Passage Bio PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our PESTLE Analysis of Passage Bio—uncover how political, economic, social, technological, legal, and environmental forces shape its trajectory. Ideal for investors and strategists, this ready-to-use report delivers actionable insights and forecasts. Purchase the full analysis now to access the complete, editable intelligence you need to make confident decisions.

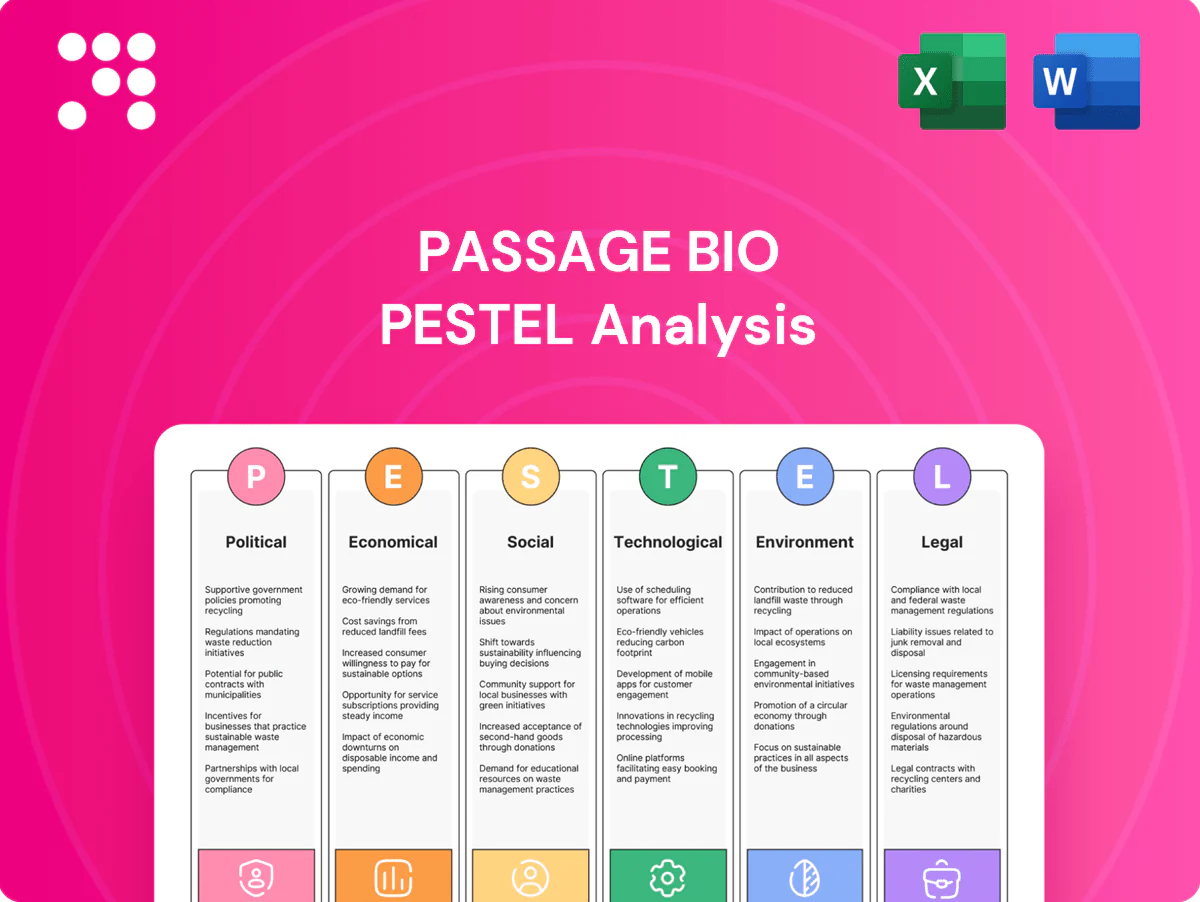

Political factors

Global orphan-drug incentives

US, EU and key Asian regimes grant orphan incentives—US 7-year market exclusivity, EU 10 years, Japan 10 years—plus US orphan drug tax credit ~25% of clinical costs and FDA user-fee waivers worth ~3.3M per filing (2024). These incentives can shorten time-to-market and boost ROI for Passage Bio programs. Changes in health budgets or law could expand or curtail benefits, so monitoring legislative updates is critical.

