Panda Restaurant Group SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

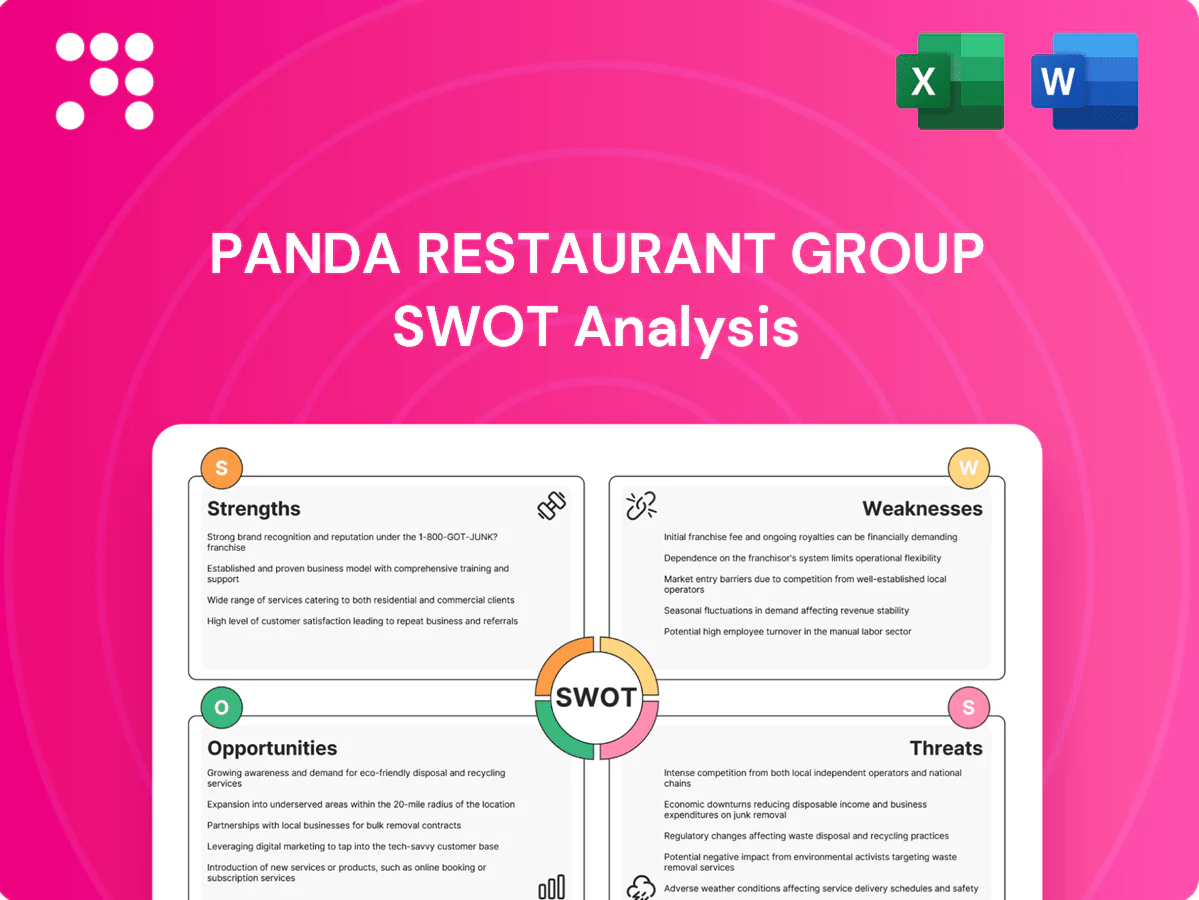

Panda Restaurant Group blends strong brand recognition and a scalable franchise model with menu innovation, while facing rising labor & commodity costs and fierce fast‑casual competition. Want the full story behind strengths, risks, and growth drivers? Purchase the complete SWOT analysis for a professionally written, editable report ideal for strategic planning and investment.

