OSI Systems Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

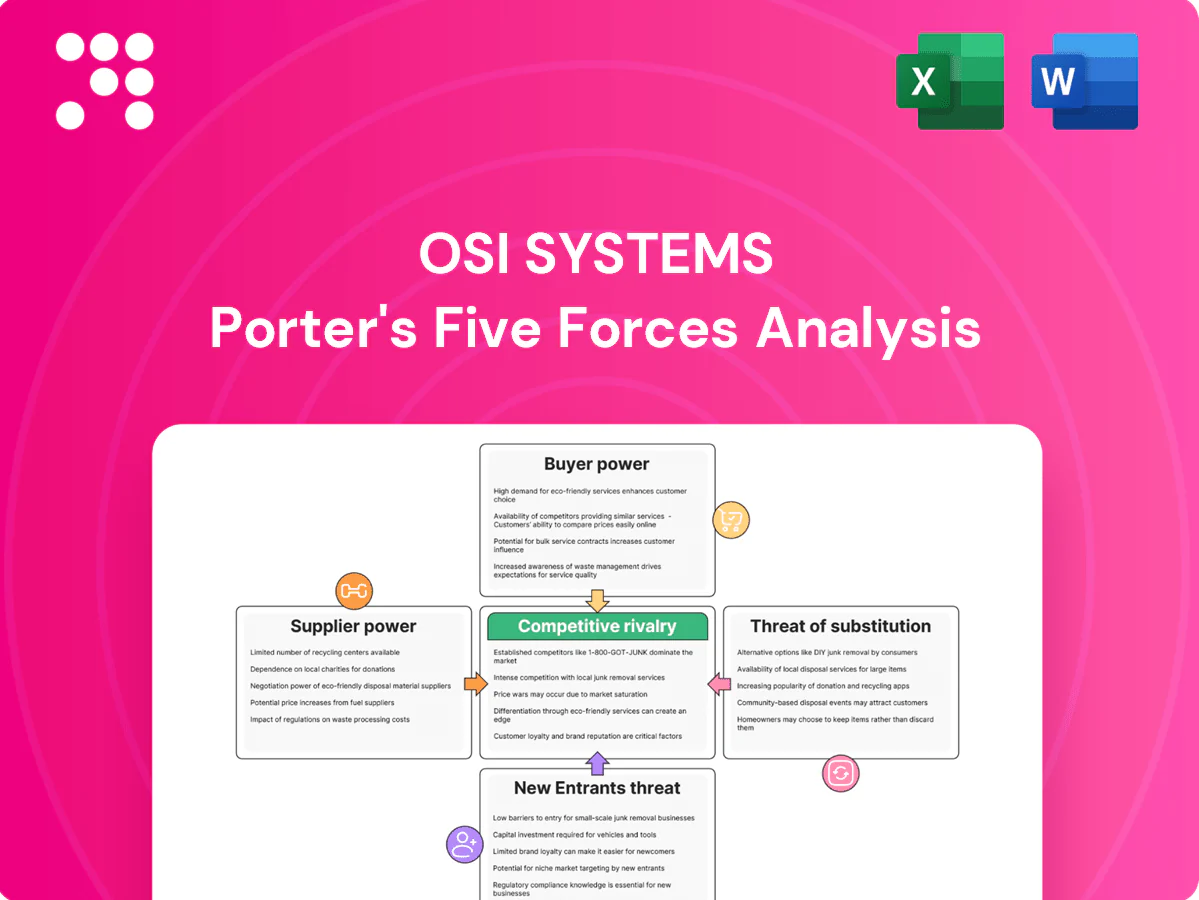

OSI Systems' Porter's Five Forces Analysis outlines competitive intensity across supplier power, buyer influence, substitution risk, threat of entrants, and intra-industry rivalry to clarify strategic pressure points. The snapshot highlights key vulnerabilities and strengths that shape margins and growth potential. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore OSI Systems’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized component concentration

OSI Systems depends on niche inputs like X-ray tubes, scintillators, high-reliability semiconductors and photodiodes, many sourced from only a handful of global vendors, increasing supplier leverage. Qualification and radiation/medical compliance extend switching timelines, often delaying replacements by 12+ weeks. This concentration raises price and lead-time risks, with procurement volatility frequently showing double-digit percentage swings and multi-month delivery slippage.

Vertical integration offsets

The Optoelectronics and Manufacturing division insources select sensors and assemblies, reducing dependence on external vendors and improving OSI Systems’ bargaining posture; in 2024 the division accounted for roughly 15% of company revenue (about $180 million of $1.2 billion). Internal capacity helps buffer shortages and mitigate price spikes seen across supply chains in 2023–24, but vertical integration does not cover all specialty components, leaving some supplier leverage intact.

