Paccar Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

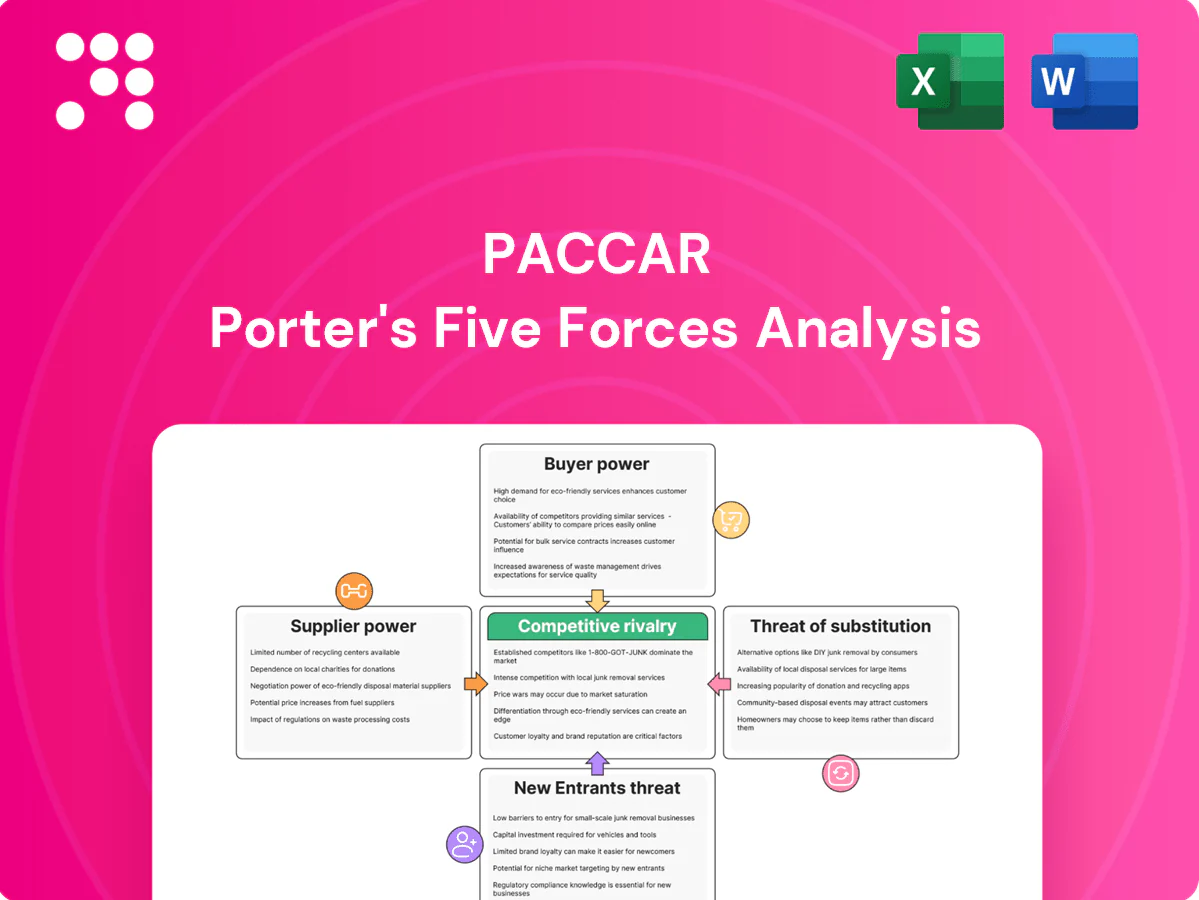

Paccar’s Porter's Five Forces analysis highlights steady buyer power, high supplier specialization, moderate threat of new entrants due to capital intensity, rivalry among established OEMs, and limited substitutes for heavy trucks. This snapshot reveals key competitive pressures and strategic implications. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for investment or strategy.

Suppliers Bargaining Power

Concentrated Tier-1 component base

Heavy-duty trucks rely on a limited set of Tier-1 suppliers for critical systems like transmissions, braking, and ADAS, concentrating bargaining power among vendors such as ZF and Bosch while PACCAR retains in-house engine production. Even with PACCAR’s engines, key modules and software still come from specialized suppliers, increasing leverage during component shortages. Long-term agreements and supplier partnerships reduce but do not eliminate exposure to supply disruptions.

