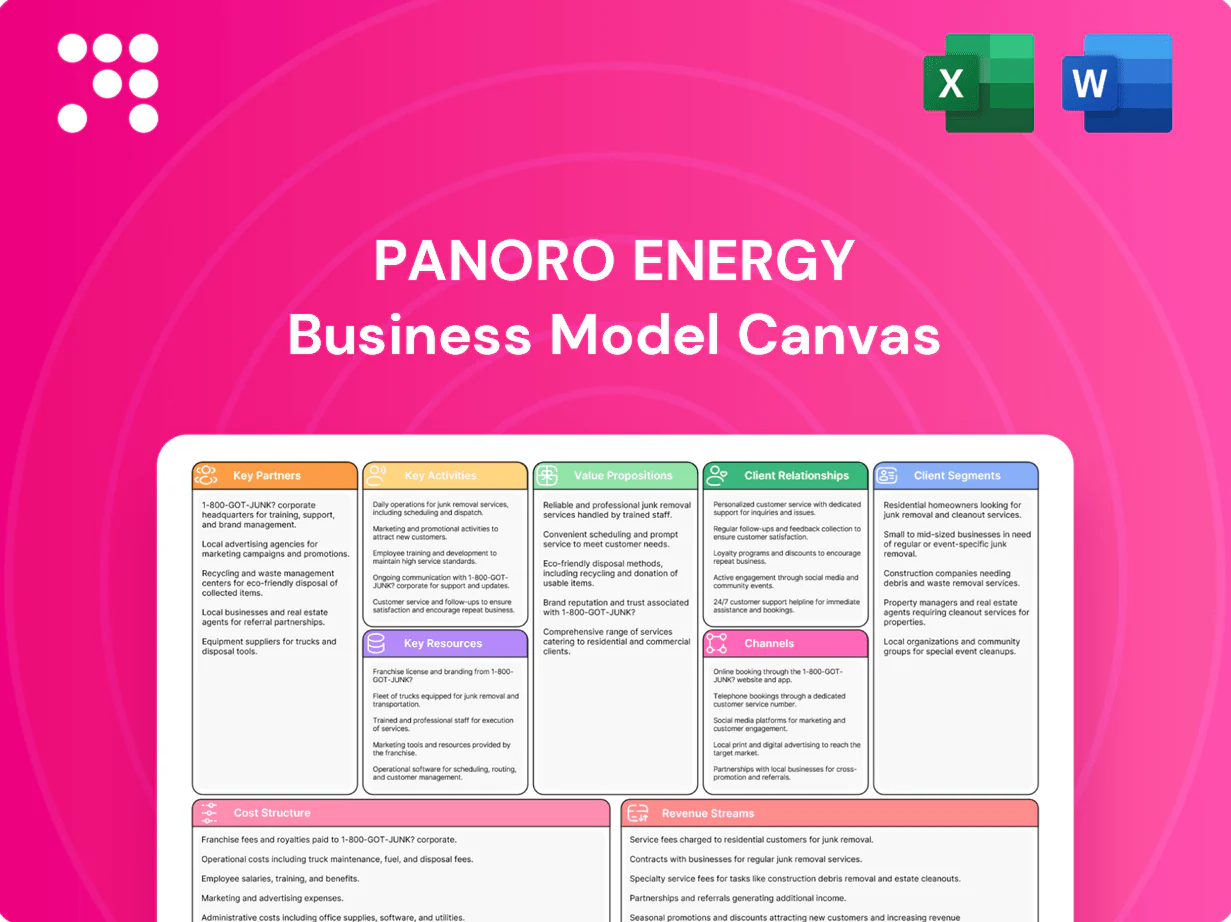

Panoro Energy Business Model Canvas

Business Model Canvas: Exploration, Asset Optimization & Partner-Led Value Drivers

Unlock the strategic core of Panoro Energy with our concise Business Model Canvas—showing how exploration, asset optimization and partner-led development drive value and revenue. This practical snapshot highlights key partners, cost drivers and growth levers. Purchase the full Canvas for a detailed, editable plan ready for investor decks and strategic use.