Qualification and regulatory lock-in

Security and medical devices require validated parts under TSA, ECAC and FDA quality systems; requalifying a supplier commonly takes 3–9 months and audit efforts often exceed 100 man-hours, creating substantial switching costs that favor suppliers. Vendors leverage this certification burden to negotiate longer contracts, typically 3–5 years, stabilizing supplier margins and raising OSI Systems’ procurement risk.

Supply chain cyclicality and lead times

Semiconductor and precision-optics cycles have pushed lead times above 20 weeks during peak shortages, increasing allocation risk as suppliers prioritize larger-volume customers; OSI must therefore lock forecasts and deposits to secure capacity, shifting working-capital strain upstream and compressing liquidity.

- Lead times: >20 weeks

- Priority: large-volume customers favored

- OSI response: forecasts + deposits

- Impact: upstream working-capital pressure

Counter-levers: multisourcing and scale

- Global sourcing: diversifies geographic risk

- Dual-sourcing: reduces single-supplier dependency

- Framework agreements: stabilize costs and terms

- Aggregated demand: improves volume leverage across three divisions

- Design-for-supply: mitigates single-point failures

- Long-term partnerships: trade visibility for cost stability

Supplier power strains med-radiation OEM; opto insourcing 15% cushions risk

OSI Systems faces high supplier power due to niche radiation/medical components, single-source vendors, and requalification timelines of 3–9 months, causing price and lead-time volatility (double-digit swings). Optoelectronics insourcing (15% of 2024 revenue, ~$180m of $1.2b) cushions risk but gaps remain. Lead times often exceed 20 weeks; suppliers win 3–5 year contracts.

| Metric | 2024 |

|---|---|

| Revenue | $1.2B |

| Opto revenue | $180M (15%) |

| Lead times | >20 weeks |

| Requalify | 3–9 months |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to OSI Systems' security and healthcare electronics businesses. Evaluates supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive technologies and strategic levers to protect market share and profitability.

A clear, one-sheet Porter's Five Forces summary for OSI Systems—perfect for quick strategic decisions, investor pitches, and boardroom slides to instantly gauge competitive pressure and prioritize actions.

Customers Bargaining Power

Government and large institutional buyers

Government and large institutional buyers such as sovereign agencies, airports and ports concentrate spend and use tender-based procurement with strict technical specs, giving buyers strong pricing leverage. TSA screened over 800 million passengers in 2023, and budget cycles plus competitive bids often compress vendor margins. Post-sale service and maintenance contracts partially rebalance economics by stabilizing revenue streams.

Hospital and IDN consolidation

Healthcare buyers are largely hospital systems and GPOs, with roughly 70% of U.S. hospitals now system-affiliated and GPOs managing about 90% of hospital purchasing volume, increasing supplier price sensitivity through volume discounts and vendor standardization. Clinical outcomes and device interoperability remain decisive in award decisions, supporting premium pricing for proven performance. Service uptime SLAs (commonly targeting 99.9% availability) offer a clear differentiator beyond price.

Technical performance comparability

Competing systems meet similar regulatory baselines, so 2024 procurement reviews show buyers focus on TCO and performance; detection-rate differences of 2–8 percentage points and false-alarm rates typically cited at 0.5–4% drive decisions, letting buyers leverage vendors on lifecycle costs, upgrade paths and total cost of ownership.

Switching costs and integration

Installed bases tie OSI Systems into hospital IT, PACS and airport screening workflows; switching requires retraining, certification and days-to-weeks of downtime, which tempers buyer power. Planned refresh cycles, typically every 5–7 years, reopen competitive opportunities. Extended warranties and paid software upgrades further increase lock-in.

- Installed integration: IT, PACS, screening

- Switching cost: retraining + downtime

- Refresh cycle: 5–7 years

- Lock-in: warranties & software upgrades

Aftermarket and service negotiations

Aftermarket spare parts, consumables and maintenance create recurring revenue for OSI Systems, with FY2024 revenue reported at $1.09 billion supporting stable service income; buyers bundling service in tenders compress margins as procurement seeks total-cost caps. Performance-based contracts shift uptime and quality risk back to OSI, while multiyear agreements trade price concessions for customer retention and predictable lifecycle revenues.