Cyclic commodity and material inputs

Steel (US HRC ~850 USD/ton in 2024), aluminum (LME ~2,300 USD/ton in 2024) and energy (Henry Hub ~2.9 USD/MMBtu, diesel ~3.9 USD/gal avg 2024) directly drive Paccar build economics; suppliers can pass through hikes in tight markets, compressing OEM margins. Hedging and multi-sourcing mitigate but leave basis and timing risk. Regional premiums and tariffs (eg 25% US steel tariffs) add further input volatility.

Semiconductors and battery supply tightness

Semiconductors and power electronics are bottlenecks for modern trucks and telematics; semiconductor content per Class 8 truck was roughly $1,500–$3,000 in 2024.

Electrification increases dependence on cells and battery materials concentrated upstream, with CATL at about 38% of global cell shipments in 2024 and the top five producers accounting for over 70% of capacity.

Suppliers can prioritize higher-margin sectors in shortages, forcing OEMs to secure 6–12 month lead-time inventory and deepen strategic partnerships to guarantee volumes.

Logistics and lead-time dependencies

Global supply chains heighten PACCAR’s exposure to transport delays and port congestion, while long lead times for custom components strengthen supplier leverage; dual sourcing and nearshoring reduce this risk but add supplier-management complexity; PACCAR’s scale helps reallocate inventory and negotiate terms but does not eliminate disruptions.

- Dual sourcing reduces single-supplier risk

- Nearshoring lowers transit disruption exposure

- Scale improves negotiating leverage but not immunity

Standards, IP, and switching frictions

Proprietary interfaces and software ecosystems at Paccar create supplier stickiness, contributing to supply-chain resilience and higher integration value; Paccar reported $29.8 billion revenue in 2024, underscoring scale-dependent dependency. Requalification for safety-critical parts is time-consuming and costly, raising short- to medium-term switching costs, while long-term platform standardization gradually reduces supplier dependence.

- Requalification: 12–24 months for safety-critical parts

- Short/medium switching cost: high

- Long-term: platform standardization lowers dependency

Concentrated Tier-1 supplier power raises costs, supply risk for Class 8 truck makers

PACCAR faces concentrated Tier-1 supplier power for transmissions, ADAS and semiconductors despite in-house engines, raising switching costs and reliance during shortages. 2024 inputs — US HRC steel ~850 USD/t, aluminum ~2,300 USD/t, Henry Hub 2.9 USD/MMBtu, diesel ~3.9 USD/gal — compress margins when passed through. Semiconductor content per Class 8 truck ~$1,500–3,000; CATL ~38% cell share heightens battery sourcing risk. Requalification for safety parts 12–24 months; PACCAR revenue $29.8B (2024).

| Metric | 2024 value |

|---|---|

| US HRC steel | ~850 USD/ton |

| Aluminum (LME) | ~2,300 USD/ton |

| Henry Hub | ~2.9 USD/MMBtu |

| Diesel (avg) | ~3.9 USD/gal |

| Semiconductor content/truck | ~1,500–3,000 USD |

| CATL share | ~38% |

| PACCAR revenue | 29.8B USD |

| Requalification time | 12–24 months |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threat of substitutes and new entrants, and rivalry intensity shaping Paccar's profitability, with strategic commentary on disruptive technologies, regulatory shifts, and market barriers that protect or threaten its position.

One-sheet Paccar Porter’s Five Forces analysis that instantly clarifies competitive pressure and decision points for strategy or investment.

Customers Bargaining Power

Large fleet buyers with scale

Major fleet buyers purchase Class 8 trucks in volumes of hundreds to thousands, negotiate aggressively and benchmark total lifecycle cost, amplifying price pressure through OEM switching; framework agreements soften but do not eliminate leverage. PACCAR counters with strong brand, uptime programs and higher residual values—supporting its FY2024 revenue of about $31.8 billion—preserving margins despite fleet bargaining power.

TCO and uptime-driven decisions

Fuel efficiency (~30% of TCO in 2024), maintenance and resale dominate procurement; buyers now demand demonstrable savings and telematics-backed uptime data to justify purchases.

PacLease, dense parts networks and extended warranties act as leverage points; transparent analytics can win deals but also make vendor offerings directly comparable, intensifying price and spec competition.

