Paul Merchants Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

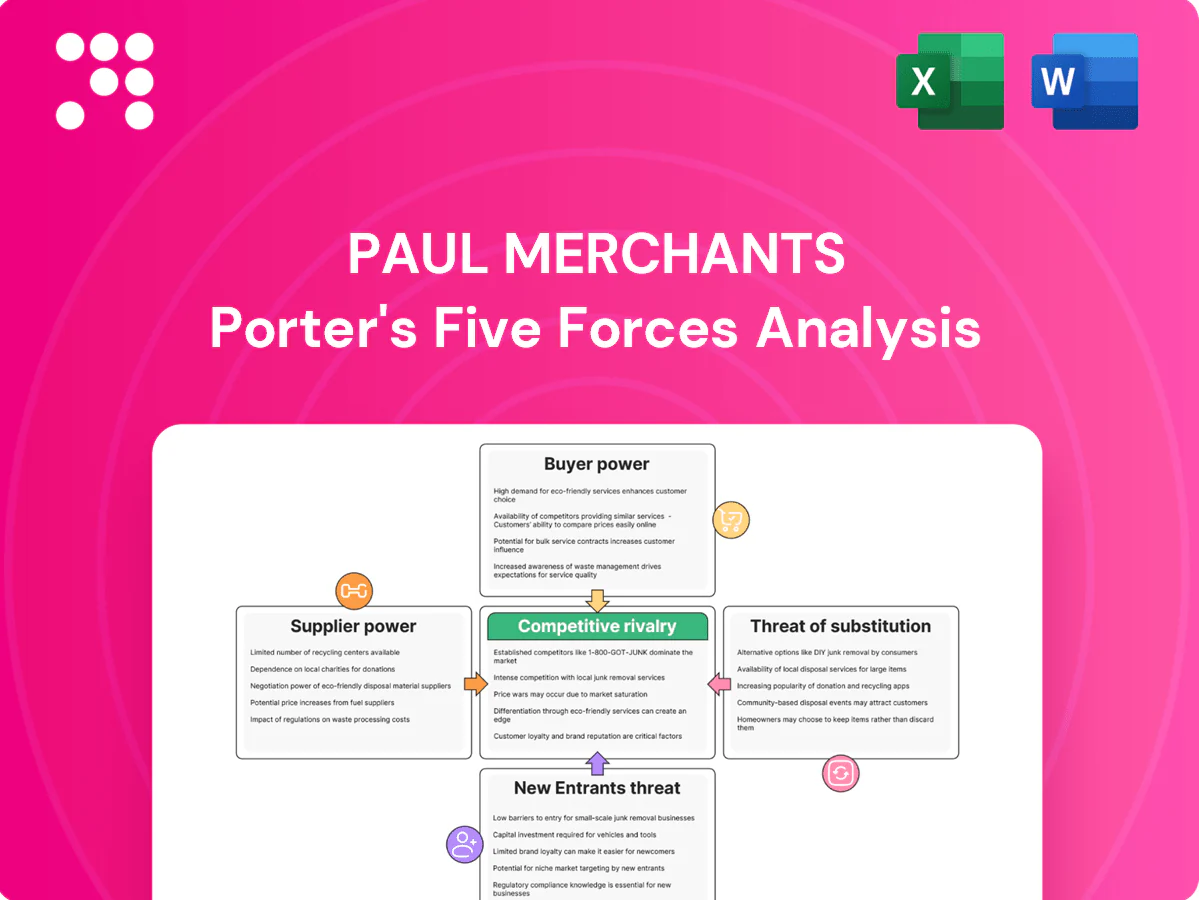

Paul Merchants faces shifting bargaining power and evolving threats across suppliers, buyers, entrants and substitutes that shape profitability and strategic choice. This brief snapshot only scratches the surface; the full Porter's Five Forces Analysis uncovers force-by-force ratings, visuals, and actionable implications tailored to Paul Merchants. Buy the complete report to translate industry dynamics into winning strategies and investment decisions.

Suppliers Bargaining Power

Reliance on banks and MTO principals

Paul Merchants depends on correspondent banks and global MTO principals for cross-border rails and liquidity; these partners can unilaterally change fees, settlement terms and cut-offs. Concentration among a few large providers raises switching costs and supplier leverage, with top providers dominating remittance rails (global remittances were roughly $700B in 2023). Long-term contracts mitigate operational risk but often embed pricing escalators.

Technology and compliance vendors

Core systems, AML/KYC tools and payment gateways are typically sourced from specialized providers, with integration complexity often representing 30–40% of total implementation costs and top 5 payment gateway providers handling over 60% of online payment volume in 2024.

