

- Delay range from instability: 6–24 months

- Planning horizon enabled by stability: 3–5 years

- Post-2023 emission tightening increased compliance capex

CBAM risk, lower TTF gas and policy funds spur battery demand by 2026

Carbon black trade exposure makes Orion sensitive to tariffs and CBAM (full 2026). European TTF gas fell from >200 €/MWh in 2022 to ~30–40 €/MWh in 2024; EU gas storage >80% in 2024 affecting feedstock costs. EU NextGenerationEU €723.8bn and US IRA $369bn lift battery-grade demand; permitting averages 12–18 months (Germany, 2024) with instability causing 6–24 month delays.

| Factor | Key 2024–25 Data |

|---|---|

| CBAM | Full 2026 |

| TTF gas | 30–40 €/MWh (2024) |

| Funding | EU €723.8bn; US $369bn |

| Permitting | 12–18 months; delays 6–24m |

What is included in the product

Explores how macro-environmental factors uniquely affect Orion Engineered Carbons GmbH across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region- and industry-specific insights. Designed for executives and investors, it highlights threats, opportunities and forward-looking scenarios ready for reports and pitch decks.

Condensed PESTLE summary for Orion Engineered Carbons GmbH that highlights regulatory, environmental, supply-chain and market risks for quick decision-making, editable for local context and presentation-ready to streamline team alignment and planning.

Economic factors

Cyclical demand in end markets

Rubber (tires), coatings, inks and polymer demand track industrial and auto cycles, so downturns compress volumes and shift mix toward lower-margin standard carbon blacks while specialty, high-performance grades show greater resilience; Orion’s geographic diversification across Europe, Americas and Asia helps smooth regional volatility and support stable cash flow.

Feedstock and energy price volatility

Carbon black production depends on carbonaceous oils and high energy input; crude (Brent ~80 USD/bbl mid-2025) and EU industrial power (~0.20 EUR/kWh) and gas (TTF ~25 EUR/MWh) swings drive margin variability for Orion. Crude oil spreads and electricity/gas moves cause short-term earnings pressure, partially offset by surcharges and index-linked pricing that pass costs with a 1–3 month lag. Active hedging programs and ongoing energy-efficiency projects reduce earnings volatility.

Currency fluctuations

Orion Engineered Carbons records revenues and costs across USD, EUR and several emerging-market currencies, with EUR/USD trading roughly 1.05–1.12 through 2024, amplifying translation effects on reported earnings. FX moves affect price competitiveness in export markets and margin volatility; emerging-market currencies experienced up to ~15% volatility in 2023–24. Local sourcing and local-currency pricing provide natural hedges while financial hedging instruments are used to align cash flows with debt and capex obligations.

Scale, utilization, and pricing power

Capacity utilization drives fixed-cost absorption—moving utilization above 85% materially lowers unit fixed costs, while prolonged overcapacity depresses pricing for commoditized grades; tight markets allow Orion to enforce price discipline and capture premiums on specialty blacks. Network optimization across plants (scheduling, feedstock flow) sustains margins through cycles by shifting volumes to higher-margin sites.

- utilization >85%: better fixed-cost absorption

- tight markets: specialty price premiums

- overcapacity: commoditized price pressure

- network optimization: margin resilience

Capital intensity and financing

Orion faces high capital intensity as environmental upgrades and debottlenecking demand substantial capex, raising project hurdle rates when interest rates rose in 2024–25 and pushed WACC higher. Access to green or sustainability-linked financing can materially lower funding costs and improve payback timelines. Strong cash generation enables deleveraging and funds strategic M&A without diluting equity.

- Capex pressure: environmental upgrades required

- Rates impact: higher WACC, raised hurdle rates

- Green finance: lowers cost of capital

- Cash flow: supports deleveraging and M&A

CBAM risk, lower TTF gas and policy funds spur battery demand by 2026

Demand and mix follow auto/industrial cycles, pressuring volumes and favoring low-margin standard blacks in downturns while specialties hold better. Feedstock and energy costs drive margins (Brent ~80 USD/bbl mid-2025; EU power ~0.20 EUR/kWh; TTF ~25 EUR/MWh) mitigated by surcharges and hedging. FX (EUR/USD 1.05–1.12) and utilization (>85% breakeven) materially affect reported earnings and unit costs; higher 2024–25 rates raised WACC, boosting capex hurdle rates.

| Metric | Value |

|---|---|

| Brent | ~80 USD/bbl (mid-2025) |

| EU power | ~0.20 EUR/kWh |

| TTF gas | ~25 EUR/MWh |

| EUR/USD | 1.05–1.12 (2024) |

| Utilization | >85% (material margin tailwind) |

| EM FX vol | ~15% (2023–24) |

Preview Before You Purchase

Orion Engineered Carbons GmbH PESTLE Analysis

The preview shown here is the exact Orion Engineered Carbons GmbH PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It provides political, economic, social, technological, legal, and environmental insights tailored to Orion’s business context. No placeholders or teasers—this is the final downloadable file. You’ll get immediate access upon payment.