Financing as a bargaining lever

PACCAR Financial enhances PACCAR truck packages via tailored leases and loans, supporting dealer sales with a finance portfolio of about $8.6 billion in receivables at year-end 2024. Sophisticated fleets exploit contract terms and residuals to extract value, while tight 2023–24 credit cycles shifted bargaining power toward cash-strong buyers. Integrated finance deepens OEM-customer ties but compresses yields as financing supports competitive pricing.

Customization and spec flexibility

Customers demand bespoke specs to meet duty cycles and regional regs, raising negotiating touchpoints as high-mix orders drive configuration complexity; in 2024 PACCAR continued using modular platforms such as the PACCAR MX engine family to contain costs and variant proliferation. Buyers increasingly leverage alternative OEMs or used-truck markets if lead times extend beyond acceptable windows.

- High-mix = more touchpoints

- Modular platforms (PACCAR MX) reduce cost/complexity

- Buyers defect if lead times stretch

Aftermarket and service expectations

Aftermarket parts availability and Paccar's >2,200 dealer locations (2024) increase switching costs by providing local inventory and rapid service. Strong dealer service and warranties lock in value, reducing buyer power. Telematics-driven maintenance raises transparency and customer expectations for predictive uptime, and poor uptime quickly triggers competitive bids.

- Dealer coverage: >2,200 locations (2024)

- Service locks buyers by reducing switching friction

- Telematics raises uptime transparency and demand for predictive maintenance

Fleet buyers squeeze margins; brands, dealer reach and finance assets defend revenue

Major fleet buyers leverage volume pricing, TCO benchmarking and OEM switching to press margins, but PACCAR's strong brands and uptime programs helped sustain FY2024 revenue of about $31.8 billion. PACCAR Financial (receivables ~$8.6 billion) and >2,200 dealer locations raise switching costs while telematics and fuel (~30% of TCO) intensify spec and price scrutiny.

| Metric | 2024 |

|---|---|

| Revenue | $31.8B |

| Finance receivables | $8.6B |

| Dealer locations | >2,200 |

| Fuel share of TCO | ~30% |

Preview the Actual Deliverable

Paccar Porter's Five Forces Analysis

This preview shows the exact Paccar Porter’s Five Forces analysis you’ll receive—fully written, formatted, and ready for immediate download after purchase. It is the same complete document provided to customers, not a sample or placeholder. Use it right away for strategic, competitive, and valuation work with no additional setup required.

A Must-Have Tool for Decision-Makers

Paccar’s Porter's Five Forces analysis highlights steady buyer power, high supplier specialization, moderate threat of new entrants due to capital intensity, rivalry among established OEMs, and limited substitutes for heavy trucks. This snapshot reveals key competitive pressures and strategic implications. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for investment or strategy.

Suppliers Bargaining Power

Concentrated Tier-1 component base

Heavy-duty trucks rely on a limited set of Tier-1 suppliers for critical systems like transmissions, braking, and ADAS, concentrating bargaining power among vendors such as ZF and Bosch while PACCAR retains in-house engine production. Even with PACCAR’s engines, key modules and software still come from specialized suppliers, increasing leverage during component shortages. Long-term agreements and supplier partnerships reduce but do not eliminate exposure to supply disruptions.

Cyclic commodity and material inputs

Steel (US HRC ~850 USD/ton in 2024), aluminum (LME ~2,300 USD/ton in 2024) and energy (Henry Hub ~2.9 USD/MMBtu, diesel ~3.9 USD/gal avg 2024) directly drive Paccar build economics; suppliers can pass through hikes in tight markets, compressing OEM margins. Hedging and multi-sourcing mitigate but leave basis and timing risk. Regional premiums and tariffs (eg 25% US steel tariffs) add further input volatility.

Semiconductors and battery supply tightness

Semiconductors and power electronics are bottlenecks for modern trucks and telematics; semiconductor content per Class 8 truck was roughly $1,500–$3,000 in 2024.

Electrification increases dependence on cells and battery materials concentrated upstream, with CATL at about 38% of global cell shipments in 2024 and the top five producers accounting for over 70% of capacity.

Suppliers can prioritize higher-margin sectors in shortages, forcing OEMs to secure 6–12 month lead-time inventory and deepen strategic partnerships to guarantee volumes.

