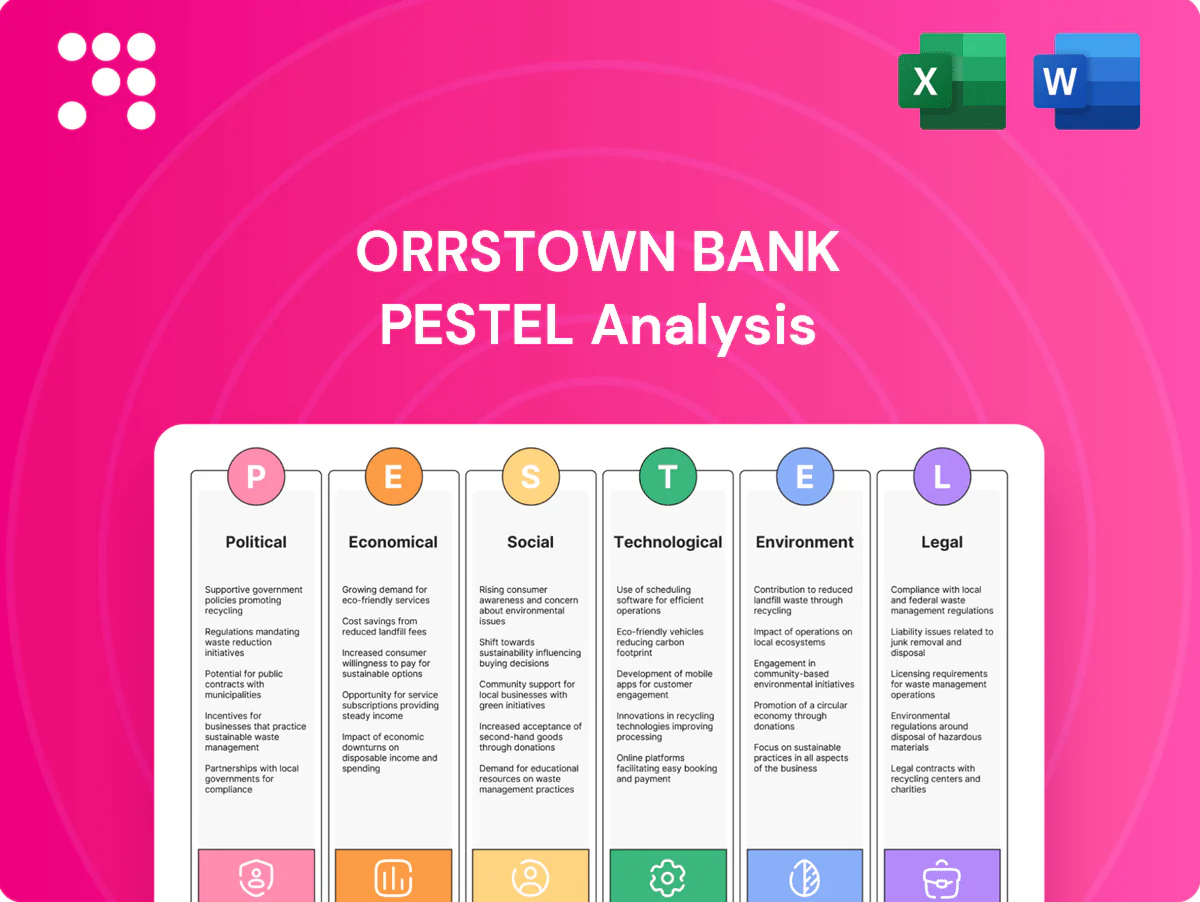

Orrstown Bank PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our targeted PESTLE Analysis of Orrstown Bank—pinpoint how political, economic, social, technological, legal, and environmental forces shape its growth and risk profile. Ideal for investors and strategists, this report delivers actionable, up-to-date insights. Purchase the full version to access the complete, editable analysis and make smarter decisions today.

Political factors

Monetary policy and community bank posture

Federal monetary policy, with the federal funds rate near 5.25% and constrained liquidity, raises funding costs and can dampen loan demand for Orrstown; shifts in Washington on community bank priorities influence SBA guarantee volumes and targeted relief programs. Increased supervisory intensity since 2023 has tightened capital planning, so Orrstown must time balance-sheet moves to policy cycles to preserve growth optionality.

