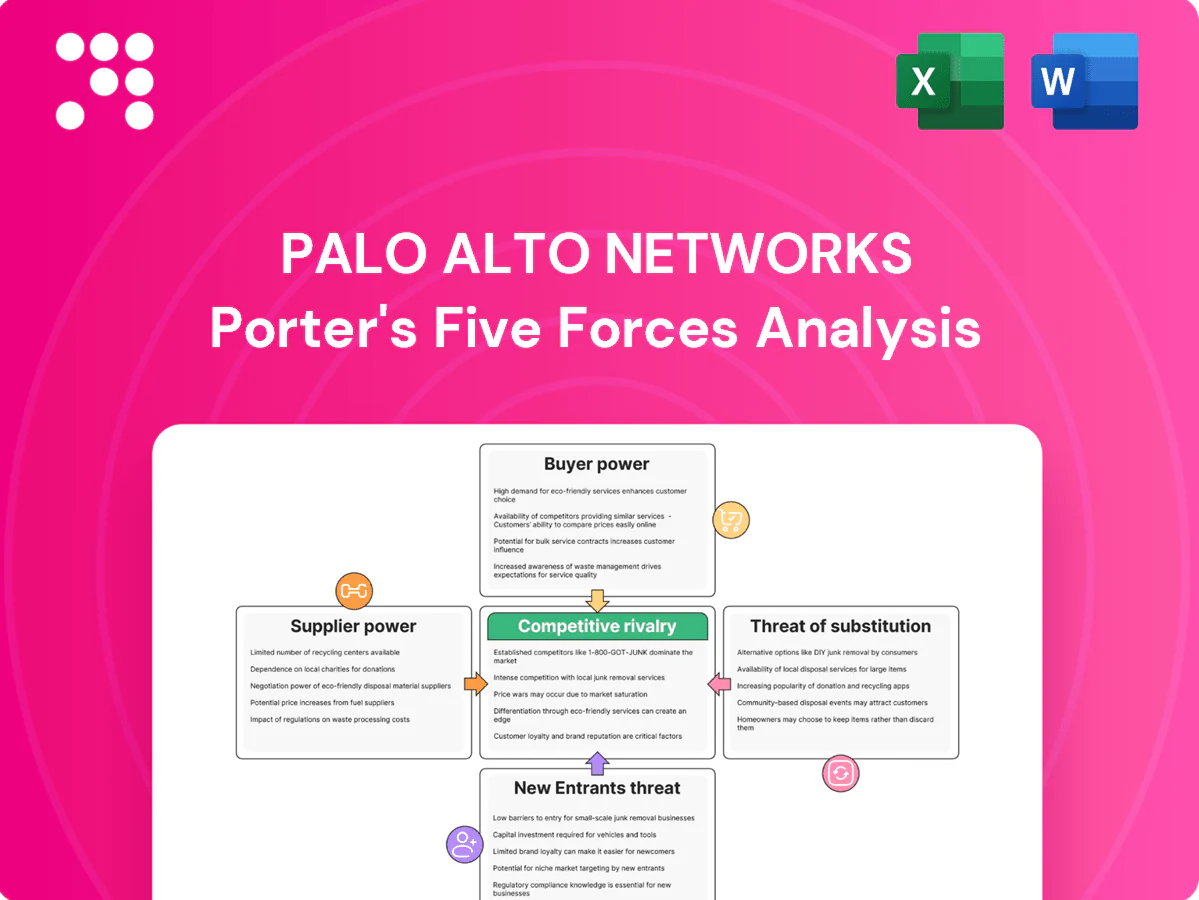

Palo Alto Networks Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Palo Alto Networks faces intense rivalry from established cybersecurity firms, significant buyer power from large enterprises, moderate supplier leverage, rising threats from cloud-native entrants, and evolving substitutes like integrated platform security.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Palo Alto Networks’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated silicon and hardware OEMs

Firewall appliances depend on a concentrated set of network silicon suppliers such as Broadcom and Intel and a handful of OEM contract manufacturers, which gives those suppliers leverage over cost and lead times. Supply-chain disruptions historically have delayed deliveries and pressured gross margins. Palo Alto reduces risk through multi-sourcing, modular design and long-term volume commitments, but switching core silicon suppliers remains slow and costly.

