Oshkosh Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

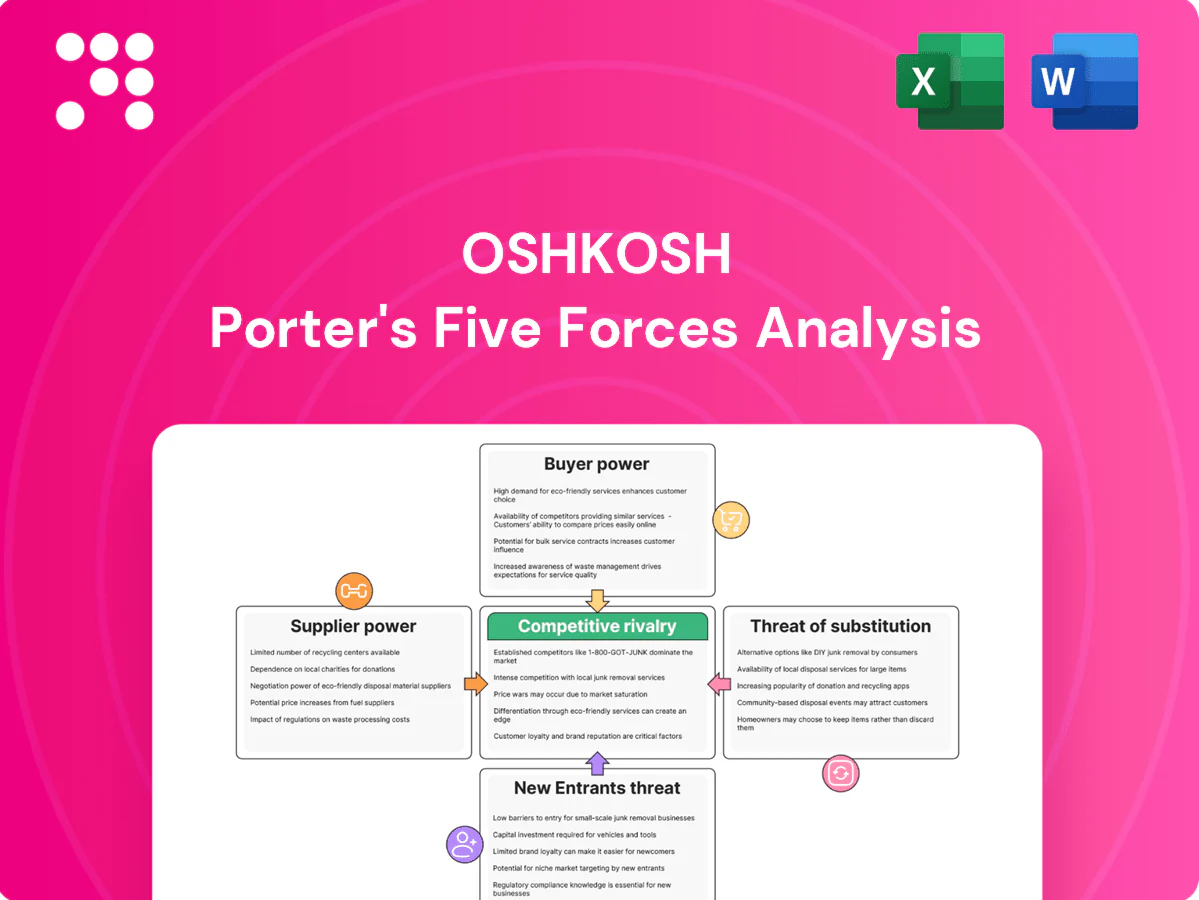

Oshkosh faces strong buyer scrutiny, concentrated suppliers, and moderate substitute threats, while scale and regulatory hurdles limit new entrants. Intense rivalry across defense and commercial segments pressures margins and innovation. This preview is just the beginning. Unlock the full Porter's Five Forces Analysis to explore Oshkosh’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical components

Engines and transmissions often come from Tier-1 suppliers like Cummins and Allison, while control electronics, hydraulics and specialty steels are concentrated among a few qualified vendors, giving suppliers pricing and allocation leverage. Military-grade specifications further narrow sources and single-source parts raise costly validation and compliance frictions. Oshkosh reduces risk by dual-qualifying suppliers where feasible and securing long-term agreements and strategic partnerships.

