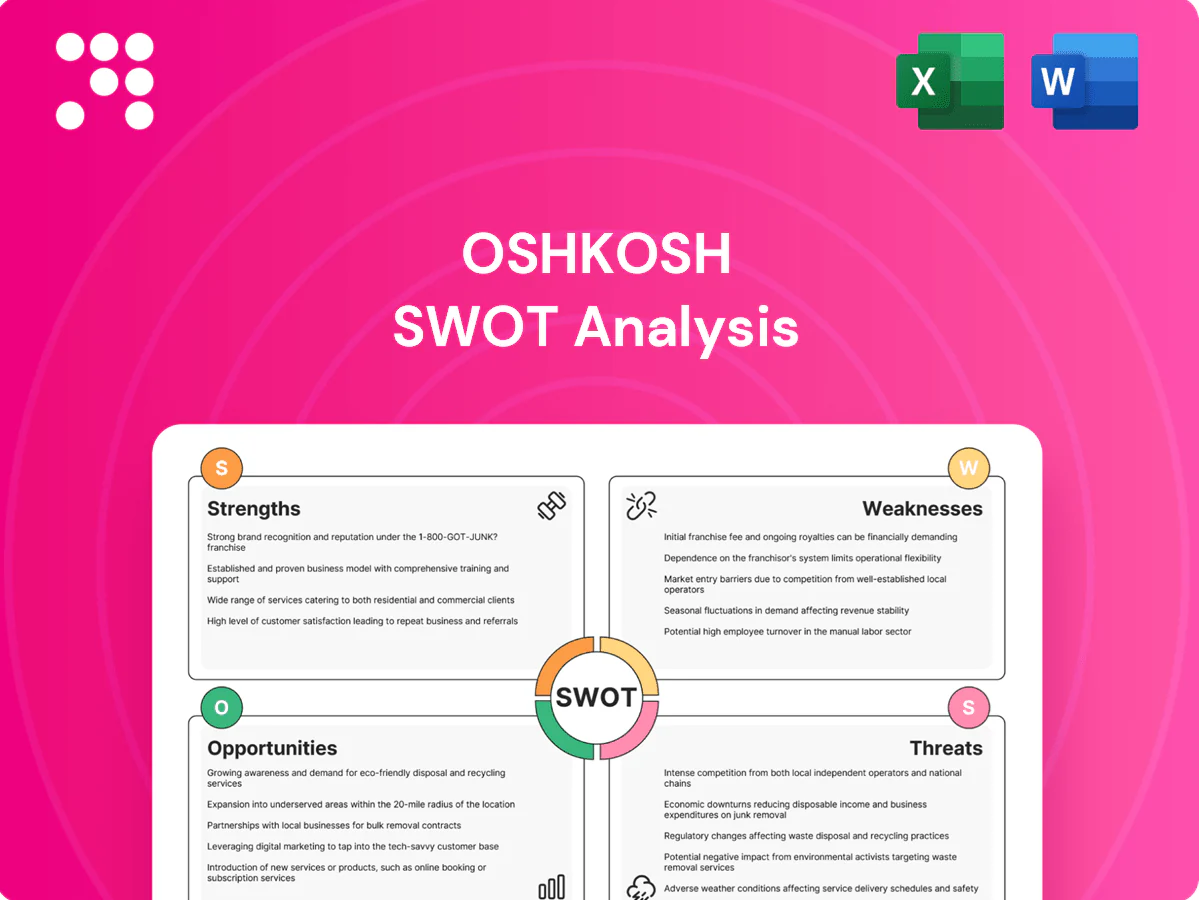

Oshkosh SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Oshkosh's diversified defense and commercial portfolio delivers durable revenue streams, but supply-chain exposure and cyclical end markets pose risks. Our concise SWOT highlights competitive moat, margin drivers, and strategic gaps. Want deeper analysis and actionable plans? Purchase the full SWOT for a downloadable Word and Excel package.

Strengths

Diversified segment portfolio

Oshkosh operates across Access Equipment, Defense, Vocational, and Fire & Emergency, reducing single-market dependency and smoothing revenue through construction and defense cycles. Cross-segment engineering, supply-chain, and manufacturing synergies cut costs and speed product development. The diversified mix broadens customer relationships across public and private sectors, enhancing resilience and repeat business.