Hyperscaler dependencies for cloud security

Prisma and Palo Alto cloud-delivered services rely on AWS, Azure and GCP infrastructure and marketplaces. Hyperscalers (2024 shares ~AWS 32%, Microsoft 23%, Google 10% = ~65% combined) can control pricing, listing terms and egress fees (up to ~$0.09/GB), impacting margins. Co-selling boosts reach but raises platform dependency risk; architectural portability and multicloud deployment reduce single-platform leverage against Palo Alto, which reported $5.62B revenue in FY2024.

Critical software and threat intel feeds

Signature databases, sandboxing engines, and third-party data enrichments are core to detection quality, and reliance on licensed IP or specialized analytics raises supplier bargaining power. Palo Alto Networks reported fiscal 2024 revenue of 6.91 billion and offsets supplier risk via its Unit 42 threat-intel team and internal ML models. Contract diversification and multiple feed sources further reduce vendor lock-in.

Skilled cybersecurity talent as a supplier

Expert cybersecurity engineers and researchers are scarce—ISC2 estimated a 3.4 million global workforce gap in 2024—so they command premium compensation (BLS May 2023 median for information security analysts was $102,600). Tight labor markets increase supplier power over wages and retention; remote work widens the talent pool but intensifies global competition, while strong culture and equity-based incentives help contain churn.

- Scarcity: 3.4M global gap (ISC2, 2024)

- Pay pressure: median $102,600 (BLS, May 2023)

- Remote work: broader pool, higher competition

- Retention: culture + equity reduce churn

Channel distribution and MSSP partners

Channel resellers and MSSPs shape market access and deal velocity, often driving enterprise adoption. Strong partners can negotiate favorable margins and co-op marketing funds, increasing supplier leverage. Palo Alto mitigates dependence through direct enterprise relationships, platform bundling and enablement/certification programs that align incentives, supporting FY2024 revenue of $6.96 billion.

- Partner-driven access

- Margin pressure

- Direct sales & bundling

- Enablement/certs

Supplier power moderate-high: hyperscalers ~65%, egress $0.09/GB, talent gap 3.4M

Supplier power is moderate to high: concentrated silicon OEMs and hyperscalers (combined ~65% share in 2024) can pressure cost, lead times and egress fees (~$0.09/GB), while Palo Alto (FY2024 revenue $6.96B) mitigates via multi-sourcing, modular design and multicloud portability. Detection feeds and scarce talent (3.4M gap, ISC2 2024) add bargaining pressure but diversification and internal R&D reduce dependence.

| Supplier | Metric | Value |

|---|---|---|

| Hyperscalers | Market share (2024) | AWS 32% / MSFT 23% / GCP 10% (~65%) |

| Palo Alto | FY2024 revenue | $6.96B |

| Talent | Workforce gap (2024) | 3.4M (ISC2) |

| Egress fees | Max | ~$0.09/GB |

What is included in the product

Concise Porter's Five Forces assessment of Palo Alto Networks, detailing competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and key disruptive trends shaping its cybersecurity market position.

One-sheet Porter's Five Forces for Palo Alto Networks—instantly visualize competitive pressure with an editable spider chart, customize inputs for evolving threats or opportunities, and drop directly into decks for fast strategic decisions.

Customers Bargaining Power

Large enterprises and governments with RFP leverage

Large enterprises and governments run formal RFPs that pit vendors head-to-head, demanding discounts and strict SLAs; multi-year, high-ACV deals (often >$1M) in 2024 further amplify buyer leverage. Compliance and certification requirements (FedRAMP, FIPS, SOC 2) shape contractual terms and procurement windows. Strong referenceability and documented ROI can narrow concessions, letting Palo Alto preserve pricing and margin.

Platform consolidation pressures pricing

Customers pushing to reduce tool sprawl across network, cloud and SOC increase willingness to consolidate, concentrating spend and extracting bundle discounts; Palo Alto Networks reported FY2024 revenue of about 6.9 billion, reflecting scale that supports package deals. Consolidation raises switching but gives Palo Alto scope to win larger share by conceding price. Demonstrable integration value across Prisma, Cortex and NGFW tempers buyer power.

