Otsuka Holding SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Otsuka Holding’s SWOT snapshot highlights diversified pharma & consumer health strengths, innovation-driven R&D, and global reach, alongside regulatory, patent, and competitive pressures that may constrain growth; emerging markets and digital health present clear opportunities. Purchase the full SWOT analysis for a research-backed, editable Word + Excel package to strategize, pitch, or invest with confidence.

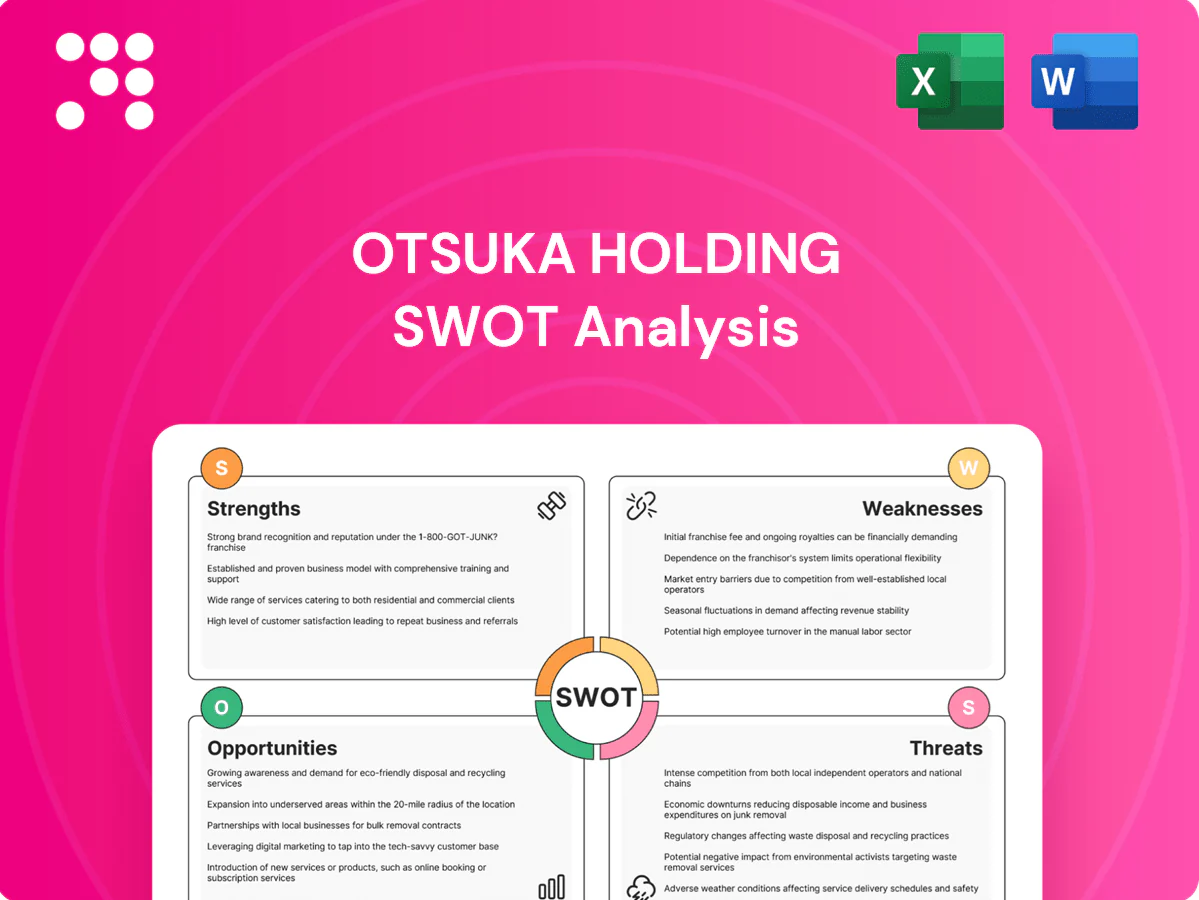

Strengths

Diversified healthcare portfolio

Otsuka spans prescription pharmaceuticals, nutraceuticals and consumer products, generating consolidated revenue of about ¥1.7 trillion in FY2023, which smooths cashflow across cycles. This breadth enables cross-brand synergies in R&D, marketing and distribution, lowering unit costs and speeding launches. Diversification reduces dependence on any single category and lets Otsuka target both treatment and prevention segments for broader market coverage.

