Orkla Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

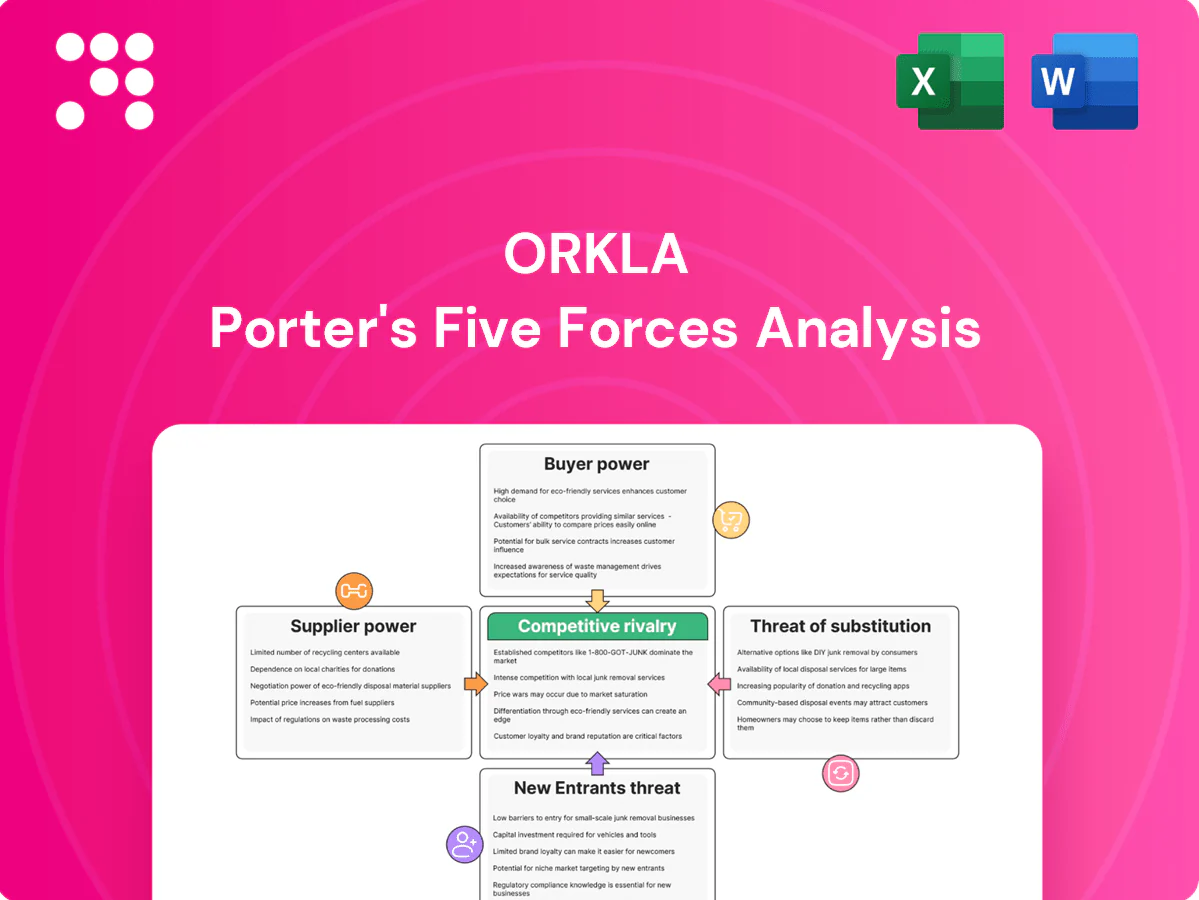

Orkla's Porter's Five Forces snapshot highlights moderate supplier power, strong buyer expectations, a fragmented competitor landscape, manageable threat of new entrants, and rising substitute pressures from private labels and sustainability trends. This brief overview teases strategic risks and opportunities. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations tailored to Orkla.