Specs-driven switching costs

Specs-driven switching costs for Oshkosh are high: defense and emergency platforms often require 6–18 months of requalification and certification, driving supplier leverage on unique parts. Design changes cascade into software, safety and performance validation, raising integration costs that can reach hundreds of thousands to millions per program. Commoditized components remain more contestable, reducing supplier power where standards prevail.

Commodity price volatility

Steel, aluminum and energy price swings fed through to Oshkosh's BOM in 2024, with spot hot-rolled coil and aluminum premiums reportedly up around mid-teens year-over-year, squeezing margins. Index-linked supply contracts and hedges provided partial protection but did not fully offset price spikes. Suppliers frequently implemented surcharges faster than Oshkosh could reprice products. Extended lead-times and logistics disruptions amplified cost volatility and working capital strain.

Capacity and logistics constraints

Tight capacity in castings, semiconductors and tires often lets suppliers prioritize larger OEMs or higher‑margin end markets, enabling allocation and tougher contract terms; global logistics disruptions continue to raise freight and expedite costs and squeeze lead times. Oshkosh can mitigate via nearshoring and inventory buffers, but those approaches tie up working capital and reduce flexibility.

- Allocation power: suppliers favor large OEMs

- Logistics: higher freight/expedite costs

- Mitigation: nearshoring/inventory = capital tied

Technology and IP dependence

EV drivetrains, battery packs, advanced telematics and ADAS modules are concentrated among a few suppliers (CATL held about 34% of global battery cell market in 2023), giving those vendors outsized leverage over OEMs like Oshkosh. Firmware, diagnostic tools and data rights create ecosystem lock‑in; co‑development improves vehicle performance but embeds path dependence. Royalty rates and software license terms therefore become primary bargaining levers.

- Concentration: CATL ~34% (2023)

- Lock‑in: firmware, diagnostics, data rights

- Co‑dev risk: path dependence

- Levers: royalties, software licenses

Supplier squeeze tightens margins: +15% metals, ~20-week chips, 6–18 month requalification

Suppliers hold moderate-to-high power: concentrated vendors for engines, batteries and ADAS plus specialty parts increase pricing and allocation leverage. 2024 commodity inflation (hot-rolled coil up ~15% YoY) and semiconductor lead times (~20 weeks) squeezed margins and raised working capital. High requalification costs (6–18 months) and software lock-in sustain supplier bargaining strength.

| Metric | 2024 value | Impact |

|---|---|---|

| HRC/Aluminum | +~15% YoY | Higher BOM, margin pressure |

| Semiconductor lead time | ~20 weeks | Allocation risk |

| Requalification | 6–18 months | High switching cost |

What is included in the product

Porter’s Five Forces analysis for Oshkosh uncovers the competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and industry rivalry shaping its pricing, margins and strategic defenses.

A concise, one-sheet Porter’s Five Forces for Oshkosh that visualizes competitive pressure and pinpoints strategic levers to relieve supplier, buyer, and rivalry pain points for faster, board-ready decisions.

Customers Bargaining Power

Large fleet buyers and rental houses

Large fleet buyers and rental houses exert strong price pressure on Oshkosh as concentrated, volume-driven customers; Oshkosh reported roughly $8.9 billion in net sales in 2024, highlighting dependence on big orders. Their ability to switch brands boosts negotiating leverage and forces aggressive service and uptime commitments. Framework agreements during downturns have compressed OEM margins by several percentage points, shifting bargaining power to fleets.

Government and defense procurement

DoD and allied agencies use competitive tenders with detailed specs and auditability, exerting tight price discipline—FY2024 US defense budget was $858 billion, reinforcing buyer leverage. Even incumbents face recompetes that cap pricing latitude, while budget cycles and appropriations create timing risk for Oshkosh deliveries and cash flow. Performance history and industrial-base importance partially offset buyer leverage, giving Oshkosh limited negotiation room.