Innovation-centric R&D culture

Otsuka prioritizes original science to tackle unmet needs, with a longstanding CNS focus evidenced by aripiprazole (Abilify) approval in 2002 and the digital pill Abilify MyCite approved in 2017. A strong discovery engine fuels a pipeline of differentiated mechanisms, enhancing clinical relevance and pricing power. This innovation ethos increases appeal for collaborations with academia and biotech partners.

Global footprint and distribution

Operations across over 80 countries give Otsuka access to diverse patient populations and growth markets, supporting scalable product launches and post-marketing surveillance. Global reach helped the group secure roughly ¥1.3 trillion revenue in FY2023 with about 60% derived overseas, mitigating single-country regulatory and reimbursement risks. Localized commercial teams tailor strategies to regional needs and accelerate uptake.

Brand equity in wellness and hydration

Otsuka’s consumer brands like Pocari Sweat, sold in over 30 countries, deliver steady cash flow and high household recognition, reinforcing a prevention-focused image through nutraceuticals and hydration products that match rising health-conscious trends. These brands enable cross-selling into adjacent categories and generate consumer usage data to guide iterative product development and targeted marketing.

Quality manufacturing and compliance

Integrated manufacturing across Otsuka's global network underpins consistent product quality and supply reliability, while robust compliance systems support approvals in stringent regulatory regimes, reducing recall risk and protecting brand trust; this infrastructure also streamlines technology transfer and enables rapid global scale-up.

- Integrated manufacturing: consistent quality, reliable supply

- Strong compliance: supports approvals, lowers recall risk

- Facilitates tech transfer: enables global scale-up

Diversified pharma-consumer group ¥1.7T, CNS R&D, 80+ countries

Otsuka’s diversified portfolio across prescription drugs, nutraceuticals and consumer products generated ¥1.7 trillion consolidated revenue in FY2023, stabilizing cashflow and enabling cross-brand synergies. A strong CNS-focused R&D engine (e.g., aripiprazole, digital pill) supports differentiated pipeline and collaboration appeal. Global operations in 80+ countries and consumer brands like Pocari Sweat (30+ countries) underpin scale, marketing reach and reliable supply.

| Metric | Value |

|---|---|

| Consolidated revenue FY2023 | ¥1.7 trillion |

| Overseas revenue | ≈¥1.3 trillion (60%) |

| Countries of operation | 80+ |

| Pocari Sweat presence | 30+ countries |

What is included in the product

Provides a concise SWOT analysis of Otsuka Holding, highlighting internal strengths and weaknesses and external opportunities and threats shaping its strategic position and growth prospects.

Provides a concise SWOT matrix tailored to Otsuka Holdings for rapid strategic alignment and stakeholder updates; editable format enables quick updates to reflect regulatory shifts, R&D pipelines, and market dynamics.

Weaknesses

Exposure to patent cycles

Dependence on a few blockbusters, notably the aripiprazole family, leaves Otsuka exposed to patent expiry and generic erosion; generics can capture up to 80% market share and U.S. prescriptions exceeded 90% by volume in 2024. Resulting revenue cliffs compress margins and constrain R&D reinvestment. Lifecycle management (line extensions, new formulations) is costly and uncertain, and pipeline delays can widen gaps during exclusivity shortfalls.

Complex multi-segment management

Running pharma, nutraceutical and consumer units creates organizational complexity for Otsuka, with around 47,000 employees globally (2024) spanning divergent operations. Differing regulatory timelines and KPIs across Rx, supplements and OTC brands complicate capital allocation and delay returns. Strategic focus can diffuse across categories, and integration costs from cross-segment M&A may dilute operating leverage and margin expansion.