Logistics and lead-time dependencies

Global supply chains heighten PACCAR’s exposure to transport delays and port congestion, while long lead times for custom components strengthen supplier leverage; dual sourcing and nearshoring reduce this risk but add supplier-management complexity; PACCAR’s scale helps reallocate inventory and negotiate terms but does not eliminate disruptions.

- Dual sourcing reduces single-supplier risk

- Nearshoring lowers transit disruption exposure

- Scale improves negotiating leverage but not immunity

Standards, IP, and switching frictions

Proprietary interfaces and software ecosystems at Paccar create supplier stickiness, contributing to supply-chain resilience and higher integration value; Paccar reported $29.8 billion revenue in 2024, underscoring scale-dependent dependency. Requalification for safety-critical parts is time-consuming and costly, raising short- to medium-term switching costs, while long-term platform standardization gradually reduces supplier dependence.

- Requalification: 12–24 months for safety-critical parts

- Short/medium switching cost: high

- Long-term: platform standardization lowers dependency

Concentrated Tier-1 supplier power raises costs, supply risk for Class 8 truck makers

PACCAR faces concentrated Tier-1 supplier power for transmissions, ADAS and semiconductors despite in-house engines, raising switching costs and reliance during shortages. 2024 inputs — US HRC steel ~850 USD/t, aluminum ~2,300 USD/t, Henry Hub 2.9 USD/MMBtu, diesel ~3.9 USD/gal — compress margins when passed through. Semiconductor content per Class 8 truck ~$1,500–3,000; CATL ~38% cell share heightens battery sourcing risk. Requalification for safety parts 12–24 months; PACCAR revenue $29.8B (2024).

| Metric | 2024 value |

|---|---|

| US HRC steel | ~850 USD/ton |

| Aluminum (LME) | ~2,300 USD/ton |

| Henry Hub | ~2.9 USD/MMBtu |

| Diesel (avg) | ~3.9 USD/gal |

| Semiconductor content/truck | ~1,500–3,000 USD |

| CATL share | ~38% |

| PACCAR revenue | 29.8B USD |

| Requalification time | 12–24 months |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threat of substitutes and new entrants, and rivalry intensity shaping Paccar's profitability, with strategic commentary on disruptive technologies, regulatory shifts, and market barriers that protect or threaten its position.

One-sheet Paccar Porter’s Five Forces analysis that instantly clarifies competitive pressure and decision points for strategy or investment.

Customers Bargaining Power

Large fleet buyers with scale

Major fleet buyers purchase Class 8 trucks in volumes of hundreds to thousands, negotiate aggressively and benchmark total lifecycle cost, amplifying price pressure through OEM switching; framework agreements soften but do not eliminate leverage. PACCAR counters with strong brand, uptime programs and higher residual values—supporting its FY2024 revenue of about $31.8 billion—preserving margins despite fleet bargaining power.

TCO and uptime-driven decisions

Fuel efficiency (~30% of TCO in 2024), maintenance and resale dominate procurement; buyers now demand demonstrable savings and telematics-backed uptime data to justify purchases.

PacLease, dense parts networks and extended warranties act as leverage points; transparent analytics can win deals but also make vendor offerings directly comparable, intensifying price and spec competition.

Financing as a bargaining lever

PACCAR Financial enhances PACCAR truck packages via tailored leases and loans, supporting dealer sales with a finance portfolio of about $8.6 billion in receivables at year-end 2024. Sophisticated fleets exploit contract terms and residuals to extract value, while tight 2023–24 credit cycles shifted bargaining power toward cash-strong buyers. Integrated finance deepens OEM-customer ties but compresses yields as financing supports competitive pricing.

Customization and spec flexibility

Customers demand bespoke specs to meet duty cycles and regional regs, raising negotiating touchpoints as high-mix orders drive configuration complexity; in 2024 PACCAR continued using modular platforms such as the PACCAR MX engine family to contain costs and variant proliferation. Buyers increasingly leverage alternative OEMs or used-truck markets if lead times extend beyond acceptable windows.

- High-mix = more touchpoints

- Modular platforms (PACCAR MX) reduce cost/complexity

- Buyers defect if lead times stretch

Aftermarket and service expectations

Aftermarket parts availability and Paccar's >2,200 dealer locations (2024) increase switching costs by providing local inventory and rapid service. Strong dealer service and warranties lock in value, reducing buyer power. Telematics-driven maintenance raises transparency and customer expectations for predictive uptime, and poor uptime quickly triggers competitive bids.

