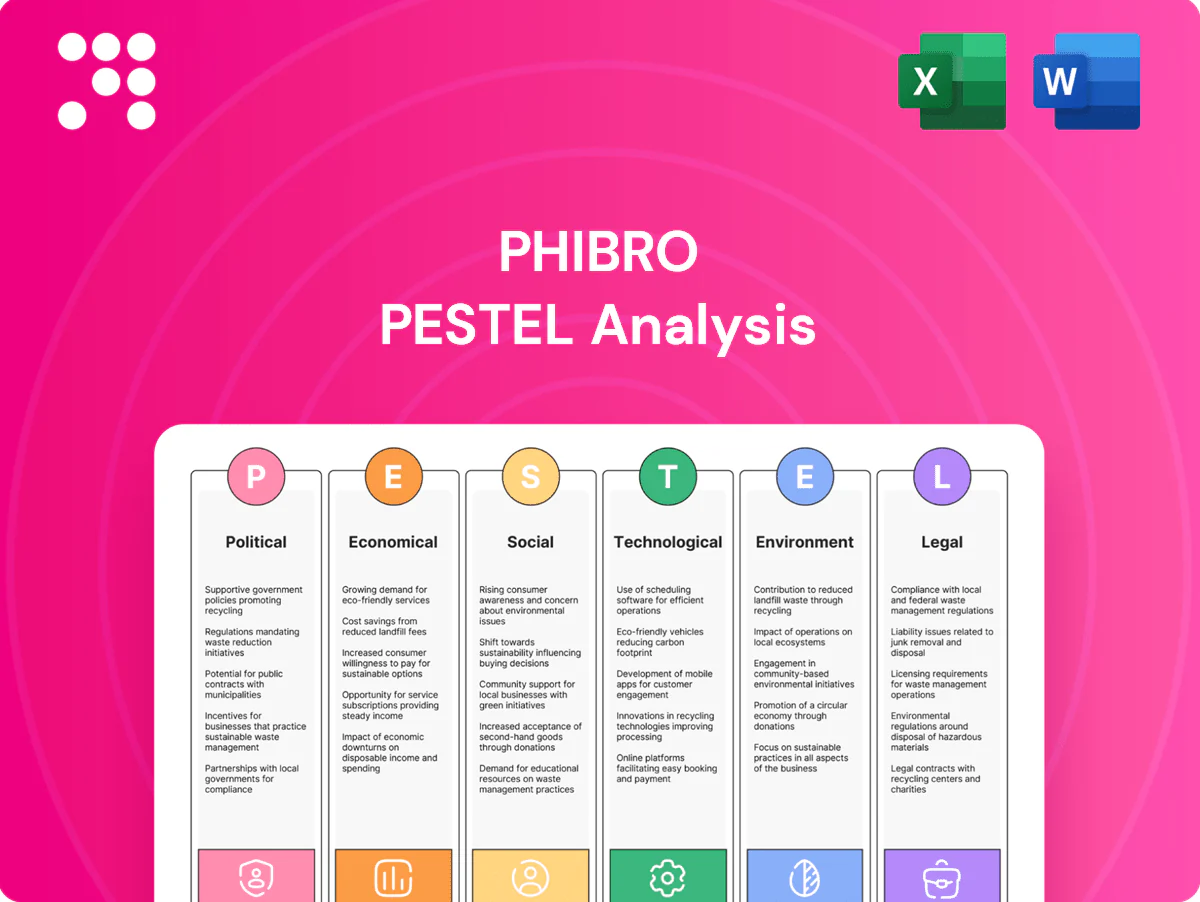

Phibro PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and environmental regulations are reshaping Phibro’s strategic outlook. Our concise PESTLE snapshot highlights key external risks and growth drivers you need to know. Ideal for investors and strategists, it points to actionable priorities. Purchase the full PESTLE for the complete, editable analysis and immediate insights.

Political factors

Regulatory oversight of animal health

National agricultural and veterinary agencies set approval, labeling and use standards for medicated feed additives and vaccines, with global animal health market size ~60 billion USD in 2024 highlighting stakes; policy shifts can accelerate or delay registrations, often extending timelines by 12–36 months. Harmonization gaps between the US, EU, Brazil, India and China add regulatory cost and time, so Phibro must sustain active regulatory affairs teams and local partnerships to navigate approvals.

