Paris Miki Holdings Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

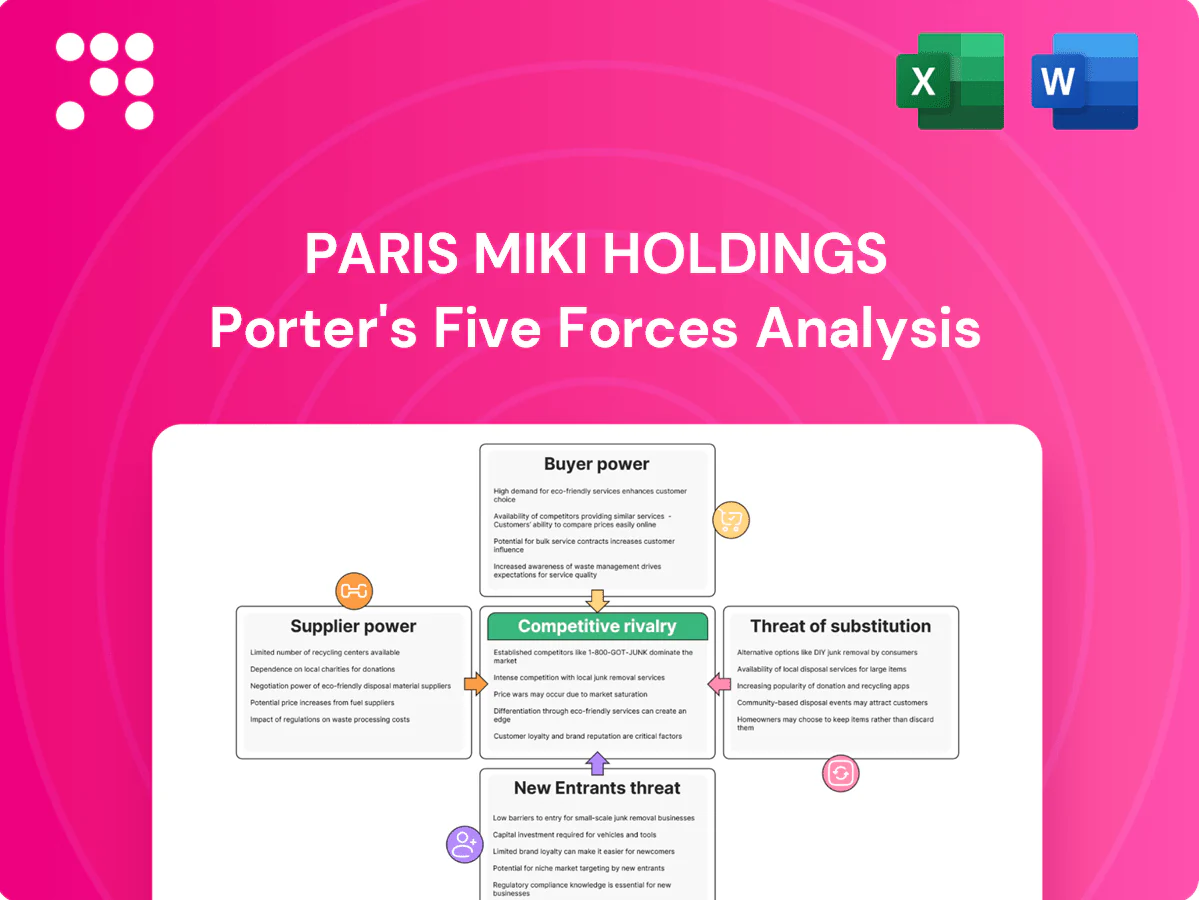

Paris Miki Holdings faces moderate buyer power, niche supplier relationships, and steady barriers to entry due to brand loyalty and retail footprint. Competitive rivalry is intense among optical chains and e-commerce entrants, while substitutes (online eyewear, teleoptometry) are rising. Regulatory and demographic shifts shape long-term demand and margin pressure. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore strategic implications in detail.

Suppliers Bargaining Power

Global lens makers concentrated

High-quality ophthalmic lenses are produced by a few global suppliers—EssilorLuxottica, HOYA and ZEISS—whose combined share exceeds 70%, giving them strong leverage on pricing and contract terms. Proprietary coatings and progressive designs deepen dependency, raising switching costs for Paris Miki. Mitigation options include multi-sourcing, private-label lenses and volume commitments; Paris Miki can negotiate rebates tied to scale. Yen weakness (~¥150/USD in 2023–24) further raises landed costs and supplier power.