- Dealer coverage: >2,200 locations (2024)

- Service locks buyers by reducing switching friction

- Telematics raises uptime transparency and demand for predictive maintenance

Fleet buyers squeeze margins; brands, dealer reach and finance assets defend revenue

Major fleet buyers leverage volume pricing, TCO benchmarking and OEM switching to press margins, but PACCAR's strong brands and uptime programs helped sustain FY2024 revenue of about $31.8 billion. PACCAR Financial (receivables ~$8.6 billion) and >2,200 dealer locations raise switching costs while telematics and fuel (~30% of TCO) intensify spec and price scrutiny.

| Metric | 2024 |

|---|---|

| Revenue | $31.8B |

| Finance receivables | $8.6B |

| Dealer locations | >2,200 |

| Fuel share of TCO | ~30% |

Preview the Actual Deliverable

Paccar Porter's Five Forces Analysis

This preview shows the exact Paccar Porter’s Five Forces analysis you’ll receive—fully written, formatted, and ready for immediate download after purchase. It is the same complete document provided to customers, not a sample or placeholder. Use it right away for strategic, competitive, and valuation work with no additional setup required.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Paccar’s Porter's Five Forces analysis highlights steady buyer power, high supplier specialization, moderate threat of new entrants due to capital intensity, rivalry among established OEMs, and limited substitutes for heavy trucks. This snapshot reveals key competitive pressures and strategic implications. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for investment or strategy.

Suppliers Bargaining Power

Concentrated Tier-1 component base

Heavy-duty trucks rely on a limited set of Tier-1 suppliers for critical systems like transmissions, braking, and ADAS, concentrating bargaining power among vendors such as ZF and Bosch while PACCAR retains in-house engine production. Even with PACCAR’s engines, key modules and software still come from specialized suppliers, increasing leverage during component shortages. Long-term agreements and supplier partnerships reduce but do not eliminate exposure to supply disruptions.

Cyclic commodity and material inputs

Steel (US HRC ~850 USD/ton in 2024), aluminum (LME ~2,300 USD/ton in 2024) and energy (Henry Hub ~2.9 USD/MMBtu, diesel ~3.9 USD/gal avg 2024) directly drive Paccar build economics; suppliers can pass through hikes in tight markets, compressing OEM margins. Hedging and multi-sourcing mitigate but leave basis and timing risk. Regional premiums and tariffs (eg 25% US steel tariffs) add further input volatility.

Semiconductors and battery supply tightness

Semiconductors and power electronics are bottlenecks for modern trucks and telematics; semiconductor content per Class 8 truck was roughly $1,500–$3,000 in 2024.

Electrification increases dependence on cells and battery materials concentrated upstream, with CATL at about 38% of global cell shipments in 2024 and the top five producers accounting for over 70% of capacity.

Suppliers can prioritize higher-margin sectors in shortages, forcing OEMs to secure 6–12 month lead-time inventory and deepen strategic partnerships to guarantee volumes.

Logistics and lead-time dependencies

Global supply chains heighten PACCAR’s exposure to transport delays and port congestion, while long lead times for custom components strengthen supplier leverage; dual sourcing and nearshoring reduce this risk but add supplier-management complexity; PACCAR’s scale helps reallocate inventory and negotiate terms but does not eliminate disruptions.

- Dual sourcing reduces single-supplier risk

- Nearshoring lowers transit disruption exposure

- Scale improves negotiating leverage but not immunity

Standards, IP, and switching frictions

Proprietary interfaces and software ecosystems at Paccar create supplier stickiness, contributing to supply-chain resilience and higher integration value; Paccar reported $29.8 billion revenue in 2024, underscoring scale-dependent dependency. Requalification for safety-critical parts is time-consuming and costly, raising short- to medium-term switching costs, while long-term platform standardization gradually reduces supplier dependence.