Suppliers Bargaining Power

Fragmented agri and packaging base

In 2024 Orkla sources grains, oils, sugar and packaging from a fragmented global supplier base, which limits individual supplier leverage and supports negotiated terms. Commodity price volatility remained elevated following 2022–23 shocks and can still compress margins despite low supplier concentration. Orkla routinely dual-sources key inputs and leverages scale to negotiate better prices. Long-term frameworks and hedging partially mitigate supply shocks.

Specialty inputs with higher leverage

Fragrances, actives and certain specialty chemicals are highly concentrated — the top four fragrance companies (Givaudan, Firmenich, IFF, Symrise) held roughly 70% of the global market in 2024 — giving suppliers marked bargaining power. Stringent qualification and regulatory regimes such as EU REACH (over 22,000 registered substances) raise switching costs. Orkla’s multi-category volumes and strategic long-term partnerships help stabilize access and pricing.

Sustainability and traceability demands

Stricter Nordic ESG standards and the 2024 EU Packaging and Packaging Waste Regulation raise supplier compliance costs, narrowing eligible supplier pools for certified palm oil, cocoa and recyclable packaging. Reduced substitution options in these certified niches can increase supplier bargaining power where compliance is scarce. Orkla’s responsible sourcing programs and supplier development aim to expand the qualified base over time, mitigating concentration risks.

Energy and logistics exposure

Orkla's access to Norwegian hydropower (Norway's electricity mix ~90% hydropower in 2024) internalizes a portion of energy costs, but broader manufacturing and distribution remain exposed to global energy and freight markets where spot prices and fuel surcharges create input volatility.

Tight logistics capacity during demand spikes transfers bargaining power to carriers; regional production and nearshoring reduce distance and lead times but do not eliminate systemic shocks—contracting and longer-term freight agreements dampen volatility.

- Hydropower share: ~90% Norway (2024)

- Regional footprint: lowers transit risk, not systemic shocks

- Spot freight spikes increase carrier power

- Fixed contracts/nearshoring reduce price volatility

Scale and category breadth

Orkla’s scale across foods, personal care and home care strengthens supplier leverage by concentrating volume and specifying standardized inputs, reducing reliance on single-source vendors.

Consolidated purchasing and group-wide specifications enable substitution and drive lower input costs while multi-year contracts improve price stability and supply continuity.

- Scale-driven leverage

- Centralized procurement

- Multi-year contracts

- Portfolio-based substitution

Low bulk supplier concentration; ~70% in fragrances plus commodity volatility raise margin risk

Orkla faces low supplier concentration for bulk agri inputs, but commodity price volatility in 2024 keeps margin risk. Specialty fragrances/actives are concentrated (top 4 ~70% global share in 2024), raising switching costs. Scale, centralized procurement and multi-year contracts (plus Norway hydropower ~90% of mix in 2024) mitigate supplier leverage.

| Factor | 2024 datapoint |

|---|---|

| Fragrance concentration | Top 4 ~70% |

| Norway hydropower | ~90% |

| Mitigant | Centralized procurement, multi-year contracts |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers and substitutes tailored exclusively for Orkla, highlighting disruptive threats and strategic advantages within its consumer goods and branded-products portfolio.

Clear, one-sheet Porter's Five Forces for Orkla that visualizes supplier, buyer, entrant, substitute and rivalry pressures—perfect for rapid strategic decisions and boardroom use.

Customers Bargaining Power

Concentrated Nordic retail

Large chains such as NorgesGruppen, Coop, ICA, S Group and REMA 1000 concentrate buying power in the Nordics, with the top retailers capturing over 75% of grocery sales in 2024, forcing sharp pricing, promotional funding and stricter payment/terms. Delisting threats in mature categories intensify margin pressure. Orkla counters through strong national brands and formal category captaincy agreements to secure shelf space and promotional prioritization.

Private label expansion

Retailers’ private labels are credible low-price alternatives, with private label making roughly 37% of European grocery sales in 2023 and Nordic penetration typically in the 35–45% range, increasing buyer leverage.

Private label growth in Eastern Europe and India showed double-digit expansion in 2023, pressuring branded margins.

Orkla must defend shelf space through clear differentiation, faster NPD and category-tailored innovation, while driving cost efficiency and layered value tiers to hit buyer price points.