Regulatory alignment (FDA/EMA) on gene therapy

Convergence of guidance on AAV safety, dosing and long-term follow-up—highlighted by FDA final long‑term follow‑up guidance (2020)—shapes Passage Bio trial design and can accelerate approvals. Harmonized expectations reduce duplicated studies across regions, as seen in cross‑border uptake after Luxturna (2017) and Zolgensma (2019). Divergent stances on durability endpoints or neurotropic vectors could delay global rollouts, so early scientific advice and parallel submissions to FDA and EMA are used to mitigate misalignment.

Government funding for neuroscience and rare diseases

Public grants and translational initiatives de-risk preclinical platforms by underwriting early costs; NIH’s ~$49 billion FY2024 budget and the EU’s Horizon Europe €95.5 billion program sustain translational pipelines. Shifts in NIH/EU priorities reshape academic partnerships and pipeline breadth, and political cycles can redirect appropriations away from gene therapy or CNS research. Diversifying collaborations across academia, biotechs and regions cushions Passage Bio against funding swings.

Trade policy and biomanufacturing inputs

Tariffs, export controls (notably US Commerce Department measures tightened in 2023–24) and sanctions can disrupt access to plasmids, capsids and single-use hardware, driving multi-week to multi-month lead times and higher COGS for Passage Bio. Supply concentrated in specific regions amplifies price volatility and logistical risk; proactive supplier diversification and onshoring reduce exposure. Engagement with trade bodies helps anticipate rule changes and shape compliance timelines.

- Tariffs/export controls: tighten access, raise costs

- Concentration risk: longer lead times, higher volatility

- Mitigation: diversify suppliers, domestic sourcing

- Policy action: engage trade bodies to anticipate rules

Healthcare reform and pricing scrutiny

Political pressure on high-cost therapies is increasing value-for-money assessments and outcomes-based contracts; Passage Bio may face mandated discounts or installment pricing as payers push back (Medicare negotiation under the IRA estimated to save about $98 billion over a decade). Gene therapies priced up to $2.125M (Zolgensma) show why national formularies wield leverage and why clear long-term benefit evidence is vital.

- Pressure: IRA negotiation ~$98B/10y

- Price precedent: Zolgensma $2.125M

- Risk: mandated discounts/installments

- Need: robust long-term outcomes data

Orphan exclusivity (7/10/10), $98B funding, trade risks push outcomes‑based pricing

US/EU/Japan orphan exclusivity (7/10/10 yrs), US orphan tax credit ~25% and FDA user‑fee waivers ~$3.3M improve Passage Bio ROI; NIH FY2024 $49B and Horizon Europe €95.5B underwrite translational risk. Trade/export controls tightened 2023–24 raise COGS and lead times; supplier diversification/onshoring mitigates. Payer pressure (IRA ~$98B/10y) and price precedent (Zolgensma $2.125M) push outcomes‑based deals.

| Factor | Key data |

|---|---|

| Orphan incentives | US7y/EU10y/JPN10y; tax credit ~25%; FDA waiver ~$3.3M |

| Funding | NIH $49B FY24; Horizon €95.5B |

| Trade risk | Controls 2023–24 → higher COGS/lead times |

| Payer pressure | IRA ~$98B/10y; Zolgensma $2.125M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Passage Bio across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, investors, and strategists. Delivered in a clean, ready-to-use format with forward-looking insights to support scenario planning and funding strategy.

A concise, visually segmented PESTLE summary for Passage Bio that’s easily dropped into presentations, editable for regional or program-specific notes, and shareable across teams to align quickly on external risks, regulatory shifts, and market positioning.

Economic factors

Capital intensity and cash runway

Gene therapy programs typically entail multi-year trials and CMC spend in the tens-to-low-hundreds of millions of dollars, stressing Passage Bio’s liquidity and runway. Higher interest rates and equity market weakness compress fundraising windows and valuation, while disciplined portfolio prioritization can extend runway without diluting core assets. Non-dilutive options—grants, milestones, royalty deals—can buffer cyclical capital markets.

