Oxbow Carbon Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

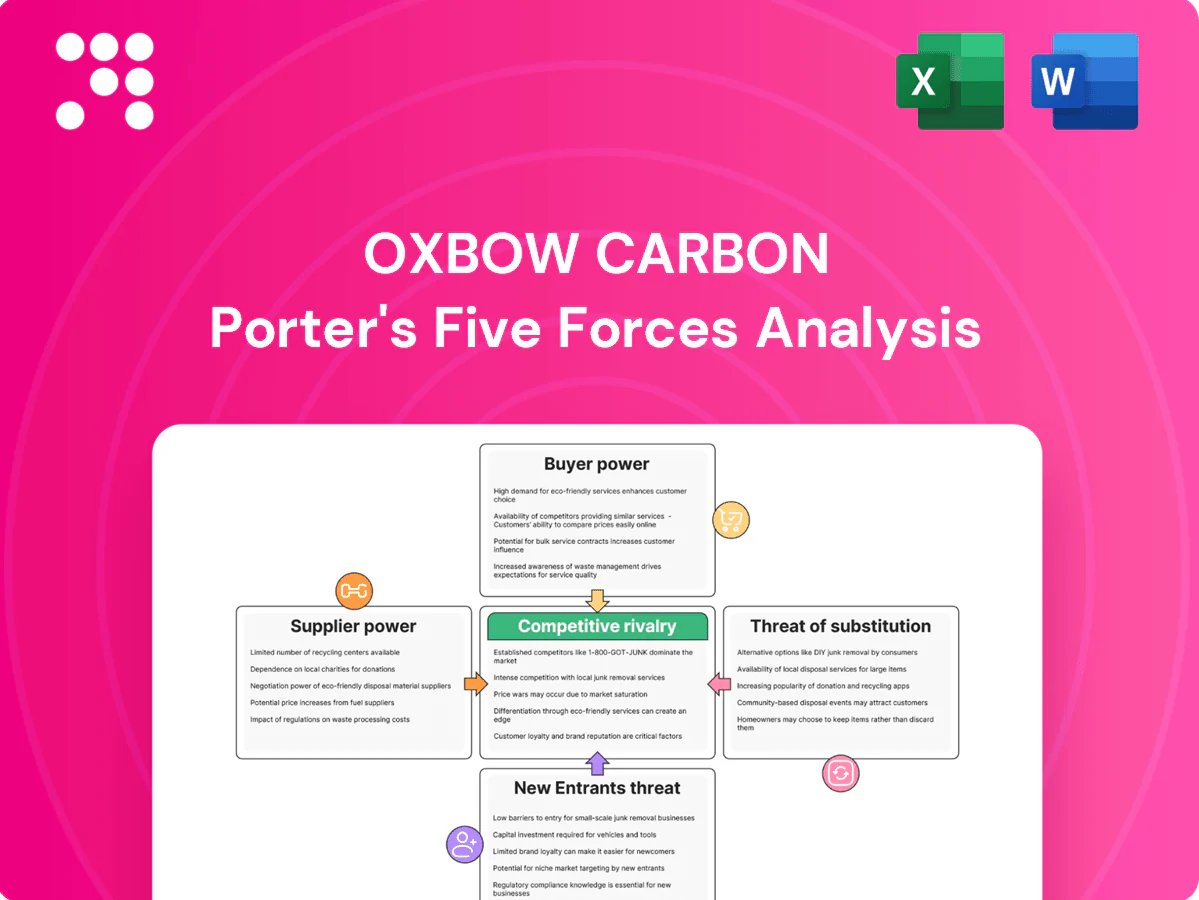

Oxbow Carbon’s Porter's Five Forces snapshot highlights strong supplier influence, moderate buyer power, niche substitutes, and significant regulatory and capital barriers shaping competitive intensity; strategic positioning hinges on feedstock control and scale. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Oxbow Carbon.

Suppliers Bargaining Power

Refinery petcoke suppliers concentrated

Petroleum coke is produced by a limited set of complex refineries, with global output concentrated in the US Gulf Coast, Middle East and India; global petcoke production was about 95 million tonnes in 2024, amplifying regional pockets by grade. This concentration gives suppliers leverage over volume allocation and timing, affecting Oxbow’s feedstock access and logistics. Because petcoke is a refinery byproduct, refineries frequently prioritize clearing output, tempering extreme pricing power despite supplier concentration.