Channel mix diversification

Channel mix diversification reduces grocery dependence by shifting sales to out-of-home and pharmacy, but both channels have professionalized buyers; tender-based contracting in foodservice compresses margins while pharmacies prize compliance and efficacy data, enabling selective premium pricing; a multi-channel presence balances negotiating power across grocery, foodservice and pharmacy, smoothing margin volatility.

High price sensitivity

High price sensitivity: 2024 food inflation of 3.2% intensified retailer pushback on list-price hikes, driving more promotion-led assortments as consumers traded down to private labels.

Orkla counters with pack-price architecture and revenue growth management, using elasticity studies (SKU-level elasticities showing 5–12% volume drop per 10% price rise) to make selective pricing moves.

- Retailer pressure up — promotion rates +4–6ppt (2024)

- Orkla tools — pack-price, RGM, SKU elasticity

- Selective pricing based on 5–12% volume elasticity

Data and category insights

Advanced retailer analytics increase transparency on performance, and in 2024 Orkla leveraged joint business plans with key retailers to ROI-proof promotions; category management preserves influence against buyer consolidation while superior shopper insights support assortment leadership and incremental margin capture.

- Retailer analytics: transparency

- Joint business plans: ROI-proofed promos

- Category mgmt: preserves influence

- Shopper insights: justify assortment

Nordic retail (>75%) and private labels raise promos and delisting risk

Concentrated Nordic retailing (>75% share by top chains in 2024) and credible private labels (EU 37% in 2023; Nordics 35–45%) amplify buyer leverage, raising promotion rates (+4–6ppt in 2024) and delisting risk. Orkla defends via national brands, category captaincy, RGM and SKU-level pricing (5–12% volume drop per 10% price rise). Joint business plans and analytics ROI-proof promotions.

| Metric | Value |

|---|---|

| Top retailers share (Nordics) | >75% (2024) |

| Private label EU | 37% (2023) |

| Nordic PL | 35–45% |

| Promo rate change | +4–6ppt (2024) |

| Food inflation | 3.2% (2024) |

| SKU elasticity | 5–12% vol per 10% price |

Preview the Actual Deliverable

Orkla Porter's Five Forces Analysis

This preview shows the complete Orkla Porter's Five Forces analysis you'll receive after purchase. It is the exact, fully formatted document—no placeholders or mockups—and is ready for immediate download and use. Purchase grants instant access to this same file.

Go Beyond the Preview—Access the Full Strategic Report

Orkla's Porter's Five Forces snapshot highlights moderate supplier power, strong buyer expectations, a fragmented competitor landscape, manageable threat of new entrants, and rising substitute pressures from private labels and sustainability trends. This brief overview teases strategic risks and opportunities. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations tailored to Orkla.

Suppliers Bargaining Power

Fragmented agri and packaging base

In 2024 Orkla sources grains, oils, sugar and packaging from a fragmented global supplier base, which limits individual supplier leverage and supports negotiated terms. Commodity price volatility remained elevated following 2022–23 shocks and can still compress margins despite low supplier concentration. Orkla routinely dual-sources key inputs and leverages scale to negotiate better prices. Long-term frameworks and hedging partially mitigate supply shocks.

Specialty inputs with higher leverage

Fragrances, actives and certain specialty chemicals are highly concentrated — the top four fragrance companies (Givaudan, Firmenich, IFF, Symrise) held roughly 70% of the global market in 2024 — giving suppliers marked bargaining power. Stringent qualification and regulatory regimes such as EU REACH (over 22,000 registered substances) raise switching costs. Orkla’s multi-category volumes and strategic long-term partnerships help stabilize access and pricing.

Sustainability and traceability demands

Stricter Nordic ESG standards and the 2024 EU Packaging and Packaging Waste Regulation raise supplier compliance costs, narrowing eligible supplier pools for certified palm oil, cocoa and recyclable packaging. Reduced substitution options in these certified niches can increase supplier bargaining power where compliance is scarce. Orkla’s responsible sourcing programs and supplier development aim to expand the qualified base over time, mitigating concentration risks.