Payer willingness-to-pay for one-time therapies

Budget impact and durability evidence drive payer willingness-to-pay for one-time rare-disease therapies: NICE typically applies 20,000–30,000 GBP/QALY (HST routes accept higher ICERs), while US benchmarks center around 100,000–150,000 USD/QALY, pressuring prices where long-term durability is unproven.

Outcomes-based agreements — increasingly used post-2020 — let payers tie payment to real-world performance, reducing upfront budget risk and aligning cost with clinical value.

Regional HTA frameworks (NICE, G-BA) routinely compress prices versus the US through strict cost-effectiveness and rebate negotiations; early health-economics modeling provides sustainable price anchors for negotiations and budget planning.

Strategic partnerships and licensing

Co-development and CMC alliances allow Passage Bio to spread technical and commercial risk and accelerate manufacturing scale-up, reducing time-to-clinic for AAV programs and lowering capex burden. Upfront payments and milestone structures from partners bolster near-term balance sheets while aligning shared upside on late-stage success. Deal economics hinge on asset maturity and competitive landscape, so retaining core-market rights preserves long-term value for shareholders.

Manufacturing scale and cost curves

Improvements in AAV yields, vector purity and batch success have driven industry COGS down, with published estimates suggesting 30–50% COGS reduction as processes mature and yields double to triple. Scale economies—especially beyond 200–1,000 L—can cut per-dose manufacturing costs by roughly 30–40%, improving margins as volumes rise. Technology choices (suspension vs adherent; baculo/Sf9 vs transient HEK293) can shift upstream unit costs by ~20–35%, and early CMC decisions typically lock in these long-run cost trajectories.

- Yield/purity gains: 30–50% COGS reduction

- Scale effects: ~30–40% per-dose cost cut >200–1,000 L

- Platform impact: 20–35% unit-cost variance (baculo vs transient)

- Early CMC: commits multi-year cost path

Currency and global launch sequencing

Passage Bio faces USD/EUR/GBP FX exposure as revenues, manufacturing and royalties span regions; EUR/USD averaged ~1.09 and GBP/USD ~1.27 in 2024, so FX moves can swing reported EPS and NPV materially. Prioritizing high-value launches (US first) raises NPV—US gene therapy list prices often exceed $1m (Zolgensma $2.125m)—but requires supply readiness, aligned reimbursement timetables and patient concentration planning; hedging and natural currency offsets can stabilize cash flows.

- FX rates: EUR/USD 2024 avg 1.09; GBP/USD 2024 avg 1.27

- High-value-first: US launch ups NPV; gene therapy prices >$1m

- Mitigation: financial hedges + operational offsets

- Sequencing based on reimbursement timing and patient clusters

Orphan exclusivity (7/10/10), $98B funding, trade risks push outcomes‑based pricing

High upfront CMC and trial costs strain liquidity; disciplined prioritization and non-dilutive grants/milestones are critical as 2024 rates and weak equity markets tighten fundraising. Payer thresholds (UK 20–30k GBP/QALY; US 100–150k USD/QALY) and outcomes-based deals shape pricing for one-time gene therapies often >$1m (Zolgensma $2.125m). Manufacturing tech and scale cut COGS ~30–50% as yields improve; FX (EUR/USD 1.09; GBP/USD 1.27 in 2024) affects reported NPV.

| Metric | Value/Range |

|---|---|

| UK ICER | 20,000–30,000 GBP/QALY |

| US ICER | 100,000–150,000 USD/QALY |

| Gene therapy list price | >1,000,000 USD (Zolgensma 2,125,000) |

| COGS reduction | 30–50% |

| EUR/USD (2024 avg) | 1.09 |

| GBP/USD (2024 avg) | 1.27 |

Preview Before You Purchase

Passage Bio PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Passage Bio PESTLE Analysis provides a structured overview of political, economic, social, technological, legal, and environmental factors affecting the company. No placeholders or teasers—what you see is the final, downloadable file available immediately after checkout.

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our PESTLE Analysis of Passage Bio—uncover how political, economic, social, technological, legal, and environmental forces shape its trajectory. Ideal for investors and strategists, this ready-to-use report delivers actionable insights and forecasts. Purchase the full analysis now to access the complete, editable intelligence you need to make confident decisions.