Municipalities and public safety

Municipal fire and emergency buyers in 2024 prioritize reliability and lifecycle support but face tight capital budgets, increasing sensitivity to total cost of ownership. Cooperative purchasing and standardized RFPs streamline comparisons and amplify price pressure. Custom vehicle and equipment configurations limit direct comparability, softening buyer leverage. Long-standing supplier relationships and regional service networks often sway awards beyond lowest bid.

Cyclical demand sensitivity

Construction and refuse end-markets fluctuate with macro cycles, shifting bargaining power toward buyers in downturns as fleets delay replacements or extend maintenance to extract concessions. In upcycles, OEM backlogs and longer lead times reduce buyer leverage, restoring pricing power. Pricing power for Oshkosh therefore varies materially with cycle positioning.

- Buyers delay capex to press discounts

- Maintenance extensions boost aftermarket negotiating leverage

- Backlogs in upcycles shorten buyer power

Aftermarket and service expectations

High uptime demands—commonly exceeding 95% for mission-critical fleets—give buyers leverage over parts pricing, warranty terms, and SLA response times; third-party service options exist but remain uneven for Oshkosh's specialized platforms. Connected diagnostics in 2024 increased visibility into failure causes, pressuring OEM parts margins and enabling service-competition. Bundled service contracts trade lower upfront parts prices for customer stickiness and recurring revenue.

- Uptime >95%: stronger buyer leverage

- Third-party services: uneven for specialized fleets

- Connected diagnostics (2024): greater transparency, margin pressure

- Bundled contracts: price-for-stickiness trade-off

Fleet buyers and DoD tenders squeeze pricing; >95% uptime raises parts, warranty & service leverage

Concentrated fleet buyers (Oshkosh net sales ~$8.9B in 2024) and DoD tenders (FY2024 defense budget $858B) exert strong price and SLA pressure, with uptime demands >95% increasing leverage on parts, warranties and service terms. Market cycles and backlogs swing bargaining power materially.

| Metric | 2024 |

|---|---|

| Oshkosh net sales | $8.9B |

| US defense budget (FY2024) | $858B |

| Typical uptime | >95% |

What You See Is What You Get

Oshkosh Porter's Five Forces Analysis

This preview shows the exact Oshkosh Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the final, professionally formatted analysis ready for download and use the moment you buy. You're viewing the complete deliverable and will get instant access to this same file upon payment.

A Must-Have Tool for Decision-Makers

Oshkosh faces strong buyer scrutiny, concentrated suppliers, and moderate substitute threats, while scale and regulatory hurdles limit new entrants. Intense rivalry across defense and commercial segments pressures margins and innovation. This preview is just the beginning. Unlock the full Porter's Five Forces Analysis to explore Oshkosh’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical components

Engines and transmissions often come from Tier-1 suppliers like Cummins and Allison, while control electronics, hydraulics and specialty steels are concentrated among a few qualified vendors, giving suppliers pricing and allocation leverage. Military-grade specifications further narrow sources and single-source parts raise costly validation and compliance frictions. Oshkosh reduces risk by dual-qualifying suppliers where feasible and securing long-term agreements and strategic partnerships.

Specs-driven switching costs

Specs-driven switching costs for Oshkosh are high: defense and emergency platforms often require 6–18 months of requalification and certification, driving supplier leverage on unique parts. Design changes cascade into software, safety and performance validation, raising integration costs that can reach hundreds of thousands to millions per program. Commoditized components remain more contestable, reducing supplier power where standards prevail.

Commodity price volatility

Steel, aluminum and energy price swings fed through to Oshkosh's BOM in 2024, with spot hot-rolled coil and aluminum premiums reportedly up around mid-teens year-over-year, squeezing margins. Index-linked supply contracts and hedges provided partial protection but did not fully offset price spikes. Suppliers frequently implemented surcharges faster than Oshkosh could reprice products. Extended lead-times and logistics disruptions amplified cost volatility and working capital strain.