Margin mix drag from consumer lines

Consumer and nutraceutical products typically show gross margins around 30–40% versus 60–80% for innovative prescription drugs, creating a clear margin mix drag for Otsuka. Higher promotional intensity in OTC/nutraceutical channels often compresses profitability and can mask underlying pharma margin expansion. That mix may constrain consolidated ROIC during heavy innovative-drug launch periods.

Regional concentration risks

Despite global operations, Otsuka’s revenue remains skewed toward key markets, so local reimbursement or policy changes in those markets can disproportionately affect results. Consumer healthcare sales show strong sensitivity to cultural preferences, limiting cross‑market uptake. Currency volatility, especially JPY fluctuations, adds short‑term earnings noise and complicates forecasting.

Clinical and regulatory execution risk

Clinical and regulatory execution risk: late-stage trial failures can wipe out years of investment and delay peak revenue; FDA standard review is ~10 months (priority ~6 months), so regulatory delays raise time-to-market and burn; safety signals may force label changes or withdrawals and trigger costly post-marketing studies.

- Late-stage failures: high sunk cost

- Regulatory delays: ~10-month FDA review

- Safety signals: label/withdrawal risk

- Post-marketing: ongoing costs

Aripiprazole patent cliffs risk margins as generics surge in US prescriptions

Heavy reliance on the aripiprazole family exposes Otsuka to patent cliffs; generics can capture up to 80% market share and US prescriptions exceeded 90% by volume in 2024, compressing margins and R&D capacity.

Operating pharma, nutraceutical and consumer arms adds complexity and integration costs; ~47,000 employees (2024) and a margin mix drag from consumer GM ~30–40% vs Rx 60–80%.

Revenue skew to key markets risks reimbursement hits and JPY volatility.

| Metric | Value |

|---|---|

| Employees (2024) | 47,000 |

| Generic share (aripiprazole peak) | up to 80% |

| US Rx volume (2024) | >90% |

| Consumer GM | 30–40% |

| Rx GM | 60–80% |

Full Version Awaits

Otsuka Holding SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full Otsuka Holding SWOT report you'll get; purchase unlocks the complete, editable version. The file is ready to use for presentations, strategic planning, or valuation work.

Elevate Your Analysis with the Complete SWOT Report

Otsuka Holding’s SWOT snapshot highlights diversified pharma & consumer health strengths, innovation-driven R&D, and global reach, alongside regulatory, patent, and competitive pressures that may constrain growth; emerging markets and digital health present clear opportunities. Purchase the full SWOT analysis for a research-backed, editable Word + Excel package to strategize, pitch, or invest with confidence.

Strengths

Diversified healthcare portfolio

Otsuka spans prescription pharmaceuticals, nutraceuticals and consumer products, generating consolidated revenue of about ¥1.7 trillion in FY2023, which smooths cashflow across cycles. This breadth enables cross-brand synergies in R&D, marketing and distribution, lowering unit costs and speeding launches. Diversification reduces dependence on any single category and lets Otsuka target both treatment and prevention segments for broader market coverage.

Innovation-centric R&D culture

Otsuka prioritizes original science to tackle unmet needs, with a longstanding CNS focus evidenced by aripiprazole (Abilify) approval in 2002 and the digital pill Abilify MyCite approved in 2017. A strong discovery engine fuels a pipeline of differentiated mechanisms, enhancing clinical relevance and pricing power. This innovation ethos increases appeal for collaborations with academia and biotech partners.

Global footprint and distribution

Operations across over 80 countries give Otsuka access to diverse patient populations and growth markets, supporting scalable product launches and post-marketing surveillance. Global reach helped the group secure roughly ¥1.3 trillion revenue in FY2023 with about 60% derived overseas, mitigating single-country regulatory and reimbursement risks. Localized commercial teams tailor strategies to regional needs and accelerate uptake.