High but surmountable switching costs

Policy migration, retraining and potential downtime make switching Palo Alto Networks non-trivial for enterprises, raising customer bargaining costs. Standardized protocols and migration tools (APIs, automation) have lowered barriers, enabling competitors to win deals. Buyers exploit alternatives to negotiate better commercial terms, while sticky subscriptions and managed services—accounting for over 70% of FY2024 revenue—help sustain net revenue retention above 115% in 2024.

Outcome-based expectations and ROI proof

Security buyers demand measurable risk reduction, fewer breaches, and operational efficiency; proof-of-value trials and pilots are now routine and poor pilot outcomes increase buyer leverage. Strong telemetry and extensive case studies defend Palo Alto Networks pricing; Palo Alto reported FY2024 revenue of about $6.9 billion and roughly 94,000 customers, strengthening its evidence base.

- Measurable outcomes required

- Proof-of-value common

- Underperformance increases buyer power

- Telemetry and case studies defend pricing

Market transparency and peer influence

Analyst reports, benchmarks and community reviews heighten buyer visibility into Palo Alto Networks offerings; Palo Alto exceeded $7 billion revenue in FY2024 and serves over 90,000 customers, providing ample comparison data. Peer CISO networks shape shortlists and pricing expectations, while transparent reference deals can anchor discounts. Differentiated features and enterprise support (Cortex, Prisma integrations) offset pure price focus.

- analytics

- benchmarks

- peer-influence

- reference-deals

- product-differentiation

Scale — revenue 6.9B, ~94,000 customers, > 70% subs, NRR > 115% sustain pricing power

Customers exert strong leverage via RFPs, consolidation and proof-of-value trials, forcing discounts and strict SLAs; large multi-year deals (>1M) amplify this. Palo Alto's FY2024 scale (revenue 6.9B, ~94,000 customers) plus >70% subscription mix and NRR >115% limit concessions and sustain pricing power.

| Metric | 2024 |

|---|---|

| Revenue | 6.9B |

| Customers | ~94,000 |

| Subscription % | >70% |

| NRR | >115% |

Full Version Awaits

Palo Alto Networks Porter's Five Forces Analysis

This preview displays the full Palo Alto Networks Porter's Five Forces analysis you'll receive—no placeholders or excerpts. It covers competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry with actionable insights. Once purchased, the exact same professionally formatted file is available for immediate download.

A Must-Have Tool for Decision-Makers

Palo Alto Networks faces intense rivalry from established cybersecurity firms, significant buyer power from large enterprises, moderate supplier leverage, rising threats from cloud-native entrants, and evolving substitutes like integrated platform security.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Palo Alto Networks’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated silicon and hardware OEMs

Firewall appliances depend on a concentrated set of network silicon suppliers such as Broadcom and Intel and a handful of OEM contract manufacturers, which gives those suppliers leverage over cost and lead times. Supply-chain disruptions historically have delayed deliveries and pressured gross margins. Palo Alto reduces risk through multi-sourcing, modular design and long-term volume commitments, but switching core silicon suppliers remains slow and costly.

Hyperscaler dependencies for cloud security

Prisma and Palo Alto cloud-delivered services rely on AWS, Azure and GCP infrastructure and marketplaces. Hyperscalers (2024 shares ~AWS 32%, Microsoft 23%, Google 10% = ~65% combined) can control pricing, listing terms and egress fees (up to ~$0.09/GB), impacting margins. Co-selling boosts reach but raises platform dependency risk; architectural portability and multicloud deployment reduce single-platform leverage against Palo Alto, which reported $5.62B revenue in FY2024.

Critical software and threat intel feeds

Signature databases, sandboxing engines, and third-party data enrichments are core to detection quality, and reliance on licensed IP or specialized analytics raises supplier bargaining power. Palo Alto Networks reported fiscal 2024 revenue of 6.91 billion and offsets supplier risk via its Unit 42 threat-intel team and internal ML models. Contract diversification and multiple feed sources further reduce vendor lock-in.