Strong brands and market positions

Brands like JLG, Pierce and McNeilus anchor Oshkosh’s leading positions across access equipment, fire apparatus and refuse, supporting pricing power and repeat contracts; Oshkosh reported FY2024 revenue of $11.1 billion, leveraging a global dealer network of roughly 1,500 points and strong aftermarket pull‑through that creates a durable moat versus smaller niche competitors.

Defense programs and government relationships

Oshkosh’s role as prime on long-term defense programs anchors recurring revenue and utilization, notably the JLTV program (estimated program value ~30 billion USD), giving multi-year production visibility. Proven vehicle survivability and field performance—deployed in thousands of units—raises switching barriers for buyers. These credentials boost bid credibility and support lifecycle sustainment contract wins.

Advanced engineering and customization

Oshkosh designs purpose-built, mission-critical vehicles with specialized features and proprietary technologies in mobility, safety, electrification and controls, enabling fit-for-mission solutions. Deep customization aligns closely with unique customer use cases, supporting premium pricing and higher value-add margins; Oshkosh reported roughly $9.3 billion revenue in FY2024, reflecting strong demand for differentiated offerings.

- Proprietary tech: mobility, safety, electrification, controls

- Customization: close fit to customer missions

- Premium positioning: supports higher margins

- Scale: ~$9.3B revenue FY2024

Global distribution and aftermarket

- Global footprint: dealer/service network across key markets

- Recurring high-margin revenue: parts, maintenance, refurbishment

- Faster delivery and local compliance

- Stronger customer retention over equipment lifecycle

Diversified defense & equipment platform with global dealers, proprietary tech, 11.1B USD

Oshkosh benefits from diversified segments (Access, Defense, Vocational, Fire) and a global dealer network (~1,500 locations), lowering market risk and boosting aftermarket revenue. Strong brands (JLG, Pierce, McNeilus) and prime-defense roles (JLTV program ~30 billion USD) provide multi-year visibility and pricing power. Proprietary mobility, safety and electrification tech enable premium margins and repeat contracts; FY2024 revenue: 11.1B USD.

| Metric | Value |

|---|---|

| FY2024 revenue | 11.1B USD |

| Dealer/service points | ~1,500 |

| JLTV program value | ~30B USD |

| Key brands | JLG, Pierce, McNeilus |

What is included in the product

Delivers a strategic overview of Oshkosh’s internal and external business factors, outlining the strengths, weaknesses, opportunities, and threats that shape its competitive position and future growth.

Condenses Oshkosh's strengths, weaknesses, opportunities, and threats into a clean, editable matrix for quick strategic alignment, executive briefings, and fast integration into reports and slides.

Weaknesses

Exposure to cyclical end markets

Access equipment and vocational demand for Oshkosh is tied to construction, municipal budgets and industrial activity, making revenue sensitive to economic cycles; fiscal 2024 net sales were about $8.5 billion. Downturns can rapidly compress orders and margins, and while Oshkosh reported a multi-billion-dollar backlog (roughly $8.7 billion at Sept 30, 2024) it cannot fully offset sharp swings. Resulting earnings volatility can weigh on valuation multiples.

High dependence on key programs

High dependence on key programs is evident as Oshkosh remains prime contractor on large platforms like the JLTV and Family of Heavy Tactical Vehicles, with program awards noted through 2024. Program delays, rebids, or cancellations can materially dent results and create utilization gaps during transition between platforms. Heavy U.S. DoD customer concentration increases negotiating-leverage risk and revenue volatility.

Supply chain and component sensitivity

Reliance on critical components like hydraulics, semiconductors and steel creates bottleneck risk for Oshkosh; supply disruptions in 2024 contributed to margin pressure after FY2024 net sales of about $11.2 billion. Disruptions inflate costs and extend lead times, while passing increases through to customers lags and compresses margins. Inventory balancing across heavy, defense and specialty lines remains complex and costly.

Capital intensity and working capital needs

Building specialty vehicles requires heavy capex and tooling, and Oshkosh’s long build cycles tie up inventory and receivables, evident in 2024 operational commentary about program backlogs and delivery schedules. These dynamics can compress free cash flow in downturns and raise break-even utilization thresholds for manufacturing lines.

