Orrstown Bank SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

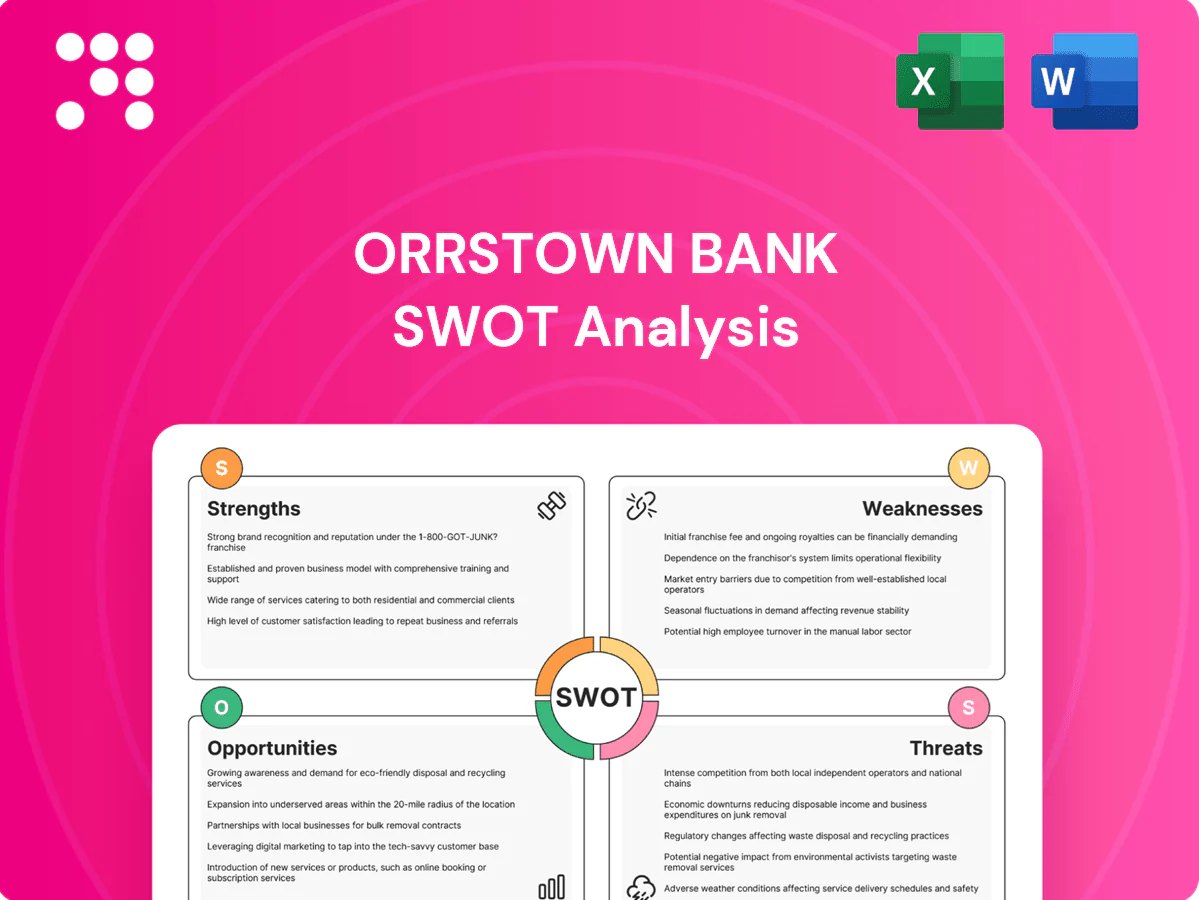

Orrstown Bank's SWOT snapshot highlights resilient community banking strengths, regional growth opportunities, and emerging risks from rate pressure and competition. Want the full story behind its strategic position and financial nuances? Purchase the complete SWOT analysis for a professionally formatted, editable report and Excel matrix to support investing, planning, and presentations.