Branded frames wield influence

Premium fashion and sports brands control the most desirable SKUs and allocate top models by partner status, concentrating supplier leverage. Limited editions and minimum advertised price policies restrict Paris Miki’s discounting latitude and protect brand positioning. The company must balance strong branded footfall against lower-margin own-label lines to preserve profitability. Exclusive supply agreements can secure inventory but reduce sourcing flexibility and negotiation power.

Contact lens oligopoly dynamics

Major manufacturers (Johnson & Johnson Vision, Alcon, Bausch + Lomb) held roughly 70% of the contact lens market in 2024, allowing them to set price floors and structured rebate programs. Strong regulatory and clinical barriers restrict alternative sourcing and private-label entry. Paris Miki preserves margin through supplier program rebates and category management. Rising subscription models and DTC programs are shifting economics toward retailers and recurring-revenue channels.

Hearing aid manufacturers concentrated

The hearing aid category is dominated by a handful of OEMs (Sonova, WS Audiology, GN Hearing, Demant) that held roughly 75% global market share in 2024, and their proprietary fitting software and firmware lock-ins raise effective switching costs for retailers. Device shortages and lead times in 2023–24 pushed replacement cycles and can force retailers into unfavorable pricing. Paris Miki can negotiate bundled hardware+service deals and service-based margins to blunt hardware supplier power while vertical tie-ins with audiology platforms still influence contract terms.

- Market share: ~75% (2024)

- Lead times: 8–12 weeks in 2023–24

- Mitigation: bundle services, margin on fittings

- Risk: firmware lock-in, platform tie-ins

Logistics and lab capacity constraints

Edge polishing, surfacing labs and coating lines can bottleneck during seasonal peaks, extending turnaround by 2–6 weeks and raising per-unit processing costs. Cross-border freight volatility in 2023–24 produced 10–30% swings in landed costs and shifted lead times unpredictably. In-house labs cut supplier power but require capex and >60% utilization to be cost-effective; nearshoring partners reduce disruption risk.

- Capacity: lab bottlenecks => 2–6 week delays

- Freight: 10–30% landed cost variance (2023–24)

- In-house: needs significant capex and >60% utilization

- Nearshoring: lowers cross-border disruption risk

Top lens suppliers >70%: pricing power amid freight swings and 2–6 week lab delays

Suppliers concentrated: top lens makers >70% (2024), contact lens OEMs ~70% and hearing aid OEMs ~75% (2024), giving strong pricing leverage and lock‑ins. Freight volatility (10–30% landed cost swings 2023–24) and lab bottlenecks (2–6 week delays) raise costs. Mitigations: private label, multi‑sourcing, in‑house labs (>60% utilization).

| Metric | Value |

|---|---|

| Top lens share | >70% (2024) |

| Contact lens OEMs | ~70% (2024) |

| Hearing OEMs | ~75% (2024) |

| Freight volatility | 10–30% (2023–24) |

| Lab delays | 2–6 weeks |

What is included in the product

Tailored Porter's Five Forces analysis for Paris Miki Holdings, revealing competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and highlighting disruptive risks and defensive barriers to protect market share.

Clear one-sheet Porter's Five Forces for Paris Miki Holdings—rapidly spot retail eyewear pressures (suppliers, buyers, substitutes, entrants, rivalry) to ease strategic decisions and update pressure levels as market shifts occur.

Customers Bargaining Power

Price-sensitive mass buyers

Price-sensitive mass buyers comparison-shop across chains and online, with online channels capturing roughly 20% of eyewear sales in 2024, intensifying downward pressure on Paris Miki’s margins. Transparent pricing for frames and lenses amplifies customers’ bargaining power and shortens decision cycles. Bundles and tiered offerings (value, mid, premium) help recapture value per transaction. Loyalty plans and membership discounts reduce churn and raise repeat-purchase rates.

Insurance and corporate plans

As of 2024, vision benefits and corporate contracts largely set fee schedules and reimbursement ceilings, constraining retail pricing for Paris Miki. Network inclusion decisions by plan administrators directly affect store traffic and realized margins. Paris Miki must optimize its corporate plan mix and actively upsell premium lens and service add-ons to improve ASPs. Excessive claim friction risks deterring buyer renewals and corporate partnerships.