Trade policies and tariffs

Tariffs on ingredients or finished products materially affect pricing and margins across borders, as seen in US tariffs of up to 25% on many Chinese imports since 2018 and WTO forecasts of only 1.7% merchandise trade volume growth in 2024. Export restrictions or sanitary barriers tied to disease outbreaks (eg, COVID-19 and avian influenza episodes) have repeatedly disrupted supply chains. Regional trade pacts like CPTPP (11 members) or USMCA can open or constrain access. Diversified sourcing and local manufacturing mitigate tariff exposure and supply shocks.

Subsidies and farm support programs

Government subsidies shape demand for livestock health inputs; OECD estimated global agricultural support near USD 700 billion in 2022. Policy incentives for biosecurity, vaccination and productivity (notably EU/US 2024 programs) raise uptake, while subsidy cuts tighten farm cash flow and lower spend. Phibro can align products with funded programs to sustain demand.

Geopolitical and biosecurity preparedness

Outbreak preparedness policies have driven stockpiling and vaccination campaigns, and WHO estimated a 2024 global health security funding gap of about 10.5 billion USD, sustaining demand for bulk APIs and adjuvants. Geopolitical tensions raise logistics delays, currency convertibility constraints and procurement risk, while public-private partnerships shape surveillance and response budgets; Phibro gains by integrating into national contingency plans, securing long‑term contracts.

- Stockpiles/vaccines — sustained volume demand

- Geopolitics — logistics, FX, procurement risk

- PPPs — direct funding to monitoring/response

- Phibro — embedded in national contingency procurement

Political stability in key markets

Political unrest can halt factory operations, impede field sales and undermine distributor reliability; stable governance, by contrast, strengthens contract enforcement and improves forecasting. Over 50 national elections in 2024 reset agriculture and food‑safety priorities, raising short‑term regulatory risk. A balanced country portfolio reduces revenue volatility for exporters and supply‑chain exposures.

- Risk: factory/distributor disruption

- Benefit: improved enforcement/forecasting

- Data: >50 national elections in 2024

- Mitigation: diversified country portfolio

Political shifts, >50 elections raise pricing and demand risk in ~60B USD animal-health market

Political shifts—regulatory timelines (often +12–36 months), tariffs (US up to 25% on some imports) and >50 elections in 2024—raise approval, pricing and demand risk for Phibro amid a ~60B USD 2024 global animal‑health market. Subsidies (~700B USD agricultural support 2022) and WHO’s 10.5B USD 2024 health security gap drive funded demand; trade growth was 1.7% in 2024. Diversified sourcing and local partnerships mitigate exposure.

| Metric | Value |

|---|---|

| Global market | ~60B USD (2024) |

| Agriculture support | ~700B USD (2022) |

| WHO funding gap | 10.5B USD (2024) |

What is included in the product

Explores how macro-environmental factors affect Phibro across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific examples; designed for executives, consultants and investors to identify risks, opportunities and support scenario planning and funding narratives.

A clean, summarized and visually segmented Phibro PESTLE for quick interpretation during meetings, easily droppable into slides, shareable across teams, and editable with notes for region- or business-specific context.

Economic factors

Livestock cycle and protein demand

Global meat production reached roughly 340 million tonnes in 2023 and aquaculture now supplies over 50% of fish for human consumption (FAO), underpinning demand for feed additives and vaccines. Herd expansions or contractions directly alter volumes for antibiotics, trace minerals and vaccines, creating short-run volatility. IMF projects emerging-market GDP growth near 4.3% in 2024, shifting diets toward animal protein. Phibro’s multi-species exposure (poultry, swine, ruminant, aquaculture) smooths cyclical swings.

Input cost inflation

Active ingredients, vitamins and excipients are highly sensitive to commodity and energy swings, with broad inflationary pressure—US CPI slowed to 3.4% in 2024—but input spikes in 2022–23 still echo through costs. Inflation compresses margins when selling prices lag procurement; industry reports cite multi-quarter lag effects. Long-term contracts and formulation flexibility mitigate volatility, while operational efficiency and procurement scale remain primary levers to protect margins.