Partnerships

Host governments and NOCs

Panoro’s concessions and production‑sharing agreements require strong ties with host ministries and NOCs; government take in African PSAs typically ranges 60–85% (2024). These partners enable access, approvals and stable operating frameworks that underpin licence security and continuity. Transparent engagement reduces dispute risk and supports uninterrupted production. Aligning local content with host targets — often 30–40% skilled local hire goals in 2024 — strengthens legitimacy and resilience.

Joint-venture and farm-in partners

Panoro leverages joint ventures and farm‑ins to share geological risk and capital load, with 2024 partnerships across West Africa reducing operator capital commitments and accelerating development timelines. Farm‑ins/farm‑outs optimize portfolio balance and funding while joint operating committees enforce technical governance and execution discipline. Diverse partners expand optionality across exploration, appraisal and production phases.

Oilfield services and EPC contractors

Drilling, subsea, seismic and EPC partners are critical to safe, timely execution for Panoro Energy’s West Africa developments, with EPC packages typically representing 30–50% of upstream development capex. Performance-based contracts align incentives and industry practice has reduced schedule overruns by notable margins. Robust vendor ecosystems enable ~20% faster scaling across cycles, while local suppliers meet 30–60% local content mandates in the region.

Offtakers, traders, and refiners

Sales partners provide market access, lifting services and pricing benchmarks, supporting Panoro Energy’s average 2024 sales of ~26,000 boe/d; term contracts (covering core volumes) stabilize cash flow while spot trades capture upside; blending and logistics support improve netbacks and reliable counterparties reduce lifting and payment risk.

- Market access: lifting services/pricing

- Hedge mix: term stability + spot upside

- Ops: blending/logistics raise netbacks

- Counterparty quality lowers lifting/payment risk

Banks, commodity financiers, and insurers

Reserve-based lending, prepayment facilities and trade finance underpinned Panoro Energy’s 2024 capital needs, enabling project funding and near-term liquidity; hedging providers (fixed-price and collar structures) reduced realized price volatility; insurers and export credit agencies mitigated operational and political risk, supporting access to international financing; a mix of banks, commodity financiers and insurers enables disciplined growth.

- PNR listed on Oslo Børs (PNR)

- Reserve-based lending + prepayments = core liquidity tools (2024)

- Hedging and insurance lower revenue and political risk

Govt/NOC JVs: 60–85% take, 30–40% local; support 26,000 boe/d

Panoro’s key partnerships with host governments and NOCs secure licences and align with 2024 government take of 60–85% and local content targets ~30–40%. JVs and farm‑ins share geological risk and capex, supporting 26,000 boe/d (2024). EPC and service contractors (30–50% of dev capex) drive delivery; financiers (RBL, prepayments) and insurers underpin liquidity and risk mitigation.

| Partner | 2024 Metric |

|---|---|

| Govt/NOC | Take 60–85% / Local content 30–40% |

| Production | 26,000 boe/d |

| Capex | EPC 30–50% |

| Finance | RBL + prepayments core |

What is included in the product

A concise, pre-written Business Model Canvas for Panoro Energy mapping its 9 blocks—customer segments, value propositions, channels, revenue streams, key resources, partners, activities, cost structure, and customer relationships—aligned to its Africa-focused E&P strategy, asset-led production growth, low-cost operations and JV partnerships; ideal for investor presentations, strategic planning, and competitive analysis.

High-level view of Panoro Energy’s business model with editable cells — quickly identify asset portfolios, revenue drivers, and cost pressures on one page to relieve analysis bottlenecks for teams and investors.

Activities

Exploration and appraisal

Exploration and appraisal de-risk prospects for Panoro Energy through seismic acquisition, integrated geoscience and targeted appraisal drilling to convert leads into commercial resources. Portfolio screening balances geological risk, basin maturity and cycle time to prioritize capital deployment and farm-down opportunities. Continuous data integration and learning from 2024 appraisal campaigns sharpen well targeting, improve resource classification and raise capital efficiency.

Field development and production

Plan and execute wells, facilities and tie-backs to monetize Panoro’s ~27,000 boe/d scale, targeting new tie-backs that can add 5–10 kbbls/d per project; focus on optimizing lift costs to around $10–12/boe, maximizing uptime and managing decline with reservoir-focused interventions. Phased developments align capex with cash flow, cutting near-term funding needs by ~30% per stage, while integrity management and HSE programs protect people, assets and reservoir value.