Capacity and logistics constraints

Tight capacity in castings, semiconductors and tires often lets suppliers prioritize larger OEMs or higher‑margin end markets, enabling allocation and tougher contract terms; global logistics disruptions continue to raise freight and expedite costs and squeeze lead times. Oshkosh can mitigate via nearshoring and inventory buffers, but those approaches tie up working capital and reduce flexibility.

- Allocation power: suppliers favor large OEMs

- Logistics: higher freight/expedite costs

- Mitigation: nearshoring/inventory = capital tied

Technology and IP dependence

EV drivetrains, battery packs, advanced telematics and ADAS modules are concentrated among a few suppliers (CATL held about 34% of global battery cell market in 2023), giving those vendors outsized leverage over OEMs like Oshkosh. Firmware, diagnostic tools and data rights create ecosystem lock‑in; co‑development improves vehicle performance but embeds path dependence. Royalty rates and software license terms therefore become primary bargaining levers.

- Concentration: CATL ~34% (2023)

- Lock‑in: firmware, diagnostics, data rights

- Co‑dev risk: path dependence

- Levers: royalties, software licenses

Supplier squeeze tightens margins: +15% metals, ~20-week chips, 6–18 month requalification

Suppliers hold moderate-to-high power: concentrated vendors for engines, batteries and ADAS plus specialty parts increase pricing and allocation leverage. 2024 commodity inflation (hot-rolled coil up ~15% YoY) and semiconductor lead times (~20 weeks) squeezed margins and raised working capital. High requalification costs (6–18 months) and software lock-in sustain supplier bargaining strength.

| Metric | 2024 value | Impact |

|---|---|---|

| HRC/Aluminum | +~15% YoY | Higher BOM, margin pressure |

| Semiconductor lead time | ~20 weeks | Allocation risk |

| Requalification | 6–18 months | High switching cost |

What is included in the product

Porter’s Five Forces analysis for Oshkosh uncovers the competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and industry rivalry shaping its pricing, margins and strategic defenses.

A concise, one-sheet Porter’s Five Forces for Oshkosh that visualizes competitive pressure and pinpoints strategic levers to relieve supplier, buyer, and rivalry pain points for faster, board-ready decisions.

Customers Bargaining Power

Large fleet buyers and rental houses

Large fleet buyers and rental houses exert strong price pressure on Oshkosh as concentrated, volume-driven customers; Oshkosh reported roughly $8.9 billion in net sales in 2024, highlighting dependence on big orders. Their ability to switch brands boosts negotiating leverage and forces aggressive service and uptime commitments. Framework agreements during downturns have compressed OEM margins by several percentage points, shifting bargaining power to fleets.

Government and defense procurement

DoD and allied agencies use competitive tenders with detailed specs and auditability, exerting tight price discipline—FY2024 US defense budget was $858 billion, reinforcing buyer leverage. Even incumbents face recompetes that cap pricing latitude, while budget cycles and appropriations create timing risk for Oshkosh deliveries and cash flow. Performance history and industrial-base importance partially offset buyer leverage, giving Oshkosh limited negotiation room.

Municipalities and public safety

Municipal fire and emergency buyers in 2024 prioritize reliability and lifecycle support but face tight capital budgets, increasing sensitivity to total cost of ownership. Cooperative purchasing and standardized RFPs streamline comparisons and amplify price pressure. Custom vehicle and equipment configurations limit direct comparability, softening buyer leverage. Long-standing supplier relationships and regional service networks often sway awards beyond lowest bid.

Cyclical demand sensitivity

Construction and refuse end-markets fluctuate with macro cycles, shifting bargaining power toward buyers in downturns as fleets delay replacements or extend maintenance to extract concessions. In upcycles, OEM backlogs and longer lead times reduce buyer leverage, restoring pricing power. Pricing power for Oshkosh therefore varies materially with cycle positioning.

- Buyers delay capex to press discounts

- Maintenance extensions boost aftermarket negotiating leverage

- Backlogs in upcycles shorten buyer power

Aftermarket and service expectations

High uptime demands—commonly exceeding 95% for mission-critical fleets—give buyers leverage over parts pricing, warranty terms, and SLA response times; third-party service options exist but remain uneven for Oshkosh's specialized platforms. Connected diagnostics in 2024 increased visibility into failure causes, pressuring OEM parts margins and enabling service-competition. Bundled service contracts trade lower upfront parts prices for customer stickiness and recurring revenue.