Strengths

Largest American Chinese chain

Panda Express, the largest American Chinese chain with over 2,200 U.S. restaurants, holds clear category leadership that drives strong brand recall and higher store traffic. Its scale yields purchasing power and marketing efficiency, supporting faster rollouts of menu and digital initiatives. Market dominance also provides landlord leverage for prime sites and drive-thru placements, creating a high barrier for smaller rivals.

Operational consistency at scale

Standardized recipes, wok-cooking processes and rigorous training deliver predictable quality across Panda's network of over 2,200 restaurants, supporting consistent dish execution and speed of service. Centralized supply partnerships and a streamlined menu reduce complexity and waste, improving margins and inventory turns. Reliable execution drives high throughput, stronger unit economics and repeat visitation rates.

Multi-format portfolio

Panda Restaurant Group spans fast-casual to full-service through Panda Express (over 2,200 locations), legacy Panda Inn (founded 1973) and newer Hibachi-San (launched 2021), allowing targeting of varied occasions, check sizes and real estate types. This multi-format portfolio helps balance cyclical dining shifts and enables cross-learning in menu R&D and service models.

Strong culture and private ownership

Founder-led stewardship by Andrew and Peggy Cherng (founded 1983) and a values-driven culture enable long-term decisions; private, family ownership allows reinvestment without quarterly pressures. Structured training and career pathways raise retention and service quality, aligning staff and leadership to enhance execution and brand reputation.

- Founder-led

- Private ownership

- Long-term reinvestment

- Employee development

Real estate and drive-thru footprint

Panda Restaurant Group operates more than 2,300 restaurants worldwide as of 2024, leveraging site-selection expertise to expand stand-alone and drive-thru units beyond malls. Drive-thrus increase convenience, strengthen sales resilience and grow off-premise mix; diverse locations capture lunch, dinner and impulse traffic, enabling format- and market-level growth.

- >2,300 restaurants (2024)

- Drive-thru expansion boosts off-premise sales

- Stand-alone sites extend beyond malls

- Covers multiple dayparts and impulse visits

Leading U.S. American-Chinese chain with >2,300 restaurants and scale-driven margins

Panda Express leads U.S. American Chinese with >2,300 restaurants (2024), strong brand recall and scale-driven purchasing and marketing advantages. Standardized wok-cooking, centralized supply and rigorous training deliver consistent quality, speed and better unit economics. Family ownership enables long-term reinvestment and rapid drive-thru/stand-alone expansion.

| Metric | Value |

|---|---|

| Restaurants (2024) | >2,300 |

| Founded | 1983 |

| Formats | Panda Express, Panda Inn, Hibachi-San |

| Ownership | Private, Cherng family |

What is included in the product

Delivers a strategic overview of Panda Restaurant Group’s internal and external business factors, highlighting strengths, weaknesses, opportunities, and threats shaping its growth, operational resilience, and competitive position.

Provides a focused SWOT matrix highlighting Panda Restaurant Group's strengths, weaknesses, opportunities, and threats for rapid strategy alignment and faster executive decision-making.

Weaknesses

Menu perceived as Americanized

Heavy reliance on American-Chinese staples limits appeal to authenticity-seeking diners and narrows flavor profiles versus broader Asian cuisines. This perception can suppress willingness to pay premium prices in select markets. As the largest Chinese fast-casual chain in the U.S. with over 2,400 locations, it faces higher barriers for international adoption without localization.

Health and nutrition concerns

Fried items and sugar-laden sauces at Panda Express, with several entrées exceeding 1,000 mg sodium per serving, deter health-conscious consumers as US average sodium intake is ~3,400 mg/day (CDC). About 65% of adults report trying to eat healthier, so perceptions clash with wellness trends. Limited low-calorie or specialty-diet options can reduce visit frequency and cap addressable occasions and corporate catering wins despite over 2,400 US locations (2024).