Commercial and marketing

Panoro negotiates offtake, lifting schedules and pricing formulas to capture value across its ~22,000 boe/d (2024) portfolio, targeting realized oil prices near $72/bl in 2024. It manages quality differentials, blending and logistics to improve realizations by limiting discounts. Term vs spot exposure is structured—roughly 35% hedged in 2024—to balance cash certainty and upside. Strong counterparty vetting and credit controls limit receivable and operational risk.

Portfolio and capital allocation

Panoro recycles capital through targeted acquisitions, farm-ins and selective divestments, prioritising projects by NPV, breakevens and payback to maximise returns; Brent averaged about 90 USD/bbl in 2024, guiding economics and funding capacity. Spend is aligned with commodity cycles and available funding, using staged commitments to maintain optionality and limit downside.

- Recycle capital: acquisitions, farm-ins, divestments

- Prioritise: NPV, breakeven, payback

- Align spend: commodity cycles & funding capacity (Brent ~90 USD/bbl 2024)

- Maintain optionality: staged commitments

Risk, HSE, and compliance

Panoro embeds safety, environmental stewardship and regulatory adherence across operations through formal HSE systems and continuous risk assessments; these practices protect asset value and limit operational interruptions. The company uses hedging, insurance and contingency planning to manage price and operational volatility, while proactive community engagement reduces social license risk. Strong governance frameworks ensure ethical, transparent conduct and regulatory compliance.

Monetize ~22k boe/d (2024), tie-backs & $10-12/boe

Explore and appraise to convert prospects into commercial resources across Panoro’s ~27,000 boe/d scale, prioritising risks, cycle time and farm-downs. Execute tie-backs and phased developments to monetize ~22,000 boe/d (2024), targeting $10–12/boe lift costs and ~30% lower near-term capex per stage. Manage offtake, hedging (~35% 2024) and logistics to realize ~$72/bl (2024) versus Brent ~$90.

| Metric | 2024 |

|---|---|

| Reported production | 22,000 boe/d |

| Portfolio scale | ~27,000 boe/d |

| Realized oil price | $72/bl |

| Brent | $90/bl |

| Hedged | 35% |

| Lift cost | $10–12/boe |

Full Version Awaits

Business Model Canvas

The Panoro Energy Business Model Canvas you see here is the actual deliverable, not a mockup; it’s a direct snapshot of the file you’ll receive after purchase. On completion, you’ll get this same ready-to-use, editable document in Word and Excel formats with all sections included—no surprises.

Business Model Canvas: Exploration, Asset Optimization & Partner-Led Value Drivers

Unlock the strategic core of Panoro Energy with our concise Business Model Canvas—showing how exploration, asset optimization and partner-led development drive value and revenue. This practical snapshot highlights key partners, cost drivers and growth levers. Purchase the full Canvas for a detailed, editable plan ready for investor decks and strategic use.

Partnerships

Host governments and NOCs

Panoro’s concessions and production‑sharing agreements require strong ties with host ministries and NOCs; government take in African PSAs typically ranges 60–85% (2024). These partners enable access, approvals and stable operating frameworks that underpin licence security and continuity. Transparent engagement reduces dispute risk and supports uninterrupted production. Aligning local content with host targets — often 30–40% skilled local hire goals in 2024 — strengthens legitimacy and resilience.

Joint-venture and farm-in partners

Panoro leverages joint ventures and farm‑ins to share geological risk and capital load, with 2024 partnerships across West Africa reducing operator capital commitments and accelerating development timelines. Farm‑ins/farm‑outs optimize portfolio balance and funding while joint operating committees enforce technical governance and execution discipline. Diverse partners expand optionality across exploration, appraisal and production phases.

Oilfield services and EPC contractors

Drilling, subsea, seismic and EPC partners are critical to safe, timely execution for Panoro Energy’s West Africa developments, with EPC packages typically representing 30–50% of upstream development capex. Performance-based contracts align incentives and industry practice has reduced schedule overruns by notable margins. Robust vendor ecosystems enable ~20% faster scaling across cycles, while local suppliers meet 30–60% local content mandates in the region.

Offtakers, traders, and refiners

Sales partners provide market access, lifting services and pricing benchmarks, supporting Panoro Energy’s average 2024 sales of ~26,000 boe/d; term contracts (covering core volumes) stabilize cash flow while spot trades capture upside; blending and logistics support improve netbacks and reliable counterparties reduce lifting and payment risk.