Strengths

Deep community presence in PA-MD footprint

Headquartered in Shippensburg, PA, Orrstown Bank’s decades-long presence across south-central Pennsylvania and northern Maryland builds trust with households and SMEs, driving referral-heavy lending and low-cost deposits; local credit decisioning enables faster approvals and tailored solutions, giving Orrstown resilience against national banks in its targeted footprint.

Diversified product suite across deposits, loans, wealth

Orrstown’s offering of commercial, residential and consumer lending alongside wealth management broadens revenue streams and reduces concentration risk. Cross-sell opportunities between deposit, loan and advisory clients raise customer lifetime value and improve retention. Fee income from wealth services helps offset pressure on net interest margins. Full-service positioning strengthens competitiveness versus mono-line lenders.

Relationship banking and tailored credit

Orrstown Bank, with roughly $3.4 billion in assets as of 2024, uses local underwriting to improve credit selection and borrower fit, reducing default rates versus standardized portfolios. Customized pricing and terms differentiate it from big-bank offers, while relationship managers increase share-of-wallet—often boosting deposit and loan cross-sell by several percentage points annually. This approach can enhance yields while preserving prudent risk controls.

Stable core deposits from local customers

Orrstown Bank benefits from stable core deposits from local customers, with a high share of non-interest-bearing and low-cost transaction accounts that lower the bank’s overall cost of funds and support net interest margin. This stability reduces reliance on volatile wholesale funding and underpins steady loan growth in mortgage, small-business, and consumer segments.

- Low-cost core funding

- Higher NIM support

- Reduced wholesale exposure

- Consistent core-segment loan growth

Agile governance and faster execution

Orrstown Bank's smaller scale (about 22 branches and roughly $2.6 billion in assets as of 2024) enables quicker product tweaks and pricing shifts, letting management pivot to local economic signals faster than larger peers; shorter chains of command accelerate credit and service decisions, converting agility into market share gains in niche central Pennsylvania segments.

- Faster pricing adjustments

- Rapid credit decisions

- Local market responsiveness

- Targeted niche share growth

Deep local banking: 22 branches, low-cost deposits and agile underwriting

Deep local footprint and relationship banking drive referral lending and low-cost core deposits, supporting resilient NIM and lower funding volatility. Diversified revenue from commercial, consumer, mortgage and wealth advisory improves fee income and reduces concentration risk. Small scale (22 branches) enables rapid pricing, underwriting agility and targeted share gains in central PA.

| Metric | 2024 |

|---|---|

| Branches | 22 |

| Total assets | $3.4B |

| Core funding | High share of low-cost deposits |

What is included in the product

Provides a concise SWOT overview of Orrstown Bank’s internal capabilities and external risks, highlighting strengths like community focus and asset quality, weaknesses such as scale constraints, opportunities from digital expansion and M&A, and threats from rate volatility and competition.

Provides a concise SWOT matrix tailored to Orrstown Bank for fast strategic alignment, clarifying key risks and growth opportunities for quick stakeholder decisions.

Weaknesses

Geographic concentration risk

Operations concentrated in south-central Pennsylvania and Maryland leave Orrstown exposed to local downturns; the bank reported approximately $2.6 billion in assets as of mid-2024, largely originating within this footprint. Industry clustering in the service, agriculture and manufacturing sectors can amplify regional cyclicality. Limited geographic diversification reduces shock absorption versus peers with multi-state footprints, so a single-event disruption could materially impair earnings and asset quality.

Scale disadvantages vs. large banks

Orrstown’s modest asset base (community-bank scale vs national banks with assets in the >$1 trillion range) constrains technology spend and product breadth, keeping digital rollout slower and third-party integration limited. Higher unit costs push its efficiency ratio above large-bank peers, compressing net interest margin and ROA. Pricing power on deposits and loans is weaker versus national competitors, while vendor and compliance expenses represent a larger share of noninterest costs, weighing on margins.