Political factors

Global orphan-drug incentives

US, EU and key Asian regimes grant orphan incentives—US 7-year market exclusivity, EU 10 years, Japan 10 years—plus US orphan drug tax credit ~25% of clinical costs and FDA user-fee waivers worth ~3.3M per filing (2024). These incentives can shorten time-to-market and boost ROI for Passage Bio programs. Changes in health budgets or law could expand or curtail benefits, so monitoring legislative updates is critical.

Regulatory alignment (FDA/EMA) on gene therapy

Convergence of guidance on AAV safety, dosing and long-term follow-up—highlighted by FDA final long‑term follow‑up guidance (2020)—shapes Passage Bio trial design and can accelerate approvals. Harmonized expectations reduce duplicated studies across regions, as seen in cross‑border uptake after Luxturna (2017) and Zolgensma (2019). Divergent stances on durability endpoints or neurotropic vectors could delay global rollouts, so early scientific advice and parallel submissions to FDA and EMA are used to mitigate misalignment.

Government funding for neuroscience and rare diseases

Public grants and translational initiatives de-risk preclinical platforms by underwriting early costs; NIH’s ~$49 billion FY2024 budget and the EU’s Horizon Europe €95.5 billion program sustain translational pipelines. Shifts in NIH/EU priorities reshape academic partnerships and pipeline breadth, and political cycles can redirect appropriations away from gene therapy or CNS research. Diversifying collaborations across academia, biotechs and regions cushions Passage Bio against funding swings.

Trade policy and biomanufacturing inputs

Tariffs, export controls (notably US Commerce Department measures tightened in 2023–24) and sanctions can disrupt access to plasmids, capsids and single-use hardware, driving multi-week to multi-month lead times and higher COGS for Passage Bio. Supply concentrated in specific regions amplifies price volatility and logistical risk; proactive supplier diversification and onshoring reduce exposure. Engagement with trade bodies helps anticipate rule changes and shape compliance timelines.

- Tariffs/export controls: tighten access, raise costs

- Concentration risk: longer lead times, higher volatility

- Mitigation: diversify suppliers, domestic sourcing

- Policy action: engage trade bodies to anticipate rules

Healthcare reform and pricing scrutiny

Political pressure on high-cost therapies is increasing value-for-money assessments and outcomes-based contracts; Passage Bio may face mandated discounts or installment pricing as payers push back (Medicare negotiation under the IRA estimated to save about $98 billion over a decade). Gene therapies priced up to $2.125M (Zolgensma) show why national formularies wield leverage and why clear long-term benefit evidence is vital.

- Pressure: IRA negotiation ~$98B/10y

- Price precedent: Zolgensma $2.125M

- Risk: mandated discounts/installments

- Need: robust long-term outcomes data

Orphan exclusivity (7/10/10), $98B funding, trade risks push outcomes‑based pricing

US/EU/Japan orphan exclusivity (7/10/10 yrs), US orphan tax credit ~25% and FDA user‑fee waivers ~$3.3M improve Passage Bio ROI; NIH FY2024 $49B and Horizon Europe €95.5B underwrite translational risk. Trade/export controls tightened 2023–24 raise COGS and lead times; supplier diversification/onshoring mitigates. Payer pressure (IRA ~$98B/10y) and price precedent (Zolgensma $2.125M) push outcomes‑based deals.

| Factor | Key data |

|---|---|

| Orphan incentives | US7y/EU10y/JPN10y; tax credit ~25%; FDA waiver ~$3.3M |

| Funding | NIH $49B FY24; Horizon €95.5B |

| Trade risk | Controls 2023–24 → higher COGS/lead times |

| Payer pressure | IRA ~$98B/10y; Zolgensma $2.125M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Passage Bio across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, investors, and strategists. Delivered in a clean, ready-to-use format with forward-looking insights to support scenario planning and funding strategy.

A concise, visually segmented PESTLE summary for Passage Bio that’s easily dropped into presentations, editable for regional or program-specific notes, and shareable across teams to align quickly on external risks, regulatory shifts, and market positioning.

Economic factors

Capital intensity and cash runway

Gene therapy programs typically entail multi-year trials and CMC spend in the tens-to-low-hundreds of millions of dollars, stressing Passage Bio’s liquidity and runway. Higher interest rates and equity market weakness compress fundraising windows and valuation, while disciplined portfolio prioritization can extend runway without diluting core assets. Non-dilutive options—grants, milestones, royalty deals—can buffer cyclical capital markets.