State and local development agendas

Pennsylvania and Maryland incentives for small business, housing, and infrastructure—including state grant programs, tax credits and local abatements—support commercial and consumer credit pipelines and can improve loan feasibility; proactive engagement with county development authorities boosts deal flow for Orrstown Bank, while policy reversals or state/local budget cuts pose upside risk to origination volumes.

Cross-border market dynamics (PA–MD)

Operating across Pennsylvania (population ~12.8M, 67 counties) and Maryland (~6.2M, 23 counties plus Baltimore City) requires navigation of differing state banking nuances and municipal priorities. Local government relationships drive public deposits and project financing opportunities. Procurement rules and depository designations can affect fee income, and elections or admin changes can quickly reshuffle access to those relationships.

Public infrastructure and procurement cycles

Transportation, broadband and utilities projects under the IIJA (total $1.2 trillion, $550 billion new federal spending) and ongoing state programs create sizable construction financing and treasury opportunities for vendors and contractors; US municipal issuance was roughly $450 billion in 2024, underpinning deal flow. Timing of appropriations shapes construction lending pipelines and delays or cancellations raise pipeline fall‑through risk. Bank cash management services can anchor long‑term relationships and recurring fee income.

- Project finance: IIJA $1.2T / $550B new

- Market signal: ~ $450B US muni issuance (2024)

- Risk: appropriation delays increase fall‑through; cash management drives retention

Election-year policy uncertainty

Election cycles like the Nov 5, 2024 federal vote shift regulatory emphasis, tax policy and SBA/USDA program funding, creating near-term planning uncertainty for Orrstown Bank.

Borrowers often delay capex and expansion decisions in election quarters, softening loan demand; post-election clarity typically reaccelerates pipelines within 1–2 quarters.

Orrstown should scenario-plan for multiple policy outcomes, stress-testing loan origination, credit costs and SBA/USDA exposure under alternative regulatory/tax scenarios.

- Election date: Nov 5, 2024

- Borrower delay window: ~1–2 quarters

- Action: scenario-plan stress tests for origination and credit

Fed ~5.25% raises cost; IIJA,$450B munis lift PA/MD loans

Federal policy (fed funds ~5.25%) raises funding costs and can damp loan demand; increased supervisory intensity since 2023 tightens capital planning. PA/MD incentives and local relationships (PA pop 12.8M; MD 6.2M) support origination but budget reversals risk volumes. IIJA-driven project pipelines (IIJA $1.2T/$550B new) and ~$450B 2024 muni issuance create lending opportunities; election Nov 5, 2024 delays capex ~1–2 quarters, so scenario-plan.

| Factor | Key data |

|---|---|

| Fed rate | ~5.25% |

| PA/MD pop | 12.8M / 6.2M |

| IIJA | $1.2T / $550B new |

| Muni issuance 2024 | ~$450B |

| Election | Nov 5, 2024 (delay 1–2 qtrs) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Orrstown Bank—grounded in regional market trends, regulatory shifts, and competitive dynamics. Designed to give executives and investors data-backed, forward-looking insights to spot risks and strategic opportunities.

Concise PESTLE summary of Orrstown Bank that’s visually segmented for quick interpretation and easily dropped into presentations to align teams and support risk discussions.

Economic factors

Interest rate cycle and net interest margin

Rising Fed funds at 5.25–5.50% in 2024 pushed asset yields higher but increased deposit betas and NIM volatility; community bank median NIM was about 3.3% in 2024 (FDIC). Rapid rate shifts stress Orrstown’s funding mix and reprice credit risk, making balance sheet hedging and disciplined product pricing critical. Stabilizing margins improves earnings visibility and capital planning.

Regional small-business health

South‑central Pennsylvania and Maryland small and medium enterprises anchor Orrstown Bank’s commercial lending and deposit base; US Census Bureau/SBA reports ~33.2 million small businesses nationwide, accounting for roughly 47% of private‑sector employment, underscoring SME importance to regional deposits. Employment trends, wage pressures, and rising input costs compress credit appetite and affect asset quality, while industry diversification in the region helps dampen local shocks; tailored treasury and payment services can deepen wallet share.

Housing market and mortgage demand

Higher 30-year rates near 7.0% (Freddie Mac, mid‑2025) have compressed purchase and refinance volumes, while national median home price around $390,000 sustains HELOC capacity for borrowers with equity. Low inventory (~2.6 months supply) and steady starts (~1.4M annualized) shift opportunity to construction lending. Tightening credit overlays reflect affordability stress, and wider TBA/MSR hedging costs (≈20–30 bps YTD) squeeze gain‑on‑sale and capital velocity.