Coal miners cyclical and diversified

Coal supply includes over a thousand producers globally, but quality, sulfur content and calorific value narrow the effective pool for industrial and metallurgical buyers; seaborne thermal coal trade in 2024 remained near 1.1 billion tonnes, concentrating premium grades. During downcycles miners typically concede pricing and volumes, while tight markets restore their leverage and push spot premia higher. Oxbow mitigates single-supplier power by arbitraging shipments across US, Australian and Indonesian basins and leveraging logistics to shift volumes.

Quality specs and blending constrain switching

End-use applications like cement, power and anode-grade calcined coke demand tight ash, sulfur and fixed-carbon specs that only a subset of suppliers reliably meet, raising effective switching costs for buyers.

Compliant suppliers therefore gain bargaining leverage through scarcity of spec-compliant feedstock and capacity.

Oxbow’s blending, inventory and logistics capabilities partially offset that supplier power by enabling tailored mixes and rapid delivery to meet end-user specs.

Logistics and terminal capacity as chokepoints

Rail, barge and port storage/throughput remain chokepoints for Oxbow Carbon, with logistics providers and terminal owners extracting premium pricing and contractual concessions when capacity tightens; 2024 industry reports continued to flag persistent congestion at major US Gulf and West Coast terminals. Take-or-pay and slot-commitment clauses in long-term contracts further lock in fixed costs and reduce operational flexibility. Securing long-term access agreements and multi-port optionality has proven the primary mitigation, lowering spot exposure and smoothing throughput risk.

- High supplier power: terminal congestion raises negotiating leverage

- Contract risk: take-or-pay and slot commitments fix costs

- Mitigation: long-term access and multi-port optionality reduce exposure

Geopolitical and regulatory risks shift power

Geopolitical sanctions, export curbs and tightening emissions rules can abruptly cut petcoke flows, boosting supplier leverage and input costs for buyers; conversely refinery coker upgrades raise petcoke output and ease tightness. As of 2024 Oxbow operates across North America, Europe and Asia‑Pacific, allowing it to shift supply among jurisdictions to balance swings.

- Sanctions tighten supply

- Coker upgrades expand output

- Oxbow: multi‑region pivot

Petcoke concentration (≈95 Mt) and port congestion strengthen suppliers; blending eases leverage

Supplier power is elevated where petcoke output concentrates (≈95 Mt global 2024) and terminals congest; seaborne thermal coal ~1.1 Bt in 2024 but premium grades are scarce. Take-or-pay contracts and slot constraints raise fixed costs, while refinery byproduct status limits extreme price control. Oxbow’s blending, inventory and multi‑port access materially reduce supplier leverage.

| Metric | 2024 |

|---|---|

| Petcoke production | 95 Mt |

| Seaborne thermal coal | 1.1 Bt |

| Terminal congestion | High (US Gulf/West Coast) |

What is included in the product

Provides a tailored Porter's Five Forces assessment for Oxbow Carbon, uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and industry rivalry; highlights disruptive threats and strategic barriers that shape pricing, profitability, and market positioning.

Oxbow Carbon's Porter's Five Forces one-sheet distills competitive pressures into a customizable, visual spider chart for instant strategic clarity. Ready-to-copy layout, no macros, and seamless dashboard integration relieve analysis bottlenecks for fast, board-ready decision-making.

Customers Bargaining Power

Large industrial buyers are concentrated

Large industrial buyers such as cement/lime producers, utilities and aluminum-anode manufacturers buy carbon products at scale—global cement output was about 4.1 billion tonnes in 2023, concentrating demand and increasing buyer leverage. Their volumes and alternative feedstock options strengthen negotiation power and pressure prices. Key-account management and demonstrated supply reliability can soften that pressure and preserve contract margins.

High price sensitivity to benchmarks

Petcoke and coal contracts are tightly linked to daily benchmarks (Brent crude averaged about $86/bbl in 2024 and the API2 ARA coal index averaged near $100/ton in 2024) plus freight, so buyers drive pricing decisions; transparent indices let purchasers push spreads down to low single-digit percentages versus index levels, though Oxbow can capture premiums for logistics, quality guarantees and blending services that justify 5–10% uplifts.