Interest rate sensitivity and margin pressure

Community banks like Orrstown face asset-liability gaps that make NIM vulnerable to rapid rate swings; the recent high-rate environment (federal funds near 5.25–5.50% in 2023–24) compressed spreads and slowed loan demand. Repricing lags on deposits versus loans have squeezed earnings as deposit betas rose faster than loan yields. Limited scale raises hedging costs and reduces available ALM tools.

Constrained brand awareness beyond core markets

Constrained brand awareness beyond core markets limits Orrstown Bank’s ability to penetrate adjacent counties and neighboring states, forcing heavier reliance on legacy branches and referrals. Acquiring customers outside its footprint drives up marketing and onboarding costs and leaves Orrstown vulnerable when competing directly with larger, better-known regional banks. This dampens growth in wealth management and specialty lending initiatives.

- Limited marketing reach

- Higher customer acquisition costs

- Direct competition with stronger regional brands

- Slower expansion of wealth and specialty lending

Concentration in CRE and mortgages typical of peers

Concentration in commercial real estate and 1-4 family mortgages mirrors peer community banks and raises sensitivity to sector-specific stress; FDIC 2024 industry data showed CRE and residential mortgage exposure remained a leading share of community bank portfolios. Elevated CRE/mortgage mix can amplify credit losses in downturns and invite closer regulatory scrutiny that limits growth in higher-risk lending buckets. A tilted portfolio mix reduces strategic flexibility during market weakness.

- Higher CRE/1-4 exposure — amplifies cyclical loss risk

- Regulatory caps/scrutiny — can constrain higher-yield growth

- Concentrated mix — limits liquidity and repricing options in downturns

South-central PA/MD focus and $2.6B scale raise CRE exposure and margin pressure

Operations concentrated in south-central PA and MD with ~2.6B assets (mid-2024) exposes Orrstown to regional downturns and sector cyclicality.

Modest scale limits tech/product investment, keeps efficiency ratio above large peers and raises unit costs, compressing NIM and ROA.

High CRE/1–4 mortgage exposure (FDIC 2024—leading share for community banks) and limited brand reach constrain growth and amplify credit risk.

| Metric | Value/Note |

|---|---|

| Assets (mid-2024) | $2.6B |

| Fed funds (2023–24) | ~5.25–5.50% |

| CRE/1–4 exposure | Leading share for community banks (FDIC 2024) |

Same Document Delivered

Orrstown Bank SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. You’re viewing a live preview of the real file—buy now to download the full, detailed Orrstown Bank SWOT.

Dive Deeper Into the Company’s Strategic Blueprint

Orrstown Bank's SWOT snapshot highlights resilient community banking strengths, regional growth opportunities, and emerging risks from rate pressure and competition. Want the full story behind its strategic position and financial nuances? Purchase the complete SWOT analysis for a professionally formatted, editable report and Excel matrix to support investing, planning, and presentations.

Strengths

Deep community presence in PA-MD footprint

Headquartered in Shippensburg, PA, Orrstown Bank’s decades-long presence across south-central Pennsylvania and northern Maryland builds trust with households and SMEs, driving referral-heavy lending and low-cost deposits; local credit decisioning enables faster approvals and tailored solutions, giving Orrstown resilience against national banks in its targeted footprint.

Diversified product suite across deposits, loans, wealth

Orrstown’s offering of commercial, residential and consumer lending alongside wealth management broadens revenue streams and reduces concentration risk. Cross-sell opportunities between deposit, loan and advisory clients raise customer lifetime value and improve retention. Fee income from wealth services helps offset pressure on net interest margins. Full-service positioning strengthens competitiveness versus mono-line lenders.

Relationship banking and tailored credit

Orrstown Bank, with roughly $3.4 billion in assets as of 2024, uses local underwriting to improve credit selection and borrower fit, reducing default rates versus standardized portfolios. Customized pricing and terms differentiate it from big-bank offers, while relationship managers increase share-of-wallet—often boosting deposit and loan cross-sell by several percentage points annually. This approach can enhance yields while preserving prudent risk controls.