Credit quality and delinquency trends

Economic slowdowns raise NPAs across CRE, C&I and consumer portfolios, so Orrstown emphasizes close portfolio monitoring and forward-looking stress tests to detect deterioration early.

Conservative LTV limits and tight covenant enforcement help limit loss severity, while prompt, documented workout strategies aim to preserve capital and recover values.

- monitoring: proactive portfolio reviews

- stress-testing: scenario-driven

- underwriting: conservative LTVs/covenants

- workouts: timely recovery focus

Deposit competition and liquidity

Competition from larger banks and fintechs has pushed cost of funds higher, with the Federal Reserve funds target settling near 5.25–5.50% in mid‑2025, raising deposit pricing pressure on community banks like Orrstown.

Shift toward higher‑yield accounts and away from noninterest‑bearing balances compresses net interest margin, while relationship pricing and value‑added services support retention and cross‑sell.

Contingent liquidity lines and brokered lines reduce funding risk and shore up short‑term liquidity amid concentration: the top five US banks hold roughly 45% of domestic deposits, intensifying competitive pressure.

- Higher market rates: Fed funds ~5.25–5.50% (mid‑2025)

- Deposit concentration: top 5 banks ~45% of deposits

- Margin pressure from mix shift to interest‑bearing accounts

- Mitigant: relationship pricing, value‑adds, contingent liquidity lines

Fed ~5.25% raises cost; IIJA,$450B munis lift PA/MD loans

Higher Fed funds (~5.25–5.50% mid‑2025) lifted asset yields but raised deposit betas and NIM volatility (community bank median NIM ~3.3% in 2024); CRE/consumer stress and slower mortgage volumes (30‑yr ~7.0%, median home price ~$390k) heighten credit and hedging costs (TBA/MSR ≈20–30bps), making disciplined pricing, stress‑testing and contingent liquidity essential.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Median NIM (2024) | 3.3% |

| 30‑yr rate | ≈7.0% |

| Median home price | $390,000 |

Preview Before You Purchase

Orrstown Bank PESTLE Analysis

The Orrstown Bank PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes professionally structured political, economic, social, technological, legal, and environmental insights. No placeholders or teasers; this is the final file. Downloadable immediately after payment.

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our targeted PESTLE Analysis of Orrstown Bank—pinpoint how political, economic, social, technological, legal, and environmental forces shape its growth and risk profile. Ideal for investors and strategists, this report delivers actionable, up-to-date insights. Purchase the full version to access the complete, editable analysis and make smarter decisions today.

Political factors

Monetary policy and community bank posture

Federal monetary policy, with the federal funds rate near 5.25% and constrained liquidity, raises funding costs and can dampen loan demand for Orrstown; shifts in Washington on community bank priorities influence SBA guarantee volumes and targeted relief programs. Increased supervisory intensity since 2023 has tightened capital planning, so Orrstown must time balance-sheet moves to policy cycles to preserve growth optionality.

State and local development agendas

Pennsylvania and Maryland incentives for small business, housing, and infrastructure—including state grant programs, tax credits and local abatements—support commercial and consumer credit pipelines and can improve loan feasibility; proactive engagement with county development authorities boosts deal flow for Orrstown Bank, while policy reversals or state/local budget cuts pose upside risk to origination volumes.

Cross-border market dynamics (PA–MD)

Operating across Pennsylvania (population ~12.8M, 67 counties) and Maryland (~6.2M, 23 counties plus Baltimore City) requires navigation of differing state banking nuances and municipal priorities. Local government relationships drive public deposits and project financing opportunities. Procurement rules and depository designations can affect fee income, and elections or admin changes can quickly reshuffle access to those relationships.

Public infrastructure and procurement cycles

Transportation, broadband and utilities projects under the IIJA (total $1.2 trillion, $550 billion new federal spending) and ongoing state programs create sizable construction financing and treasury opportunities for vendors and contractors; US municipal issuance was roughly $450 billion in 2024, underpinning deal flow. Timing of appropriations shapes construction lending pipelines and delays or cancellations raise pipeline fall‑through risk. Bank cash management services can anchor long‑term relationships and recurring fee income.