Energy and logistics exposure

Orkla's access to Norwegian hydropower (Norway's electricity mix ~90% hydropower in 2024) internalizes a portion of energy costs, but broader manufacturing and distribution remain exposed to global energy and freight markets where spot prices and fuel surcharges create input volatility.

Tight logistics capacity during demand spikes transfers bargaining power to carriers; regional production and nearshoring reduce distance and lead times but do not eliminate systemic shocks—contracting and longer-term freight agreements dampen volatility.

- Hydropower share: ~90% Norway (2024)

- Regional footprint: lowers transit risk, not systemic shocks

- Spot freight spikes increase carrier power

- Fixed contracts/nearshoring reduce price volatility

Scale and category breadth

Orkla’s scale across foods, personal care and home care strengthens supplier leverage by concentrating volume and specifying standardized inputs, reducing reliance on single-source vendors.

Consolidated purchasing and group-wide specifications enable substitution and drive lower input costs while multi-year contracts improve price stability and supply continuity.

- Scale-driven leverage

- Centralized procurement

- Multi-year contracts

- Portfolio-based substitution

Low bulk supplier concentration; ~70% in fragrances plus commodity volatility raise margin risk

Orkla faces low supplier concentration for bulk agri inputs, but commodity price volatility in 2024 keeps margin risk. Specialty fragrances/actives are concentrated (top 4 ~70% global share in 2024), raising switching costs. Scale, centralized procurement and multi-year contracts (plus Norway hydropower ~90% of mix in 2024) mitigate supplier leverage.

| Factor | 2024 datapoint |

|---|---|

| Fragrance concentration | Top 4 ~70% |

| Norway hydropower | ~90% |

| Mitigant | Centralized procurement, multi-year contracts |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers and substitutes tailored exclusively for Orkla, highlighting disruptive threats and strategic advantages within its consumer goods and branded-products portfolio.

Clear, one-sheet Porter's Five Forces for Orkla that visualizes supplier, buyer, entrant, substitute and rivalry pressures—perfect for rapid strategic decisions and boardroom use.

Customers Bargaining Power

Concentrated Nordic retail

Large chains such as NorgesGruppen, Coop, ICA, S Group and REMA 1000 concentrate buying power in the Nordics, with the top retailers capturing over 75% of grocery sales in 2024, forcing sharp pricing, promotional funding and stricter payment/terms. Delisting threats in mature categories intensify margin pressure. Orkla counters through strong national brands and formal category captaincy agreements to secure shelf space and promotional prioritization.

Private label expansion

Retailers’ private labels are credible low-price alternatives, with private label making roughly 37% of European grocery sales in 2023 and Nordic penetration typically in the 35–45% range, increasing buyer leverage.

Private label growth in Eastern Europe and India showed double-digit expansion in 2023, pressuring branded margins.

Orkla must defend shelf space through clear differentiation, faster NPD and category-tailored innovation, while driving cost efficiency and layered value tiers to hit buyer price points.

Channel mix diversification

Channel mix diversification reduces grocery dependence by shifting sales to out-of-home and pharmacy, but both channels have professionalized buyers; tender-based contracting in foodservice compresses margins while pharmacies prize compliance and efficacy data, enabling selective premium pricing; a multi-channel presence balances negotiating power across grocery, foodservice and pharmacy, smoothing margin volatility.

High price sensitivity

High price sensitivity: 2024 food inflation of 3.2% intensified retailer pushback on list-price hikes, driving more promotion-led assortments as consumers traded down to private labels.

Orkla counters with pack-price architecture and revenue growth management, using elasticity studies (SKU-level elasticities showing 5–12% volume drop per 10% price rise) to make selective pricing moves.

- Retailer pressure up — promotion rates +4–6ppt (2024)

- Orkla tools — pack-price, RGM, SKU elasticity

- Selective pricing based on 5–12% volume elasticity

Data and category insights

Advanced retailer analytics increase transparency on performance, and in 2024 Orkla leveraged joint business plans with key retailers to ROI-proof promotions; category management preserves influence against buyer consolidation while superior shopper insights support assortment leadership and incremental margin capture.