- Spare parts & consumables: recurring margin

- Bundled tenders: cap buyer costs, pressure margins

- Performance contracts: vendor assumes operational risk

- Multiyear deals: lower price, higher retention

GPO-driven tenders raise price pressure; FY2024 service revenue $1.09B

Buyers hold strong leverage via tendered, spec-driven procurement; 2024 sourcing emphasizes TCO and detection performance. Healthcare GPOs account for ~90% of hospital purchasing and ~70% of hospitals are system-affiliated, raising price sensitivity. FY2024 aftermarket/service revenue was $1.09 billion, but bundled tenders and 5–7 year refresh cycles compress margins and reopen competition.

| Metric | Value |

|---|---|

| FY2024 service revenue | $1.09B |

| Hospital system affiliation | ~70% |

| GPO purchasing share | ~90% |

| Refresh cycle | 5–7 yrs |

Full Version Awaits

OSI Systems Porter's Five Forces Analysis

This preview shows the exact OSI Systems Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for immediate download and use the moment you buy. What you see here is the final deliverable, identical to the document provided upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

OSI Systems' Porter's Five Forces Analysis outlines competitive intensity across supplier power, buyer influence, substitution risk, threat of entrants, and intra-industry rivalry to clarify strategic pressure points. The snapshot highlights key vulnerabilities and strengths that shape margins and growth potential. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore OSI Systems’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized component concentration

OSI Systems depends on niche inputs like X-ray tubes, scintillators, high-reliability semiconductors and photodiodes, many sourced from only a handful of global vendors, increasing supplier leverage. Qualification and radiation/medical compliance extend switching timelines, often delaying replacements by 12+ weeks. This concentration raises price and lead-time risks, with procurement volatility frequently showing double-digit percentage swings and multi-month delivery slippage.

Vertical integration offsets

The Optoelectronics and Manufacturing division insources select sensors and assemblies, reducing dependence on external vendors and improving OSI Systems’ bargaining posture; in 2024 the division accounted for roughly 15% of company revenue (about $180 million of $1.2 billion). Internal capacity helps buffer shortages and mitigate price spikes seen across supply chains in 2023–24, but vertical integration does not cover all specialty components, leaving some supplier leverage intact.

Qualification and regulatory lock-in

Security and medical devices require validated parts under TSA, ECAC and FDA quality systems; requalifying a supplier commonly takes 3–9 months and audit efforts often exceed 100 man-hours, creating substantial switching costs that favor suppliers. Vendors leverage this certification burden to negotiate longer contracts, typically 3–5 years, stabilizing supplier margins and raising OSI Systems’ procurement risk.

Supply chain cyclicality and lead times

Semiconductor and precision-optics cycles have pushed lead times above 20 weeks during peak shortages, increasing allocation risk as suppliers prioritize larger-volume customers; OSI must therefore lock forecasts and deposits to secure capacity, shifting working-capital strain upstream and compressing liquidity.

- Lead times: >20 weeks

- Priority: large-volume customers favored

- OSI response: forecasts + deposits

- Impact: upstream working-capital pressure

Counter-levers: multisourcing and scale

- Global sourcing: diversifies geographic risk

- Dual-sourcing: reduces single-supplier dependency

- Framework agreements: stabilize costs and terms

- Aggregated demand: improves volume leverage across three divisions

- Design-for-supply: mitigates single-point failures

- Long-term partnerships: trade visibility for cost stability

Supplier power strains med-radiation OEM; opto insourcing 15% cushions risk

OSI Systems faces high supplier power due to niche radiation/medical components, single-source vendors, and requalification timelines of 3–9 months, causing price and lead-time volatility (double-digit swings). Optoelectronics insourcing (15% of 2024 revenue, ~$180m of $1.2b) cushions risk but gaps remain. Lead times often exceed 20 weeks; suppliers win 3–5 year contracts.

| Metric | 2024 |

|---|---|

| Revenue | $1.2B |

| Opto revenue | $180M (15%) |

| Lead times | >20 weeks |

| Requalify | 3–9 months |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to OSI Systems' security and healthcare electronics businesses. Evaluates supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive technologies and strategic levers to protect market share and profitability.

A clear, one-sheet Porter's Five Forces summary for OSI Systems—perfect for quick strategic decisions, investor pitches, and boardroom slides to instantly gauge competitive pressure and prioritize actions.

Customers Bargaining Power

Government and large institutional buyers

Government and large institutional buyers such as sovereign agencies, airports and ports concentrate spend and use tender-based procurement with strict technical specs, giving buyers strong pricing leverage. TSA screened over 800 million passengers in 2023, and budget cycles plus competitive bids often compress vendor margins. Post-sale service and maintenance contracts partially rebalance economics by stabilizing revenue streams.