Skilled cybersecurity talent as a supplier

Expert cybersecurity engineers and researchers are scarce—ISC2 estimated a 3.4 million global workforce gap in 2024—so they command premium compensation (BLS May 2023 median for information security analysts was $102,600). Tight labor markets increase supplier power over wages and retention; remote work widens the talent pool but intensifies global competition, while strong culture and equity-based incentives help contain churn.

- Scarcity: 3.4M global gap (ISC2, 2024)

- Pay pressure: median $102,600 (BLS, May 2023)

- Remote work: broader pool, higher competition

- Retention: culture + equity reduce churn

Channel distribution and MSSP partners

Channel resellers and MSSPs shape market access and deal velocity, often driving enterprise adoption. Strong partners can negotiate favorable margins and co-op marketing funds, increasing supplier leverage. Palo Alto mitigates dependence through direct enterprise relationships, platform bundling and enablement/certification programs that align incentives, supporting FY2024 revenue of $6.96 billion.

- Partner-driven access

- Margin pressure

- Direct sales & bundling

- Enablement/certs

Supplier power moderate-high: hyperscalers ~65%, egress $0.09/GB, talent gap 3.4M

Supplier power is moderate to high: concentrated silicon OEMs and hyperscalers (combined ~65% share in 2024) can pressure cost, lead times and egress fees (~$0.09/GB), while Palo Alto (FY2024 revenue $6.96B) mitigates via multi-sourcing, modular design and multicloud portability. Detection feeds and scarce talent (3.4M gap, ISC2 2024) add bargaining pressure but diversification and internal R&D reduce dependence.

| Supplier | Metric | Value |

|---|---|---|

| Hyperscalers | Market share (2024) | AWS 32% / MSFT 23% / GCP 10% (~65%) |

| Palo Alto | FY2024 revenue | $6.96B |

| Talent | Workforce gap (2024) | 3.4M (ISC2) |

| Egress fees | Max | ~$0.09/GB |

What is included in the product

Concise Porter's Five Forces assessment of Palo Alto Networks, detailing competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and key disruptive trends shaping its cybersecurity market position.

One-sheet Porter's Five Forces for Palo Alto Networks—instantly visualize competitive pressure with an editable spider chart, customize inputs for evolving threats or opportunities, and drop directly into decks for fast strategic decisions.

Customers Bargaining Power

Large enterprises and governments with RFP leverage

Large enterprises and governments run formal RFPs that pit vendors head-to-head, demanding discounts and strict SLAs; multi-year, high-ACV deals (often >$1M) in 2024 further amplify buyer leverage. Compliance and certification requirements (FedRAMP, FIPS, SOC 2) shape contractual terms and procurement windows. Strong referenceability and documented ROI can narrow concessions, letting Palo Alto preserve pricing and margin.

Platform consolidation pressures pricing

Customers pushing to reduce tool sprawl across network, cloud and SOC increase willingness to consolidate, concentrating spend and extracting bundle discounts; Palo Alto Networks reported FY2024 revenue of about 6.9 billion, reflecting scale that supports package deals. Consolidation raises switching but gives Palo Alto scope to win larger share by conceding price. Demonstrable integration value across Prisma, Cortex and NGFW tempers buyer power.

High but surmountable switching costs

Policy migration, retraining and potential downtime make switching Palo Alto Networks non-trivial for enterprises, raising customer bargaining costs. Standardized protocols and migration tools (APIs, automation) have lowered barriers, enabling competitors to win deals. Buyers exploit alternatives to negotiate better commercial terms, while sticky subscriptions and managed services—accounting for over 70% of FY2024 revenue—help sustain net revenue retention above 115% in 2024.

Outcome-based expectations and ROI proof

Security buyers demand measurable risk reduction, fewer breaches, and operational efficiency; proof-of-value trials and pilots are now routine and poor pilot outcomes increase buyer leverage. Strong telemetry and extensive case studies defend Palo Alto Networks pricing; Palo Alto reported FY2024 revenue of about $6.9 billion and roughly 94,000 customers, strengthening its evidence base.

- Measurable outcomes required

- Proof-of-value common

- Underperformance increases buyer power

- Telemetry and case studies defend pricing

Market transparency and peer influence

Analyst reports, benchmarks and community reviews heighten buyer visibility into Palo Alto Networks offerings; Palo Alto exceeded $7 billion revenue in FY2024 and serves over 90,000 customers, providing ample comparison data. Peer CISO networks shape shortlists and pricing expectations, while transparent reference deals can anchor discounts. Differentiated features and enterprise support (Cortex, Prisma integrations) offset pure price focus.