- Retailer analytics: transparency

- Joint business plans: ROI-proofed promos

- Category mgmt: preserves influence

- Shopper insights: justify assortment

Nordic retail (>75%) and private labels raise promos and delisting risk

Concentrated Nordic retailing (>75% share by top chains in 2024) and credible private labels (EU 37% in 2023; Nordics 35–45%) amplify buyer leverage, raising promotion rates (+4–6ppt in 2024) and delisting risk. Orkla defends via national brands, category captaincy, RGM and SKU-level pricing (5–12% volume drop per 10% price rise). Joint business plans and analytics ROI-proof promotions.

| Metric | Value |

|---|---|

| Top retailers share (Nordics) | >75% (2024) |

| Private label EU | 37% (2023) |

| Nordic PL | 35–45% |

| Promo rate change | +4–6ppt (2024) |

| Food inflation | 3.2% (2024) |

| SKU elasticity | 5–12% vol per 10% price |

Preview the Actual Deliverable

Orkla Porter's Five Forces Analysis

This preview shows the complete Orkla Porter's Five Forces analysis you'll receive after purchase. It is the exact, fully formatted document—no placeholders or mockups—and is ready for immediate download and use. Purchase grants instant access to this same file.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Orkla's Porter's Five Forces snapshot highlights moderate supplier power, strong buyer expectations, a fragmented competitor landscape, manageable threat of new entrants, and rising substitute pressures from private labels and sustainability trends. This brief overview teases strategic risks and opportunities. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations tailored to Orkla.

Suppliers Bargaining Power

Fragmented agri and packaging base

In 2024 Orkla sources grains, oils, sugar and packaging from a fragmented global supplier base, which limits individual supplier leverage and supports negotiated terms. Commodity price volatility remained elevated following 2022–23 shocks and can still compress margins despite low supplier concentration. Orkla routinely dual-sources key inputs and leverages scale to negotiate better prices. Long-term frameworks and hedging partially mitigate supply shocks.

Specialty inputs with higher leverage

Fragrances, actives and certain specialty chemicals are highly concentrated — the top four fragrance companies (Givaudan, Firmenich, IFF, Symrise) held roughly 70% of the global market in 2024 — giving suppliers marked bargaining power. Stringent qualification and regulatory regimes such as EU REACH (over 22,000 registered substances) raise switching costs. Orkla’s multi-category volumes and strategic long-term partnerships help stabilize access and pricing.

Sustainability and traceability demands

Stricter Nordic ESG standards and the 2024 EU Packaging and Packaging Waste Regulation raise supplier compliance costs, narrowing eligible supplier pools for certified palm oil, cocoa and recyclable packaging. Reduced substitution options in these certified niches can increase supplier bargaining power where compliance is scarce. Orkla’s responsible sourcing programs and supplier development aim to expand the qualified base over time, mitigating concentration risks.

Energy and logistics exposure

Orkla's access to Norwegian hydropower (Norway's electricity mix ~90% hydropower in 2024) internalizes a portion of energy costs, but broader manufacturing and distribution remain exposed to global energy and freight markets where spot prices and fuel surcharges create input volatility.

Tight logistics capacity during demand spikes transfers bargaining power to carriers; regional production and nearshoring reduce distance and lead times but do not eliminate systemic shocks—contracting and longer-term freight agreements dampen volatility.

- Hydropower share: ~90% Norway (2024)

- Regional footprint: lowers transit risk, not systemic shocks

- Spot freight spikes increase carrier power

- Fixed contracts/nearshoring reduce price volatility

Scale and category breadth

Orkla’s scale across foods, personal care and home care strengthens supplier leverage by concentrating volume and specifying standardized inputs, reducing reliance on single-source vendors.

Consolidated purchasing and group-wide specifications enable substitution and drive lower input costs while multi-year contracts improve price stability and supply continuity.