Hospital and IDN consolidation

Healthcare buyers are largely hospital systems and GPOs, with roughly 70% of U.S. hospitals now system-affiliated and GPOs managing about 90% of hospital purchasing volume, increasing supplier price sensitivity through volume discounts and vendor standardization. Clinical outcomes and device interoperability remain decisive in award decisions, supporting premium pricing for proven performance. Service uptime SLAs (commonly targeting 99.9% availability) offer a clear differentiator beyond price.

Technical performance comparability

Competing systems meet similar regulatory baselines, so 2024 procurement reviews show buyers focus on TCO and performance; detection-rate differences of 2–8 percentage points and false-alarm rates typically cited at 0.5–4% drive decisions, letting buyers leverage vendors on lifecycle costs, upgrade paths and total cost of ownership.

Switching costs and integration

Installed bases tie OSI Systems into hospital IT, PACS and airport screening workflows; switching requires retraining, certification and days-to-weeks of downtime, which tempers buyer power. Planned refresh cycles, typically every 5–7 years, reopen competitive opportunities. Extended warranties and paid software upgrades further increase lock-in.

- Installed integration: IT, PACS, screening

- Switching cost: retraining + downtime

- Refresh cycle: 5–7 years

- Lock-in: warranties & software upgrades

Aftermarket and service negotiations

Aftermarket spare parts, consumables and maintenance create recurring revenue for OSI Systems, with FY2024 revenue reported at $1.09 billion supporting stable service income; buyers bundling service in tenders compress margins as procurement seeks total-cost caps. Performance-based contracts shift uptime and quality risk back to OSI, while multiyear agreements trade price concessions for customer retention and predictable lifecycle revenues.

- Spare parts & consumables: recurring margin

- Bundled tenders: cap buyer costs, pressure margins

- Performance contracts: vendor assumes operational risk

- Multiyear deals: lower price, higher retention

GPO-driven tenders raise price pressure; FY2024 service revenue $1.09B

Buyers hold strong leverage via tendered, spec-driven procurement; 2024 sourcing emphasizes TCO and detection performance. Healthcare GPOs account for ~90% of hospital purchasing and ~70% of hospitals are system-affiliated, raising price sensitivity. FY2024 aftermarket/service revenue was $1.09 billion, but bundled tenders and 5–7 year refresh cycles compress margins and reopen competition.

| Metric | Value |

|---|---|

| FY2024 service revenue | $1.09B |

| Hospital system affiliation | ~70% |

| GPO purchasing share | ~90% |

| Refresh cycle | 5–7 yrs |

Full Version Awaits

OSI Systems Porter's Five Forces Analysis

This preview shows the exact OSI Systems Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for immediate download and use the moment you buy. What you see here is the final deliverable, identical to the document provided upon payment.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

OSI Systems' Porter's Five Forces Analysis outlines competitive intensity across supplier power, buyer influence, substitution risk, threat of entrants, and intra-industry rivalry to clarify strategic pressure points. The snapshot highlights key vulnerabilities and strengths that shape margins and growth potential. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore OSI Systems’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized component concentration

OSI Systems depends on niche inputs like X-ray tubes, scintillators, high-reliability semiconductors and photodiodes, many sourced from only a handful of global vendors, increasing supplier leverage. Qualification and radiation/medical compliance extend switching timelines, often delaying replacements by 12+ weeks. This concentration raises price and lead-time risks, with procurement volatility frequently showing double-digit percentage swings and multi-month delivery slippage.

Vertical integration offsets

The Optoelectronics and Manufacturing division insources select sensors and assemblies, reducing dependence on external vendors and improving OSI Systems’ bargaining posture; in 2024 the division accounted for roughly 15% of company revenue (about $180 million of $1.2 billion). Internal capacity helps buffer shortages and mitigate price spikes seen across supply chains in 2023–24, but vertical integration does not cover all specialty components, leaving some supplier leverage intact.

Qualification and regulatory lock-in

Security and medical devices require validated parts under TSA, ECAC and FDA quality systems; requalifying a supplier commonly takes 3–9 months and audit efforts often exceed 100 man-hours, creating substantial switching costs that favor suppliers. Vendors leverage this certification burden to negotiate longer contracts, typically 3–5 years, stabilizing supplier margins and raising OSI Systems’ procurement risk.

Supply chain cyclicality and lead times

Semiconductor and precision-optics cycles have pushed lead times above 20 weeks during peak shortages, increasing allocation risk as suppliers prioritize larger-volume customers; OSI must therefore lock forecasts and deposits to secure capacity, shifting working-capital strain upstream and compressing liquidity.