- Requalification: 12–24 months for safety-critical parts

- Short/medium switching cost: high

- Long-term: platform standardization lowers dependency

Concentrated Tier-1 supplier power raises costs, supply risk for Class 8 truck makers

PACCAR faces concentrated Tier-1 supplier power for transmissions, ADAS and semiconductors despite in-house engines, raising switching costs and reliance during shortages. 2024 inputs — US HRC steel ~850 USD/t, aluminum ~2,300 USD/t, Henry Hub 2.9 USD/MMBtu, diesel ~3.9 USD/gal — compress margins when passed through. Semiconductor content per Class 8 truck ~$1,500–3,000; CATL ~38% cell share heightens battery sourcing risk. Requalification for safety parts 12–24 months; PACCAR revenue $29.8B (2024).

| Metric | 2024 value |

|---|---|

| US HRC steel | ~850 USD/ton |

| Aluminum (LME) | ~2,300 USD/ton |

| Henry Hub | ~2.9 USD/MMBtu |

| Diesel (avg) | ~3.9 USD/gal |

| Semiconductor content/truck | ~1,500–3,000 USD |

| CATL share | ~38% |

| PACCAR revenue | 29.8B USD |

| Requalification time | 12–24 months |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threat of substitutes and new entrants, and rivalry intensity shaping Paccar's profitability, with strategic commentary on disruptive technologies, regulatory shifts, and market barriers that protect or threaten its position.

One-sheet Paccar Porter’s Five Forces analysis that instantly clarifies competitive pressure and decision points for strategy or investment.

Customers Bargaining Power

Large fleet buyers with scale

Major fleet buyers purchase Class 8 trucks in volumes of hundreds to thousands, negotiate aggressively and benchmark total lifecycle cost, amplifying price pressure through OEM switching; framework agreements soften but do not eliminate leverage. PACCAR counters with strong brand, uptime programs and higher residual values—supporting its FY2024 revenue of about $31.8 billion—preserving margins despite fleet bargaining power.

TCO and uptime-driven decisions

Fuel efficiency (~30% of TCO in 2024), maintenance and resale dominate procurement; buyers now demand demonstrable savings and telematics-backed uptime data to justify purchases.

PacLease, dense parts networks and extended warranties act as leverage points; transparent analytics can win deals but also make vendor offerings directly comparable, intensifying price and spec competition.

Financing as a bargaining lever

PACCAR Financial enhances PACCAR truck packages via tailored leases and loans, supporting dealer sales with a finance portfolio of about $8.6 billion in receivables at year-end 2024. Sophisticated fleets exploit contract terms and residuals to extract value, while tight 2023–24 credit cycles shifted bargaining power toward cash-strong buyers. Integrated finance deepens OEM-customer ties but compresses yields as financing supports competitive pricing.

Customization and spec flexibility

Customers demand bespoke specs to meet duty cycles and regional regs, raising negotiating touchpoints as high-mix orders drive configuration complexity; in 2024 PACCAR continued using modular platforms such as the PACCAR MX engine family to contain costs and variant proliferation. Buyers increasingly leverage alternative OEMs or used-truck markets if lead times extend beyond acceptable windows.

- High-mix = more touchpoints

- Modular platforms (PACCAR MX) reduce cost/complexity

- Buyers defect if lead times stretch

Aftermarket and service expectations

Aftermarket parts availability and Paccar's >2,200 dealer locations (2024) increase switching costs by providing local inventory and rapid service. Strong dealer service and warranties lock in value, reducing buyer power. Telematics-driven maintenance raises transparency and customer expectations for predictive uptime, and poor uptime quickly triggers competitive bids.

- Dealer coverage: >2,200 locations (2024)

- Service locks buyers by reducing switching friction

- Telematics raises uptime transparency and demand for predictive maintenance

Fleet buyers squeeze margins; brands, dealer reach and finance assets defend revenue

Major fleet buyers leverage volume pricing, TCO benchmarking and OEM switching to press margins, but PACCAR's strong brands and uptime programs helped sustain FY2024 revenue of about $31.8 billion. PACCAR Financial (receivables ~$8.6 billion) and >2,200 dealer locations raise switching costs while telematics and fuel (~30% of TCO) intensify spec and price scrutiny.

| Metric | 2024 |

|---|---|

| Revenue | $31.8B |

| Finance receivables | $8.6B |

| Dealer locations | >2,200 |

| Fuel share of TCO | ~30% |

Preview the Actual Deliverable

Paccar Porter's Five Forces Analysis

This preview shows the exact Paccar Porter’s Five Forces analysis you’ll receive—fully written, formatted, and ready for immediate download after purchase. It is the same complete document provided to customers, not a sample or placeholder. Use it right away for strategic, competitive, and valuation work with no additional setup required.