Pampa Energía PESTLE Analysis

Skip the Research. Get the Strategy.

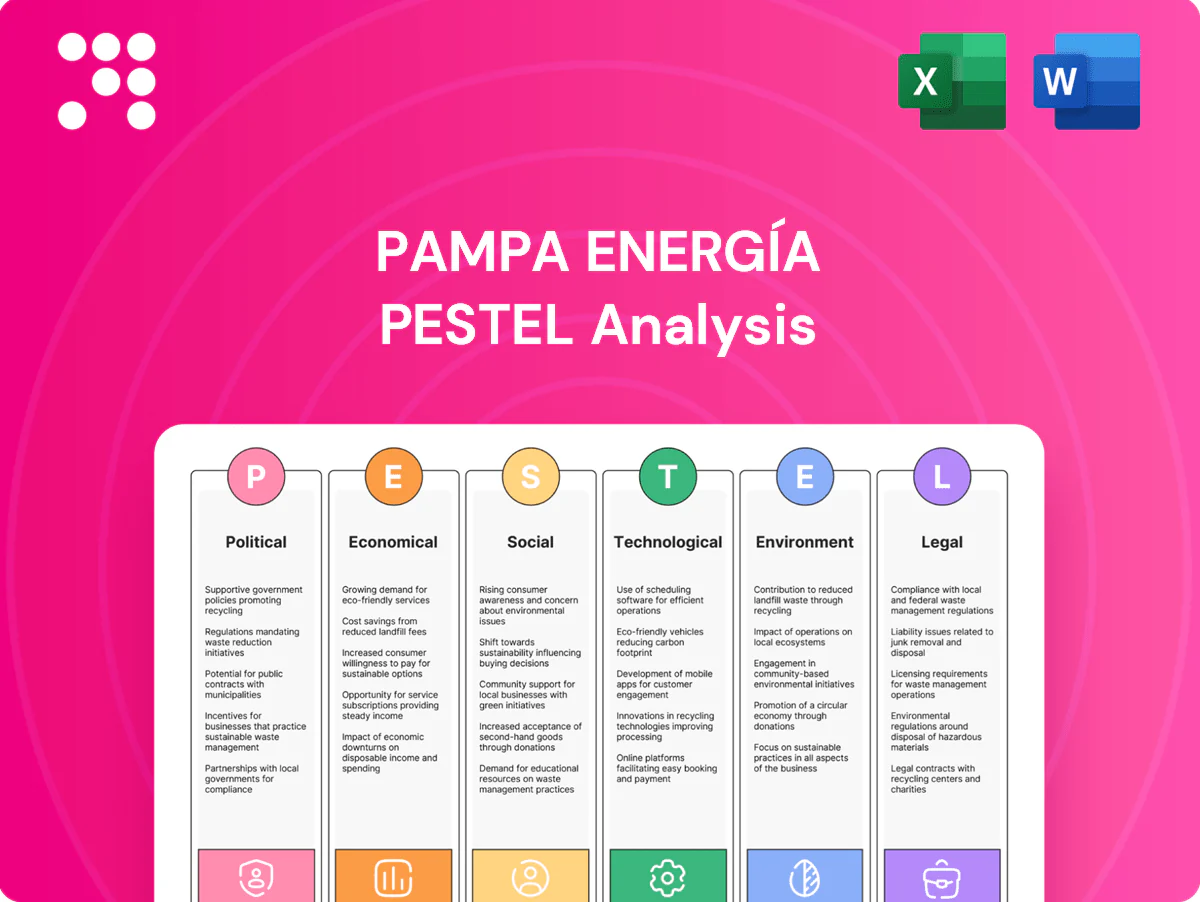

Gain a strategic advantage with our Pampa Energía PESTLE: concise, actionable insight into political, economic, social, technological, legal and environmental forces shaping the company’s trajectory. Ideal for investors and strategists, this fully researched report saves hours of work. Purchase the full analysis to access detailed risks, opportunities and ready-to-use slides and spreadsheets.

Political factors

Tariff and subsidy regime volatility

Argentine administrations frequently adjust electricity and gas tariffs and subsidies, eroding Pampa Energía’s revenue visibility and making near-term cash flows harder to forecast. Sudden freezes or hikes have historically swung operating cash and capex planning within quarters, pressuring investment timing and debt service. Policy reversals between affordability and fiscal consolidation remain a core operational and financial risk, requiring close monitoring of budget dynamics and social considerations.