High labor intensity

High labor intensity at Panda — driven by wok cooking and peak-service staffing — requires skilled hires and training, tying into industry labor costs that typically run 30–35% of sales (National Restaurant Association). Higher wage pressure (food prep/serving average hourly wage $15.07, BLS May 2024) raises operating costs and turnover sensitivity. Staffing gaps produce execution variance and complicate rapid new-unit rollouts.

Capital-heavy company-operated model

Owning the majority of its more than 2,400 restaurants (2024) concentrates CAPEX and operating risk on Panda, raising exposure to same-store volatility. Growth pace depends on internal capital and execution bandwidth rather than franchising, limiting asset-light scalability. Limited franchising increases exposure to localized downturns and slows capital-efficient expansion.

- High CAPEX concentration

- Growth tied to internal capital

- Low asset-light scalability

- Greater local downturn exposure

U.S.-centric revenue base

Panda Restaurant Group's revenue is primarily U.S.-centric, tying performance closely to domestic economic cycles and consumer spending swings. Limited international penetration reduces currency and market diversification, leaving growth dependent on a single macro environment. Regional saturation raises cannibalization risk and heightens sensitivity to U.S. labor, wage and real estate cost pressures.

- U.S.-centric exposure

- Low currency/market diversification

- Regional saturation → cannibalization

- Higher macroeconomic sensitivity

High-sodium menu and high labor costs threaten appeal vs 2,400+ US outlets

Heavy reliance on American-Chinese staples and limited authentic/menu diversity constrains upscale appeal; over 2,400 US locations (2024) also hinder easy international adoption. Menu health issues—several entrées >1,000 mg sodium—clash with ~65% of adults trying to eat healthier and US avg sodium 3,400 mg/day (CDC). High labor intensity raises costs amid industry labor at 30–35% of sales and avg food service wage $15.07 (BLS May 2024).

| Metric | Value (source) |

|---|---|

| US locations | >2,400 (2024) |

| Entrées sodium | several >1,000 mg (menu data) |

| US avg sodium | 3,400 mg/day (CDC) |

| Adults trying healthier | ~65% (survey) |

| Labor % of sales | 30–35% (Natl Restaurant Assoc) |

| Avg wage (food prep) | $15.07/hr (BLS May 2024) |

Same Document Delivered

Panda Restaurant Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The content is ready to use and becomes available immediately after checkout.

Elevate Your Analysis with the Complete SWOT Report

Panda Restaurant Group blends strong brand recognition and a scalable franchise model with menu innovation, while facing rising labor & commodity costs and fierce fast‑casual competition. Want the full story behind strengths, risks, and growth drivers? Purchase the complete SWOT analysis for a professionally written, editable report ideal for strategic planning and investment.

Strengths

Largest American Chinese chain

Panda Express, the largest American Chinese chain with over 2,200 U.S. restaurants, holds clear category leadership that drives strong brand recall and higher store traffic. Its scale yields purchasing power and marketing efficiency, supporting faster rollouts of menu and digital initiatives. Market dominance also provides landlord leverage for prime sites and drive-thru placements, creating a high barrier for smaller rivals.

Operational consistency at scale

Standardized recipes, wok-cooking processes and rigorous training deliver predictable quality across Panda's network of over 2,200 restaurants, supporting consistent dish execution and speed of service. Centralized supply partnerships and a streamlined menu reduce complexity and waste, improving margins and inventory turns. Reliable execution drives high throughput, stronger unit economics and repeat visitation rates.

Multi-format portfolio

Panda Restaurant Group spans fast-casual to full-service through Panda Express (over 2,200 locations), legacy Panda Inn (founded 1973) and newer Hibachi-San (launched 2021), allowing targeting of varied occasions, check sizes and real estate types. This multi-format portfolio helps balance cyclical dining shifts and enables cross-learning in menu R&D and service models.