- Uptime >95%: stronger buyer leverage

- Third-party services: uneven for specialized fleets

- Connected diagnostics (2024): greater transparency, margin pressure

- Bundled contracts: price-for-stickiness trade-off

Fleet buyers and DoD tenders squeeze pricing; >95% uptime raises parts, warranty & service leverage

Concentrated fleet buyers (Oshkosh net sales ~$8.9B in 2024) and DoD tenders (FY2024 defense budget $858B) exert strong price and SLA pressure, with uptime demands >95% increasing leverage on parts, warranties and service terms. Market cycles and backlogs swing bargaining power materially.

| Metric | 2024 |

|---|---|

| Oshkosh net sales | $8.9B |

| US defense budget (FY2024) | $858B |

| Typical uptime | >95% |

What You See Is What You Get

Oshkosh Porter's Five Forces Analysis

This preview shows the exact Oshkosh Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the final, professionally formatted analysis ready for download and use the moment you buy. You're viewing the complete deliverable and will get instant access to this same file upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Oshkosh faces strong buyer scrutiny, concentrated suppliers, and moderate substitute threats, while scale and regulatory hurdles limit new entrants. Intense rivalry across defense and commercial segments pressures margins and innovation. This preview is just the beginning. Unlock the full Porter's Five Forces Analysis to explore Oshkosh’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical components

Engines and transmissions often come from Tier-1 suppliers like Cummins and Allison, while control electronics, hydraulics and specialty steels are concentrated among a few qualified vendors, giving suppliers pricing and allocation leverage. Military-grade specifications further narrow sources and single-source parts raise costly validation and compliance frictions. Oshkosh reduces risk by dual-qualifying suppliers where feasible and securing long-term agreements and strategic partnerships.

Specs-driven switching costs

Specs-driven switching costs for Oshkosh are high: defense and emergency platforms often require 6–18 months of requalification and certification, driving supplier leverage on unique parts. Design changes cascade into software, safety and performance validation, raising integration costs that can reach hundreds of thousands to millions per program. Commoditized components remain more contestable, reducing supplier power where standards prevail.

Commodity price volatility

Steel, aluminum and energy price swings fed through to Oshkosh's BOM in 2024, with spot hot-rolled coil and aluminum premiums reportedly up around mid-teens year-over-year, squeezing margins. Index-linked supply contracts and hedges provided partial protection but did not fully offset price spikes. Suppliers frequently implemented surcharges faster than Oshkosh could reprice products. Extended lead-times and logistics disruptions amplified cost volatility and working capital strain.

Capacity and logistics constraints

Tight capacity in castings, semiconductors and tires often lets suppliers prioritize larger OEMs or higher‑margin end markets, enabling allocation and tougher contract terms; global logistics disruptions continue to raise freight and expedite costs and squeeze lead times. Oshkosh can mitigate via nearshoring and inventory buffers, but those approaches tie up working capital and reduce flexibility.

- Allocation power: suppliers favor large OEMs

- Logistics: higher freight/expedite costs

- Mitigation: nearshoring/inventory = capital tied

Technology and IP dependence

EV drivetrains, battery packs, advanced telematics and ADAS modules are concentrated among a few suppliers (CATL held about 34% of global battery cell market in 2023), giving those vendors outsized leverage over OEMs like Oshkosh. Firmware, diagnostic tools and data rights create ecosystem lock‑in; co‑development improves vehicle performance but embeds path dependence. Royalty rates and software license terms therefore become primary bargaining levers.