Vendor lock-in and bespoke integrations give suppliers pricing leverage; regulatory-driven upgrades (AML/KYC) drive ongoing spend—the AML/KYC software market was roughly $3.2 billion in 2024 with ~12% CAGR.

Negotiating power improves with scale and optionality: firms with diversified vendor stacks or >$50 billion assets under management can secure 20–30% better licensing and integration terms.

Cash management and currency liquidity

FX liquidity providers and vault/cash logistics firms directly shape spreads and availability in a market whose average daily FX turnover was $7.5 trillion per BIS Triennial 2022 (spot 32%, swaps 48%). Volatility spikes, notably March 2020, widened dealer quotes and strained dollar funding, prompting central bank intervention. Same-day liquidity needs often command premium pricing; using diversified counterparties lowers single-supplier risk but raises coordination costs.

Agent network as quasi-suppliers

Agent networks act as quasi-suppliers for last-mile distribution, with franchisees and agents driving fulfillment for platforms that handled roughly $5.7 trillion in e-commerce GMV in 2024; high-performing agents can demand better commissions, squeezing margins by several percentage points. Regional concentration amplifies local leverage, while performance-based contracts and digital channels (route optimization, real-time tracking) can rebalance power.

- Agents supply last-mile distribution

- Top agents extract higher commissions, reducing margins

- Regional concentration increases bargaining leverage

- Performance contracts and digital tools shift power back to firms

Payment networks and rail owners

- NPCI 2024: billions of annual transactions across UPI/IMPS/NEFT

- Card schemes: standardized interchange and brand fees limit bargaining

- SWIFT: global messaging rules/fees affect cross‑border costs

- Multi‑rail routing: mitigates outage and rule‑change risk

Concentrated rails and AML vendors raise remittance costs; scale and rails diversification mitigate

Paul Merchants faces high supplier power from concentrated correspondent banks, FX/liquidity providers and payment rails—global remittances ~$700B (2023) and payment gateways top5 = 60% volume (2024) increase switching costs. AML/KYC market ~$3.2B (2024) and complex integrations (30–40% of implementation) embed ongoing vendor leverage. Diversified rails and scale (>$50B AUM wins 20–30% better terms) reduce, but do not eliminate, supplier risk.

| Metric | Value |

|---|---|

| Remittances (2023) | $700B |

| Payment gateway top5 (2024) | 60% volume |

| AML/KYC market (2024) | $3.2B |

| FX daily turnover (BIS 2022) | $7.5T |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Paul Merchants, uncovering competitive pressures, supplier and buyer power, threats from substitutes and new entrants, and strategic recommendations to protect and grow market share.

A concise, one-sheet Paul Merchants Porter's Five Forces that instantly reveals strategic pressure with an editable spider chart—perfect for quick decisions and pitch decks. Customize force levels, swap in your data, and use without macros for fast, boardroom-ready insights.

Customers Bargaining Power

Price-sensitive retail remitters

Individuals routinely compare fees and FX margins across apps and counters; low switching costs and online price transparency make choices highly elastic. Even tiny price gaps trigger churn, particularly in crowded corridors (World Bank reported a 6.3% average global remittance cost in 2023). Loyalty programs and speed guarantees help retain users by offsetting pure price-driven switching.

SMEs and travel clients negotiate

SMEs with recurring FX needs—given SMEs make up about 90% of businesses globally and ~50% of employment (World Bank)—can aggregate flows to negotiate tighter spreads. Corporate travel blocks increasingly demand bundled discounts and SLAs as business travel volumes recovered to roughly $1.1 trillion in 2024. Volume-based tiering for >$1m monthly flows materially increases buyer leverage, while value-added reporting and hedging education shift negotiations from price to service.

Digital multi-homing

Customers increasingly multi-home across apps, banks and fintechs, eroding lock-in and forcing firms to spend more on acquisition; Bain reports acquiring a new customer can cost up to 5x more than retaining one. UX, 24x7 support and fast dispute resolution now drive retention beyond price, while open-banking and interoperability standards lower switching friction and raise effective bargaining power of customers.

Demand for speed and transparency

Customers now expect real-time status, guaranteed delivery windows and upfront pricing; 63% of consumers in 2024 surveys prioritized real-time tracking and transparency, and any friction prompts immediate switching, compressing spreads as mid-rate references become visible; proactive, timely communication preserves trust during delays.