Stable core deposits from local customers

Orrstown Bank benefits from stable core deposits from local customers, with a high share of non-interest-bearing and low-cost transaction accounts that lower the bank’s overall cost of funds and support net interest margin. This stability reduces reliance on volatile wholesale funding and underpins steady loan growth in mortgage, small-business, and consumer segments.

- Low-cost core funding

- Higher NIM support

- Reduced wholesale exposure

- Consistent core-segment loan growth

Agile governance and faster execution

Orrstown Bank's smaller scale (about 22 branches and roughly $2.6 billion in assets as of 2024) enables quicker product tweaks and pricing shifts, letting management pivot to local economic signals faster than larger peers; shorter chains of command accelerate credit and service decisions, converting agility into market share gains in niche central Pennsylvania segments.

- Faster pricing adjustments

- Rapid credit decisions

- Local market responsiveness

- Targeted niche share growth

Deep local banking: 22 branches, low-cost deposits and agile underwriting

Deep local footprint and relationship banking drive referral lending and low-cost core deposits, supporting resilient NIM and lower funding volatility. Diversified revenue from commercial, consumer, mortgage and wealth advisory improves fee income and reduces concentration risk. Small scale (22 branches) enables rapid pricing, underwriting agility and targeted share gains in central PA.

| Metric | 2024 |

|---|---|

| Branches | 22 |

| Total assets | $3.4B |

| Core funding | High share of low-cost deposits |

What is included in the product

Provides a concise SWOT overview of Orrstown Bank’s internal capabilities and external risks, highlighting strengths like community focus and asset quality, weaknesses such as scale constraints, opportunities from digital expansion and M&A, and threats from rate volatility and competition.

Provides a concise SWOT matrix tailored to Orrstown Bank for fast strategic alignment, clarifying key risks and growth opportunities for quick stakeholder decisions.

Weaknesses

Geographic concentration risk

Operations concentrated in south-central Pennsylvania and Maryland leave Orrstown exposed to local downturns; the bank reported approximately $2.6 billion in assets as of mid-2024, largely originating within this footprint. Industry clustering in the service, agriculture and manufacturing sectors can amplify regional cyclicality. Limited geographic diversification reduces shock absorption versus peers with multi-state footprints, so a single-event disruption could materially impair earnings and asset quality.

Scale disadvantages vs. large banks

Orrstown’s modest asset base (community-bank scale vs national banks with assets in the >$1 trillion range) constrains technology spend and product breadth, keeping digital rollout slower and third-party integration limited. Higher unit costs push its efficiency ratio above large-bank peers, compressing net interest margin and ROA. Pricing power on deposits and loans is weaker versus national competitors, while vendor and compliance expenses represent a larger share of noninterest costs, weighing on margins.

Interest rate sensitivity and margin pressure

Community banks like Orrstown face asset-liability gaps that make NIM vulnerable to rapid rate swings; the recent high-rate environment (federal funds near 5.25–5.50% in 2023–24) compressed spreads and slowed loan demand. Repricing lags on deposits versus loans have squeezed earnings as deposit betas rose faster than loan yields. Limited scale raises hedging costs and reduces available ALM tools.

Constrained brand awareness beyond core markets

Constrained brand awareness beyond core markets limits Orrstown Bank’s ability to penetrate adjacent counties and neighboring states, forcing heavier reliance on legacy branches and referrals. Acquiring customers outside its footprint drives up marketing and onboarding costs and leaves Orrstown vulnerable when competing directly with larger, better-known regional banks. This dampens growth in wealth management and specialty lending initiatives.

- Limited marketing reach

- Higher customer acquisition costs

- Direct competition with stronger regional brands

- Slower expansion of wealth and specialty lending

Concentration in CRE and mortgages typical of peers

Concentration in commercial real estate and 1-4 family mortgages mirrors peer community banks and raises sensitivity to sector-specific stress; FDIC 2024 industry data showed CRE and residential mortgage exposure remained a leading share of community bank portfolios. Elevated CRE/mortgage mix can amplify credit losses in downturns and invite closer regulatory scrutiny that limits growth in higher-risk lending buckets. A tilted portfolio mix reduces strategic flexibility during market weakness.