Brand equity in wellness and hydration

Otsuka’s consumer brands like Pocari Sweat, sold in over 30 countries, deliver steady cash flow and high household recognition, reinforcing a prevention-focused image through nutraceuticals and hydration products that match rising health-conscious trends. These brands enable cross-selling into adjacent categories and generate consumer usage data to guide iterative product development and targeted marketing.

Quality manufacturing and compliance

Integrated manufacturing across Otsuka's global network underpins consistent product quality and supply reliability, while robust compliance systems support approvals in stringent regulatory regimes, reducing recall risk and protecting brand trust; this infrastructure also streamlines technology transfer and enables rapid global scale-up.

- Integrated manufacturing: consistent quality, reliable supply

- Strong compliance: supports approvals, lowers recall risk

- Facilitates tech transfer: enables global scale-up

Diversified pharma-consumer group ¥1.7T, CNS R&D, 80+ countries

Otsuka’s diversified portfolio across prescription drugs, nutraceuticals and consumer products generated ¥1.7 trillion consolidated revenue in FY2023, stabilizing cashflow and enabling cross-brand synergies. A strong CNS-focused R&D engine (e.g., aripiprazole, digital pill) supports differentiated pipeline and collaboration appeal. Global operations in 80+ countries and consumer brands like Pocari Sweat (30+ countries) underpin scale, marketing reach and reliable supply.

| Metric | Value |

|---|---|

| Consolidated revenue FY2023 | ¥1.7 trillion |

| Overseas revenue | ≈¥1.3 trillion (60%) |

| Countries of operation | 80+ |

| Pocari Sweat presence | 30+ countries |

What is included in the product

Provides a concise SWOT analysis of Otsuka Holding, highlighting internal strengths and weaknesses and external opportunities and threats shaping its strategic position and growth prospects.

Provides a concise SWOT matrix tailored to Otsuka Holdings for rapid strategic alignment and stakeholder updates; editable format enables quick updates to reflect regulatory shifts, R&D pipelines, and market dynamics.

Weaknesses

Exposure to patent cycles

Dependence on a few blockbusters, notably the aripiprazole family, leaves Otsuka exposed to patent expiry and generic erosion; generics can capture up to 80% market share and U.S. prescriptions exceeded 90% by volume in 2024. Resulting revenue cliffs compress margins and constrain R&D reinvestment. Lifecycle management (line extensions, new formulations) is costly and uncertain, and pipeline delays can widen gaps during exclusivity shortfalls.

Complex multi-segment management

Running pharma, nutraceutical and consumer units creates organizational complexity for Otsuka, with around 47,000 employees globally (2024) spanning divergent operations. Differing regulatory timelines and KPIs across Rx, supplements and OTC brands complicate capital allocation and delay returns. Strategic focus can diffuse across categories, and integration costs from cross-segment M&A may dilute operating leverage and margin expansion.

Margin mix drag from consumer lines

Consumer and nutraceutical products typically show gross margins around 30–40% versus 60–80% for innovative prescription drugs, creating a clear margin mix drag for Otsuka. Higher promotional intensity in OTC/nutraceutical channels often compresses profitability and can mask underlying pharma margin expansion. That mix may constrain consolidated ROIC during heavy innovative-drug launch periods.

Regional concentration risks

Despite global operations, Otsuka’s revenue remains skewed toward key markets, so local reimbursement or policy changes in those markets can disproportionately affect results. Consumer healthcare sales show strong sensitivity to cultural preferences, limiting cross‑market uptake. Currency volatility, especially JPY fluctuations, adds short‑term earnings noise and complicates forecasting.

Clinical and regulatory execution risk

Clinical and regulatory execution risk: late-stage trial failures can wipe out years of investment and delay peak revenue; FDA standard review is ~10 months (priority ~6 months), so regulatory delays raise time-to-market and burn; safety signals may force label changes or withdrawals and trigger costly post-marketing studies.