- Real-time status: 63% (2024)

- Guaranteed windows: retention driver

- Upfront pricing: narrows spreads

- Proactive comms: trust salvage

Regional and diaspora preferences

- Corridors: India, Mexico top recipients in 2024

- Language impact: Spanish/Hindi drive adoption in key markets

- Retention vs replicability: localized service raises loyalty but is imitable

- Risk: missed localization = lost market share to rivals

Customers wield power: 6.3% fees drive churn; 63% want real-time tracking

Customers exert high bargaining power: low switching costs, online price transparency and multi-homing drive elasticity, with 6.3% average remittance cost (2023) prompting churn. SMEs (≈90% of firms; ~50% employment) and >$1m monthly flows secure tighter spreads; business travel rebound (~$1.1T in 2024) raises demand for SLAs. 63% of consumers (2024) prioritize real-time tracking, making UX and service key retention levers.

| Metric | Value |

|---|---|

| Avg remittance cost (2023) | 6.3% |

| SME share of firms | ≈90% |

| Business travel (2024) | $1.1T |

| Consumers preferring real-time (2024) | 63% |

Preview Before You Purchase

Paul Merchants Porter's Five Forces Analysis

This preview shows the exact Paul Merchants Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the final, professionally formatted file, ready for download and use the moment you buy. You're viewing the same deliverable that will be available to you instantly after payment.

Go Beyond the Preview—Access the Full Strategic Report

Paul Merchants faces shifting bargaining power and evolving threats across suppliers, buyers, entrants and substitutes that shape profitability and strategic choice. This brief snapshot only scratches the surface; the full Porter's Five Forces Analysis uncovers force-by-force ratings, visuals, and actionable implications tailored to Paul Merchants. Buy the complete report to translate industry dynamics into winning strategies and investment decisions.

Suppliers Bargaining Power

Reliance on banks and MTO principals

Paul Merchants depends on correspondent banks and global MTO principals for cross-border rails and liquidity; these partners can unilaterally change fees, settlement terms and cut-offs. Concentration among a few large providers raises switching costs and supplier leverage, with top providers dominating remittance rails (global remittances were roughly $700B in 2023). Long-term contracts mitigate operational risk but often embed pricing escalators.

Technology and compliance vendors

Core systems, AML/KYC tools and payment gateways are typically sourced from specialized providers, with integration complexity often representing 30–40% of total implementation costs and top 5 payment gateway providers handling over 60% of online payment volume in 2024.

Vendor lock-in and bespoke integrations give suppliers pricing leverage; regulatory-driven upgrades (AML/KYC) drive ongoing spend—the AML/KYC software market was roughly $3.2 billion in 2024 with ~12% CAGR.

Negotiating power improves with scale and optionality: firms with diversified vendor stacks or >$50 billion assets under management can secure 20–30% better licensing and integration terms.

Cash management and currency liquidity

FX liquidity providers and vault/cash logistics firms directly shape spreads and availability in a market whose average daily FX turnover was $7.5 trillion per BIS Triennial 2022 (spot 32%, swaps 48%). Volatility spikes, notably March 2020, widened dealer quotes and strained dollar funding, prompting central bank intervention. Same-day liquidity needs often command premium pricing; using diversified counterparties lowers single-supplier risk but raises coordination costs.

Agent network as quasi-suppliers

Agent networks act as quasi-suppliers for last-mile distribution, with franchisees and agents driving fulfillment for platforms that handled roughly $5.7 trillion in e-commerce GMV in 2024; high-performing agents can demand better commissions, squeezing margins by several percentage points. Regional concentration amplifies local leverage, while performance-based contracts and digital channels (route optimization, real-time tracking) can rebalance power.

- Agents supply last-mile distribution

- Top agents extract higher commissions, reducing margins

- Regional concentration increases bargaining leverage

- Performance contracts and digital tools shift power back to firms

Payment networks and rail owners

- NPCI 2024: billions of annual transactions across UPI/IMPS/NEFT

- Card schemes: standardized interchange and brand fees limit bargaining

- SWIFT: global messaging rules/fees affect cross‑border costs

- Multi‑rail routing: mitigates outage and rule‑change risk

Concentrated rails and AML vendors raise remittance costs; scale and rails diversification mitigate

Paul Merchants faces high supplier power from concentrated correspondent banks, FX/liquidity providers and payment rails—global remittances ~$700B (2023) and payment gateways top5 = 60% volume (2024) increase switching costs. AML/KYC market ~$3.2B (2024) and complex integrations (30–40% of implementation) embed ongoing vendor leverage. Diversified rails and scale (>$50B AUM wins 20–30% better terms) reduce, but do not eliminate, supplier risk.

| Metric | Value |

|---|---|

| Remittances (2023) | $700B |

| Payment gateway top5 (2024) | 60% volume |

| AML/KYC market (2024) | $3.2B |

| FX daily turnover (BIS 2022) | $7.5T |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Paul Merchants, uncovering competitive pressures, supplier and buyer power, threats from substitutes and new entrants, and strategic recommendations to protect and grow market share.