FX fluctuations

Multi-currency revenue and cost bases expose Phibro earnings to exchange-rate swings, with the US dollar strengthening roughly 5% versus major currencies in 2024–mid‑2025, pressuring reported sales and competitiveness. Natural hedges from geographically matched revenues/costs and FX forwards/options have stabilized cash flows historically. Active pricing localization eases pass‑through in volatile markets, reducing margin erosion.

Farmer profitability and credit

Feed costs represent roughly 60-70% of livestock production costs, while volatile live-animal prices directly determine buyer purchasing power; constrained margins and tighter ag lending have reduced discretionary spend in 2024–25, shifting demand toward products with clear ROI and causing deferred purchases of nonessential supplements during downturns.

- Feed share: 60-70%

- Tight margins → ROI focus

- Supplements often deferred

- Proven payback boosts adoption

Market consolidation

Integrator consolidation in poultry and swine has increased buyer power; in the US the top four beef packers account for about 85% of processing (USDA 2023) and pork packing is concentrated at roughly two-thirds, driving larger integrators to demand compliance, traceability data and disciplined pricing from suppliers like Phibro.

- Consolidation: top-4 meatpackers ~85% beef, ~66% pork (USDA)

- Buyer demands: compliance, traceability, pricing discipline

- Distributor consolidation shifts channel terms

- Mitigation: strategic key-account management to secure share

Political shifts, >50 elections raise pricing and demand risk in ~60B USD animal-health market

Global meat production ~340m t (2023) and aquaculture >50% of fish supply underpin steady feed-additive demand; herd cycles create short-run volatility. Input costs remain sensitive to commodity/energy swings (US CPI 3.4% in 2024), compressing margins when prices lag. Consolidation (top-4 beef packers ~85%) raises buyer power, favoring suppliers with ROI-proven products.

| Metric | Value |

|---|---|

| Global meat (2023) | ~340m t |

| Aquaculture share | >50% |

| Feed cost share | 60–70% |

| US CPI (2024) | 3.4% |

| Top-4 beef packers | ~85% |

Full Version Awaits

Phibro PESTLE Analysis

The preview shown here is the exact Phibro PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is the real, finished file with no placeholders or surprises. After checkout you’ll instantly download this same professionally structured analysis.

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and environmental regulations are reshaping Phibro’s strategic outlook. Our concise PESTLE snapshot highlights key external risks and growth drivers you need to know. Ideal for investors and strategists, it points to actionable priorities. Purchase the full PESTLE for the complete, editable analysis and immediate insights.

Political factors

Regulatory oversight of animal health

National agricultural and veterinary agencies set approval, labeling and use standards for medicated feed additives and vaccines, with global animal health market size ~60 billion USD in 2024 highlighting stakes; policy shifts can accelerate or delay registrations, often extending timelines by 12–36 months. Harmonization gaps between the US, EU, Brazil, India and China add regulatory cost and time, so Phibro must sustain active regulatory affairs teams and local partnerships to navigate approvals.

Trade policies and tariffs

Tariffs on ingredients or finished products materially affect pricing and margins across borders, as seen in US tariffs of up to 25% on many Chinese imports since 2018 and WTO forecasts of only 1.7% merchandise trade volume growth in 2024. Export restrictions or sanitary barriers tied to disease outbreaks (eg, COVID-19 and avian influenza episodes) have repeatedly disrupted supply chains. Regional trade pacts like CPTPP (11 members) or USMCA can open or constrain access. Diversified sourcing and local manufacturing mitigate tariff exposure and supply shocks.

Subsidies and farm support programs

Government subsidies shape demand for livestock health inputs; OECD estimated global agricultural support near USD 700 billion in 2022. Policy incentives for biosecurity, vaccination and productivity (notably EU/US 2024 programs) raise uptake, while subsidy cuts tighten farm cash flow and lower spend. Phibro can align products with funded programs to sustain demand.