- Late-stage failures: high sunk cost

- Regulatory delays: ~10-month FDA review

- Safety signals: label/withdrawal risk

- Post-marketing: ongoing costs

Aripiprazole patent cliffs risk margins as generics surge in US prescriptions

Heavy reliance on the aripiprazole family exposes Otsuka to patent cliffs; generics can capture up to 80% market share and US prescriptions exceeded 90% by volume in 2024, compressing margins and R&D capacity.

Operating pharma, nutraceutical and consumer arms adds complexity and integration costs; ~47,000 employees (2024) and a margin mix drag from consumer GM ~30–40% vs Rx 60–80%.

Revenue skew to key markets risks reimbursement hits and JPY volatility.

| Metric | Value |

|---|---|

| Employees (2024) | 47,000 |

| Generic share (aripiprazole peak) | up to 80% |

| US Rx volume (2024) | >90% |

| Consumer GM | 30–40% |

| Rx GM | 60–80% |

Full Version Awaits

Otsuka Holding SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full Otsuka Holding SWOT report you'll get; purchase unlocks the complete, editable version. The file is ready to use for presentations, strategic planning, or valuation work.

Description

Elevate Your Analysis with the Complete SWOT Report

Otsuka Holding’s SWOT snapshot highlights diversified pharma & consumer health strengths, innovation-driven R&D, and global reach, alongside regulatory, patent, and competitive pressures that may constrain growth; emerging markets and digital health present clear opportunities. Purchase the full SWOT analysis for a research-backed, editable Word + Excel package to strategize, pitch, or invest with confidence.

Strengths

Diversified healthcare portfolio

Otsuka spans prescription pharmaceuticals, nutraceuticals and consumer products, generating consolidated revenue of about ¥1.7 trillion in FY2023, which smooths cashflow across cycles. This breadth enables cross-brand synergies in R&D, marketing and distribution, lowering unit costs and speeding launches. Diversification reduces dependence on any single category and lets Otsuka target both treatment and prevention segments for broader market coverage.

Innovation-centric R&D culture

Otsuka prioritizes original science to tackle unmet needs, with a longstanding CNS focus evidenced by aripiprazole (Abilify) approval in 2002 and the digital pill Abilify MyCite approved in 2017. A strong discovery engine fuels a pipeline of differentiated mechanisms, enhancing clinical relevance and pricing power. This innovation ethos increases appeal for collaborations with academia and biotech partners.

Global footprint and distribution

Operations across over 80 countries give Otsuka access to diverse patient populations and growth markets, supporting scalable product launches and post-marketing surveillance. Global reach helped the group secure roughly ¥1.3 trillion revenue in FY2023 with about 60% derived overseas, mitigating single-country regulatory and reimbursement risks. Localized commercial teams tailor strategies to regional needs and accelerate uptake.

Brand equity in wellness and hydration

Otsuka’s consumer brands like Pocari Sweat, sold in over 30 countries, deliver steady cash flow and high household recognition, reinforcing a prevention-focused image through nutraceuticals and hydration products that match rising health-conscious trends. These brands enable cross-selling into adjacent categories and generate consumer usage data to guide iterative product development and targeted marketing.

Quality manufacturing and compliance

Integrated manufacturing across Otsuka's global network underpins consistent product quality and supply reliability, while robust compliance systems support approvals in stringent regulatory regimes, reducing recall risk and protecting brand trust; this infrastructure also streamlines technology transfer and enables rapid global scale-up.

