Pangea Natural Foods Porter's Five Forces Analysis

Don't Miss the Bigger Picture

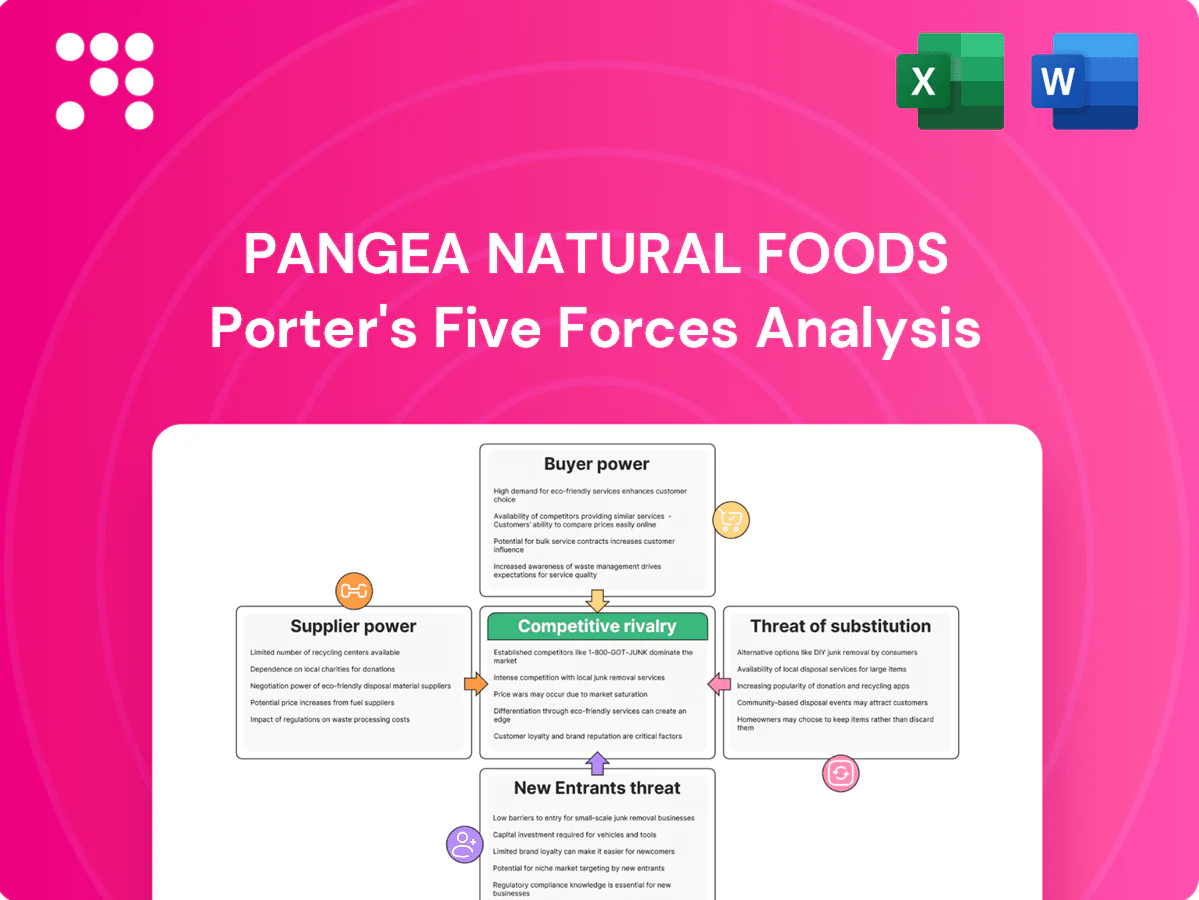

Pangea Natural Foods faces moderate supplier power from specialty ingredients, strong buyer bargaining in retail/private-label channels, and growing substitute pressure as mainstream brands naturalize. Entry barriers are mixed—brand and quality help, but scale and distribution matter—while rivalry hinges on innovation and channel access. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentration of protein and oil inputs

Pangea depends on concentrated suppliers for pea/soy proteins, coconut/canola oils and specialty binders, giving those suppliers outsized leverage on price and contract terms. Long-term contracts and dual-sourcing strategies implemented in 2024 reduce supply disruption risk and lock pricing, but they do not eliminate exposure. Volatility in agri-commodity markets can still transmit to COGS and compress margins.