Geopolitical and biosecurity preparedness

Outbreak preparedness policies have driven stockpiling and vaccination campaigns, and WHO estimated a 2024 global health security funding gap of about 10.5 billion USD, sustaining demand for bulk APIs and adjuvants. Geopolitical tensions raise logistics delays, currency convertibility constraints and procurement risk, while public-private partnerships shape surveillance and response budgets; Phibro gains by integrating into national contingency plans, securing long‑term contracts.

- Stockpiles/vaccines — sustained volume demand

- Geopolitics — logistics, FX, procurement risk

- PPPs — direct funding to monitoring/response

- Phibro — embedded in national contingency procurement

Political stability in key markets

Political unrest can halt factory operations, impede field sales and undermine distributor reliability; stable governance, by contrast, strengthens contract enforcement and improves forecasting. Over 50 national elections in 2024 reset agriculture and food‑safety priorities, raising short‑term regulatory risk. A balanced country portfolio reduces revenue volatility for exporters and supply‑chain exposures.

- Risk: factory/distributor disruption

- Benefit: improved enforcement/forecasting

- Data: >50 national elections in 2024

- Mitigation: diversified country portfolio

Political shifts, >50 elections raise pricing and demand risk in ~60B USD animal-health market

Political shifts—regulatory timelines (often +12–36 months), tariffs (US up to 25% on some imports) and >50 elections in 2024—raise approval, pricing and demand risk for Phibro amid a ~60B USD 2024 global animal‑health market. Subsidies (~700B USD agricultural support 2022) and WHO’s 10.5B USD 2024 health security gap drive funded demand; trade growth was 1.7% in 2024. Diversified sourcing and local partnerships mitigate exposure.

| Metric | Value |

|---|---|

| Global market | ~60B USD (2024) |

| Agriculture support | ~700B USD (2022) |

| WHO funding gap | 10.5B USD (2024) |

What is included in the product

Explores how macro-environmental factors affect Phibro across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific examples; designed for executives, consultants and investors to identify risks, opportunities and support scenario planning and funding narratives.

A clean, summarized and visually segmented Phibro PESTLE for quick interpretation during meetings, easily droppable into slides, shareable across teams, and editable with notes for region- or business-specific context.

Economic factors

Livestock cycle and protein demand

Global meat production reached roughly 340 million tonnes in 2023 and aquaculture now supplies over 50% of fish for human consumption (FAO), underpinning demand for feed additives and vaccines. Herd expansions or contractions directly alter volumes for antibiotics, trace minerals and vaccines, creating short-run volatility. IMF projects emerging-market GDP growth near 4.3% in 2024, shifting diets toward animal protein. Phibro’s multi-species exposure (poultry, swine, ruminant, aquaculture) smooths cyclical swings.

Input cost inflation

Active ingredients, vitamins and excipients are highly sensitive to commodity and energy swings, with broad inflationary pressure—US CPI slowed to 3.4% in 2024—but input spikes in 2022–23 still echo through costs. Inflation compresses margins when selling prices lag procurement; industry reports cite multi-quarter lag effects. Long-term contracts and formulation flexibility mitigate volatility, while operational efficiency and procurement scale remain primary levers to protect margins.

FX fluctuations

Multi-currency revenue and cost bases expose Phibro earnings to exchange-rate swings, with the US dollar strengthening roughly 5% versus major currencies in 2024–mid‑2025, pressuring reported sales and competitiveness. Natural hedges from geographically matched revenues/costs and FX forwards/options have stabilized cash flows historically. Active pricing localization eases pass‑through in volatile markets, reducing margin erosion.

Farmer profitability and credit

Feed costs represent roughly 60-70% of livestock production costs, while volatile live-animal prices directly determine buyer purchasing power; constrained margins and tighter ag lending have reduced discretionary spend in 2024–25, shifting demand toward products with clear ROI and causing deferred purchases of nonessential supplements during downturns.

- Feed share: 60-70%

- Tight margins → ROI focus

- Supplements often deferred

- Proven payback boosts adoption

Market consolidation

Integrator consolidation in poultry and swine has increased buyer power; in the US the top four beef packers account for about 85% of processing (USDA 2023) and pork packing is concentrated at roughly two-thirds, driving larger integrators to demand compliance, traceability data and disciplined pricing from suppliers like Phibro.