- Project finance: IIJA $1.2T / $550B new

- Market signal: ~ $450B US muni issuance (2024)

- Risk: appropriation delays increase fall‑through; cash management drives retention

Election-year policy uncertainty

Election cycles like the Nov 5, 2024 federal vote shift regulatory emphasis, tax policy and SBA/USDA program funding, creating near-term planning uncertainty for Orrstown Bank.

Borrowers often delay capex and expansion decisions in election quarters, softening loan demand; post-election clarity typically reaccelerates pipelines within 1–2 quarters.

Orrstown should scenario-plan for multiple policy outcomes, stress-testing loan origination, credit costs and SBA/USDA exposure under alternative regulatory/tax scenarios.

- Election date: Nov 5, 2024

- Borrower delay window: ~1–2 quarters

- Action: scenario-plan stress tests for origination and credit

Fed ~5.25% raises cost; IIJA,$450B munis lift PA/MD loans

Federal policy (fed funds ~5.25%) raises funding costs and can damp loan demand; increased supervisory intensity since 2023 tightens capital planning. PA/MD incentives and local relationships (PA pop 12.8M; MD 6.2M) support origination but budget reversals risk volumes. IIJA-driven project pipelines (IIJA $1.2T/$550B new) and ~$450B 2024 muni issuance create lending opportunities; election Nov 5, 2024 delays capex ~1–2 quarters, so scenario-plan.

| Factor | Key data |

|---|---|

| Fed rate | ~5.25% |

| PA/MD pop | 12.8M / 6.2M |

| IIJA | $1.2T / $550B new |

| Muni issuance 2024 | ~$450B |

| Election | Nov 5, 2024 (delay 1–2 qtrs) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Orrstown Bank—grounded in regional market trends, regulatory shifts, and competitive dynamics. Designed to give executives and investors data-backed, forward-looking insights to spot risks and strategic opportunities.

Concise PESTLE summary of Orrstown Bank that’s visually segmented for quick interpretation and easily dropped into presentations to align teams and support risk discussions.

Economic factors

Interest rate cycle and net interest margin

Rising Fed funds at 5.25–5.50% in 2024 pushed asset yields higher but increased deposit betas and NIM volatility; community bank median NIM was about 3.3% in 2024 (FDIC). Rapid rate shifts stress Orrstown’s funding mix and reprice credit risk, making balance sheet hedging and disciplined product pricing critical. Stabilizing margins improves earnings visibility and capital planning.

Regional small-business health

South‑central Pennsylvania and Maryland small and medium enterprises anchor Orrstown Bank’s commercial lending and deposit base; US Census Bureau/SBA reports ~33.2 million small businesses nationwide, accounting for roughly 47% of private‑sector employment, underscoring SME importance to regional deposits. Employment trends, wage pressures, and rising input costs compress credit appetite and affect asset quality, while industry diversification in the region helps dampen local shocks; tailored treasury and payment services can deepen wallet share.

Housing market and mortgage demand

Higher 30-year rates near 7.0% (Freddie Mac, mid‑2025) have compressed purchase and refinance volumes, while national median home price around $390,000 sustains HELOC capacity for borrowers with equity. Low inventory (~2.6 months supply) and steady starts (~1.4M annualized) shift opportunity to construction lending. Tightening credit overlays reflect affordability stress, and wider TBA/MSR hedging costs (≈20–30 bps YTD) squeeze gain‑on‑sale and capital velocity.

Credit quality and delinquency trends

Economic slowdowns raise NPAs across CRE, C&I and consumer portfolios, so Orrstown emphasizes close portfolio monitoring and forward-looking stress tests to detect deterioration early.

Conservative LTV limits and tight covenant enforcement help limit loss severity, while prompt, documented workout strategies aim to preserve capital and recover values.

- monitoring: proactive portfolio reviews

- stress-testing: scenario-driven

- underwriting: conservative LTVs/covenants

- workouts: timely recovery focus

Deposit competition and liquidity

Competition from larger banks and fintechs has pushed cost of funds higher, with the Federal Reserve funds target settling near 5.25–5.50% in mid‑2025, raising deposit pricing pressure on community banks like Orrstown.

Shift toward higher‑yield accounts and away from noninterest‑bearing balances compresses net interest margin, while relationship pricing and value‑added services support retention and cross‑sell.

Contingent liquidity lines and brokered lines reduce funding risk and shore up short‑term liquidity amid concentration: the top five US banks hold roughly 45% of domestic deposits, intensifying competitive pressure.