Specialty ingredients and IP-dependent inputs

Certain flavor systems, texturizers and enzymes are proprietary or niche, limiting substitutes and letting suppliers command premiums often in the 10–30% range and set high MOQs (commonly thousands of kilograms). Reformulation to alternatives typically requires 3–9 months and carries sensory and shelf-life risks that can affect launch timelines. Strategic partnerships, co-development deals and forward contracts can secure access and have reduced input volatility by up to ~20% in comparable food ingredient agreements in 2024.

Co-manufacturing and capacity constraints

If Pangea relies on co-packers for extrusion or aseptic fills, available capacity is often tight with industry utilization frequently above 80%, boosting switching costs and giving capable co-mans leverage. Dedicated runs and line-time reservations force higher WIP and finished-goods inventory, increasing working capital needs and minimum order commitments. Building in-house extrusion/aseptic capacity typically requires low-to-mid single-digit million-dollar capex per line but reduces supplier dependence.

Packaging and sustainability requirements

- Qualified vendors <25% (2024)

- Vetting costs +15–30% (2024)

- Multi-sourcing reduces dependency

Geography, logistics, and ESG traceability

Import routes and seasonality drive freight cost and reliability volatility—Freightos Baltic Index fell roughly 80% from 2022 peaks to 2024 averages, narrowing but not eliminating route risk. Traceability requirements for non-GMO, allergen control and ethical sourcing shrink viable suppliers and raise compliance costs; suppliers meeting ESG criteria commonly command 5–15% premiums in 2024. Digital supplier scorecards enable negotiations focused on quality, traceability and lead-time, not just price.

- Freight volatility: FBX ~80% down from 2022 to 2024

- ESG premium: 5–15% (2024)

- Traceability limits supplier pool

- Scorecards shift leverage beyond price

High supplier power, tight co-packer capacity and ESG/commodity premia squeeze COGS

Pangea faces high supplier power from concentrated protein/oil suppliers, niche flavor/texturizer vendors and tight co-packer capacity, keeping switching costs and premiums elevated. Long-term contracts and dual-sourcing cut disruption risk but do not remove commodity and ESG-driven cost exposure. 2024 metrics show limited qualified vendors and material premia affecting COGS.

| Metric | 2024 |

|---|---|

| Qualified recyclable vendors | <25% |

| Vetting cost increase | +15–30% |

| ESG premium | 5–15% |

| Co-packer util. | >80% |

| FBX change | ~80% down vs 2022 |

What is included in the product

Tailored Porter's Five Forces assessment of Pangea Natural Foods, highlighting competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive forces and strategic levers to protect margins and market share.

A concise one-sheet Porter's Five Forces for Pangea Natural Foods that highlights competitive pressures and actional relief strategies—easy to paste into decks, update with new data, and communicate priority responses to suppliers, rivals, buyers, entrants, and substitutes.

Customers Bargaining Power

Retail and foodservice consolidation

Large grocers, club stores and QSRs exert strong buyer power—top four US grocers held roughly 50% of grocery sales in 2024, with Walmart reporting ~$611B and Costco ~$266B in FY2024—commanding slotting fees, trade spend and strict fill rates. Their scale pressures pricing and promotions, forcing margin concessions to win distribution. Diversifying channels (e‑commerce, natural food co-ops, foodservice) dilutes any single buyer’s leverage.

Low switching costs for consumers

Low switching costs let plant-based shoppers jump brands on taste, price or promotions, boosting buyer power at shelf; the global plant-based retail market was roughly $46 billion in 2024, intensifying competition. Limited product differentiation magnifies this effect, while superior sensory profile and nutrition drive loyalty; consistent quality, packaging and branding are critical to reduce churn.

Private label alternatives

Retailers are expanding private-label plant-based SKUs that often undercut branded pricing; NielsenIQ reported private-label grocery dollar share at about 16.5% in 2023, pressuring margins for brands like Pangea. Retailers can favor their own labels in shelf placement and promotions, reducing branded visibility and sales velocity. Pangea must justify its premium through measurable innovation, robust third-party claims, and SKU-level ROI to defend price and placement.