High information availability

High information availability raises buyer knowledge: global e-commerce penetration reached about 22% in 2024, fueling review-driven purchase decisions and widespread use of AR try-on tools. Customers increasingly demand fast delivery and clear warranty terms, with surveys showing roughly 60% expect same- or next-day options. Paris Miki must articulate clear value stories on coatings and lens tech; service differentiation can justify premium pricing.

Switching costs are moderate

Switching costs for Paris Miki customers are moderate: prescriptions can be filled elsewhere with limited friction, but repeat purchases depend heavily on frame fit and aftercare quality. Warranty, free adjustments and servicing increase customer stickiness, while subscription or auto-ship contact lens programs further reduce churn.

- Limited friction to switch

- Aftercare drives loyalty

- Warranty/servicing raises stickiness

- Auto-ship lowers churn

Premium segment less price elastic

Affluent buyers of premium eyewear prioritize fashion, craftsmanship and personalization, making demand less price elastic and reducing direct price pressure while increasing expectations for concierge-level service. Limited editions and bespoke fittings can raise ARPU by roughly 2–3x versus mass-market SKUs, and clienteling tools (CRM, appointmenting) measurably extend lifetime value.

- Lower elasticity: higher margin resilience

- Service intensity: increased operating costs

- Limited editions: higher ARPU (≈2–3x)

- Clienteling: boosts retention and LTV

Prioritize upsells, subscriptions and limited editions as 22% online sales compress margins

Customers are price-sensitive: online/omnichannel sales ~22% in 2024, intensifying margin pressure and shortening decision cycles. Corporate vision plans constrain retail pricing, so upsells (premium lenses/services) are needed to lift ASPs. Warranty, aftercare and subscriptions increase stickiness; limited editions yield ≈2–3x ARPU versus mass SKUs.

| Metric | 2024 value | Impact |

|---|---|---|

| Online/omnichannel share | ≈22% | Higher price competition |

| Same/next-day expectation | ≈60% | Service differentiation needed |

| Premium ARPU uplift | ≈2–3x | Margin resilience |

Full Version Awaits

Paris Miki Holdings Porter's Five Forces Analysis

This preview shows the Paris Miki Holdings Porter’s Five Forces analysis exactly as delivered—comprehensive industry rivalry, supplier and buyer power, threat of new entrants and substitutes. The document you see is the final, fully formatted file you’ll receive instantly after purchase. No placeholders, no mockups—ready for immediate download and use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Paris Miki Holdings faces moderate buyer power, niche supplier relationships, and steady barriers to entry due to brand loyalty and retail footprint. Competitive rivalry is intense among optical chains and e-commerce entrants, while substitutes (online eyewear, teleoptometry) are rising. Regulatory and demographic shifts shape long-term demand and margin pressure. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore strategic implications in detail.

Suppliers Bargaining Power

Global lens makers concentrated

High-quality ophthalmic lenses are produced by a few global suppliers—EssilorLuxottica, HOYA and ZEISS—whose combined share exceeds 70%, giving them strong leverage on pricing and contract terms. Proprietary coatings and progressive designs deepen dependency, raising switching costs for Paris Miki. Mitigation options include multi-sourcing, private-label lenses and volume commitments; Paris Miki can negotiate rebates tied to scale. Yen weakness (~¥150/USD in 2023–24) further raises landed costs and supplier power.

Branded frames wield influence

Premium fashion and sports brands control the most desirable SKUs and allocate top models by partner status, concentrating supplier leverage. Limited editions and minimum advertised price policies restrict Paris Miki’s discounting latitude and protect brand positioning. The company must balance strong branded footfall against lower-margin own-label lines to preserve profitability. Exclusive supply agreements can secure inventory but reduce sourcing flexibility and negotiation power.

Contact lens oligopoly dynamics

Major manufacturers (Johnson & Johnson Vision, Alcon, Bausch + Lomb) held roughly 70% of the contact lens market in 2024, allowing them to set price floors and structured rebate programs. Strong regulatory and clinical barriers restrict alternative sourcing and private-label entry. Paris Miki preserves margin through supplier program rebates and category management. Rising subscription models and DTC programs are shifting economics toward retailers and recurring-revenue channels.