- High capex and tooling

- Long build cycles → tied inventory/receivables

- Constrains FCF in downcycles

- Higher break-even utilization

Electrification and software gaps vs disruptors

Cyclical equipment demand and DoD concentration drive volatile earnings despite large backlog

Oshkosh revenues and equipment demand are cyclical (FY2024 net sales cited at about $11.2B), with order sensitivity that fuels earnings volatility; backlog (~$8.7B at Sept 30, 2024) cushions but does not eliminate swings. Heavy DoD program concentration and long build cycles raise utilization and cash-flow risk, while supply-chain and EV/telematics scaling create margin pressure and 12–36 month certification lags.

| Metric | Value |

|---|---|

| FY2024 net sales | $11.2B |

| Access-equipment FY2024 | $8.5B |

| Backlog (Sep 30, 2024) | $8.7B |

| Certification delay | 12–36 months |

Preview the Actual Deliverable

Oshkosh SWOT Analysis

This is the actual Oshkosh SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get. Buy now to unlock the complete, editable version.

Make Insightful Decisions Backed by Expert Research

Oshkosh's diversified defense and commercial portfolio delivers durable revenue streams, but supply-chain exposure and cyclical end markets pose risks. Our concise SWOT highlights competitive moat, margin drivers, and strategic gaps. Want deeper analysis and actionable plans? Purchase the full SWOT for a downloadable Word and Excel package.

Strengths

Diversified segment portfolio

Oshkosh operates across Access Equipment, Defense, Vocational, and Fire & Emergency, reducing single-market dependency and smoothing revenue through construction and defense cycles. Cross-segment engineering, supply-chain, and manufacturing synergies cut costs and speed product development. The diversified mix broadens customer relationships across public and private sectors, enhancing resilience and repeat business.

Strong brands and market positions

Brands like JLG, Pierce and McNeilus anchor Oshkosh’s leading positions across access equipment, fire apparatus and refuse, supporting pricing power and repeat contracts; Oshkosh reported FY2024 revenue of $11.1 billion, leveraging a global dealer network of roughly 1,500 points and strong aftermarket pull‑through that creates a durable moat versus smaller niche competitors.

Defense programs and government relationships

Oshkosh’s role as prime on long-term defense programs anchors recurring revenue and utilization, notably the JLTV program (estimated program value ~30 billion USD), giving multi-year production visibility. Proven vehicle survivability and field performance—deployed in thousands of units—raises switching barriers for buyers. These credentials boost bid credibility and support lifecycle sustainment contract wins.

Advanced engineering and customization

Oshkosh designs purpose-built, mission-critical vehicles with specialized features and proprietary technologies in mobility, safety, electrification and controls, enabling fit-for-mission solutions. Deep customization aligns closely with unique customer use cases, supporting premium pricing and higher value-add margins; Oshkosh reported roughly $9.3 billion revenue in FY2024, reflecting strong demand for differentiated offerings.

- Proprietary tech: mobility, safety, electrification, controls

- Customization: close fit to customer missions

- Premium positioning: supports higher margins

- Scale: ~$9.3B revenue FY2024

Global distribution and aftermarket

- Global footprint: dealer/service network across key markets

- Recurring high-margin revenue: parts, maintenance, refurbishment

- Faster delivery and local compliance

- Stronger customer retention over equipment lifecycle

Diversified defense & equipment platform with global dealers, proprietary tech, 11.1B USD

Oshkosh benefits from diversified segments (Access, Defense, Vocational, Fire) and a global dealer network (~1,500 locations), lowering market risk and boosting aftermarket revenue. Strong brands (JLG, Pierce, McNeilus) and prime-defense roles (JLTV program ~30 billion USD) provide multi-year visibility and pricing power. Proprietary mobility, safety and electrification tech enable premium margins and repeat contracts; FY2024 revenue: 11.1B USD.

| Metric | Value |

|---|---|

| FY2024 revenue | 11.1B USD |

| Dealer/service points | ~1,500 |

| JLTV program value | ~30B USD |

| Key brands | JLG, Pierce, McNeilus |

What is included in the product

Delivers a strategic overview of Oshkosh’s internal and external business factors, outlining the strengths, weaknesses, opportunities, and threats that shape its competitive position and future growth.

Condenses Oshkosh's strengths, weaknesses, opportunities, and threats into a clean, editable matrix for quick strategic alignment, executive briefings, and fast integration into reports and slides.