Payer willingness-to-pay for one-time therapies

Budget impact and durability evidence drive payer willingness-to-pay for one-time rare-disease therapies: NICE typically applies 20,000–30,000 GBP/QALY (HST routes accept higher ICERs), while US benchmarks center around 100,000–150,000 USD/QALY, pressuring prices where long-term durability is unproven.

Outcomes-based agreements — increasingly used post-2020 — let payers tie payment to real-world performance, reducing upfront budget risk and aligning cost with clinical value.

Regional HTA frameworks (NICE, G-BA) routinely compress prices versus the US through strict cost-effectiveness and rebate negotiations; early health-economics modeling provides sustainable price anchors for negotiations and budget planning.

Strategic partnerships and licensing

Co-development and CMC alliances allow Passage Bio to spread technical and commercial risk and accelerate manufacturing scale-up, reducing time-to-clinic for AAV programs and lowering capex burden. Upfront payments and milestone structures from partners bolster near-term balance sheets while aligning shared upside on late-stage success. Deal economics hinge on asset maturity and competitive landscape, so retaining core-market rights preserves long-term value for shareholders.

Manufacturing scale and cost curves

Improvements in AAV yields, vector purity and batch success have driven industry COGS down, with published estimates suggesting 30–50% COGS reduction as processes mature and yields double to triple. Scale economies—especially beyond 200–1,000 L—can cut per-dose manufacturing costs by roughly 30–40%, improving margins as volumes rise. Technology choices (suspension vs adherent; baculo/Sf9 vs transient HEK293) can shift upstream unit costs by ~20–35%, and early CMC decisions typically lock in these long-run cost trajectories.

- Yield/purity gains: 30–50% COGS reduction

- Scale effects: ~30–40% per-dose cost cut >200–1,000 L

- Platform impact: 20–35% unit-cost variance (baculo vs transient)

- Early CMC: commits multi-year cost path

Currency and global launch sequencing

Passage Bio faces USD/EUR/GBP FX exposure as revenues, manufacturing and royalties span regions; EUR/USD averaged ~1.09 and GBP/USD ~1.27 in 2024, so FX moves can swing reported EPS and NPV materially. Prioritizing high-value launches (US first) raises NPV—US gene therapy list prices often exceed $1m (Zolgensma $2.125m)—but requires supply readiness, aligned reimbursement timetables and patient concentration planning; hedging and natural currency offsets can stabilize cash flows.

- FX rates: EUR/USD 2024 avg 1.09; GBP/USD 2024 avg 1.27

- High-value-first: US launch ups NPV; gene therapy prices >$1m

- Mitigation: financial hedges + operational offsets

- Sequencing based on reimbursement timing and patient clusters

Orphan exclusivity (7/10/10), $98B funding, trade risks push outcomes‑based pricing

High upfront CMC and trial costs strain liquidity; disciplined prioritization and non-dilutive grants/milestones are critical as 2024 rates and weak equity markets tighten fundraising. Payer thresholds (UK 20–30k GBP/QALY; US 100–150k USD/QALY) and outcomes-based deals shape pricing for one-time gene therapies often >$1m (Zolgensma $2.125m). Manufacturing tech and scale cut COGS ~30–50% as yields improve; FX (EUR/USD 1.09; GBP/USD 1.27 in 2024) affects reported NPV.

| Metric | Value/Range |

|---|---|

| UK ICER | 20,000–30,000 GBP/QALY |

| US ICER | 100,000–150,000 USD/QALY |

| Gene therapy list price | >1,000,000 USD (Zolgensma 2,125,000) |

| COGS reduction | 30–50% |

| EUR/USD (2024 avg) | 1.09 |

| GBP/USD (2024 avg) | 1.27 |

Preview Before You Purchase

Passage Bio PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Passage Bio PESTLE Analysis provides a structured overview of political, economic, social, technological, legal, and environmental factors affecting the company. No placeholders or teasers—what you see is the final, downloadable file available immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our PESTLE Analysis of Passage Bio—uncover how political, economic, social, technological, legal, and environmental forces shape its trajectory. Ideal for investors and strategists, this ready-to-use report delivers actionable insights and forecasts. Purchase the full analysis now to access the complete, editable intelligence you need to make confident decisions.