- Higher CRE/1-4 exposure — amplifies cyclical loss risk

- Regulatory caps/scrutiny — can constrain higher-yield growth

- Concentrated mix — limits liquidity and repricing options in downturns

South-central PA/MD focus and $2.6B scale raise CRE exposure and margin pressure

Operations concentrated in south-central PA and MD with ~2.6B assets (mid-2024) exposes Orrstown to regional downturns and sector cyclicality.

Modest scale limits tech/product investment, keeps efficiency ratio above large peers and raises unit costs, compressing NIM and ROA.

High CRE/1–4 mortgage exposure (FDIC 2024—leading share for community banks) and limited brand reach constrain growth and amplify credit risk.

| Metric | Value/Note |

|---|---|

| Assets (mid-2024) | $2.6B |

| Fed funds (2023–24) | ~5.25–5.50% |

| CRE/1–4 exposure | Leading share for community banks (FDIC 2024) |

Same Document Delivered

Orrstown Bank SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. You’re viewing a live preview of the real file—buy now to download the full, detailed Orrstown Bank SWOT.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Orrstown Bank's SWOT snapshot highlights resilient community banking strengths, regional growth opportunities, and emerging risks from rate pressure and competition. Want the full story behind its strategic position and financial nuances? Purchase the complete SWOT analysis for a professionally formatted, editable report and Excel matrix to support investing, planning, and presentations.

Strengths

Deep community presence in PA-MD footprint

Headquartered in Shippensburg, PA, Orrstown Bank’s decades-long presence across south-central Pennsylvania and northern Maryland builds trust with households and SMEs, driving referral-heavy lending and low-cost deposits; local credit decisioning enables faster approvals and tailored solutions, giving Orrstown resilience against national banks in its targeted footprint.

Diversified product suite across deposits, loans, wealth

Orrstown’s offering of commercial, residential and consumer lending alongside wealth management broadens revenue streams and reduces concentration risk. Cross-sell opportunities between deposit, loan and advisory clients raise customer lifetime value and improve retention. Fee income from wealth services helps offset pressure on net interest margins. Full-service positioning strengthens competitiveness versus mono-line lenders.

Relationship banking and tailored credit

Orrstown Bank, with roughly $3.4 billion in assets as of 2024, uses local underwriting to improve credit selection and borrower fit, reducing default rates versus standardized portfolios. Customized pricing and terms differentiate it from big-bank offers, while relationship managers increase share-of-wallet—often boosting deposit and loan cross-sell by several percentage points annually. This approach can enhance yields while preserving prudent risk controls.

Stable core deposits from local customers

Orrstown Bank benefits from stable core deposits from local customers, with a high share of non-interest-bearing and low-cost transaction accounts that lower the bank’s overall cost of funds and support net interest margin. This stability reduces reliance on volatile wholesale funding and underpins steady loan growth in mortgage, small-business, and consumer segments.

- Low-cost core funding

- Higher NIM support

- Reduced wholesale exposure

- Consistent core-segment loan growth

Agile governance and faster execution

Orrstown Bank's smaller scale (about 22 branches and roughly $2.6 billion in assets as of 2024) enables quicker product tweaks and pricing shifts, letting management pivot to local economic signals faster than larger peers; shorter chains of command accelerate credit and service decisions, converting agility into market share gains in niche central Pennsylvania segments.

- Faster pricing adjustments

- Rapid credit decisions

- Local market responsiveness

- Targeted niche share growth

Deep local banking: 22 branches, low-cost deposits and agile underwriting

Deep local footprint and relationship banking drive referral lending and low-cost core deposits, supporting resilient NIM and lower funding volatility. Diversified revenue from commercial, consumer, mortgage and wealth advisory improves fee income and reduces concentration risk. Small scale (22 branches) enables rapid pricing, underwriting agility and targeted share gains in central PA.

| Metric | 2024 |

|---|---|

| Branches | 22 |

| Total assets | $3.4B |

| Core funding | High share of low-cost deposits |

What is included in the product

Provides a concise SWOT overview of Orrstown Bank’s internal capabilities and external risks, highlighting strengths like community focus and asset quality, weaknesses such as scale constraints, opportunities from digital expansion and M&A, and threats from rate volatility and competition.