A concise, one-sheet Paul Merchants Porter's Five Forces that instantly reveals strategic pressure with an editable spider chart—perfect for quick decisions and pitch decks. Customize force levels, swap in your data, and use without macros for fast, boardroom-ready insights.

Customers Bargaining Power

Price-sensitive retail remitters

Individuals routinely compare fees and FX margins across apps and counters; low switching costs and online price transparency make choices highly elastic. Even tiny price gaps trigger churn, particularly in crowded corridors (World Bank reported a 6.3% average global remittance cost in 2023). Loyalty programs and speed guarantees help retain users by offsetting pure price-driven switching.

SMEs and travel clients negotiate

SMEs with recurring FX needs—given SMEs make up about 90% of businesses globally and ~50% of employment (World Bank)—can aggregate flows to negotiate tighter spreads. Corporate travel blocks increasingly demand bundled discounts and SLAs as business travel volumes recovered to roughly $1.1 trillion in 2024. Volume-based tiering for >$1m monthly flows materially increases buyer leverage, while value-added reporting and hedging education shift negotiations from price to service.

Digital multi-homing

Customers increasingly multi-home across apps, banks and fintechs, eroding lock-in and forcing firms to spend more on acquisition; Bain reports acquiring a new customer can cost up to 5x more than retaining one. UX, 24x7 support and fast dispute resolution now drive retention beyond price, while open-banking and interoperability standards lower switching friction and raise effective bargaining power of customers.

Demand for speed and transparency

Customers now expect real-time status, guaranteed delivery windows and upfront pricing; 63% of consumers in 2024 surveys prioritized real-time tracking and transparency, and any friction prompts immediate switching, compressing spreads as mid-rate references become visible; proactive, timely communication preserves trust during delays.

- Real-time status: 63% (2024)

- Guaranteed windows: retention driver

- Upfront pricing: narrows spreads

- Proactive comms: trust salvage

Regional and diaspora preferences

- Corridors: India, Mexico top recipients in 2024

- Language impact: Spanish/Hindi drive adoption in key markets

- Retention vs replicability: localized service raises loyalty but is imitable

- Risk: missed localization = lost market share to rivals

Customers wield power: 6.3% fees drive churn; 63% want real-time tracking

Customers exert high bargaining power: low switching costs, online price transparency and multi-homing drive elasticity, with 6.3% average remittance cost (2023) prompting churn. SMEs (≈90% of firms; ~50% employment) and >$1m monthly flows secure tighter spreads; business travel rebound (~$1.1T in 2024) raises demand for SLAs. 63% of consumers (2024) prioritize real-time tracking, making UX and service key retention levers.

| Metric | Value |

|---|---|

| Avg remittance cost (2023) | 6.3% |

| SME share of firms | ≈90% |

| Business travel (2024) | $1.1T |

| Consumers preferring real-time (2024) | 63% |

Preview Before You Purchase

Paul Merchants Porter's Five Forces Analysis

This preview shows the exact Paul Merchants Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the final, professionally formatted file, ready for download and use the moment you buy. You're viewing the same deliverable that will be available to you instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Paul Merchants faces shifting bargaining power and evolving threats across suppliers, buyers, entrants and substitutes that shape profitability and strategic choice. This brief snapshot only scratches the surface; the full Porter's Five Forces Analysis uncovers force-by-force ratings, visuals, and actionable implications tailored to Paul Merchants. Buy the complete report to translate industry dynamics into winning strategies and investment decisions.

Suppliers Bargaining Power

Reliance on banks and MTO principals

Paul Merchants depends on correspondent banks and global MTO principals for cross-border rails and liquidity; these partners can unilaterally change fees, settlement terms and cut-offs. Concentration among a few large providers raises switching costs and supplier leverage, with top providers dominating remittance rails (global remittances were roughly $700B in 2023). Long-term contracts mitigate operational risk but often embed pricing escalators.

Technology and compliance vendors

Core systems, AML/KYC tools and payment gateways are typically sourced from specialized providers, with integration complexity often representing 30–40% of total implementation costs and top 5 payment gateway providers handling over 60% of online payment volume in 2024.

Vendor lock-in and bespoke integrations give suppliers pricing leverage; regulatory-driven upgrades (AML/KYC) drive ongoing spend—the AML/KYC software market was roughly $3.2 billion in 2024 with ~12% CAGR.

Negotiating power improves with scale and optionality: firms with diversified vendor stacks or >$50 billion assets under management can secure 20–30% better licensing and integration terms.