Regulatory oversight and state involvement

Agencies ENRE and ENARGAS set tariff formulas, service quality standards and investment obligations that directly affect Pampa Energía’s cash flow and capex recovery; compliance is central given Pampa is Argentina’s largest private power generator with diversified thermal and hydro assets.

State influence in transmission and distribution, notably via Transener and provincial utilities, can compress returns and delay projects through access rules and compensation timelines.

Regulatory resets after elections are common—post‑2023 adjustments altered tariff review timetables—so sustained constructive engagement reduces approval and compliance risks.

Federal–provincial dynamics and resource control

Provinces hold constitutional control over upstream hydrocarbons, setting royalties, permits and local-content rules that materially affect Pampa Energía project economics. Alignment (or mismatch) between federal energy targets and provincial priorities influences development pace in basins like Vaca Muerta, which supplied over 50% of Argentina’s natural gas in 2024. Municipal approvals add unpredictable timeline layers and costs. Comprehensive stakeholder mapping across federal, provincial and municipal jurisdictions is therefore critical.

Capital controls and FX repatriation policies

Political decisions on capital controls determine Pampa Energía’s dollar access for debt service and imported turbines; FX rationing has historically delayed dividend remittances and equipment procurement, forcing months-long deferrals.

Policy liberalization or tightening produces immediate operational impacts on cashflow and project timelines, making hedging and onshore financing strategic levers to manage FX volatility and allocation risk.

- capital-controls: affect dollar access for debt and imports

- fx-rationing: delays dividends and equipment procurement

- policy-shifts: immediate operational and cashflow impact

- risk-mitigation: hedging and onshore financing essential

Energy transition policy signals

- Target: ~20% renewables by 2025

- Gas as transition: policy support to 2030

- Auctions/incentives: intermittent since 2022

- Net‑zero discourse: 2050 horizon

Policy shifts and capital controls squeeze energy cash flow; Vaca Muerta >50%, renewables ~20%

Frequent tariff/subsidy shifts reduce revenue visibility and compress near‑term cash flow; ENRE/ENARGAS decisions directly affect capex recovery. Provincial control over royalties and permits shapes project economics—Vaca Muerta supplied >50% of Argentina’s gas in 2024. Capital controls limit dollar access for debt/imports, delaying payments. Renewables target ~20% of power by 2025, guiding mid‑term allocation.

| Metric | 2024/25 |

|---|---|

| Vaca Muerta gas share | >50% |

| Renewables target | ~20% by 2025 |

What is included in the product

Explores how macro-environmental factors uniquely affect Pampa Energía across Political, Economic, Social, Technological, Environmental and Legal dimensions, combining data-driven trends and region-specific regulatory context to surface risks and opportunities for executives and investors; includes forward-looking insights to support scenario planning and strategic decision-making.

Provides a concise, PESTLE‑segmented summary of Pampa Energía’s external risks and opportunities that can be dropped into presentations or strategy sessions for quick alignment across teams.

Economic factors

High inflation and cost indexation

Chronic inflation in Argentina (annual CPI above 200% in 2024 per INDEC) sharply raises Pampa Energía’s opex and capex while eroding ARS-denominated revenues, forcing frequent tariff reviews. Indexation clauses and periodic tariff updates are vital to protect margins and cash flow. Working capital needs swell as price levels accelerate, and procurement strategies must prioritize multi-year contracts and FX hedges to lock predictable costs.

Currency depreciation and balance sheet risk

ARS depreciation has raised the peso cost of servicing Pampa Energía’s USD-denominated debt and importing equipment, with the peso losing roughly half its value vs the dollar between 2023–mid‑2025, intensifying FX translation and cash‑flow strain. Dollar‑linked inputs vs peso‑earned power and fuel revenues create currency mismatches that squeeze margins. Access to hard‑currency liquidity and export FX bolsters resilience, while USD‑linked upstream prices provide a natural hedge by lifting dollar cash inflows.

Commodity price cycles (oil and gas)

Global oil and gas prices (Brent ~86 USD/bbl in 2024; Henry Hub ~3.9 USD/MMBtu in 2024) drive upstream cash flow and investment appetite for Pampa Energía. Domestic price caps and regulated gas tariffs in Argentina can decouple local realizations from those international benchmarks. Seasonal gas demand peaks amplify price and supply volatility. A balanced portfolio across power generation and E&P smooths this cyclicality.