Hearing aid manufacturers concentrated

The hearing aid category is dominated by a handful of OEMs (Sonova, WS Audiology, GN Hearing, Demant) that held roughly 75% global market share in 2024, and their proprietary fitting software and firmware lock-ins raise effective switching costs for retailers. Device shortages and lead times in 2023–24 pushed replacement cycles and can force retailers into unfavorable pricing. Paris Miki can negotiate bundled hardware+service deals and service-based margins to blunt hardware supplier power while vertical tie-ins with audiology platforms still influence contract terms.

- Market share: ~75% (2024)

- Lead times: 8–12 weeks in 2023–24

- Mitigation: bundle services, margin on fittings

- Risk: firmware lock-in, platform tie-ins

Logistics and lab capacity constraints

Edge polishing, surfacing labs and coating lines can bottleneck during seasonal peaks, extending turnaround by 2–6 weeks and raising per-unit processing costs. Cross-border freight volatility in 2023–24 produced 10–30% swings in landed costs and shifted lead times unpredictably. In-house labs cut supplier power but require capex and >60% utilization to be cost-effective; nearshoring partners reduce disruption risk.

- Capacity: lab bottlenecks => 2–6 week delays

- Freight: 10–30% landed cost variance (2023–24)

- In-house: needs significant capex and >60% utilization

- Nearshoring: lowers cross-border disruption risk

Top lens suppliers >70%: pricing power amid freight swings and 2–6 week lab delays

Suppliers concentrated: top lens makers >70% (2024), contact lens OEMs ~70% and hearing aid OEMs ~75% (2024), giving strong pricing leverage and lock‑ins. Freight volatility (10–30% landed cost swings 2023–24) and lab bottlenecks (2–6 week delays) raise costs. Mitigations: private label, multi‑sourcing, in‑house labs (>60% utilization).

| Metric | Value |

|---|---|

| Top lens share | >70% (2024) |

| Contact lens OEMs | ~70% (2024) |

| Hearing OEMs | ~75% (2024) |

| Freight volatility | 10–30% (2023–24) |

| Lab delays | 2–6 weeks |

What is included in the product

Tailored Porter's Five Forces analysis for Paris Miki Holdings, revealing competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and highlighting disruptive risks and defensive barriers to protect market share.

Clear one-sheet Porter's Five Forces for Paris Miki Holdings—rapidly spot retail eyewear pressures (suppliers, buyers, substitutes, entrants, rivalry) to ease strategic decisions and update pressure levels as market shifts occur.

Customers Bargaining Power

Price-sensitive mass buyers

Price-sensitive mass buyers comparison-shop across chains and online, with online channels capturing roughly 20% of eyewear sales in 2024, intensifying downward pressure on Paris Miki’s margins. Transparent pricing for frames and lenses amplifies customers’ bargaining power and shortens decision cycles. Bundles and tiered offerings (value, mid, premium) help recapture value per transaction. Loyalty plans and membership discounts reduce churn and raise repeat-purchase rates.

Insurance and corporate plans

As of 2024, vision benefits and corporate contracts largely set fee schedules and reimbursement ceilings, constraining retail pricing for Paris Miki. Network inclusion decisions by plan administrators directly affect store traffic and realized margins. Paris Miki must optimize its corporate plan mix and actively upsell premium lens and service add-ons to improve ASPs. Excessive claim friction risks deterring buyer renewals and corporate partnerships.

High information availability

High information availability raises buyer knowledge: global e-commerce penetration reached about 22% in 2024, fueling review-driven purchase decisions and widespread use of AR try-on tools. Customers increasingly demand fast delivery and clear warranty terms, with surveys showing roughly 60% expect same- or next-day options. Paris Miki must articulate clear value stories on coatings and lens tech; service differentiation can justify premium pricing.

Switching costs are moderate

Switching costs for Paris Miki customers are moderate: prescriptions can be filled elsewhere with limited friction, but repeat purchases depend heavily on frame fit and aftercare quality. Warranty, free adjustments and servicing increase customer stickiness, while subscription or auto-ship contact lens programs further reduce churn.

- Limited friction to switch

- Aftercare drives loyalty

- Warranty/servicing raises stickiness

- Auto-ship lowers churn

Premium segment less price elastic

Affluent buyers of premium eyewear prioritize fashion, craftsmanship and personalization, making demand less price elastic and reducing direct price pressure while increasing expectations for concierge-level service. Limited editions and bespoke fittings can raise ARPU by roughly 2–3x versus mass-market SKUs, and clienteling tools (CRM, appointmenting) measurably extend lifetime value.