- Higher market rates: Fed funds ~5.25–5.50% (mid‑2025)

- Deposit concentration: top 5 banks ~45% of deposits

- Margin pressure from mix shift to interest‑bearing accounts

- Mitigant: relationship pricing, value‑adds, contingent liquidity lines

Fed ~5.25% raises cost; IIJA,$450B munis lift PA/MD loans

Higher Fed funds (~5.25–5.50% mid‑2025) lifted asset yields but raised deposit betas and NIM volatility (community bank median NIM ~3.3% in 2024); CRE/consumer stress and slower mortgage volumes (30‑yr ~7.0%, median home price ~$390k) heighten credit and hedging costs (TBA/MSR ≈20–30bps), making disciplined pricing, stress‑testing and contingent liquidity essential.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Median NIM (2024) | 3.3% |

| 30‑yr rate | ≈7.0% |

| Median home price | $390,000 |

Preview Before You Purchase

Orrstown Bank PESTLE Analysis

The Orrstown Bank PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes professionally structured political, economic, social, technological, legal, and environmental insights. No placeholders or teasers; this is the final file. Downloadable immediately after payment.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our targeted PESTLE Analysis of Orrstown Bank—pinpoint how political, economic, social, technological, legal, and environmental forces shape its growth and risk profile. Ideal for investors and strategists, this report delivers actionable, up-to-date insights. Purchase the full version to access the complete, editable analysis and make smarter decisions today.

Political factors

Monetary policy and community bank posture

Federal monetary policy, with the federal funds rate near 5.25% and constrained liquidity, raises funding costs and can dampen loan demand for Orrstown; shifts in Washington on community bank priorities influence SBA guarantee volumes and targeted relief programs. Increased supervisory intensity since 2023 has tightened capital planning, so Orrstown must time balance-sheet moves to policy cycles to preserve growth optionality.

State and local development agendas

Pennsylvania and Maryland incentives for small business, housing, and infrastructure—including state grant programs, tax credits and local abatements—support commercial and consumer credit pipelines and can improve loan feasibility; proactive engagement with county development authorities boosts deal flow for Orrstown Bank, while policy reversals or state/local budget cuts pose upside risk to origination volumes.

Cross-border market dynamics (PA–MD)

Operating across Pennsylvania (population ~12.8M, 67 counties) and Maryland (~6.2M, 23 counties plus Baltimore City) requires navigation of differing state banking nuances and municipal priorities. Local government relationships drive public deposits and project financing opportunities. Procurement rules and depository designations can affect fee income, and elections or admin changes can quickly reshuffle access to those relationships.

Public infrastructure and procurement cycles

Transportation, broadband and utilities projects under the IIJA (total $1.2 trillion, $550 billion new federal spending) and ongoing state programs create sizable construction financing and treasury opportunities for vendors and contractors; US municipal issuance was roughly $450 billion in 2024, underpinning deal flow. Timing of appropriations shapes construction lending pipelines and delays or cancellations raise pipeline fall‑through risk. Bank cash management services can anchor long‑term relationships and recurring fee income.

- Project finance: IIJA $1.2T / $550B new

- Market signal: ~ $450B US muni issuance (2024)

- Risk: appropriation delays increase fall‑through; cash management drives retention

Election-year policy uncertainty

Election cycles like the Nov 5, 2024 federal vote shift regulatory emphasis, tax policy and SBA/USDA program funding, creating near-term planning uncertainty for Orrstown Bank.

Borrowers often delay capex and expansion decisions in election quarters, softening loan demand; post-election clarity typically reaccelerates pipelines within 1–2 quarters.

Orrstown should scenario-plan for multiple policy outcomes, stress-testing loan origination, credit costs and SBA/USDA exposure under alternative regulatory/tax scenarios.