Substitutability with coal and gas

Many industrial buyers can switch between petcoke, coal, or gas if equipment specs and permits allow, giving them meaningful leverage over Oxbow; dual-fuel capability is common in cement, steel, and power sectors. This optionality strengthens buyer power in stable markets, compressing margins when fuel spreads narrow. Emissions compliance alters decisions materially: EU ETS averaged about €85/ton CO2 in 2024, raising the relative cost of high-carbon petcoke and coal.

Long-term offtakes vs spot flexibility

Some industrial buyers secure long-term offtakes with fixed pricing and quality specs to stabilize supply and moderate short-term bargaining swings, while other customers exploit spot flexibility to capture market volatility. Oxbow can tier products and contract terms—firm offtakes, indexed contracts, and spot sales—to align with differing risk appetites and dilute concentrated buyer leverage. This mix preserves margin resilience and contract negotiation leverage.

- Tiered offerings reduce single-buyer dependence

- Firm contracts limit short-term price pressure

- Spot sales capture upside from market volatility

Service, credit, and logistics reduce power

Coordinated shipping, storage, blending and trade finance from Oxbow address buyer pain points, raising switching costs and shifting negotiations away from pure price; integrated services convert spot buyers into contracted partners. Performance history and on-time delivery — logistics benchmarks often exceed 95% in 2024 — further curb buyer leverage.

- Services: bundled logistics and finance

- Switching cost: higher due to blending/storage

- Leverage reduced: >95% on-time delivery (2024 benchmark)

Buyers squeeze; EU ETS & benchmarks lift leverage; premiums, >95% OT

Large industrial buyers (cement 4.1bn t 2023) concentrate demand and press prices; benchmarks (Brent $86/bbl 2024, API2 ~$100/t 2024) empower purchasers but Oxbow captures 5–10% logistics/quality premiums. Dual-fuel switching and EU ETS €85/t (2024) increase buyer leverage; bundled logistics, finance and >95% on-time delivery raise switching costs.

| Metric | 2023/24 | Impact |

|---|---|---|

| Cement demand | 4.1bn t | Concentrated buyers |

| Brent | $86/bbl | Benchmark pricing |

| EU ETS | €85/t | Raises carbon cost |

| On-time delivery | >95% | Reduces churn |

Same Document Delivered

Oxbow Carbon Porter's Five Forces Analysis

This preview is the exact Oxbow Carbon Porter's Five Forces Analysis you'll receive upon purchase—no samples or placeholders. It contains the full, professionally formatted assessment ready for immediate download and use. Buy and get instant access to this same complete document.

A Must-Have Tool for Decision-Makers

Oxbow Carbon’s Porter's Five Forces snapshot highlights strong supplier influence, moderate buyer power, niche substitutes, and significant regulatory and capital barriers shaping competitive intensity; strategic positioning hinges on feedstock control and scale. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Oxbow Carbon.

Suppliers Bargaining Power

Refinery petcoke suppliers concentrated

Petroleum coke is produced by a limited set of complex refineries, with global output concentrated in the US Gulf Coast, Middle East and India; global petcoke production was about 95 million tonnes in 2024, amplifying regional pockets by grade. This concentration gives suppliers leverage over volume allocation and timing, affecting Oxbow’s feedstock access and logistics. Because petcoke is a refinery byproduct, refineries frequently prioritize clearing output, tempering extreme pricing power despite supplier concentration.

Coal miners cyclical and diversified

Coal supply includes over a thousand producers globally, but quality, sulfur content and calorific value narrow the effective pool for industrial and metallurgical buyers; seaborne thermal coal trade in 2024 remained near 1.1 billion tonnes, concentrating premium grades. During downcycles miners typically concede pricing and volumes, while tight markets restore their leverage and push spot premia higher. Oxbow mitigates single-supplier power by arbitraging shipments across US, Australian and Indonesian basins and leveraging logistics to shift volumes.

Quality specs and blending constrain switching

End-use applications like cement, power and anode-grade calcined coke demand tight ash, sulfur and fixed-carbon specs that only a subset of suppliers reliably meet, raising effective switching costs for buyers.

Compliant suppliers therefore gain bargaining leverage through scarcity of spec-compliant feedstock and capacity.

Oxbow’s blending, inventory and logistics capabilities partially offset that supplier power by enabling tailored mixes and rapid delivery to meet end-user specs.