Political factors

Global orphan-drug incentives

US, EU and key Asian regimes grant orphan incentives—US 7-year market exclusivity, EU 10 years, Japan 10 years—plus US orphan drug tax credit ~25% of clinical costs and FDA user-fee waivers worth ~3.3M per filing (2024). These incentives can shorten time-to-market and boost ROI for Passage Bio programs. Changes in health budgets or law could expand or curtail benefits, so monitoring legislative updates is critical.

Regulatory alignment (FDA/EMA) on gene therapy

Convergence of guidance on AAV safety, dosing and long-term follow-up—highlighted by FDA final long‑term follow‑up guidance (2020)—shapes Passage Bio trial design and can accelerate approvals. Harmonized expectations reduce duplicated studies across regions, as seen in cross‑border uptake after Luxturna (2017) and Zolgensma (2019). Divergent stances on durability endpoints or neurotropic vectors could delay global rollouts, so early scientific advice and parallel submissions to FDA and EMA are used to mitigate misalignment.

Government funding for neuroscience and rare diseases

Public grants and translational initiatives de-risk preclinical platforms by underwriting early costs; NIH’s ~$49 billion FY2024 budget and the EU’s Horizon Europe €95.5 billion program sustain translational pipelines. Shifts in NIH/EU priorities reshape academic partnerships and pipeline breadth, and political cycles can redirect appropriations away from gene therapy or CNS research. Diversifying collaborations across academia, biotechs and regions cushions Passage Bio against funding swings.

Trade policy and biomanufacturing inputs

Tariffs, export controls (notably US Commerce Department measures tightened in 2023–24) and sanctions can disrupt access to plasmids, capsids and single-use hardware, driving multi-week to multi-month lead times and higher COGS for Passage Bio. Supply concentrated in specific regions amplifies price volatility and logistical risk; proactive supplier diversification and onshoring reduce exposure. Engagement with trade bodies helps anticipate rule changes and shape compliance timelines.

- Tariffs/export controls: tighten access, raise costs

- Concentration risk: longer lead times, higher volatility

- Mitigation: diversify suppliers, domestic sourcing

- Policy action: engage trade bodies to anticipate rules

Healthcare reform and pricing scrutiny

Political pressure on high-cost therapies is increasing value-for-money assessments and outcomes-based contracts; Passage Bio may face mandated discounts or installment pricing as payers push back (Medicare negotiation under the IRA estimated to save about $98 billion over a decade). Gene therapies priced up to $2.125M (Zolgensma) show why national formularies wield leverage and why clear long-term benefit evidence is vital.

- Pressure: IRA negotiation ~$98B/10y

- Price precedent: Zolgensma $2.125M

- Risk: mandated discounts/installments

- Need: robust long-term outcomes data

Orphan exclusivity (7/10/10), $98B funding, trade risks push outcomes‑based pricing

US/EU/Japan orphan exclusivity (7/10/10 yrs), US orphan tax credit ~25% and FDA user‑fee waivers ~$3.3M improve Passage Bio ROI; NIH FY2024 $49B and Horizon Europe €95.5B underwrite translational risk. Trade/export controls tightened 2023–24 raise COGS and lead times; supplier diversification/onshoring mitigates. Payer pressure (IRA ~$98B/10y) and price precedent (Zolgensma $2.125M) push outcomes‑based deals.

| Factor | Key data |

|---|---|

| Orphan incentives | US7y/EU10y/JPN10y; tax credit ~25%; FDA waiver ~$3.3M |

| Funding | NIH $49B FY24; Horizon €95.5B |

| Trade risk | Controls 2023–24 → higher COGS/lead times |

| Payer pressure | IRA ~$98B/10y; Zolgensma $2.125M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Passage Bio across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, investors, and strategists. Delivered in a clean, ready-to-use format with forward-looking insights to support scenario planning and funding strategy.

A concise, visually segmented PESTLE summary for Passage Bio that’s easily dropped into presentations, editable for regional or program-specific notes, and shareable across teams to align quickly on external risks, regulatory shifts, and market positioning.