- Election date: Nov 5, 2024

- Borrower delay window: ~1–2 quarters

- Action: scenario-plan stress tests for origination and credit

Fed ~5.25% raises cost; IIJA,$450B munis lift PA/MD loans

Federal policy (fed funds ~5.25%) raises funding costs and can damp loan demand; increased supervisory intensity since 2023 tightens capital planning. PA/MD incentives and local relationships (PA pop 12.8M; MD 6.2M) support origination but budget reversals risk volumes. IIJA-driven project pipelines (IIJA $1.2T/$550B new) and ~$450B 2024 muni issuance create lending opportunities; election Nov 5, 2024 delays capex ~1–2 quarters, so scenario-plan.

| Factor | Key data |

|---|---|

| Fed rate | ~5.25% |

| PA/MD pop | 12.8M / 6.2M |

| IIJA | $1.2T / $550B new |

| Muni issuance 2024 | ~$450B |

| Election | Nov 5, 2024 (delay 1–2 qtrs) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Orrstown Bank—grounded in regional market trends, regulatory shifts, and competitive dynamics. Designed to give executives and investors data-backed, forward-looking insights to spot risks and strategic opportunities.

Concise PESTLE summary of Orrstown Bank that’s visually segmented for quick interpretation and easily dropped into presentations to align teams and support risk discussions.

Economic factors

Interest rate cycle and net interest margin

Rising Fed funds at 5.25–5.50% in 2024 pushed asset yields higher but increased deposit betas and NIM volatility; community bank median NIM was about 3.3% in 2024 (FDIC). Rapid rate shifts stress Orrstown’s funding mix and reprice credit risk, making balance sheet hedging and disciplined product pricing critical. Stabilizing margins improves earnings visibility and capital planning.

Regional small-business health

South‑central Pennsylvania and Maryland small and medium enterprises anchor Orrstown Bank’s commercial lending and deposit base; US Census Bureau/SBA reports ~33.2 million small businesses nationwide, accounting for roughly 47% of private‑sector employment, underscoring SME importance to regional deposits. Employment trends, wage pressures, and rising input costs compress credit appetite and affect asset quality, while industry diversification in the region helps dampen local shocks; tailored treasury and payment services can deepen wallet share.

Housing market and mortgage demand

Higher 30-year rates near 7.0% (Freddie Mac, mid‑2025) have compressed purchase and refinance volumes, while national median home price around $390,000 sustains HELOC capacity for borrowers with equity. Low inventory (~2.6 months supply) and steady starts (~1.4M annualized) shift opportunity to construction lending. Tightening credit overlays reflect affordability stress, and wider TBA/MSR hedging costs (≈20–30 bps YTD) squeeze gain‑on‑sale and capital velocity.

Credit quality and delinquency trends

Economic slowdowns raise NPAs across CRE, C&I and consumer portfolios, so Orrstown emphasizes close portfolio monitoring and forward-looking stress tests to detect deterioration early.

Conservative LTV limits and tight covenant enforcement help limit loss severity, while prompt, documented workout strategies aim to preserve capital and recover values.

- monitoring: proactive portfolio reviews

- stress-testing: scenario-driven

- underwriting: conservative LTVs/covenants

- workouts: timely recovery focus

Deposit competition and liquidity

Competition from larger banks and fintechs has pushed cost of funds higher, with the Federal Reserve funds target settling near 5.25–5.50% in mid‑2025, raising deposit pricing pressure on community banks like Orrstown.

Shift toward higher‑yield accounts and away from noninterest‑bearing balances compresses net interest margin, while relationship pricing and value‑added services support retention and cross‑sell.

Contingent liquidity lines and brokered lines reduce funding risk and shore up short‑term liquidity amid concentration: the top five US banks hold roughly 45% of domestic deposits, intensifying competitive pressure.

- Higher market rates: Fed funds ~5.25–5.50% (mid‑2025)

- Deposit concentration: top 5 banks ~45% of deposits

- Margin pressure from mix shift to interest‑bearing accounts

- Mitigant: relationship pricing, value‑adds, contingent liquidity lines

Fed ~5.25% raises cost; IIJA,$450B munis lift PA/MD loans

Higher Fed funds (~5.25–5.50% mid‑2025) lifted asset yields but raised deposit betas and NIM volatility (community bank median NIM ~3.3% in 2024); CRE/consumer stress and slower mortgage volumes (30‑yr ~7.0%, median home price ~$390k) heighten credit and hedging costs (TBA/MSR ≈20–30bps), making disciplined pricing, stress‑testing and contingent liquidity essential.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Median NIM (2024) | 3.3% |

| 30‑yr rate | ≈7.0% |

| Median home price | $390,000 |

Preview Before You Purchase

Orrstown Bank PESTLE Analysis

The Orrstown Bank PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes professionally structured political, economic, social, technological, legal, and environmental insights. No placeholders or teasers; this is the final file. Downloadable immediately after payment.