- analytics

- benchmarks

- peer-influence

- reference-deals

- product-differentiation

Scale — revenue 6.9B, ~94,000 customers, > 70% subs, NRR > 115% sustain pricing power

Customers exert strong leverage via RFPs, consolidation and proof-of-value trials, forcing discounts and strict SLAs; large multi-year deals (>1M) amplify this. Palo Alto's FY2024 scale (revenue 6.9B, ~94,000 customers) plus >70% subscription mix and NRR >115% limit concessions and sustain pricing power.

| Metric | 2024 |

|---|---|

| Revenue | 6.9B |

| Customers | ~94,000 |

| Subscription % | >70% |

| NRR | >115% |

Full Version Awaits

Palo Alto Networks Porter's Five Forces Analysis

This preview displays the full Palo Alto Networks Porter's Five Forces analysis you'll receive—no placeholders or excerpts. It covers competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry with actionable insights. Once purchased, the exact same professionally formatted file is available for immediate download.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Palo Alto Networks faces intense rivalry from established cybersecurity firms, significant buyer power from large enterprises, moderate supplier leverage, rising threats from cloud-native entrants, and evolving substitutes like integrated platform security.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Palo Alto Networks’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated silicon and hardware OEMs

Firewall appliances depend on a concentrated set of network silicon suppliers such as Broadcom and Intel and a handful of OEM contract manufacturers, which gives those suppliers leverage over cost and lead times. Supply-chain disruptions historically have delayed deliveries and pressured gross margins. Palo Alto reduces risk through multi-sourcing, modular design and long-term volume commitments, but switching core silicon suppliers remains slow and costly.

Hyperscaler dependencies for cloud security

Prisma and Palo Alto cloud-delivered services rely on AWS, Azure and GCP infrastructure and marketplaces. Hyperscalers (2024 shares ~AWS 32%, Microsoft 23%, Google 10% = ~65% combined) can control pricing, listing terms and egress fees (up to ~$0.09/GB), impacting margins. Co-selling boosts reach but raises platform dependency risk; architectural portability and multicloud deployment reduce single-platform leverage against Palo Alto, which reported $5.62B revenue in FY2024.

Critical software and threat intel feeds

Signature databases, sandboxing engines, and third-party data enrichments are core to detection quality, and reliance on licensed IP or specialized analytics raises supplier bargaining power. Palo Alto Networks reported fiscal 2024 revenue of 6.91 billion and offsets supplier risk via its Unit 42 threat-intel team and internal ML models. Contract diversification and multiple feed sources further reduce vendor lock-in.

Skilled cybersecurity talent as a supplier

Expert cybersecurity engineers and researchers are scarce—ISC2 estimated a 3.4 million global workforce gap in 2024—so they command premium compensation (BLS May 2023 median for information security analysts was $102,600). Tight labor markets increase supplier power over wages and retention; remote work widens the talent pool but intensifies global competition, while strong culture and equity-based incentives help contain churn.

- Scarcity: 3.4M global gap (ISC2, 2024)

- Pay pressure: median $102,600 (BLS, May 2023)

- Remote work: broader pool, higher competition

- Retention: culture + equity reduce churn

Channel distribution and MSSP partners

Channel resellers and MSSPs shape market access and deal velocity, often driving enterprise adoption. Strong partners can negotiate favorable margins and co-op marketing funds, increasing supplier leverage. Palo Alto mitigates dependence through direct enterprise relationships, platform bundling and enablement/certification programs that align incentives, supporting FY2024 revenue of $6.96 billion.