Strong culture and private ownership

Founder-led stewardship by Andrew and Peggy Cherng (founded 1983) and a values-driven culture enable long-term decisions; private, family ownership allows reinvestment without quarterly pressures. Structured training and career pathways raise retention and service quality, aligning staff and leadership to enhance execution and brand reputation.

- Founder-led

- Private ownership

- Long-term reinvestment

- Employee development

Real estate and drive-thru footprint

Panda Restaurant Group operates more than 2,300 restaurants worldwide as of 2024, leveraging site-selection expertise to expand stand-alone and drive-thru units beyond malls. Drive-thrus increase convenience, strengthen sales resilience and grow off-premise mix; diverse locations capture lunch, dinner and impulse traffic, enabling format- and market-level growth.

- >2,300 restaurants (2024)

- Drive-thru expansion boosts off-premise sales

- Stand-alone sites extend beyond malls

- Covers multiple dayparts and impulse visits

Leading U.S. American-Chinese chain with >2,300 restaurants and scale-driven margins

Panda Express leads U.S. American Chinese with >2,300 restaurants (2024), strong brand recall and scale-driven purchasing and marketing advantages. Standardized wok-cooking, centralized supply and rigorous training deliver consistent quality, speed and better unit economics. Family ownership enables long-term reinvestment and rapid drive-thru/stand-alone expansion.

| Metric | Value |

|---|---|

| Restaurants (2024) | >2,300 |

| Founded | 1983 |

| Formats | Panda Express, Panda Inn, Hibachi-San |

| Ownership | Private, Cherng family |

What is included in the product

Delivers a strategic overview of Panda Restaurant Group’s internal and external business factors, highlighting strengths, weaknesses, opportunities, and threats shaping its growth, operational resilience, and competitive position.

Provides a focused SWOT matrix highlighting Panda Restaurant Group's strengths, weaknesses, opportunities, and threats for rapid strategy alignment and faster executive decision-making.

Weaknesses

Menu perceived as Americanized

Heavy reliance on American-Chinese staples limits appeal to authenticity-seeking diners and narrows flavor profiles versus broader Asian cuisines. This perception can suppress willingness to pay premium prices in select markets. As the largest Chinese fast-casual chain in the U.S. with over 2,400 locations, it faces higher barriers for international adoption without localization.

Health and nutrition concerns

Fried items and sugar-laden sauces at Panda Express, with several entrées exceeding 1,000 mg sodium per serving, deter health-conscious consumers as US average sodium intake is ~3,400 mg/day (CDC). About 65% of adults report trying to eat healthier, so perceptions clash with wellness trends. Limited low-calorie or specialty-diet options can reduce visit frequency and cap addressable occasions and corporate catering wins despite over 2,400 US locations (2024).

High labor intensity

High labor intensity at Panda — driven by wok cooking and peak-service staffing — requires skilled hires and training, tying into industry labor costs that typically run 30–35% of sales (National Restaurant Association). Higher wage pressure (food prep/serving average hourly wage $15.07, BLS May 2024) raises operating costs and turnover sensitivity. Staffing gaps produce execution variance and complicate rapid new-unit rollouts.

Capital-heavy company-operated model

Owning the majority of its more than 2,400 restaurants (2024) concentrates CAPEX and operating risk on Panda, raising exposure to same-store volatility. Growth pace depends on internal capital and execution bandwidth rather than franchising, limiting asset-light scalability. Limited franchising increases exposure to localized downturns and slows capital-efficient expansion.

- High CAPEX concentration

- Growth tied to internal capital

- Low asset-light scalability

- Greater local downturn exposure

U.S.-centric revenue base

Panda Restaurant Group's revenue is primarily U.S.-centric, tying performance closely to domestic economic cycles and consumer spending swings. Limited international penetration reduces currency and market diversification, leaving growth dependent on a single macro environment. Regional saturation raises cannibalization risk and heightens sensitivity to U.S. labor, wage and real estate cost pressures.