Provides a concise SWOT matrix tailored to Orrstown Bank for fast strategic alignment, clarifying key risks and growth opportunities for quick stakeholder decisions.

Weaknesses

Geographic concentration risk

Operations concentrated in south-central Pennsylvania and Maryland leave Orrstown exposed to local downturns; the bank reported approximately $2.6 billion in assets as of mid-2024, largely originating within this footprint. Industry clustering in the service, agriculture and manufacturing sectors can amplify regional cyclicality. Limited geographic diversification reduces shock absorption versus peers with multi-state footprints, so a single-event disruption could materially impair earnings and asset quality.

Scale disadvantages vs. large banks

Orrstown’s modest asset base (community-bank scale vs national banks with assets in the >$1 trillion range) constrains technology spend and product breadth, keeping digital rollout slower and third-party integration limited. Higher unit costs push its efficiency ratio above large-bank peers, compressing net interest margin and ROA. Pricing power on deposits and loans is weaker versus national competitors, while vendor and compliance expenses represent a larger share of noninterest costs, weighing on margins.

Interest rate sensitivity and margin pressure

Community banks like Orrstown face asset-liability gaps that make NIM vulnerable to rapid rate swings; the recent high-rate environment (federal funds near 5.25–5.50% in 2023–24) compressed spreads and slowed loan demand. Repricing lags on deposits versus loans have squeezed earnings as deposit betas rose faster than loan yields. Limited scale raises hedging costs and reduces available ALM tools.

Constrained brand awareness beyond core markets

Constrained brand awareness beyond core markets limits Orrstown Bank’s ability to penetrate adjacent counties and neighboring states, forcing heavier reliance on legacy branches and referrals. Acquiring customers outside its footprint drives up marketing and onboarding costs and leaves Orrstown vulnerable when competing directly with larger, better-known regional banks. This dampens growth in wealth management and specialty lending initiatives.

- Limited marketing reach

- Higher customer acquisition costs

- Direct competition with stronger regional brands

- Slower expansion of wealth and specialty lending

Concentration in CRE and mortgages typical of peers

Concentration in commercial real estate and 1-4 family mortgages mirrors peer community banks and raises sensitivity to sector-specific stress; FDIC 2024 industry data showed CRE and residential mortgage exposure remained a leading share of community bank portfolios. Elevated CRE/mortgage mix can amplify credit losses in downturns and invite closer regulatory scrutiny that limits growth in higher-risk lending buckets. A tilted portfolio mix reduces strategic flexibility during market weakness.

- Higher CRE/1-4 exposure — amplifies cyclical loss risk

- Regulatory caps/scrutiny — can constrain higher-yield growth

- Concentrated mix — limits liquidity and repricing options in downturns

South-central PA/MD focus and $2.6B scale raise CRE exposure and margin pressure

Operations concentrated in south-central PA and MD with ~2.6B assets (mid-2024) exposes Orrstown to regional downturns and sector cyclicality.

Modest scale limits tech/product investment, keeps efficiency ratio above large peers and raises unit costs, compressing NIM and ROA.

High CRE/1–4 mortgage exposure (FDIC 2024—leading share for community banks) and limited brand reach constrain growth and amplify credit risk.

| Metric | Value/Note |

|---|---|

| Assets (mid-2024) | $2.6B |

| Fed funds (2023–24) | ~5.25–5.50% |

| CRE/1–4 exposure | Leading share for community banks (FDIC 2024) |

Same Document Delivered

Orrstown Bank SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. You’re viewing a live preview of the real file—buy now to download the full, detailed Orrstown Bank SWOT.