- Market access: lifting services/pricing

- Hedge mix: term stability + spot upside

- Ops: blending/logistics raise netbacks

- Counterparty quality lowers lifting/payment risk

Banks, commodity financiers, and insurers

Reserve-based lending, prepayment facilities and trade finance underpinned Panoro Energy’s 2024 capital needs, enabling project funding and near-term liquidity; hedging providers (fixed-price and collar structures) reduced realized price volatility; insurers and export credit agencies mitigated operational and political risk, supporting access to international financing; a mix of banks, commodity financiers and insurers enables disciplined growth.

- PNR listed on Oslo Børs (PNR)

- Reserve-based lending + prepayments = core liquidity tools (2024)

- Hedging and insurance lower revenue and political risk

Govt/NOC JVs: 60–85% take, 30–40% local; support 26,000 boe/d

Panoro’s key partnerships with host governments and NOCs secure licences and align with 2024 government take of 60–85% and local content targets ~30–40%. JVs and farm‑ins share geological risk and capex, supporting 26,000 boe/d (2024). EPC and service contractors (30–50% of dev capex) drive delivery; financiers (RBL, prepayments) and insurers underpin liquidity and risk mitigation.

| Partner | 2024 Metric |

|---|---|

| Govt/NOC | Take 60–85% / Local content 30–40% |

| Production | 26,000 boe/d |

| Capex | EPC 30–50% |

| Finance | RBL + prepayments core |

What is included in the product

A concise, pre-written Business Model Canvas for Panoro Energy mapping its 9 blocks—customer segments, value propositions, channels, revenue streams, key resources, partners, activities, cost structure, and customer relationships—aligned to its Africa-focused E&P strategy, asset-led production growth, low-cost operations and JV partnerships; ideal for investor presentations, strategic planning, and competitive analysis.

High-level view of Panoro Energy’s business model with editable cells — quickly identify asset portfolios, revenue drivers, and cost pressures on one page to relieve analysis bottlenecks for teams and investors.

Activities

Exploration and appraisal

Exploration and appraisal de-risk prospects for Panoro Energy through seismic acquisition, integrated geoscience and targeted appraisal drilling to convert leads into commercial resources. Portfolio screening balances geological risk, basin maturity and cycle time to prioritize capital deployment and farm-down opportunities. Continuous data integration and learning from 2024 appraisal campaigns sharpen well targeting, improve resource classification and raise capital efficiency.

Field development and production

Plan and execute wells, facilities and tie-backs to monetize Panoro’s ~27,000 boe/d scale, targeting new tie-backs that can add 5–10 kbbls/d per project; focus on optimizing lift costs to around $10–12/boe, maximizing uptime and managing decline with reservoir-focused interventions. Phased developments align capex with cash flow, cutting near-term funding needs by ~30% per stage, while integrity management and HSE programs protect people, assets and reservoir value.

Commercial and marketing

Panoro negotiates offtake, lifting schedules and pricing formulas to capture value across its ~22,000 boe/d (2024) portfolio, targeting realized oil prices near $72/bl in 2024. It manages quality differentials, blending and logistics to improve realizations by limiting discounts. Term vs spot exposure is structured—roughly 35% hedged in 2024—to balance cash certainty and upside. Strong counterparty vetting and credit controls limit receivable and operational risk.

Portfolio and capital allocation

Panoro recycles capital through targeted acquisitions, farm-ins and selective divestments, prioritising projects by NPV, breakevens and payback to maximise returns; Brent averaged about 90 USD/bbl in 2024, guiding economics and funding capacity. Spend is aligned with commodity cycles and available funding, using staged commitments to maintain optionality and limit downside.

- Recycle capital: acquisitions, farm-ins, divestments

- Prioritise: NPV, breakeven, payback

- Align spend: commodity cycles & funding capacity (Brent ~90 USD/bbl 2024)

- Maintain optionality: staged commitments

Risk, HSE, and compliance

Panoro embeds safety, environmental stewardship and regulatory adherence across operations through formal HSE systems and continuous risk assessments; these practices protect asset value and limit operational interruptions. The company uses hedging, insurance and contingency planning to manage price and operational volatility, while proactive community engagement reduces social license risk. Strong governance frameworks ensure ethical, transparent conduct and regulatory compliance.