Economic activity and electricity demand

Industrial output and household consumption remain the primary drivers of load growth and capacity needs for Pampa Energía, with downturns lowering demand and collections while recoveries compress reserve margins.

Demand shows material sensitivity to tariff adjustments, so volume elasticity to price changes is a key risk for revenues and system utilization.

Under Argentina’s high macro volatility, forecast accuracy for demand and peak shaving is essential for dispatch planning and capital allocation.

- Drivers: industrial output, household consumption

- Risks: recessions → lower demand/collections

- Recovery impact: tighter reserve margins

- Tariff elasticity: affects volumes/revenues

- Priority: robust demand forecasting

Cost of capital and sovereign risk

Argentina’s elevated country risk raises Pampa Energía’s funding costs and limits tenor, pushing reliance on higher-yield local debt and shorter maturities; inflation remained ~100%+ in 2023–24, sustaining risk premia. Multilateral lenders and export-credit agencies (World Bank, IDB, ECA) bridge infrastructure gaps. Macro stabilization would compress spreads and unlock projects. Flexible capital structure preserves resilience.

Policy shifts and capital controls squeeze energy cash flow; Vaca Muerta >50%, renewables ~20%

Chronic inflation (CPI >200% in 2024 per INDEC) and ~50% ARS depreciation vs USD (2023–mid‑2025) squeeze margins, raise opex/capex and swell working capital; indexation and FX hedges are essential. Global benchmarks (Brent ~86 USD/bbl, Henry Hub ~3.9 USD/MMBtu in 2024) drive E&P cash flow but domestic tariffs can decouple realizations. High country risk keeps spreads wide; multilaterals partially fill gaps.

| Metric | Value |

|---|---|

| Inflation 2024 (INDEC) | >200% |

| ARS change 2023–mid‑2025 | ~‑50% |

| Brent 2024 | ~86 USD/bbl |

| Henry Hub 2024 | ~3.9 USD/MMBtu |

Preview Before You Purchase

Pampa Energía PESTLE Analysis

This Pampa Energía PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted and ready to use. It delivers political, economic, social, technological, legal and environmental insights specific to Pampa Energía with actionable implications for strategy and investment. No placeholders or surprises: the file shown is the final version available for immediate download.

Skip the Research. Get the Strategy.

Gain a strategic advantage with our Pampa Energía PESTLE: concise, actionable insight into political, economic, social, technological, legal and environmental forces shaping the company’s trajectory. Ideal for investors and strategists, this fully researched report saves hours of work. Purchase the full analysis to access detailed risks, opportunities and ready-to-use slides and spreadsheets.

Political factors

Tariff and subsidy regime volatility

Argentine administrations frequently adjust electricity and gas tariffs and subsidies, eroding Pampa Energía’s revenue visibility and making near-term cash flows harder to forecast. Sudden freezes or hikes have historically swung operating cash and capex planning within quarters, pressuring investment timing and debt service. Policy reversals between affordability and fiscal consolidation remain a core operational and financial risk, requiring close monitoring of budget dynamics and social considerations.

Regulatory oversight and state involvement

Agencies ENRE and ENARGAS set tariff formulas, service quality standards and investment obligations that directly affect Pampa Energía’s cash flow and capex recovery; compliance is central given Pampa is Argentina’s largest private power generator with diversified thermal and hydro assets.

State influence in transmission and distribution, notably via Transener and provincial utilities, can compress returns and delay projects through access rules and compensation timelines.

Regulatory resets after elections are common—post‑2023 adjustments altered tariff review timetables—so sustained constructive engagement reduces approval and compliance risks.

Federal–provincial dynamics and resource control

Provinces hold constitutional control over upstream hydrocarbons, setting royalties, permits and local-content rules that materially affect Pampa Energía project economics. Alignment (or mismatch) between federal energy targets and provincial priorities influences development pace in basins like Vaca Muerta, which supplied over 50% of Argentina’s natural gas in 2024. Municipal approvals add unpredictable timeline layers and costs. Comprehensive stakeholder mapping across federal, provincial and municipal jurisdictions is therefore critical.