- U.S.-centric exposure

- Low currency/market diversification

- Regional saturation → cannibalization

- Higher macroeconomic sensitivity

High-sodium menu and high labor costs threaten appeal vs 2,400+ US outlets

Heavy reliance on American-Chinese staples and limited authentic/menu diversity constrains upscale appeal; over 2,400 US locations (2024) also hinder easy international adoption. Menu health issues—several entrées >1,000 mg sodium—clash with ~65% of adults trying to eat healthier and US avg sodium 3,400 mg/day (CDC). High labor intensity raises costs amid industry labor at 30–35% of sales and avg food service wage $15.07 (BLS May 2024).

| Metric | Value (source) |

|---|---|

| US locations | >2,400 (2024) |

| Entrées sodium | several >1,000 mg (menu data) |

| US avg sodium | 3,400 mg/day (CDC) |

| Adults trying healthier | ~65% (survey) |

| Labor % of sales | 30–35% (Natl Restaurant Assoc) |

| Avg wage (food prep) | $15.07/hr (BLS May 2024) |

Same Document Delivered

Panda Restaurant Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The content is ready to use and becomes available immediately after checkout.

Description

Elevate Your Analysis with the Complete SWOT Report

Panda Restaurant Group blends strong brand recognition and a scalable franchise model with menu innovation, while facing rising labor & commodity costs and fierce fast‑casual competition. Want the full story behind strengths, risks, and growth drivers? Purchase the complete SWOT analysis for a professionally written, editable report ideal for strategic planning and investment.

Strengths

Largest American Chinese chain

Panda Express, the largest American Chinese chain with over 2,200 U.S. restaurants, holds clear category leadership that drives strong brand recall and higher store traffic. Its scale yields purchasing power and marketing efficiency, supporting faster rollouts of menu and digital initiatives. Market dominance also provides landlord leverage for prime sites and drive-thru placements, creating a high barrier for smaller rivals.

Operational consistency at scale

Standardized recipes, wok-cooking processes and rigorous training deliver predictable quality across Panda's network of over 2,200 restaurants, supporting consistent dish execution and speed of service. Centralized supply partnerships and a streamlined menu reduce complexity and waste, improving margins and inventory turns. Reliable execution drives high throughput, stronger unit economics and repeat visitation rates.

Multi-format portfolio

Panda Restaurant Group spans fast-casual to full-service through Panda Express (over 2,200 locations), legacy Panda Inn (founded 1973) and newer Hibachi-San (launched 2021), allowing targeting of varied occasions, check sizes and real estate types. This multi-format portfolio helps balance cyclical dining shifts and enables cross-learning in menu R&D and service models.

Strong culture and private ownership

Founder-led stewardship by Andrew and Peggy Cherng (founded 1983) and a values-driven culture enable long-term decisions; private, family ownership allows reinvestment without quarterly pressures. Structured training and career pathways raise retention and service quality, aligning staff and leadership to enhance execution and brand reputation.

- Founder-led

- Private ownership

- Long-term reinvestment

- Employee development

Real estate and drive-thru footprint

Panda Restaurant Group operates more than 2,300 restaurants worldwide as of 2024, leveraging site-selection expertise to expand stand-alone and drive-thru units beyond malls. Drive-thrus increase convenience, strengthen sales resilience and grow off-premise mix; diverse locations capture lunch, dinner and impulse traffic, enabling format- and market-level growth.