Monetize ~22k boe/d (2024), tie-backs & $10-12/boe

Explore and appraise to convert prospects into commercial resources across Panoro’s ~27,000 boe/d scale, prioritising risks, cycle time and farm-downs. Execute tie-backs and phased developments to monetize ~22,000 boe/d (2024), targeting $10–12/boe lift costs and ~30% lower near-term capex per stage. Manage offtake, hedging (~35% 2024) and logistics to realize ~$72/bl (2024) versus Brent ~$90.

| Metric | 2024 |

|---|---|

| Reported production | 22,000 boe/d |

| Portfolio scale | ~27,000 boe/d |

| Realized oil price | $72/bl |

| Brent | $90/bl |

| Hedged | 35% |

| Lift cost | $10–12/boe |

Full Version Awaits

Business Model Canvas

The Panoro Energy Business Model Canvas you see here is the actual deliverable, not a mockup; it’s a direct snapshot of the file you’ll receive after purchase. On completion, you’ll get this same ready-to-use, editable document in Word and Excel formats with all sections included—no surprises.

Original: $10.00

-65%$10.00

$3.50Description

Business Model Canvas: Exploration, Asset Optimization & Partner-Led Value Drivers

Unlock the strategic core of Panoro Energy with our concise Business Model Canvas—showing how exploration, asset optimization and partner-led development drive value and revenue. This practical snapshot highlights key partners, cost drivers and growth levers. Purchase the full Canvas for a detailed, editable plan ready for investor decks and strategic use.

Partnerships

Host governments and NOCs

Panoro’s concessions and production‑sharing agreements require strong ties with host ministries and NOCs; government take in African PSAs typically ranges 60–85% (2024). These partners enable access, approvals and stable operating frameworks that underpin licence security and continuity. Transparent engagement reduces dispute risk and supports uninterrupted production. Aligning local content with host targets — often 30–40% skilled local hire goals in 2024 — strengthens legitimacy and resilience.

Joint-venture and farm-in partners

Panoro leverages joint ventures and farm‑ins to share geological risk and capital load, with 2024 partnerships across West Africa reducing operator capital commitments and accelerating development timelines. Farm‑ins/farm‑outs optimize portfolio balance and funding while joint operating committees enforce technical governance and execution discipline. Diverse partners expand optionality across exploration, appraisal and production phases.

Oilfield services and EPC contractors

Drilling, subsea, seismic and EPC partners are critical to safe, timely execution for Panoro Energy’s West Africa developments, with EPC packages typically representing 30–50% of upstream development capex. Performance-based contracts align incentives and industry practice has reduced schedule overruns by notable margins. Robust vendor ecosystems enable ~20% faster scaling across cycles, while local suppliers meet 30–60% local content mandates in the region.

Offtakers, traders, and refiners

Sales partners provide market access, lifting services and pricing benchmarks, supporting Panoro Energy’s average 2024 sales of ~26,000 boe/d; term contracts (covering core volumes) stabilize cash flow while spot trades capture upside; blending and logistics support improve netbacks and reliable counterparties reduce lifting and payment risk.

- Market access: lifting services/pricing

- Hedge mix: term stability + spot upside

- Ops: blending/logistics raise netbacks

- Counterparty quality lowers lifting/payment risk

Banks, commodity financiers, and insurers

Reserve-based lending, prepayment facilities and trade finance underpinned Panoro Energy’s 2024 capital needs, enabling project funding and near-term liquidity; hedging providers (fixed-price and collar structures) reduced realized price volatility; insurers and export credit agencies mitigated operational and political risk, supporting access to international financing; a mix of banks, commodity financiers and insurers enables disciplined growth.