Capital controls and FX repatriation policies

Political decisions on capital controls determine Pampa Energía’s dollar access for debt service and imported turbines; FX rationing has historically delayed dividend remittances and equipment procurement, forcing months-long deferrals.

Policy liberalization or tightening produces immediate operational impacts on cashflow and project timelines, making hedging and onshore financing strategic levers to manage FX volatility and allocation risk.

- capital-controls: affect dollar access for debt and imports

- fx-rationing: delays dividends and equipment procurement

- policy-shifts: immediate operational and cashflow impact

- risk-mitigation: hedging and onshore financing essential

Energy transition policy signals

- Target: ~20% renewables by 2025

- Gas as transition: policy support to 2030

- Auctions/incentives: intermittent since 2022

- Net‑zero discourse: 2050 horizon

Policy shifts and capital controls squeeze energy cash flow; Vaca Muerta >50%, renewables ~20%

Frequent tariff/subsidy shifts reduce revenue visibility and compress near‑term cash flow; ENRE/ENARGAS decisions directly affect capex recovery. Provincial control over royalties and permits shapes project economics—Vaca Muerta supplied >50% of Argentina’s gas in 2024. Capital controls limit dollar access for debt/imports, delaying payments. Renewables target ~20% of power by 2025, guiding mid‑term allocation.

| Metric | 2024/25 |

|---|---|

| Vaca Muerta gas share | >50% |

| Renewables target | ~20% by 2025 |

What is included in the product

Explores how macro-environmental factors uniquely affect Pampa Energía across Political, Economic, Social, Technological, Environmental and Legal dimensions, combining data-driven trends and region-specific regulatory context to surface risks and opportunities for executives and investors; includes forward-looking insights to support scenario planning and strategic decision-making.

Provides a concise, PESTLE‑segmented summary of Pampa Energía’s external risks and opportunities that can be dropped into presentations or strategy sessions for quick alignment across teams.

Economic factors

High inflation and cost indexation

Chronic inflation in Argentina (annual CPI above 200% in 2024 per INDEC) sharply raises Pampa Energía’s opex and capex while eroding ARS-denominated revenues, forcing frequent tariff reviews. Indexation clauses and periodic tariff updates are vital to protect margins and cash flow. Working capital needs swell as price levels accelerate, and procurement strategies must prioritize multi-year contracts and FX hedges to lock predictable costs.

Currency depreciation and balance sheet risk

ARS depreciation has raised the peso cost of servicing Pampa Energía’s USD-denominated debt and importing equipment, with the peso losing roughly half its value vs the dollar between 2023–mid‑2025, intensifying FX translation and cash‑flow strain. Dollar‑linked inputs vs peso‑earned power and fuel revenues create currency mismatches that squeeze margins. Access to hard‑currency liquidity and export FX bolsters resilience, while USD‑linked upstream prices provide a natural hedge by lifting dollar cash inflows.

Commodity price cycles (oil and gas)

Global oil and gas prices (Brent ~86 USD/bbl in 2024; Henry Hub ~3.9 USD/MMBtu in 2024) drive upstream cash flow and investment appetite for Pampa Energía. Domestic price caps and regulated gas tariffs in Argentina can decouple local realizations from those international benchmarks. Seasonal gas demand peaks amplify price and supply volatility. A balanced portfolio across power generation and E&P smooths this cyclicality.

Economic activity and electricity demand

Industrial output and household consumption remain the primary drivers of load growth and capacity needs for Pampa Energía, with downturns lowering demand and collections while recoveries compress reserve margins.

Demand shows material sensitivity to tariff adjustments, so volume elasticity to price changes is a key risk for revenues and system utilization.

Under Argentina’s high macro volatility, forecast accuracy for demand and peak shaving is essential for dispatch planning and capital allocation.

- Drivers: industrial output, household consumption

- Risks: recessions → lower demand/collections

- Recovery impact: tighter reserve margins

- Tariff elasticity: affects volumes/revenues

- Priority: robust demand forecasting

Cost of capital and sovereign risk

Argentina’s elevated country risk raises Pampa Energía’s funding costs and limits tenor, pushing reliance on higher-yield local debt and shorter maturities; inflation remained ~100%+ in 2023–24, sustaining risk premia. Multilateral lenders and export-credit agencies (World Bank, IDB, ECA) bridge infrastructure gaps. Macro stabilization would compress spreads and unlock projects. Flexible capital structure preserves resilience.