- >2,300 restaurants (2024)

- Drive-thru expansion boosts off-premise sales

- Stand-alone sites extend beyond malls

- Covers multiple dayparts and impulse visits

Leading U.S. American-Chinese chain with >2,300 restaurants and scale-driven margins

Panda Express leads U.S. American Chinese with >2,300 restaurants (2024), strong brand recall and scale-driven purchasing and marketing advantages. Standardized wok-cooking, centralized supply and rigorous training deliver consistent quality, speed and better unit economics. Family ownership enables long-term reinvestment and rapid drive-thru/stand-alone expansion.

| Metric | Value |

|---|---|

| Restaurants (2024) | >2,300 |

| Founded | 1983 |

| Formats | Panda Express, Panda Inn, Hibachi-San |

| Ownership | Private, Cherng family |

What is included in the product

Delivers a strategic overview of Panda Restaurant Group’s internal and external business factors, highlighting strengths, weaknesses, opportunities, and threats shaping its growth, operational resilience, and competitive position.

Provides a focused SWOT matrix highlighting Panda Restaurant Group's strengths, weaknesses, opportunities, and threats for rapid strategy alignment and faster executive decision-making.

Weaknesses

Menu perceived as Americanized

Heavy reliance on American-Chinese staples limits appeal to authenticity-seeking diners and narrows flavor profiles versus broader Asian cuisines. This perception can suppress willingness to pay premium prices in select markets. As the largest Chinese fast-casual chain in the U.S. with over 2,400 locations, it faces higher barriers for international adoption without localization.

Health and nutrition concerns

Fried items and sugar-laden sauces at Panda Express, with several entrées exceeding 1,000 mg sodium per serving, deter health-conscious consumers as US average sodium intake is ~3,400 mg/day (CDC). About 65% of adults report trying to eat healthier, so perceptions clash with wellness trends. Limited low-calorie or specialty-diet options can reduce visit frequency and cap addressable occasions and corporate catering wins despite over 2,400 US locations (2024).

High labor intensity

High labor intensity at Panda — driven by wok cooking and peak-service staffing — requires skilled hires and training, tying into industry labor costs that typically run 30–35% of sales (National Restaurant Association). Higher wage pressure (food prep/serving average hourly wage $15.07, BLS May 2024) raises operating costs and turnover sensitivity. Staffing gaps produce execution variance and complicate rapid new-unit rollouts.

Capital-heavy company-operated model

Owning the majority of its more than 2,400 restaurants (2024) concentrates CAPEX and operating risk on Panda, raising exposure to same-store volatility. Growth pace depends on internal capital and execution bandwidth rather than franchising, limiting asset-light scalability. Limited franchising increases exposure to localized downturns and slows capital-efficient expansion.

- High CAPEX concentration

- Growth tied to internal capital

- Low asset-light scalability

- Greater local downturn exposure

U.S.-centric revenue base

Panda Restaurant Group's revenue is primarily U.S.-centric, tying performance closely to domestic economic cycles and consumer spending swings. Limited international penetration reduces currency and market diversification, leaving growth dependent on a single macro environment. Regional saturation raises cannibalization risk and heightens sensitivity to U.S. labor, wage and real estate cost pressures.

- U.S.-centric exposure

- Low currency/market diversification

- Regional saturation → cannibalization

- Higher macroeconomic sensitivity

High-sodium menu and high labor costs threaten appeal vs 2,400+ US outlets

Heavy reliance on American-Chinese staples and limited authentic/menu diversity constrains upscale appeal; over 2,400 US locations (2024) also hinder easy international adoption. Menu health issues—several entrées >1,000 mg sodium—clash with ~65% of adults trying to eat healthier and US avg sodium 3,400 mg/day (CDC). High labor intensity raises costs amid industry labor at 30–35% of sales and avg food service wage $15.07 (BLS May 2024).

| Metric | Value (source) |

|---|---|

| US locations | >2,400 (2024) |

| Entrées sodium | several >1,000 mg (menu data) |

| US avg sodium | 3,400 mg/day (CDC) |

| Adults trying healthier | ~65% (survey) |

| Labor % of sales | 30–35% (Natl Restaurant Assoc) |

| Avg wage (food prep) | $15.07/hr (BLS May 2024) |

Same Document Delivered

Panda Restaurant Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The content is ready to use and becomes available immediately after checkout.