Logistics and terminal capacity as chokepoints

Rail, barge and port storage/throughput remain chokepoints for Oxbow Carbon, with logistics providers and terminal owners extracting premium pricing and contractual concessions when capacity tightens; 2024 industry reports continued to flag persistent congestion at major US Gulf and West Coast terminals. Take-or-pay and slot-commitment clauses in long-term contracts further lock in fixed costs and reduce operational flexibility. Securing long-term access agreements and multi-port optionality has proven the primary mitigation, lowering spot exposure and smoothing throughput risk.

- High supplier power: terminal congestion raises negotiating leverage

- Contract risk: take-or-pay and slot commitments fix costs

- Mitigation: long-term access and multi-port optionality reduce exposure

Geopolitical and regulatory risks shift power

Geopolitical sanctions, export curbs and tightening emissions rules can abruptly cut petcoke flows, boosting supplier leverage and input costs for buyers; conversely refinery coker upgrades raise petcoke output and ease tightness. As of 2024 Oxbow operates across North America, Europe and Asia‑Pacific, allowing it to shift supply among jurisdictions to balance swings.

- Sanctions tighten supply

- Coker upgrades expand output

- Oxbow: multi‑region pivot

Petcoke concentration (≈95 Mt) and port congestion strengthen suppliers; blending eases leverage

Supplier power is elevated where petcoke output concentrates (≈95 Mt global 2024) and terminals congest; seaborne thermal coal ~1.1 Bt in 2024 but premium grades are scarce. Take-or-pay contracts and slot constraints raise fixed costs, while refinery byproduct status limits extreme price control. Oxbow’s blending, inventory and multi‑port access materially reduce supplier leverage.

| Metric | 2024 |

|---|---|

| Petcoke production | 95 Mt |

| Seaborne thermal coal | 1.1 Bt |

| Terminal congestion | High (US Gulf/West Coast) |

What is included in the product

Provides a tailored Porter's Five Forces assessment for Oxbow Carbon, uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and industry rivalry; highlights disruptive threats and strategic barriers that shape pricing, profitability, and market positioning.

Oxbow Carbon's Porter's Five Forces one-sheet distills competitive pressures into a customizable, visual spider chart for instant strategic clarity. Ready-to-copy layout, no macros, and seamless dashboard integration relieve analysis bottlenecks for fast, board-ready decision-making.

Customers Bargaining Power

Large industrial buyers are concentrated

Large industrial buyers such as cement/lime producers, utilities and aluminum-anode manufacturers buy carbon products at scale—global cement output was about 4.1 billion tonnes in 2023, concentrating demand and increasing buyer leverage. Their volumes and alternative feedstock options strengthen negotiation power and pressure prices. Key-account management and demonstrated supply reliability can soften that pressure and preserve contract margins.

High price sensitivity to benchmarks

Petcoke and coal contracts are tightly linked to daily benchmarks (Brent crude averaged about $86/bbl in 2024 and the API2 ARA coal index averaged near $100/ton in 2024) plus freight, so buyers drive pricing decisions; transparent indices let purchasers push spreads down to low single-digit percentages versus index levels, though Oxbow can capture premiums for logistics, quality guarantees and blending services that justify 5–10% uplifts.

Substitutability with coal and gas

Many industrial buyers can switch between petcoke, coal, or gas if equipment specs and permits allow, giving them meaningful leverage over Oxbow; dual-fuel capability is common in cement, steel, and power sectors. This optionality strengthens buyer power in stable markets, compressing margins when fuel spreads narrow. Emissions compliance alters decisions materially: EU ETS averaged about €85/ton CO2 in 2024, raising the relative cost of high-carbon petcoke and coal.

Long-term offtakes vs spot flexibility

Some industrial buyers secure long-term offtakes with fixed pricing and quality specs to stabilize supply and moderate short-term bargaining swings, while other customers exploit spot flexibility to capture market volatility. Oxbow can tier products and contract terms—firm offtakes, indexed contracts, and spot sales—to align with differing risk appetites and dilute concentrated buyer leverage. This mix preserves margin resilience and contract negotiation leverage.

- Tiered offerings reduce single-buyer dependence

- Firm contracts limit short-term price pressure

- Spot sales capture upside from market volatility

Service, credit, and logistics reduce power

Coordinated shipping, storage, blending and trade finance from Oxbow address buyer pain points, raising switching costs and shifting negotiations away from pure price; integrated services convert spot buyers into contracted partners. Performance history and on-time delivery — logistics benchmarks often exceed 95% in 2024 — further curb buyer leverage.