Demand for clean-label and transparency

In 2024, 68% of consumers surveyed said clean-label and ingredient transparency heavily influence purchase decisions, so informed buyers closely scrutinize ingredient lists, allergens, and sourcing and will switch brands quickly if standards aren’t met. Robust labeling and third-party verified claims reduce buyer objection power and can boost willingness to pay, while certifications (organic, non-GMO, Fair Trade) unlock higher-margin segments and premium placement.

- Informed scrutiny: ingredient lists, allergens, sourcing

- Switching risk: rapid churn if standards fail

- Mitigation: strong labels + verified claims

- Opportunity: certifications -> premium margins

Elasticity in inflationary periods

When budgets tighten consumers trade down or revert to animal proteins, amplifying price sensitivity; US headline CPI eased to about 3.4% in 2024 while food-at-home inflation remained elevated near 4.0%, heightening buyer power during spikes. Pack-size engineering and value SKUs defend volumes, and targeted promos can protect velocity without eroding brand equity.

- price-sensitivity: higher during inflation spikes

- defense: pack-size & value SKUs preserve market share

- promo: targeted offers protect velocity, limit brand dilution

Grocers control ~50% of sales; plant-based $46B, clean-label 68%

Large US grocers hold ~50% of grocery sales in 2024 (Walmart ~$611B, Costco ~$266B FY2024), exerting strong slotting and pricing pressure; plant-based retail was ≈$46B in 2024, intensifying buyer choice. Low switching costs and private-label share (~16.5% grocery dollars, 2023) raise buyer leverage; 68% of consumers cite clean-label importance (2024). Food-at-home inflation ~4.0% (2024) increases price sensitivity.

| Metric | Value |

|---|---|

| Top-4 grocers share | ~50% (2024) |

| Walmart revenue | ~$611B FY2024 |

| Costco revenue | ~$266B FY2024 |

| Plant-based market | ~$46B (2024) |

| Private-label share | 16.5% (2023) |

| Clean-label importance | 68% (2024) |

| Food-at-home inflation | ~4.0% (2024) |

Full Version Awaits

Pangea Natural Foods Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Pangea Natural Foods you'll receive immediately after purchase—fully formatted and ready to use. No mockups or placeholders: the document displayed is the complete, download-ready file you'll get instantly upon payment. It includes actionable insights and data used in the final deliverable.

Don't Miss the Bigger Picture

Pangea Natural Foods faces moderate supplier power from specialty ingredients, strong buyer bargaining in retail/private-label channels, and growing substitute pressure as mainstream brands naturalize. Entry barriers are mixed—brand and quality help, but scale and distribution matter—while rivalry hinges on innovation and channel access. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentration of protein and oil inputs

Pangea depends on concentrated suppliers for pea/soy proteins, coconut/canola oils and specialty binders, giving those suppliers outsized leverage on price and contract terms. Long-term contracts and dual-sourcing strategies implemented in 2024 reduce supply disruption risk and lock pricing, but they do not eliminate exposure. Volatility in agri-commodity markets can still transmit to COGS and compress margins.

Specialty ingredients and IP-dependent inputs

Certain flavor systems, texturizers and enzymes are proprietary or niche, limiting substitutes and letting suppliers command premiums often in the 10–30% range and set high MOQs (commonly thousands of kilograms). Reformulation to alternatives typically requires 3–9 months and carries sensory and shelf-life risks that can affect launch timelines. Strategic partnerships, co-development deals and forward contracts can secure access and have reduced input volatility by up to ~20% in comparable food ingredient agreements in 2024.

Co-manufacturing and capacity constraints

If Pangea relies on co-packers for extrusion or aseptic fills, available capacity is often tight with industry utilization frequently above 80%, boosting switching costs and giving capable co-mans leverage. Dedicated runs and line-time reservations force higher WIP and finished-goods inventory, increasing working capital needs and minimum order commitments. Building in-house extrusion/aseptic capacity typically requires low-to-mid single-digit million-dollar capex per line but reduces supplier dependence.