- Consolidation: top-4 meatpackers ~85% beef, ~66% pork (USDA)

- Buyer demands: compliance, traceability, pricing discipline

- Distributor consolidation shifts channel terms

- Mitigation: strategic key-account management to secure share

Political shifts, >50 elections raise pricing and demand risk in ~60B USD animal-health market

Global meat production ~340m t (2023) and aquaculture >50% of fish supply underpin steady feed-additive demand; herd cycles create short-run volatility. Input costs remain sensitive to commodity/energy swings (US CPI 3.4% in 2024), compressing margins when prices lag. Consolidation (top-4 beef packers ~85%) raises buyer power, favoring suppliers with ROI-proven products.

| Metric | Value |

|---|---|

| Global meat (2023) | ~340m t |

| Aquaculture share | >50% |

| Feed cost share | 60–70% |

| US CPI (2024) | 3.4% |

| Top-4 beef packers | ~85% |

Full Version Awaits

Phibro PESTLE Analysis

The preview shown here is the exact Phibro PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is the real, finished file with no placeholders or surprises. After checkout you’ll instantly download this same professionally structured analysis.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and environmental regulations are reshaping Phibro’s strategic outlook. Our concise PESTLE snapshot highlights key external risks and growth drivers you need to know. Ideal for investors and strategists, it points to actionable priorities. Purchase the full PESTLE for the complete, editable analysis and immediate insights.

Political factors

Regulatory oversight of animal health

National agricultural and veterinary agencies set approval, labeling and use standards for medicated feed additives and vaccines, with global animal health market size ~60 billion USD in 2024 highlighting stakes; policy shifts can accelerate or delay registrations, often extending timelines by 12–36 months. Harmonization gaps between the US, EU, Brazil, India and China add regulatory cost and time, so Phibro must sustain active regulatory affairs teams and local partnerships to navigate approvals.

Trade policies and tariffs

Tariffs on ingredients or finished products materially affect pricing and margins across borders, as seen in US tariffs of up to 25% on many Chinese imports since 2018 and WTO forecasts of only 1.7% merchandise trade volume growth in 2024. Export restrictions or sanitary barriers tied to disease outbreaks (eg, COVID-19 and avian influenza episodes) have repeatedly disrupted supply chains. Regional trade pacts like CPTPP (11 members) or USMCA can open or constrain access. Diversified sourcing and local manufacturing mitigate tariff exposure and supply shocks.

Subsidies and farm support programs

Government subsidies shape demand for livestock health inputs; OECD estimated global agricultural support near USD 700 billion in 2022. Policy incentives for biosecurity, vaccination and productivity (notably EU/US 2024 programs) raise uptake, while subsidy cuts tighten farm cash flow and lower spend. Phibro can align products with funded programs to sustain demand.

Geopolitical and biosecurity preparedness

Outbreak preparedness policies have driven stockpiling and vaccination campaigns, and WHO estimated a 2024 global health security funding gap of about 10.5 billion USD, sustaining demand for bulk APIs and adjuvants. Geopolitical tensions raise logistics delays, currency convertibility constraints and procurement risk, while public-private partnerships shape surveillance and response budgets; Phibro gains by integrating into national contingency plans, securing long‑term contracts.

- Stockpiles/vaccines — sustained volume demand

- Geopolitics — logistics, FX, procurement risk

- PPPs — direct funding to monitoring/response

- Phibro — embedded in national contingency procurement

Political stability in key markets

Political unrest can halt factory operations, impede field sales and undermine distributor reliability; stable governance, by contrast, strengthens contract enforcement and improves forecasting. Over 50 national elections in 2024 reset agriculture and food‑safety priorities, raising short‑term regulatory risk. A balanced country portfolio reduces revenue volatility for exporters and supply‑chain exposures.