- Lower elasticity: higher margin resilience

- Service intensity: increased operating costs

- Limited editions: higher ARPU (≈2–3x)

- Clienteling: boosts retention and LTV

Prioritize upsells, subscriptions and limited editions as 22% online sales compress margins

Customers are price-sensitive: online/omnichannel sales ~22% in 2024, intensifying margin pressure and shortening decision cycles. Corporate vision plans constrain retail pricing, so upsells (premium lenses/services) are needed to lift ASPs. Warranty, aftercare and subscriptions increase stickiness; limited editions yield ≈2–3x ARPU versus mass SKUs.

| Metric | 2024 value | Impact |

|---|---|---|

| Online/omnichannel share | ≈22% | Higher price competition |

| Same/next-day expectation | ≈60% | Service differentiation needed |

| Premium ARPU uplift | ≈2–3x | Margin resilience |

Full Version Awaits

Paris Miki Holdings Porter's Five Forces Analysis

This preview shows the Paris Miki Holdings Porter’s Five Forces analysis exactly as delivered—comprehensive industry rivalry, supplier and buyer power, threat of new entrants and substitutes. The document you see is the final, fully formatted file you’ll receive instantly after purchase. No placeholders, no mockups—ready for immediate download and use.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Paris Miki Holdings faces moderate buyer power, niche supplier relationships, and steady barriers to entry due to brand loyalty and retail footprint. Competitive rivalry is intense among optical chains and e-commerce entrants, while substitutes (online eyewear, teleoptometry) are rising. Regulatory and demographic shifts shape long-term demand and margin pressure. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore strategic implications in detail.

Suppliers Bargaining Power

Global lens makers concentrated

High-quality ophthalmic lenses are produced by a few global suppliers—EssilorLuxottica, HOYA and ZEISS—whose combined share exceeds 70%, giving them strong leverage on pricing and contract terms. Proprietary coatings and progressive designs deepen dependency, raising switching costs for Paris Miki. Mitigation options include multi-sourcing, private-label lenses and volume commitments; Paris Miki can negotiate rebates tied to scale. Yen weakness (~¥150/USD in 2023–24) further raises landed costs and supplier power.

Branded frames wield influence

Premium fashion and sports brands control the most desirable SKUs and allocate top models by partner status, concentrating supplier leverage. Limited editions and minimum advertised price policies restrict Paris Miki’s discounting latitude and protect brand positioning. The company must balance strong branded footfall against lower-margin own-label lines to preserve profitability. Exclusive supply agreements can secure inventory but reduce sourcing flexibility and negotiation power.

Contact lens oligopoly dynamics

Major manufacturers (Johnson & Johnson Vision, Alcon, Bausch + Lomb) held roughly 70% of the contact lens market in 2024, allowing them to set price floors and structured rebate programs. Strong regulatory and clinical barriers restrict alternative sourcing and private-label entry. Paris Miki preserves margin through supplier program rebates and category management. Rising subscription models and DTC programs are shifting economics toward retailers and recurring-revenue channels.

Hearing aid manufacturers concentrated

The hearing aid category is dominated by a handful of OEMs (Sonova, WS Audiology, GN Hearing, Demant) that held roughly 75% global market share in 2024, and their proprietary fitting software and firmware lock-ins raise effective switching costs for retailers. Device shortages and lead times in 2023–24 pushed replacement cycles and can force retailers into unfavorable pricing. Paris Miki can negotiate bundled hardware+service deals and service-based margins to blunt hardware supplier power while vertical tie-ins with audiology platforms still influence contract terms.

- Market share: ~75% (2024)

- Lead times: 8–12 weeks in 2023–24

- Mitigation: bundle services, margin on fittings

- Risk: firmware lock-in, platform tie-ins

Logistics and lab capacity constraints

Edge polishing, surfacing labs and coating lines can bottleneck during seasonal peaks, extending turnaround by 2–6 weeks and raising per-unit processing costs. Cross-border freight volatility in 2023–24 produced 10–30% swings in landed costs and shifted lead times unpredictably. In-house labs cut supplier power but require capex and >60% utilization to be cost-effective; nearshoring partners reduce disruption risk.