- Services: bundled logistics and finance

- Switching cost: higher due to blending/storage

- Leverage reduced: >95% on-time delivery (2024 benchmark)

Buyers squeeze; EU ETS & benchmarks lift leverage; premiums, >95% OT

Large industrial buyers (cement 4.1bn t 2023) concentrate demand and press prices; benchmarks (Brent $86/bbl 2024, API2 ~$100/t 2024) empower purchasers but Oxbow captures 5–10% logistics/quality premiums. Dual-fuel switching and EU ETS €85/t (2024) increase buyer leverage; bundled logistics, finance and >95% on-time delivery raise switching costs.

| Metric | 2023/24 | Impact |

|---|---|---|

| Cement demand | 4.1bn t | Concentrated buyers |

| Brent | $86/bbl | Benchmark pricing |

| EU ETS | €85/t | Raises carbon cost |

| On-time delivery | >95% | Reduces churn |

Same Document Delivered

Oxbow Carbon Porter's Five Forces Analysis

This preview is the exact Oxbow Carbon Porter's Five Forces Analysis you'll receive upon purchase—no samples or placeholders. It contains the full, professionally formatted assessment ready for immediate download and use. Buy and get instant access to this same complete document.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Oxbow Carbon’s Porter's Five Forces snapshot highlights strong supplier influence, moderate buyer power, niche substitutes, and significant regulatory and capital barriers shaping competitive intensity; strategic positioning hinges on feedstock control and scale. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Oxbow Carbon.

Suppliers Bargaining Power

Refinery petcoke suppliers concentrated

Petroleum coke is produced by a limited set of complex refineries, with global output concentrated in the US Gulf Coast, Middle East and India; global petcoke production was about 95 million tonnes in 2024, amplifying regional pockets by grade. This concentration gives suppliers leverage over volume allocation and timing, affecting Oxbow’s feedstock access and logistics. Because petcoke is a refinery byproduct, refineries frequently prioritize clearing output, tempering extreme pricing power despite supplier concentration.

Coal miners cyclical and diversified

Coal supply includes over a thousand producers globally, but quality, sulfur content and calorific value narrow the effective pool for industrial and metallurgical buyers; seaborne thermal coal trade in 2024 remained near 1.1 billion tonnes, concentrating premium grades. During downcycles miners typically concede pricing and volumes, while tight markets restore their leverage and push spot premia higher. Oxbow mitigates single-supplier power by arbitraging shipments across US, Australian and Indonesian basins and leveraging logistics to shift volumes.

Quality specs and blending constrain switching

End-use applications like cement, power and anode-grade calcined coke demand tight ash, sulfur and fixed-carbon specs that only a subset of suppliers reliably meet, raising effective switching costs for buyers.

Compliant suppliers therefore gain bargaining leverage through scarcity of spec-compliant feedstock and capacity.

Oxbow’s blending, inventory and logistics capabilities partially offset that supplier power by enabling tailored mixes and rapid delivery to meet end-user specs.

Logistics and terminal capacity as chokepoints

Rail, barge and port storage/throughput remain chokepoints for Oxbow Carbon, with logistics providers and terminal owners extracting premium pricing and contractual concessions when capacity tightens; 2024 industry reports continued to flag persistent congestion at major US Gulf and West Coast terminals. Take-or-pay and slot-commitment clauses in long-term contracts further lock in fixed costs and reduce operational flexibility. Securing long-term access agreements and multi-port optionality has proven the primary mitigation, lowering spot exposure and smoothing throughput risk.

- High supplier power: terminal congestion raises negotiating leverage

- Contract risk: take-or-pay and slot commitments fix costs

- Mitigation: long-term access and multi-port optionality reduce exposure

Geopolitical and regulatory risks shift power

Geopolitical sanctions, export curbs and tightening emissions rules can abruptly cut petcoke flows, boosting supplier leverage and input costs for buyers; conversely refinery coker upgrades raise petcoke output and ease tightness. As of 2024 Oxbow operates across North America, Europe and Asia‑Pacific, allowing it to shift supply among jurisdictions to balance swings.