- Concentration: CATL ~34% (2023)

- Lock‑in: firmware, diagnostics, data rights

- Co‑dev risk: path dependence

- Levers: royalties, software licenses

Supplier squeeze tightens margins: +15% metals, ~20-week chips, 6–18 month requalification

Suppliers hold moderate-to-high power: concentrated vendors for engines, batteries and ADAS plus specialty parts increase pricing and allocation leverage. 2024 commodity inflation (hot-rolled coil up ~15% YoY) and semiconductor lead times (~20 weeks) squeezed margins and raised working capital. High requalification costs (6–18 months) and software lock-in sustain supplier bargaining strength.

| Metric | 2024 value | Impact |

|---|---|---|

| HRC/Aluminum | +~15% YoY | Higher BOM, margin pressure |

| Semiconductor lead time | ~20 weeks | Allocation risk |

| Requalification | 6–18 months | High switching cost |

What is included in the product

Porter’s Five Forces analysis for Oshkosh uncovers the competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and industry rivalry shaping its pricing, margins and strategic defenses.

A concise, one-sheet Porter’s Five Forces for Oshkosh that visualizes competitive pressure and pinpoints strategic levers to relieve supplier, buyer, and rivalry pain points for faster, board-ready decisions.

Customers Bargaining Power

Large fleet buyers and rental houses

Large fleet buyers and rental houses exert strong price pressure on Oshkosh as concentrated, volume-driven customers; Oshkosh reported roughly $8.9 billion in net sales in 2024, highlighting dependence on big orders. Their ability to switch brands boosts negotiating leverage and forces aggressive service and uptime commitments. Framework agreements during downturns have compressed OEM margins by several percentage points, shifting bargaining power to fleets.

Government and defense procurement

DoD and allied agencies use competitive tenders with detailed specs and auditability, exerting tight price discipline—FY2024 US defense budget was $858 billion, reinforcing buyer leverage. Even incumbents face recompetes that cap pricing latitude, while budget cycles and appropriations create timing risk for Oshkosh deliveries and cash flow. Performance history and industrial-base importance partially offset buyer leverage, giving Oshkosh limited negotiation room.

Municipalities and public safety

Municipal fire and emergency buyers in 2024 prioritize reliability and lifecycle support but face tight capital budgets, increasing sensitivity to total cost of ownership. Cooperative purchasing and standardized RFPs streamline comparisons and amplify price pressure. Custom vehicle and equipment configurations limit direct comparability, softening buyer leverage. Long-standing supplier relationships and regional service networks often sway awards beyond lowest bid.

Cyclical demand sensitivity

Construction and refuse end-markets fluctuate with macro cycles, shifting bargaining power toward buyers in downturns as fleets delay replacements or extend maintenance to extract concessions. In upcycles, OEM backlogs and longer lead times reduce buyer leverage, restoring pricing power. Pricing power for Oshkosh therefore varies materially with cycle positioning.

- Buyers delay capex to press discounts

- Maintenance extensions boost aftermarket negotiating leverage

- Backlogs in upcycles shorten buyer power

Aftermarket and service expectations

High uptime demands—commonly exceeding 95% for mission-critical fleets—give buyers leverage over parts pricing, warranty terms, and SLA response times; third-party service options exist but remain uneven for Oshkosh's specialized platforms. Connected diagnostics in 2024 increased visibility into failure causes, pressuring OEM parts margins and enabling service-competition. Bundled service contracts trade lower upfront parts prices for customer stickiness and recurring revenue.

- Uptime >95%: stronger buyer leverage

- Third-party services: uneven for specialized fleets

- Connected diagnostics (2024): greater transparency, margin pressure

- Bundled contracts: price-for-stickiness trade-off

Fleet buyers and DoD tenders squeeze pricing; >95% uptime raises parts, warranty & service leverage

Concentrated fleet buyers (Oshkosh net sales ~$8.9B in 2024) and DoD tenders (FY2024 defense budget $858B) exert strong price and SLA pressure, with uptime demands >95% increasing leverage on parts, warranties and service terms. Market cycles and backlogs swing bargaining power materially.

| Metric | 2024 |

|---|---|

| Oshkosh net sales | $8.9B |

| US defense budget (FY2024) | $858B |

| Typical uptime | >95% |

What You See Is What You Get

Oshkosh Porter's Five Forces Analysis

This preview shows the exact Oshkosh Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the final, professionally formatted analysis ready for download and use the moment you buy. You're viewing the complete deliverable and will get instant access to this same file upon payment.