- PNR listed on Oslo Børs (PNR)

- Reserve-based lending + prepayments = core liquidity tools (2024)

- Hedging and insurance lower revenue and political risk

Govt/NOC JVs: 60–85% take, 30–40% local; support 26,000 boe/d

Panoro’s key partnerships with host governments and NOCs secure licences and align with 2024 government take of 60–85% and local content targets ~30–40%. JVs and farm‑ins share geological risk and capex, supporting 26,000 boe/d (2024). EPC and service contractors (30–50% of dev capex) drive delivery; financiers (RBL, prepayments) and insurers underpin liquidity and risk mitigation.

| Partner | 2024 Metric |

|---|---|

| Govt/NOC | Take 60–85% / Local content 30–40% |

| Production | 26,000 boe/d |

| Capex | EPC 30–50% |

| Finance | RBL + prepayments core |

What is included in the product

A concise, pre-written Business Model Canvas for Panoro Energy mapping its 9 blocks—customer segments, value propositions, channels, revenue streams, key resources, partners, activities, cost structure, and customer relationships—aligned to its Africa-focused E&P strategy, asset-led production growth, low-cost operations and JV partnerships; ideal for investor presentations, strategic planning, and competitive analysis.

High-level view of Panoro Energy’s business model with editable cells — quickly identify asset portfolios, revenue drivers, and cost pressures on one page to relieve analysis bottlenecks for teams and investors.

Activities

Exploration and appraisal

Exploration and appraisal de-risk prospects for Panoro Energy through seismic acquisition, integrated geoscience and targeted appraisal drilling to convert leads into commercial resources. Portfolio screening balances geological risk, basin maturity and cycle time to prioritize capital deployment and farm-down opportunities. Continuous data integration and learning from 2024 appraisal campaigns sharpen well targeting, improve resource classification and raise capital efficiency.

Field development and production

Plan and execute wells, facilities and tie-backs to monetize Panoro’s ~27,000 boe/d scale, targeting new tie-backs that can add 5–10 kbbls/d per project; focus on optimizing lift costs to around $10–12/boe, maximizing uptime and managing decline with reservoir-focused interventions. Phased developments align capex with cash flow, cutting near-term funding needs by ~30% per stage, while integrity management and HSE programs protect people, assets and reservoir value.

Commercial and marketing

Panoro negotiates offtake, lifting schedules and pricing formulas to capture value across its ~22,000 boe/d (2024) portfolio, targeting realized oil prices near $72/bl in 2024. It manages quality differentials, blending and logistics to improve realizations by limiting discounts. Term vs spot exposure is structured—roughly 35% hedged in 2024—to balance cash certainty and upside. Strong counterparty vetting and credit controls limit receivable and operational risk.

Portfolio and capital allocation

Panoro recycles capital through targeted acquisitions, farm-ins and selective divestments, prioritising projects by NPV, breakevens and payback to maximise returns; Brent averaged about 90 USD/bbl in 2024, guiding economics and funding capacity. Spend is aligned with commodity cycles and available funding, using staged commitments to maintain optionality and limit downside.

- Recycle capital: acquisitions, farm-ins, divestments

- Prioritise: NPV, breakeven, payback

- Align spend: commodity cycles & funding capacity (Brent ~90 USD/bbl 2024)

- Maintain optionality: staged commitments

Risk, HSE, and compliance

Panoro embeds safety, environmental stewardship and regulatory adherence across operations through formal HSE systems and continuous risk assessments; these practices protect asset value and limit operational interruptions. The company uses hedging, insurance and contingency planning to manage price and operational volatility, while proactive community engagement reduces social license risk. Strong governance frameworks ensure ethical, transparent conduct and regulatory compliance.

Monetize ~22k boe/d (2024), tie-backs & $10-12/boe

Explore and appraise to convert prospects into commercial resources across Panoro’s ~27,000 boe/d scale, prioritising risks, cycle time and farm-downs. Execute tie-backs and phased developments to monetize ~22,000 boe/d (2024), targeting $10–12/boe lift costs and ~30% lower near-term capex per stage. Manage offtake, hedging (~35% 2024) and logistics to realize ~$72/bl (2024) versus Brent ~$90.

| Metric | 2024 |

|---|---|

| Reported production | 22,000 boe/d |

| Portfolio scale | ~27,000 boe/d |

| Realized oil price | $72/bl |

| Brent | $90/bl |

| Hedged | 35% |

| Lift cost | $10–12/boe |

Full Version Awaits

Business Model Canvas

The Panoro Energy Business Model Canvas you see here is the actual deliverable, not a mockup; it’s a direct snapshot of the file you’ll receive after purchase. On completion, you’ll get this same ready-to-use, editable document in Word and Excel formats with all sections included—no surprises.