Packaging and sustainability requirements

- Qualified vendors <25% (2024)

- Vetting costs +15–30% (2024)

- Multi-sourcing reduces dependency

Geography, logistics, and ESG traceability

Import routes and seasonality drive freight cost and reliability volatility—Freightos Baltic Index fell roughly 80% from 2022 peaks to 2024 averages, narrowing but not eliminating route risk. Traceability requirements for non-GMO, allergen control and ethical sourcing shrink viable suppliers and raise compliance costs; suppliers meeting ESG criteria commonly command 5–15% premiums in 2024. Digital supplier scorecards enable negotiations focused on quality, traceability and lead-time, not just price.

- Freight volatility: FBX ~80% down from 2022 to 2024

- ESG premium: 5–15% (2024)

- Traceability limits supplier pool

- Scorecards shift leverage beyond price

High supplier power, tight co-packer capacity and ESG/commodity premia squeeze COGS

Pangea faces high supplier power from concentrated protein/oil suppliers, niche flavor/texturizer vendors and tight co-packer capacity, keeping switching costs and premiums elevated. Long-term contracts and dual-sourcing cut disruption risk but do not remove commodity and ESG-driven cost exposure. 2024 metrics show limited qualified vendors and material premia affecting COGS.

| Metric | 2024 |

|---|---|

| Qualified recyclable vendors | <25% |

| Vetting cost increase | +15–30% |

| ESG premium | 5–15% |

| Co-packer util. | >80% |

| FBX change | ~80% down vs 2022 |

What is included in the product

Tailored Porter's Five Forces assessment of Pangea Natural Foods, highlighting competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive forces and strategic levers to protect margins and market share.

A concise one-sheet Porter's Five Forces for Pangea Natural Foods that highlights competitive pressures and actional relief strategies—easy to paste into decks, update with new data, and communicate priority responses to suppliers, rivals, buyers, entrants, and substitutes.

Customers Bargaining Power

Retail and foodservice consolidation

Large grocers, club stores and QSRs exert strong buyer power—top four US grocers held roughly 50% of grocery sales in 2024, with Walmart reporting ~$611B and Costco ~$266B in FY2024—commanding slotting fees, trade spend and strict fill rates. Their scale pressures pricing and promotions, forcing margin concessions to win distribution. Diversifying channels (e‑commerce, natural food co-ops, foodservice) dilutes any single buyer’s leverage.

Low switching costs for consumers

Low switching costs let plant-based shoppers jump brands on taste, price or promotions, boosting buyer power at shelf; the global plant-based retail market was roughly $46 billion in 2024, intensifying competition. Limited product differentiation magnifies this effect, while superior sensory profile and nutrition drive loyalty; consistent quality, packaging and branding are critical to reduce churn.

Private label alternatives

Retailers are expanding private-label plant-based SKUs that often undercut branded pricing; NielsenIQ reported private-label grocery dollar share at about 16.5% in 2023, pressuring margins for brands like Pangea. Retailers can favor their own labels in shelf placement and promotions, reducing branded visibility and sales velocity. Pangea must justify its premium through measurable innovation, robust third-party claims, and SKU-level ROI to defend price and placement.

Demand for clean-label and transparency

In 2024, 68% of consumers surveyed said clean-label and ingredient transparency heavily influence purchase decisions, so informed buyers closely scrutinize ingredient lists, allergens, and sourcing and will switch brands quickly if standards aren’t met. Robust labeling and third-party verified claims reduce buyer objection power and can boost willingness to pay, while certifications (organic, non-GMO, Fair Trade) unlock higher-margin segments and premium placement.

- Informed scrutiny: ingredient lists, allergens, sourcing

- Switching risk: rapid churn if standards fail

- Mitigation: strong labels + verified claims

- Opportunity: certifications -> premium margins

Elasticity in inflationary periods

When budgets tighten consumers trade down or revert to animal proteins, amplifying price sensitivity; US headline CPI eased to about 3.4% in 2024 while food-at-home inflation remained elevated near 4.0%, heightening buyer power during spikes. Pack-size engineering and value SKUs defend volumes, and targeted promos can protect velocity without eroding brand equity.