- Risk: factory/distributor disruption

- Benefit: improved enforcement/forecasting

- Data: >50 national elections in 2024

- Mitigation: diversified country portfolio

Political shifts, >50 elections raise pricing and demand risk in ~60B USD animal-health market

Political shifts—regulatory timelines (often +12–36 months), tariffs (US up to 25% on some imports) and >50 elections in 2024—raise approval, pricing and demand risk for Phibro amid a ~60B USD 2024 global animal‑health market. Subsidies (~700B USD agricultural support 2022) and WHO’s 10.5B USD 2024 health security gap drive funded demand; trade growth was 1.7% in 2024. Diversified sourcing and local partnerships mitigate exposure.

| Metric | Value |

|---|---|

| Global market | ~60B USD (2024) |

| Agriculture support | ~700B USD (2022) |

| WHO funding gap | 10.5B USD (2024) |

What is included in the product

Explores how macro-environmental factors affect Phibro across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific examples; designed for executives, consultants and investors to identify risks, opportunities and support scenario planning and funding narratives.

A clean, summarized and visually segmented Phibro PESTLE for quick interpretation during meetings, easily droppable into slides, shareable across teams, and editable with notes for region- or business-specific context.

Economic factors

Livestock cycle and protein demand

Global meat production reached roughly 340 million tonnes in 2023 and aquaculture now supplies over 50% of fish for human consumption (FAO), underpinning demand for feed additives and vaccines. Herd expansions or contractions directly alter volumes for antibiotics, trace minerals and vaccines, creating short-run volatility. IMF projects emerging-market GDP growth near 4.3% in 2024, shifting diets toward animal protein. Phibro’s multi-species exposure (poultry, swine, ruminant, aquaculture) smooths cyclical swings.

Input cost inflation

Active ingredients, vitamins and excipients are highly sensitive to commodity and energy swings, with broad inflationary pressure—US CPI slowed to 3.4% in 2024—but input spikes in 2022–23 still echo through costs. Inflation compresses margins when selling prices lag procurement; industry reports cite multi-quarter lag effects. Long-term contracts and formulation flexibility mitigate volatility, while operational efficiency and procurement scale remain primary levers to protect margins.

FX fluctuations

Multi-currency revenue and cost bases expose Phibro earnings to exchange-rate swings, with the US dollar strengthening roughly 5% versus major currencies in 2024–mid‑2025, pressuring reported sales and competitiveness. Natural hedges from geographically matched revenues/costs and FX forwards/options have stabilized cash flows historically. Active pricing localization eases pass‑through in volatile markets, reducing margin erosion.

Farmer profitability and credit

Feed costs represent roughly 60-70% of livestock production costs, while volatile live-animal prices directly determine buyer purchasing power; constrained margins and tighter ag lending have reduced discretionary spend in 2024–25, shifting demand toward products with clear ROI and causing deferred purchases of nonessential supplements during downturns.

- Feed share: 60-70%

- Tight margins → ROI focus

- Supplements often deferred

- Proven payback boosts adoption

Market consolidation

Integrator consolidation in poultry and swine has increased buyer power; in the US the top four beef packers account for about 85% of processing (USDA 2023) and pork packing is concentrated at roughly two-thirds, driving larger integrators to demand compliance, traceability data and disciplined pricing from suppliers like Phibro.

- Consolidation: top-4 meatpackers ~85% beef, ~66% pork (USDA)

- Buyer demands: compliance, traceability, pricing discipline

- Distributor consolidation shifts channel terms

- Mitigation: strategic key-account management to secure share

Political shifts, >50 elections raise pricing and demand risk in ~60B USD animal-health market

Global meat production ~340m t (2023) and aquaculture >50% of fish supply underpin steady feed-additive demand; herd cycles create short-run volatility. Input costs remain sensitive to commodity/energy swings (US CPI 3.4% in 2024), compressing margins when prices lag. Consolidation (top-4 beef packers ~85%) raises buyer power, favoring suppliers with ROI-proven products.

| Metric | Value |

|---|---|

| Global meat (2023) | ~340m t |

| Aquaculture share | >50% |

| Feed cost share | 60–70% |

| US CPI (2024) | 3.4% |

| Top-4 beef packers | ~85% |

Full Version Awaits

Phibro PESTLE Analysis

The preview shown here is the exact Phibro PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is the real, finished file with no placeholders or surprises. After checkout you’ll instantly download this same professionally structured analysis.