Weaknesses

Exposure to cyclical end markets

Access equipment and vocational demand for Oshkosh is tied to construction, municipal budgets and industrial activity, making revenue sensitive to economic cycles; fiscal 2024 net sales were about $8.5 billion. Downturns can rapidly compress orders and margins, and while Oshkosh reported a multi-billion-dollar backlog (roughly $8.7 billion at Sept 30, 2024) it cannot fully offset sharp swings. Resulting earnings volatility can weigh on valuation multiples.

High dependence on key programs

High dependence on key programs is evident as Oshkosh remains prime contractor on large platforms like the JLTV and Family of Heavy Tactical Vehicles, with program awards noted through 2024. Program delays, rebids, or cancellations can materially dent results and create utilization gaps during transition between platforms. Heavy U.S. DoD customer concentration increases negotiating-leverage risk and revenue volatility.

Supply chain and component sensitivity

Reliance on critical components like hydraulics, semiconductors and steel creates bottleneck risk for Oshkosh; supply disruptions in 2024 contributed to margin pressure after FY2024 net sales of about $11.2 billion. Disruptions inflate costs and extend lead times, while passing increases through to customers lags and compresses margins. Inventory balancing across heavy, defense and specialty lines remains complex and costly.

Capital intensity and working capital needs

Building specialty vehicles requires heavy capex and tooling, and Oshkosh’s long build cycles tie up inventory and receivables, evident in 2024 operational commentary about program backlogs and delivery schedules. These dynamics can compress free cash flow in downturns and raise break-even utilization thresholds for manufacturing lines.

- High capex and tooling

- Long build cycles → tied inventory/receivables

- Constrains FCF in downcycles

- Higher break-even utilization

Electrification and software gaps vs disruptors

Cyclical equipment demand and DoD concentration drive volatile earnings despite large backlog

Oshkosh revenues and equipment demand are cyclical (FY2024 net sales cited at about $11.2B), with order sensitivity that fuels earnings volatility; backlog (~$8.7B at Sept 30, 2024) cushions but does not eliminate swings. Heavy DoD program concentration and long build cycles raise utilization and cash-flow risk, while supply-chain and EV/telematics scaling create margin pressure and 12–36 month certification lags.

| Metric | Value |

|---|---|

| FY2024 net sales | $11.2B |

| Access-equipment FY2024 | $8.5B |

| Backlog (Sep 30, 2024) | $8.7B |

| Certification delay | 12–36 months |

Preview the Actual Deliverable

Oshkosh SWOT Analysis

This is the actual Oshkosh SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get. Buy now to unlock the complete, editable version.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Oshkosh's diversified defense and commercial portfolio delivers durable revenue streams, but supply-chain exposure and cyclical end markets pose risks. Our concise SWOT highlights competitive moat, margin drivers, and strategic gaps. Want deeper analysis and actionable plans? Purchase the full SWOT for a downloadable Word and Excel package.

Strengths

Diversified segment portfolio

Oshkosh operates across Access Equipment, Defense, Vocational, and Fire & Emergency, reducing single-market dependency and smoothing revenue through construction and defense cycles. Cross-segment engineering, supply-chain, and manufacturing synergies cut costs and speed product development. The diversified mix broadens customer relationships across public and private sectors, enhancing resilience and repeat business.

Strong brands and market positions

Brands like JLG, Pierce and McNeilus anchor Oshkosh’s leading positions across access equipment, fire apparatus and refuse, supporting pricing power and repeat contracts; Oshkosh reported FY2024 revenue of $11.1 billion, leveraging a global dealer network of roughly 1,500 points and strong aftermarket pull‑through that creates a durable moat versus smaller niche competitors.

Defense programs and government relationships

Oshkosh’s role as prime on long-term defense programs anchors recurring revenue and utilization, notably the JLTV program (estimated program value ~30 billion USD), giving multi-year production visibility. Proven vehicle survivability and field performance—deployed in thousands of units—raises switching barriers for buyers. These credentials boost bid credibility and support lifecycle sustainment contract wins.

Advanced engineering and customization

Oshkosh designs purpose-built, mission-critical vehicles with specialized features and proprietary technologies in mobility, safety, electrification and controls, enabling fit-for-mission solutions. Deep customization aligns closely with unique customer use cases, supporting premium pricing and higher value-add margins; Oshkosh reported roughly $9.3 billion revenue in FY2024, reflecting strong demand for differentiated offerings.