- Partner-driven access

- Margin pressure

- Direct sales & bundling

- Enablement/certs

Supplier power moderate-high: hyperscalers ~65%, egress $0.09/GB, talent gap 3.4M

Supplier power is moderate to high: concentrated silicon OEMs and hyperscalers (combined ~65% share in 2024) can pressure cost, lead times and egress fees (~$0.09/GB), while Palo Alto (FY2024 revenue $6.96B) mitigates via multi-sourcing, modular design and multicloud portability. Detection feeds and scarce talent (3.4M gap, ISC2 2024) add bargaining pressure but diversification and internal R&D reduce dependence.

| Supplier | Metric | Value |

|---|---|---|

| Hyperscalers | Market share (2024) | AWS 32% / MSFT 23% / GCP 10% (~65%) |

| Palo Alto | FY2024 revenue | $6.96B |

| Talent | Workforce gap (2024) | 3.4M (ISC2) |

| Egress fees | Max | ~$0.09/GB |

What is included in the product

Concise Porter's Five Forces assessment of Palo Alto Networks, detailing competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and key disruptive trends shaping its cybersecurity market position.

One-sheet Porter's Five Forces for Palo Alto Networks—instantly visualize competitive pressure with an editable spider chart, customize inputs for evolving threats or opportunities, and drop directly into decks for fast strategic decisions.

Customers Bargaining Power

Large enterprises and governments with RFP leverage

Large enterprises and governments run formal RFPs that pit vendors head-to-head, demanding discounts and strict SLAs; multi-year, high-ACV deals (often >$1M) in 2024 further amplify buyer leverage. Compliance and certification requirements (FedRAMP, FIPS, SOC 2) shape contractual terms and procurement windows. Strong referenceability and documented ROI can narrow concessions, letting Palo Alto preserve pricing and margin.

Platform consolidation pressures pricing

Customers pushing to reduce tool sprawl across network, cloud and SOC increase willingness to consolidate, concentrating spend and extracting bundle discounts; Palo Alto Networks reported FY2024 revenue of about 6.9 billion, reflecting scale that supports package deals. Consolidation raises switching but gives Palo Alto scope to win larger share by conceding price. Demonstrable integration value across Prisma, Cortex and NGFW tempers buyer power.

High but surmountable switching costs

Policy migration, retraining and potential downtime make switching Palo Alto Networks non-trivial for enterprises, raising customer bargaining costs. Standardized protocols and migration tools (APIs, automation) have lowered barriers, enabling competitors to win deals. Buyers exploit alternatives to negotiate better commercial terms, while sticky subscriptions and managed services—accounting for over 70% of FY2024 revenue—help sustain net revenue retention above 115% in 2024.

Outcome-based expectations and ROI proof

Security buyers demand measurable risk reduction, fewer breaches, and operational efficiency; proof-of-value trials and pilots are now routine and poor pilot outcomes increase buyer leverage. Strong telemetry and extensive case studies defend Palo Alto Networks pricing; Palo Alto reported FY2024 revenue of about $6.9 billion and roughly 94,000 customers, strengthening its evidence base.

- Measurable outcomes required

- Proof-of-value common

- Underperformance increases buyer power

- Telemetry and case studies defend pricing

Market transparency and peer influence

Analyst reports, benchmarks and community reviews heighten buyer visibility into Palo Alto Networks offerings; Palo Alto exceeded $7 billion revenue in FY2024 and serves over 90,000 customers, providing ample comparison data. Peer CISO networks shape shortlists and pricing expectations, while transparent reference deals can anchor discounts. Differentiated features and enterprise support (Cortex, Prisma integrations) offset pure price focus.

- analytics

- benchmarks

- peer-influence

- reference-deals

- product-differentiation

Scale — revenue 6.9B, ~94,000 customers, > 70% subs, NRR > 115% sustain pricing power

Customers exert strong leverage via RFPs, consolidation and proof-of-value trials, forcing discounts and strict SLAs; large multi-year deals (>1M) amplify this. Palo Alto's FY2024 scale (revenue 6.9B, ~94,000 customers) plus >70% subscription mix and NRR >115% limit concessions and sustain pricing power.

| Metric | 2024 |

|---|---|

| Revenue | 6.9B |

| Customers | ~94,000 |

| Subscription % | >70% |

| NRR | >115% |

Full Version Awaits

Palo Alto Networks Porter's Five Forces Analysis

This preview displays the full Palo Alto Networks Porter's Five Forces analysis you'll receive—no placeholders or excerpts. It covers competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry with actionable insights. Once purchased, the exact same professionally formatted file is available for immediate download.