- Capacity: lab bottlenecks => 2–6 week delays

- Freight: 10–30% landed cost variance (2023–24)

- In-house: needs significant capex and >60% utilization

- Nearshoring: lowers cross-border disruption risk

Top lens suppliers >70%: pricing power amid freight swings and 2–6 week lab delays

Suppliers concentrated: top lens makers >70% (2024), contact lens OEMs ~70% and hearing aid OEMs ~75% (2024), giving strong pricing leverage and lock‑ins. Freight volatility (10–30% landed cost swings 2023–24) and lab bottlenecks (2–6 week delays) raise costs. Mitigations: private label, multi‑sourcing, in‑house labs (>60% utilization).

| Metric | Value |

|---|---|

| Top lens share | >70% (2024) |

| Contact lens OEMs | ~70% (2024) |

| Hearing OEMs | ~75% (2024) |

| Freight volatility | 10–30% (2023–24) |

| Lab delays | 2–6 weeks |

What is included in the product

Tailored Porter's Five Forces analysis for Paris Miki Holdings, revealing competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and highlighting disruptive risks and defensive barriers to protect market share.

Clear one-sheet Porter's Five Forces for Paris Miki Holdings—rapidly spot retail eyewear pressures (suppliers, buyers, substitutes, entrants, rivalry) to ease strategic decisions and update pressure levels as market shifts occur.

Customers Bargaining Power

Price-sensitive mass buyers

Price-sensitive mass buyers comparison-shop across chains and online, with online channels capturing roughly 20% of eyewear sales in 2024, intensifying downward pressure on Paris Miki’s margins. Transparent pricing for frames and lenses amplifies customers’ bargaining power and shortens decision cycles. Bundles and tiered offerings (value, mid, premium) help recapture value per transaction. Loyalty plans and membership discounts reduce churn and raise repeat-purchase rates.

Insurance and corporate plans

As of 2024, vision benefits and corporate contracts largely set fee schedules and reimbursement ceilings, constraining retail pricing for Paris Miki. Network inclusion decisions by plan administrators directly affect store traffic and realized margins. Paris Miki must optimize its corporate plan mix and actively upsell premium lens and service add-ons to improve ASPs. Excessive claim friction risks deterring buyer renewals and corporate partnerships.

High information availability

High information availability raises buyer knowledge: global e-commerce penetration reached about 22% in 2024, fueling review-driven purchase decisions and widespread use of AR try-on tools. Customers increasingly demand fast delivery and clear warranty terms, with surveys showing roughly 60% expect same- or next-day options. Paris Miki must articulate clear value stories on coatings and lens tech; service differentiation can justify premium pricing.

Switching costs are moderate

Switching costs for Paris Miki customers are moderate: prescriptions can be filled elsewhere with limited friction, but repeat purchases depend heavily on frame fit and aftercare quality. Warranty, free adjustments and servicing increase customer stickiness, while subscription or auto-ship contact lens programs further reduce churn.

- Limited friction to switch

- Aftercare drives loyalty

- Warranty/servicing raises stickiness

- Auto-ship lowers churn

Premium segment less price elastic

Affluent buyers of premium eyewear prioritize fashion, craftsmanship and personalization, making demand less price elastic and reducing direct price pressure while increasing expectations for concierge-level service. Limited editions and bespoke fittings can raise ARPU by roughly 2–3x versus mass-market SKUs, and clienteling tools (CRM, appointmenting) measurably extend lifetime value.

- Lower elasticity: higher margin resilience

- Service intensity: increased operating costs

- Limited editions: higher ARPU (≈2–3x)

- Clienteling: boosts retention and LTV

Prioritize upsells, subscriptions and limited editions as 22% online sales compress margins

Customers are price-sensitive: online/omnichannel sales ~22% in 2024, intensifying margin pressure and shortening decision cycles. Corporate vision plans constrain retail pricing, so upsells (premium lenses/services) are needed to lift ASPs. Warranty, aftercare and subscriptions increase stickiness; limited editions yield ≈2–3x ARPU versus mass SKUs.

| Metric | 2024 value | Impact |

|---|---|---|

| Online/omnichannel share | ≈22% | Higher price competition |

| Same/next-day expectation | ≈60% | Service differentiation needed |

| Premium ARPU uplift | ≈2–3x | Margin resilience |

Full Version Awaits

Paris Miki Holdings Porter's Five Forces Analysis

This preview shows the Paris Miki Holdings Porter’s Five Forces analysis exactly as delivered—comprehensive industry rivalry, supplier and buyer power, threat of new entrants and substitutes. The document you see is the final, fully formatted file you’ll receive instantly after purchase. No placeholders, no mockups—ready for immediate download and use.