- price-sensitivity: higher during inflation spikes

- defense: pack-size & value SKUs preserve market share

- promo: targeted offers protect velocity, limit brand dilution

Grocers control ~50% of sales; plant-based $46B, clean-label 68%

Large US grocers hold ~50% of grocery sales in 2024 (Walmart ~$611B, Costco ~$266B FY2024), exerting strong slotting and pricing pressure; plant-based retail was ≈$46B in 2024, intensifying buyer choice. Low switching costs and private-label share (~16.5% grocery dollars, 2023) raise buyer leverage; 68% of consumers cite clean-label importance (2024). Food-at-home inflation ~4.0% (2024) increases price sensitivity.

| Metric | Value |

|---|---|

| Top-4 grocers share | ~50% (2024) |

| Walmart revenue | ~$611B FY2024 |

| Costco revenue | ~$266B FY2024 |

| Plant-based market | ~$46B (2024) |

| Private-label share | 16.5% (2023) |

| Clean-label importance | 68% (2024) |

| Food-at-home inflation | ~4.0% (2024) |

Full Version Awaits

Pangea Natural Foods Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Pangea Natural Foods you'll receive immediately after purchase—fully formatted and ready to use. No mockups or placeholders: the document displayed is the complete, download-ready file you'll get instantly upon payment. It includes actionable insights and data used in the final deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Pangea Natural Foods faces moderate supplier power from specialty ingredients, strong buyer bargaining in retail/private-label channels, and growing substitute pressure as mainstream brands naturalize. Entry barriers are mixed—brand and quality help, but scale and distribution matter—while rivalry hinges on innovation and channel access. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentration of protein and oil inputs

Pangea depends on concentrated suppliers for pea/soy proteins, coconut/canola oils and specialty binders, giving those suppliers outsized leverage on price and contract terms. Long-term contracts and dual-sourcing strategies implemented in 2024 reduce supply disruption risk and lock pricing, but they do not eliminate exposure. Volatility in agri-commodity markets can still transmit to COGS and compress margins.

Specialty ingredients and IP-dependent inputs

Certain flavor systems, texturizers and enzymes are proprietary or niche, limiting substitutes and letting suppliers command premiums often in the 10–30% range and set high MOQs (commonly thousands of kilograms). Reformulation to alternatives typically requires 3–9 months and carries sensory and shelf-life risks that can affect launch timelines. Strategic partnerships, co-development deals and forward contracts can secure access and have reduced input volatility by up to ~20% in comparable food ingredient agreements in 2024.

Co-manufacturing and capacity constraints

If Pangea relies on co-packers for extrusion or aseptic fills, available capacity is often tight with industry utilization frequently above 80%, boosting switching costs and giving capable co-mans leverage. Dedicated runs and line-time reservations force higher WIP and finished-goods inventory, increasing working capital needs and minimum order commitments. Building in-house extrusion/aseptic capacity typically requires low-to-mid single-digit million-dollar capex per line but reduces supplier dependence.

Packaging and sustainability requirements

- Qualified vendors <25% (2024)

- Vetting costs +15–30% (2024)

- Multi-sourcing reduces dependency

Geography, logistics, and ESG traceability

Import routes and seasonality drive freight cost and reliability volatility—Freightos Baltic Index fell roughly 80% from 2022 peaks to 2024 averages, narrowing but not eliminating route risk. Traceability requirements for non-GMO, allergen control and ethical sourcing shrink viable suppliers and raise compliance costs; suppliers meeting ESG criteria commonly command 5–15% premiums in 2024. Digital supplier scorecards enable negotiations focused on quality, traceability and lead-time, not just price.

- Freight volatility: FBX ~80% down from 2022 to 2024

- ESG premium: 5–15% (2024)

- Traceability limits supplier pool

- Scorecards shift leverage beyond price

High supplier power, tight co-packer capacity and ESG/commodity premia squeeze COGS

Pangea faces high supplier power from concentrated protein/oil suppliers, niche flavor/texturizer vendors and tight co-packer capacity, keeping switching costs and premiums elevated. Long-term contracts and dual-sourcing cut disruption risk but do not remove commodity and ESG-driven cost exposure. 2024 metrics show limited qualified vendors and material premia affecting COGS.

| Metric | 2024 |

|---|---|

| Qualified recyclable vendors | <25% |

| Vetting cost increase | +15–30% |

| ESG premium | 5–15% |

| Co-packer util. | >80% |

| FBX change | ~80% down vs 2022 |

What is included in the product

Tailored Porter's Five Forces assessment of Pangea Natural Foods, highlighting competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive forces and strategic levers to protect margins and market share.