- Proprietary tech: mobility, safety, electrification, controls

- Customization: close fit to customer missions

- Premium positioning: supports higher margins

- Scale: ~$9.3B revenue FY2024

Global distribution and aftermarket

- Global footprint: dealer/service network across key markets

- Recurring high-margin revenue: parts, maintenance, refurbishment

- Faster delivery and local compliance

- Stronger customer retention over equipment lifecycle

Diversified defense & equipment platform with global dealers, proprietary tech, 11.1B USD

Oshkosh benefits from diversified segments (Access, Defense, Vocational, Fire) and a global dealer network (~1,500 locations), lowering market risk and boosting aftermarket revenue. Strong brands (JLG, Pierce, McNeilus) and prime-defense roles (JLTV program ~30 billion USD) provide multi-year visibility and pricing power. Proprietary mobility, safety and electrification tech enable premium margins and repeat contracts; FY2024 revenue: 11.1B USD.

| Metric | Value |

|---|---|

| FY2024 revenue | 11.1B USD |

| Dealer/service points | ~1,500 |

| JLTV program value | ~30B USD |

| Key brands | JLG, Pierce, McNeilus |

What is included in the product

Delivers a strategic overview of Oshkosh’s internal and external business factors, outlining the strengths, weaknesses, opportunities, and threats that shape its competitive position and future growth.

Condenses Oshkosh's strengths, weaknesses, opportunities, and threats into a clean, editable matrix for quick strategic alignment, executive briefings, and fast integration into reports and slides.

Weaknesses

Exposure to cyclical end markets

Access equipment and vocational demand for Oshkosh is tied to construction, municipal budgets and industrial activity, making revenue sensitive to economic cycles; fiscal 2024 net sales were about $8.5 billion. Downturns can rapidly compress orders and margins, and while Oshkosh reported a multi-billion-dollar backlog (roughly $8.7 billion at Sept 30, 2024) it cannot fully offset sharp swings. Resulting earnings volatility can weigh on valuation multiples.

High dependence on key programs

High dependence on key programs is evident as Oshkosh remains prime contractor on large platforms like the JLTV and Family of Heavy Tactical Vehicles, with program awards noted through 2024. Program delays, rebids, or cancellations can materially dent results and create utilization gaps during transition between platforms. Heavy U.S. DoD customer concentration increases negotiating-leverage risk and revenue volatility.

Supply chain and component sensitivity

Reliance on critical components like hydraulics, semiconductors and steel creates bottleneck risk for Oshkosh; supply disruptions in 2024 contributed to margin pressure after FY2024 net sales of about $11.2 billion. Disruptions inflate costs and extend lead times, while passing increases through to customers lags and compresses margins. Inventory balancing across heavy, defense and specialty lines remains complex and costly.

Capital intensity and working capital needs

Building specialty vehicles requires heavy capex and tooling, and Oshkosh’s long build cycles tie up inventory and receivables, evident in 2024 operational commentary about program backlogs and delivery schedules. These dynamics can compress free cash flow in downturns and raise break-even utilization thresholds for manufacturing lines.

- High capex and tooling

- Long build cycles → tied inventory/receivables

- Constrains FCF in downcycles

- Higher break-even utilization

Electrification and software gaps vs disruptors

Cyclical equipment demand and DoD concentration drive volatile earnings despite large backlog

Oshkosh revenues and equipment demand are cyclical (FY2024 net sales cited at about $11.2B), with order sensitivity that fuels earnings volatility; backlog (~$8.7B at Sept 30, 2024) cushions but does not eliminate swings. Heavy DoD program concentration and long build cycles raise utilization and cash-flow risk, while supply-chain and EV/telematics scaling create margin pressure and 12–36 month certification lags.

| Metric | Value |

|---|---|

| FY2024 net sales | $11.2B |

| Access-equipment FY2024 | $8.5B |

| Backlog (Sep 30, 2024) | $8.7B |

| Certification delay | 12–36 months |

Preview the Actual Deliverable

Oshkosh SWOT Analysis

This is the actual Oshkosh SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get. Buy now to unlock the complete, editable version.