Economic factors

Capital intensity and cash runway

Gene therapy programs typically entail multi-year trials and CMC spend in the tens-to-low-hundreds of millions of dollars, stressing Passage Bio’s liquidity and runway. Higher interest rates and equity market weakness compress fundraising windows and valuation, while disciplined portfolio prioritization can extend runway without diluting core assets. Non-dilutive options—grants, milestones, royalty deals—can buffer cyclical capital markets.

Payer willingness-to-pay for one-time therapies

Budget impact and durability evidence drive payer willingness-to-pay for one-time rare-disease therapies: NICE typically applies 20,000–30,000 GBP/QALY (HST routes accept higher ICERs), while US benchmarks center around 100,000–150,000 USD/QALY, pressuring prices where long-term durability is unproven.

Outcomes-based agreements — increasingly used post-2020 — let payers tie payment to real-world performance, reducing upfront budget risk and aligning cost with clinical value.

Regional HTA frameworks (NICE, G-BA) routinely compress prices versus the US through strict cost-effectiveness and rebate negotiations; early health-economics modeling provides sustainable price anchors for negotiations and budget planning.

Strategic partnerships and licensing

Co-development and CMC alliances allow Passage Bio to spread technical and commercial risk and accelerate manufacturing scale-up, reducing time-to-clinic for AAV programs and lowering capex burden. Upfront payments and milestone structures from partners bolster near-term balance sheets while aligning shared upside on late-stage success. Deal economics hinge on asset maturity and competitive landscape, so retaining core-market rights preserves long-term value for shareholders.

Manufacturing scale and cost curves

Improvements in AAV yields, vector purity and batch success have driven industry COGS down, with published estimates suggesting 30–50% COGS reduction as processes mature and yields double to triple. Scale economies—especially beyond 200–1,000 L—can cut per-dose manufacturing costs by roughly 30–40%, improving margins as volumes rise. Technology choices (suspension vs adherent; baculo/Sf9 vs transient HEK293) can shift upstream unit costs by ~20–35%, and early CMC decisions typically lock in these long-run cost trajectories.

- Yield/purity gains: 30–50% COGS reduction

- Scale effects: ~30–40% per-dose cost cut >200–1,000 L

- Platform impact: 20–35% unit-cost variance (baculo vs transient)

- Early CMC: commits multi-year cost path

Currency and global launch sequencing

Passage Bio faces USD/EUR/GBP FX exposure as revenues, manufacturing and royalties span regions; EUR/USD averaged ~1.09 and GBP/USD ~1.27 in 2024, so FX moves can swing reported EPS and NPV materially. Prioritizing high-value launches (US first) raises NPV—US gene therapy list prices often exceed $1m (Zolgensma $2.125m)—but requires supply readiness, aligned reimbursement timetables and patient concentration planning; hedging and natural currency offsets can stabilize cash flows.

- FX rates: EUR/USD 2024 avg 1.09; GBP/USD 2024 avg 1.27

- High-value-first: US launch ups NPV; gene therapy prices >$1m

- Mitigation: financial hedges + operational offsets

- Sequencing based on reimbursement timing and patient clusters

Orphan exclusivity (7/10/10), $98B funding, trade risks push outcomes‑based pricing

High upfront CMC and trial costs strain liquidity; disciplined prioritization and non-dilutive grants/milestones are critical as 2024 rates and weak equity markets tighten fundraising. Payer thresholds (UK 20–30k GBP/QALY; US 100–150k USD/QALY) and outcomes-based deals shape pricing for one-time gene therapies often >$1m (Zolgensma $2.125m). Manufacturing tech and scale cut COGS ~30–50% as yields improve; FX (EUR/USD 1.09; GBP/USD 1.27 in 2024) affects reported NPV.

| Metric | Value/Range |

|---|---|

| UK ICER | 20,000–30,000 GBP/QALY |

| US ICER | 100,000–150,000 USD/QALY |

| Gene therapy list price | >1,000,000 USD (Zolgensma 2,125,000) |

| COGS reduction | 30–50% |

| EUR/USD (2024 avg) | 1.09 |

| GBP/USD (2024 avg) | 1.27 |

Preview Before You Purchase

Passage Bio PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Passage Bio PESTLE Analysis provides a structured overview of political, economic, social, technological, legal, and environmental factors affecting the company. No placeholders or teasers—what you see is the final, downloadable file available immediately after checkout.