- Integrated manufacturing: consistent quality, reliable supply

- Strong compliance: supports approvals, lowers recall risk

- Facilitates tech transfer: enables global scale-up

Diversified pharma-consumer group ¥1.7T, CNS R&D, 80+ countries

Otsuka’s diversified portfolio across prescription drugs, nutraceuticals and consumer products generated ¥1.7 trillion consolidated revenue in FY2023, stabilizing cashflow and enabling cross-brand synergies. A strong CNS-focused R&D engine (e.g., aripiprazole, digital pill) supports differentiated pipeline and collaboration appeal. Global operations in 80+ countries and consumer brands like Pocari Sweat (30+ countries) underpin scale, marketing reach and reliable supply.

| Metric | Value |

|---|---|

| Consolidated revenue FY2023 | ¥1.7 trillion |

| Overseas revenue | ≈¥1.3 trillion (60%) |

| Countries of operation | 80+ |

| Pocari Sweat presence | 30+ countries |

What is included in the product

Provides a concise SWOT analysis of Otsuka Holding, highlighting internal strengths and weaknesses and external opportunities and threats shaping its strategic position and growth prospects.

Provides a concise SWOT matrix tailored to Otsuka Holdings for rapid strategic alignment and stakeholder updates; editable format enables quick updates to reflect regulatory shifts, R&D pipelines, and market dynamics.

Weaknesses

Exposure to patent cycles

Dependence on a few blockbusters, notably the aripiprazole family, leaves Otsuka exposed to patent expiry and generic erosion; generics can capture up to 80% market share and U.S. prescriptions exceeded 90% by volume in 2024. Resulting revenue cliffs compress margins and constrain R&D reinvestment. Lifecycle management (line extensions, new formulations) is costly and uncertain, and pipeline delays can widen gaps during exclusivity shortfalls.

Complex multi-segment management

Running pharma, nutraceutical and consumer units creates organizational complexity for Otsuka, with around 47,000 employees globally (2024) spanning divergent operations. Differing regulatory timelines and KPIs across Rx, supplements and OTC brands complicate capital allocation and delay returns. Strategic focus can diffuse across categories, and integration costs from cross-segment M&A may dilute operating leverage and margin expansion.

Margin mix drag from consumer lines

Consumer and nutraceutical products typically show gross margins around 30–40% versus 60–80% for innovative prescription drugs, creating a clear margin mix drag for Otsuka. Higher promotional intensity in OTC/nutraceutical channels often compresses profitability and can mask underlying pharma margin expansion. That mix may constrain consolidated ROIC during heavy innovative-drug launch periods.

Regional concentration risks

Despite global operations, Otsuka’s revenue remains skewed toward key markets, so local reimbursement or policy changes in those markets can disproportionately affect results. Consumer healthcare sales show strong sensitivity to cultural preferences, limiting cross‑market uptake. Currency volatility, especially JPY fluctuations, adds short‑term earnings noise and complicates forecasting.

Clinical and regulatory execution risk

Clinical and regulatory execution risk: late-stage trial failures can wipe out years of investment and delay peak revenue; FDA standard review is ~10 months (priority ~6 months), so regulatory delays raise time-to-market and burn; safety signals may force label changes or withdrawals and trigger costly post-marketing studies.

- Late-stage failures: high sunk cost

- Regulatory delays: ~10-month FDA review

- Safety signals: label/withdrawal risk

- Post-marketing: ongoing costs

Aripiprazole patent cliffs risk margins as generics surge in US prescriptions

Heavy reliance on the aripiprazole family exposes Otsuka to patent cliffs; generics can capture up to 80% market share and US prescriptions exceeded 90% by volume in 2024, compressing margins and R&D capacity.

Operating pharma, nutraceutical and consumer arms adds complexity and integration costs; ~47,000 employees (2024) and a margin mix drag from consumer GM ~30–40% vs Rx 60–80%.

Revenue skew to key markets risks reimbursement hits and JPY volatility.

| Metric | Value |

|---|---|

| Employees (2024) | 47,000 |

| Generic share (aripiprazole peak) | up to 80% |

| US Rx volume (2024) | >90% |

| Consumer GM | 30–40% |

| Rx GM | 60–80% |

Full Version Awaits

Otsuka Holding SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full Otsuka Holding SWOT report you'll get; purchase unlocks the complete, editable version. The file is ready to use for presentations, strategic planning, or valuation work.