A concise one-sheet Porter's Five Forces for Pangea Natural Foods that highlights competitive pressures and actional relief strategies—easy to paste into decks, update with new data, and communicate priority responses to suppliers, rivals, buyers, entrants, and substitutes.

Customers Bargaining Power

Retail and foodservice consolidation

Large grocers, club stores and QSRs exert strong buyer power—top four US grocers held roughly 50% of grocery sales in 2024, with Walmart reporting ~$611B and Costco ~$266B in FY2024—commanding slotting fees, trade spend and strict fill rates. Their scale pressures pricing and promotions, forcing margin concessions to win distribution. Diversifying channels (e‑commerce, natural food co-ops, foodservice) dilutes any single buyer’s leverage.

Low switching costs for consumers

Low switching costs let plant-based shoppers jump brands on taste, price or promotions, boosting buyer power at shelf; the global plant-based retail market was roughly $46 billion in 2024, intensifying competition. Limited product differentiation magnifies this effect, while superior sensory profile and nutrition drive loyalty; consistent quality, packaging and branding are critical to reduce churn.

Private label alternatives

Retailers are expanding private-label plant-based SKUs that often undercut branded pricing; NielsenIQ reported private-label grocery dollar share at about 16.5% in 2023, pressuring margins for brands like Pangea. Retailers can favor their own labels in shelf placement and promotions, reducing branded visibility and sales velocity. Pangea must justify its premium through measurable innovation, robust third-party claims, and SKU-level ROI to defend price and placement.

Demand for clean-label and transparency

In 2024, 68% of consumers surveyed said clean-label and ingredient transparency heavily influence purchase decisions, so informed buyers closely scrutinize ingredient lists, allergens, and sourcing and will switch brands quickly if standards aren’t met. Robust labeling and third-party verified claims reduce buyer objection power and can boost willingness to pay, while certifications (organic, non-GMO, Fair Trade) unlock higher-margin segments and premium placement.

- Informed scrutiny: ingredient lists, allergens, sourcing

- Switching risk: rapid churn if standards fail

- Mitigation: strong labels + verified claims

- Opportunity: certifications -> premium margins

Elasticity in inflationary periods

When budgets tighten consumers trade down or revert to animal proteins, amplifying price sensitivity; US headline CPI eased to about 3.4% in 2024 while food-at-home inflation remained elevated near 4.0%, heightening buyer power during spikes. Pack-size engineering and value SKUs defend volumes, and targeted promos can protect velocity without eroding brand equity.

- price-sensitivity: higher during inflation spikes

- defense: pack-size & value SKUs preserve market share

- promo: targeted offers protect velocity, limit brand dilution

Grocers control ~50% of sales; plant-based $46B, clean-label 68%

Large US grocers hold ~50% of grocery sales in 2024 (Walmart ~$611B, Costco ~$266B FY2024), exerting strong slotting and pricing pressure; plant-based retail was ≈$46B in 2024, intensifying buyer choice. Low switching costs and private-label share (~16.5% grocery dollars, 2023) raise buyer leverage; 68% of consumers cite clean-label importance (2024). Food-at-home inflation ~4.0% (2024) increases price sensitivity.

| Metric | Value |

|---|---|

| Top-4 grocers share | ~50% (2024) |

| Walmart revenue | ~$611B FY2024 |

| Costco revenue | ~$266B FY2024 |

| Plant-based market | ~$46B (2024) |

| Private-label share | 16.5% (2023) |

| Clean-label importance | 68% (2024) |

| Food-at-home inflation | ~4.0% (2024) |

Full Version Awaits

Pangea Natural Foods Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Pangea Natural Foods you'll receive immediately after purchase—fully formatted and ready to use. No mockups or placeholders: the document displayed is the complete, download-ready file you'll get instantly upon payment. It includes actionable insights and data used in the final deliverable.