- Scale-driven leverage

- Centralized procurement

- Multi-year contracts

- Portfolio-based substitution

Low bulk supplier concentration; ~70% in fragrances plus commodity volatility raise margin risk

Orkla faces low supplier concentration for bulk agri inputs, but commodity price volatility in 2024 keeps margin risk. Specialty fragrances/actives are concentrated (top 4 ~70% global share in 2024), raising switching costs. Scale, centralized procurement and multi-year contracts (plus Norway hydropower ~90% of mix in 2024) mitigate supplier leverage.

| Factor | 2024 datapoint |

|---|---|

| Fragrance concentration | Top 4 ~70% |

| Norway hydropower | ~90% |

| Mitigant | Centralized procurement, multi-year contracts |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers and substitutes tailored exclusively for Orkla, highlighting disruptive threats and strategic advantages within its consumer goods and branded-products portfolio.

Clear, one-sheet Porter's Five Forces for Orkla that visualizes supplier, buyer, entrant, substitute and rivalry pressures—perfect for rapid strategic decisions and boardroom use.

Customers Bargaining Power

Concentrated Nordic retail

Large chains such as NorgesGruppen, Coop, ICA, S Group and REMA 1000 concentrate buying power in the Nordics, with the top retailers capturing over 75% of grocery sales in 2024, forcing sharp pricing, promotional funding and stricter payment/terms. Delisting threats in mature categories intensify margin pressure. Orkla counters through strong national brands and formal category captaincy agreements to secure shelf space and promotional prioritization.

Private label expansion

Retailers’ private labels are credible low-price alternatives, with private label making roughly 37% of European grocery sales in 2023 and Nordic penetration typically in the 35–45% range, increasing buyer leverage.

Private label growth in Eastern Europe and India showed double-digit expansion in 2023, pressuring branded margins.

Orkla must defend shelf space through clear differentiation, faster NPD and category-tailored innovation, while driving cost efficiency and layered value tiers to hit buyer price points.

Channel mix diversification

Channel mix diversification reduces grocery dependence by shifting sales to out-of-home and pharmacy, but both channels have professionalized buyers; tender-based contracting in foodservice compresses margins while pharmacies prize compliance and efficacy data, enabling selective premium pricing; a multi-channel presence balances negotiating power across grocery, foodservice and pharmacy, smoothing margin volatility.

High price sensitivity

High price sensitivity: 2024 food inflation of 3.2% intensified retailer pushback on list-price hikes, driving more promotion-led assortments as consumers traded down to private labels.

Orkla counters with pack-price architecture and revenue growth management, using elasticity studies (SKU-level elasticities showing 5–12% volume drop per 10% price rise) to make selective pricing moves.

- Retailer pressure up — promotion rates +4–6ppt (2024)

- Orkla tools — pack-price, RGM, SKU elasticity

- Selective pricing based on 5–12% volume elasticity

Data and category insights

Advanced retailer analytics increase transparency on performance, and in 2024 Orkla leveraged joint business plans with key retailers to ROI-proof promotions; category management preserves influence against buyer consolidation while superior shopper insights support assortment leadership and incremental margin capture.

- Retailer analytics: transparency

- Joint business plans: ROI-proofed promos

- Category mgmt: preserves influence

- Shopper insights: justify assortment

Nordic retail (>75%) and private labels raise promos and delisting risk

Concentrated Nordic retailing (>75% share by top chains in 2024) and credible private labels (EU 37% in 2023; Nordics 35–45%) amplify buyer leverage, raising promotion rates (+4–6ppt in 2024) and delisting risk. Orkla defends via national brands, category captaincy, RGM and SKU-level pricing (5–12% volume drop per 10% price rise). Joint business plans and analytics ROI-proof promotions.

| Metric | Value |

|---|---|

| Top retailers share (Nordics) | >75% (2024) |

| Private label EU | 37% (2023) |

| Nordic PL | 35–45% |

| Promo rate change | +4–6ppt (2024) |

| Food inflation | 3.2% (2024) |

| SKU elasticity | 5–12% vol per 10% price |

Preview the Actual Deliverable

Orkla Porter's Five Forces Analysis

This preview shows the complete Orkla Porter's Five Forces analysis you'll receive after purchase. It is the exact, fully formatted document—no placeholders or mockups—and is ready for immediate download and use. Purchase grants instant access to this same file.