- Lead times: >20 weeks

- Priority: large-volume customers favored

- OSI response: forecasts + deposits

- Impact: upstream working-capital pressure

Counter-levers: multisourcing and scale

- Global sourcing: diversifies geographic risk

- Dual-sourcing: reduces single-supplier dependency

- Framework agreements: stabilize costs and terms

- Aggregated demand: improves volume leverage across three divisions

- Design-for-supply: mitigates single-point failures

- Long-term partnerships: trade visibility for cost stability

Supplier power strains med-radiation OEM; opto insourcing 15% cushions risk

OSI Systems faces high supplier power due to niche radiation/medical components, single-source vendors, and requalification timelines of 3–9 months, causing price and lead-time volatility (double-digit swings). Optoelectronics insourcing (15% of 2024 revenue, ~$180m of $1.2b) cushions risk but gaps remain. Lead times often exceed 20 weeks; suppliers win 3–5 year contracts.

| Metric | 2024 |

|---|---|

| Revenue | $1.2B |

| Opto revenue | $180M (15%) |

| Lead times | >20 weeks |

| Requalify | 3–9 months |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to OSI Systems' security and healthcare electronics businesses. Evaluates supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive technologies and strategic levers to protect market share and profitability.

A clear, one-sheet Porter's Five Forces summary for OSI Systems—perfect for quick strategic decisions, investor pitches, and boardroom slides to instantly gauge competitive pressure and prioritize actions.

Customers Bargaining Power

Government and large institutional buyers

Government and large institutional buyers such as sovereign agencies, airports and ports concentrate spend and use tender-based procurement with strict technical specs, giving buyers strong pricing leverage. TSA screened over 800 million passengers in 2023, and budget cycles plus competitive bids often compress vendor margins. Post-sale service and maintenance contracts partially rebalance economics by stabilizing revenue streams.

Hospital and IDN consolidation

Healthcare buyers are largely hospital systems and GPOs, with roughly 70% of U.S. hospitals now system-affiliated and GPOs managing about 90% of hospital purchasing volume, increasing supplier price sensitivity through volume discounts and vendor standardization. Clinical outcomes and device interoperability remain decisive in award decisions, supporting premium pricing for proven performance. Service uptime SLAs (commonly targeting 99.9% availability) offer a clear differentiator beyond price.

Technical performance comparability

Competing systems meet similar regulatory baselines, so 2024 procurement reviews show buyers focus on TCO and performance; detection-rate differences of 2–8 percentage points and false-alarm rates typically cited at 0.5–4% drive decisions, letting buyers leverage vendors on lifecycle costs, upgrade paths and total cost of ownership.

Switching costs and integration

Installed bases tie OSI Systems into hospital IT, PACS and airport screening workflows; switching requires retraining, certification and days-to-weeks of downtime, which tempers buyer power. Planned refresh cycles, typically every 5–7 years, reopen competitive opportunities. Extended warranties and paid software upgrades further increase lock-in.

- Installed integration: IT, PACS, screening

- Switching cost: retraining + downtime

- Refresh cycle: 5–7 years

- Lock-in: warranties & software upgrades

Aftermarket and service negotiations

Aftermarket spare parts, consumables and maintenance create recurring revenue for OSI Systems, with FY2024 revenue reported at $1.09 billion supporting stable service income; buyers bundling service in tenders compress margins as procurement seeks total-cost caps. Performance-based contracts shift uptime and quality risk back to OSI, while multiyear agreements trade price concessions for customer retention and predictable lifecycle revenues.

- Spare parts & consumables: recurring margin

- Bundled tenders: cap buyer costs, pressure margins

- Performance contracts: vendor assumes operational risk

- Multiyear deals: lower price, higher retention

GPO-driven tenders raise price pressure; FY2024 service revenue $1.09B

Buyers hold strong leverage via tendered, spec-driven procurement; 2024 sourcing emphasizes TCO and detection performance. Healthcare GPOs account for ~90% of hospital purchasing and ~70% of hospitals are system-affiliated, raising price sensitivity. FY2024 aftermarket/service revenue was $1.09 billion, but bundled tenders and 5–7 year refresh cycles compress margins and reopen competition.

| Metric | Value |

|---|---|

| FY2024 service revenue | $1.09B |

| Hospital system affiliation | ~70% |

| GPO purchasing share | ~90% |

| Refresh cycle | 5–7 yrs |

Full Version Awaits

OSI Systems Porter's Five Forces Analysis

This preview shows the exact OSI Systems Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for immediate download and use the moment you buy. What you see here is the final deliverable, identical to the document provided upon payment.