Policy shifts and capital controls squeeze energy cash flow; Vaca Muerta >50%, renewables ~20%

Chronic inflation (CPI >200% in 2024 per INDEC) and ~50% ARS depreciation vs USD (2023–mid‑2025) squeeze margins, raise opex/capex and swell working capital; indexation and FX hedges are essential. Global benchmarks (Brent ~86 USD/bbl, Henry Hub ~3.9 USD/MMBtu in 2024) drive E&P cash flow but domestic tariffs can decouple realizations. High country risk keeps spreads wide; multilaterals partially fill gaps.

| Metric | Value |

|---|---|

| Inflation 2024 (INDEC) | >200% |

| ARS change 2023–mid‑2025 | ~‑50% |

| Brent 2024 | ~86 USD/bbl |

| Henry Hub 2024 | ~3.9 USD/MMBtu |

Preview Before You Purchase

Pampa Energía PESTLE Analysis

This Pampa Energía PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted and ready to use. It delivers political, economic, social, technological, legal and environmental insights specific to Pampa Energía with actionable implications for strategy and investment. No placeholders or surprises: the file shown is the final version available for immediate download.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Gain a strategic advantage with our Pampa Energía PESTLE: concise, actionable insight into political, economic, social, technological, legal and environmental forces shaping the company’s trajectory. Ideal for investors and strategists, this fully researched report saves hours of work. Purchase the full analysis to access detailed risks, opportunities and ready-to-use slides and spreadsheets.

Political factors

Tariff and subsidy regime volatility

Argentine administrations frequently adjust electricity and gas tariffs and subsidies, eroding Pampa Energía’s revenue visibility and making near-term cash flows harder to forecast. Sudden freezes or hikes have historically swung operating cash and capex planning within quarters, pressuring investment timing and debt service. Policy reversals between affordability and fiscal consolidation remain a core operational and financial risk, requiring close monitoring of budget dynamics and social considerations.

Regulatory oversight and state involvement

Agencies ENRE and ENARGAS set tariff formulas, service quality standards and investment obligations that directly affect Pampa Energía’s cash flow and capex recovery; compliance is central given Pampa is Argentina’s largest private power generator with diversified thermal and hydro assets.

State influence in transmission and distribution, notably via Transener and provincial utilities, can compress returns and delay projects through access rules and compensation timelines.

Regulatory resets after elections are common—post‑2023 adjustments altered tariff review timetables—so sustained constructive engagement reduces approval and compliance risks.

Federal–provincial dynamics and resource control

Provinces hold constitutional control over upstream hydrocarbons, setting royalties, permits and local-content rules that materially affect Pampa Energía project economics. Alignment (or mismatch) between federal energy targets and provincial priorities influences development pace in basins like Vaca Muerta, which supplied over 50% of Argentina’s natural gas in 2024. Municipal approvals add unpredictable timeline layers and costs. Comprehensive stakeholder mapping across federal, provincial and municipal jurisdictions is therefore critical.

Capital controls and FX repatriation policies

Political decisions on capital controls determine Pampa Energía’s dollar access for debt service and imported turbines; FX rationing has historically delayed dividend remittances and equipment procurement, forcing months-long deferrals.

Policy liberalization or tightening produces immediate operational impacts on cashflow and project timelines, making hedging and onshore financing strategic levers to manage FX volatility and allocation risk.

- capital-controls: affect dollar access for debt and imports

- fx-rationing: delays dividends and equipment procurement

- policy-shifts: immediate operational and cashflow impact

- risk-mitigation: hedging and onshore financing essential

Energy transition policy signals

- Target: ~20% renewables by 2025

- Gas as transition: policy support to 2030

- Auctions/incentives: intermittent since 2022

- Net‑zero discourse: 2050 horizon

Policy shifts and capital controls squeeze energy cash flow; Vaca Muerta >50%, renewables ~20%

Frequent tariff/subsidy shifts reduce revenue visibility and compress near‑term cash flow; ENRE/ENARGAS decisions directly affect capex recovery. Provincial control over royalties and permits shapes project economics—Vaca Muerta supplied >50% of Argentina’s gas in 2024. Capital controls limit dollar access for debt/imports, delaying payments. Renewables target ~20% of power by 2025, guiding mid‑term allocation.

| Metric | 2024/25 |

|---|---|

| Vaca Muerta gas share | >50% |

| Renewables target | ~20% by 2025 |

What is included in the product

Explores how macro-environmental factors uniquely affect Pampa Energía across Political, Economic, Social, Technological, Environmental and Legal dimensions, combining data-driven trends and region-specific regulatory context to surface risks and opportunities for executives and investors; includes forward-looking insights to support scenario planning and strategic decision-making.