- Sanctions tighten supply

- Coker upgrades expand output

- Oxbow: multi‑region pivot

Petcoke concentration (≈95 Mt) and port congestion strengthen suppliers; blending eases leverage

Supplier power is elevated where petcoke output concentrates (≈95 Mt global 2024) and terminals congest; seaborne thermal coal ~1.1 Bt in 2024 but premium grades are scarce. Take-or-pay contracts and slot constraints raise fixed costs, while refinery byproduct status limits extreme price control. Oxbow’s blending, inventory and multi‑port access materially reduce supplier leverage.

| Metric | 2024 |

|---|---|

| Petcoke production | 95 Mt |

| Seaborne thermal coal | 1.1 Bt |

| Terminal congestion | High (US Gulf/West Coast) |

What is included in the product

Provides a tailored Porter's Five Forces assessment for Oxbow Carbon, uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and industry rivalry; highlights disruptive threats and strategic barriers that shape pricing, profitability, and market positioning.

Oxbow Carbon's Porter's Five Forces one-sheet distills competitive pressures into a customizable, visual spider chart for instant strategic clarity. Ready-to-copy layout, no macros, and seamless dashboard integration relieve analysis bottlenecks for fast, board-ready decision-making.

Customers Bargaining Power

Large industrial buyers are concentrated

Large industrial buyers such as cement/lime producers, utilities and aluminum-anode manufacturers buy carbon products at scale—global cement output was about 4.1 billion tonnes in 2023, concentrating demand and increasing buyer leverage. Their volumes and alternative feedstock options strengthen negotiation power and pressure prices. Key-account management and demonstrated supply reliability can soften that pressure and preserve contract margins.

High price sensitivity to benchmarks

Petcoke and coal contracts are tightly linked to daily benchmarks (Brent crude averaged about $86/bbl in 2024 and the API2 ARA coal index averaged near $100/ton in 2024) plus freight, so buyers drive pricing decisions; transparent indices let purchasers push spreads down to low single-digit percentages versus index levels, though Oxbow can capture premiums for logistics, quality guarantees and blending services that justify 5–10% uplifts.

Substitutability with coal and gas

Many industrial buyers can switch between petcoke, coal, or gas if equipment specs and permits allow, giving them meaningful leverage over Oxbow; dual-fuel capability is common in cement, steel, and power sectors. This optionality strengthens buyer power in stable markets, compressing margins when fuel spreads narrow. Emissions compliance alters decisions materially: EU ETS averaged about €85/ton CO2 in 2024, raising the relative cost of high-carbon petcoke and coal.

Long-term offtakes vs spot flexibility

Some industrial buyers secure long-term offtakes with fixed pricing and quality specs to stabilize supply and moderate short-term bargaining swings, while other customers exploit spot flexibility to capture market volatility. Oxbow can tier products and contract terms—firm offtakes, indexed contracts, and spot sales—to align with differing risk appetites and dilute concentrated buyer leverage. This mix preserves margin resilience and contract negotiation leverage.

- Tiered offerings reduce single-buyer dependence

- Firm contracts limit short-term price pressure

- Spot sales capture upside from market volatility

Service, credit, and logistics reduce power

Coordinated shipping, storage, blending and trade finance from Oxbow address buyer pain points, raising switching costs and shifting negotiations away from pure price; integrated services convert spot buyers into contracted partners. Performance history and on-time delivery — logistics benchmarks often exceed 95% in 2024 — further curb buyer leverage.

- Services: bundled logistics and finance

- Switching cost: higher due to blending/storage

- Leverage reduced: >95% on-time delivery (2024 benchmark)

Buyers squeeze; EU ETS & benchmarks lift leverage; premiums, >95% OT

Large industrial buyers (cement 4.1bn t 2023) concentrate demand and press prices; benchmarks (Brent $86/bbl 2024, API2 ~$100/t 2024) empower purchasers but Oxbow captures 5–10% logistics/quality premiums. Dual-fuel switching and EU ETS €85/t (2024) increase buyer leverage; bundled logistics, finance and >95% on-time delivery raise switching costs.

| Metric | 2023/24 | Impact |

|---|---|---|

| Cement demand | 4.1bn t | Concentrated buyers |

| Brent | $86/bbl | Benchmark pricing |

| EU ETS | €85/t | Raises carbon cost |

| On-time delivery | >95% | Reduces churn |

Same Document Delivered

Oxbow Carbon Porter's Five Forces Analysis

This preview is the exact Oxbow Carbon Porter's Five Forces Analysis you'll receive upon purchase—no samples or placeholders. It contains the full, professionally formatted assessment ready for immediate download and use. Buy and get instant access to this same complete document.