Provides a concise, PESTLE‑segmented summary of Pampa Energía’s external risks and opportunities that can be dropped into presentations or strategy sessions for quick alignment across teams.

Economic factors

High inflation and cost indexation

Chronic inflation in Argentina (annual CPI above 200% in 2024 per INDEC) sharply raises Pampa Energía’s opex and capex while eroding ARS-denominated revenues, forcing frequent tariff reviews. Indexation clauses and periodic tariff updates are vital to protect margins and cash flow. Working capital needs swell as price levels accelerate, and procurement strategies must prioritize multi-year contracts and FX hedges to lock predictable costs.

Currency depreciation and balance sheet risk

ARS depreciation has raised the peso cost of servicing Pampa Energía’s USD-denominated debt and importing equipment, with the peso losing roughly half its value vs the dollar between 2023–mid‑2025, intensifying FX translation and cash‑flow strain. Dollar‑linked inputs vs peso‑earned power and fuel revenues create currency mismatches that squeeze margins. Access to hard‑currency liquidity and export FX bolsters resilience, while USD‑linked upstream prices provide a natural hedge by lifting dollar cash inflows.

Commodity price cycles (oil and gas)

Global oil and gas prices (Brent ~86 USD/bbl in 2024; Henry Hub ~3.9 USD/MMBtu in 2024) drive upstream cash flow and investment appetite for Pampa Energía. Domestic price caps and regulated gas tariffs in Argentina can decouple local realizations from those international benchmarks. Seasonal gas demand peaks amplify price and supply volatility. A balanced portfolio across power generation and E&P smooths this cyclicality.

Economic activity and electricity demand

Industrial output and household consumption remain the primary drivers of load growth and capacity needs for Pampa Energía, with downturns lowering demand and collections while recoveries compress reserve margins.

Demand shows material sensitivity to tariff adjustments, so volume elasticity to price changes is a key risk for revenues and system utilization.

Under Argentina’s high macro volatility, forecast accuracy for demand and peak shaving is essential for dispatch planning and capital allocation.

- Drivers: industrial output, household consumption

- Risks: recessions → lower demand/collections

- Recovery impact: tighter reserve margins

- Tariff elasticity: affects volumes/revenues

- Priority: robust demand forecasting

Cost of capital and sovereign risk

Argentina’s elevated country risk raises Pampa Energía’s funding costs and limits tenor, pushing reliance on higher-yield local debt and shorter maturities; inflation remained ~100%+ in 2023–24, sustaining risk premia. Multilateral lenders and export-credit agencies (World Bank, IDB, ECA) bridge infrastructure gaps. Macro stabilization would compress spreads and unlock projects. Flexible capital structure preserves resilience.

Policy shifts and capital controls squeeze energy cash flow; Vaca Muerta >50%, renewables ~20%

Chronic inflation (CPI >200% in 2024 per INDEC) and ~50% ARS depreciation vs USD (2023–mid‑2025) squeeze margins, raise opex/capex and swell working capital; indexation and FX hedges are essential. Global benchmarks (Brent ~86 USD/bbl, Henry Hub ~3.9 USD/MMBtu in 2024) drive E&P cash flow but domestic tariffs can decouple realizations. High country risk keeps spreads wide; multilaterals partially fill gaps.

| Metric | Value |

|---|---|

| Inflation 2024 (INDEC) | >200% |

| ARS change 2023–mid‑2025 | ~‑50% |

| Brent 2024 | ~86 USD/bbl |

| Henry Hub 2024 | ~3.9 USD/MMBtu |

Preview Before You Purchase

Pampa Energía PESTLE Analysis

This Pampa Energía PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted and ready to use. It delivers political, economic, social, technological, legal and environmental insights specific to Pampa Energía with actionable implications for strategy and investment. No placeholders or surprises: the file shown is the final version available for immediate download.