Cash management and currency liquidity

FX liquidity providers and vault/cash logistics firms directly shape spreads and availability in a market whose average daily FX turnover was $7.5 trillion per BIS Triennial 2022 (spot 32%, swaps 48%). Volatility spikes, notably March 2020, widened dealer quotes and strained dollar funding, prompting central bank intervention. Same-day liquidity needs often command premium pricing; using diversified counterparties lowers single-supplier risk but raises coordination costs.

Agent network as quasi-suppliers

Agent networks act as quasi-suppliers for last-mile distribution, with franchisees and agents driving fulfillment for platforms that handled roughly $5.7 trillion in e-commerce GMV in 2024; high-performing agents can demand better commissions, squeezing margins by several percentage points. Regional concentration amplifies local leverage, while performance-based contracts and digital channels (route optimization, real-time tracking) can rebalance power.

- Agents supply last-mile distribution

- Top agents extract higher commissions, reducing margins

- Regional concentration increases bargaining leverage

- Performance contracts and digital tools shift power back to firms

Payment networks and rail owners

- NPCI 2024: billions of annual transactions across UPI/IMPS/NEFT

- Card schemes: standardized interchange and brand fees limit bargaining

- SWIFT: global messaging rules/fees affect cross‑border costs

- Multi‑rail routing: mitigates outage and rule‑change risk

Concentrated rails and AML vendors raise remittance costs; scale and rails diversification mitigate

Paul Merchants faces high supplier power from concentrated correspondent banks, FX/liquidity providers and payment rails—global remittances ~$700B (2023) and payment gateways top5 = 60% volume (2024) increase switching costs. AML/KYC market ~$3.2B (2024) and complex integrations (30–40% of implementation) embed ongoing vendor leverage. Diversified rails and scale (>$50B AUM wins 20–30% better terms) reduce, but do not eliminate, supplier risk.

| Metric | Value |

|---|---|

| Remittances (2023) | $700B |

| Payment gateway top5 (2024) | 60% volume |

| AML/KYC market (2024) | $3.2B |

| FX daily turnover (BIS 2022) | $7.5T |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Paul Merchants, uncovering competitive pressures, supplier and buyer power, threats from substitutes and new entrants, and strategic recommendations to protect and grow market share.

A concise, one-sheet Paul Merchants Porter's Five Forces that instantly reveals strategic pressure with an editable spider chart—perfect for quick decisions and pitch decks. Customize force levels, swap in your data, and use without macros for fast, boardroom-ready insights.

Customers Bargaining Power

Price-sensitive retail remitters

Individuals routinely compare fees and FX margins across apps and counters; low switching costs and online price transparency make choices highly elastic. Even tiny price gaps trigger churn, particularly in crowded corridors (World Bank reported a 6.3% average global remittance cost in 2023). Loyalty programs and speed guarantees help retain users by offsetting pure price-driven switching.

SMEs and travel clients negotiate

SMEs with recurring FX needs—given SMEs make up about 90% of businesses globally and ~50% of employment (World Bank)—can aggregate flows to negotiate tighter spreads. Corporate travel blocks increasingly demand bundled discounts and SLAs as business travel volumes recovered to roughly $1.1 trillion in 2024. Volume-based tiering for >$1m monthly flows materially increases buyer leverage, while value-added reporting and hedging education shift negotiations from price to service.

Digital multi-homing

Customers increasingly multi-home across apps, banks and fintechs, eroding lock-in and forcing firms to spend more on acquisition; Bain reports acquiring a new customer can cost up to 5x more than retaining one. UX, 24x7 support and fast dispute resolution now drive retention beyond price, while open-banking and interoperability standards lower switching friction and raise effective bargaining power of customers.

Demand for speed and transparency

Customers now expect real-time status, guaranteed delivery windows and upfront pricing; 63% of consumers in 2024 surveys prioritized real-time tracking and transparency, and any friction prompts immediate switching, compressing spreads as mid-rate references become visible; proactive, timely communication preserves trust during delays.

- Real-time status: 63% (2024)

- Guaranteed windows: retention driver

- Upfront pricing: narrows spreads

- Proactive comms: trust salvage

Regional and diaspora preferences

- Corridors: India, Mexico top recipients in 2024

- Language impact: Spanish/Hindi drive adoption in key markets

- Retention vs replicability: localized service raises loyalty but is imitable

- Risk: missed localization = lost market share to rivals

Customers wield power: 6.3% fees drive churn; 63% want real-time tracking

Customers exert high bargaining power: low switching costs, online price transparency and multi-homing drive elasticity, with 6.3% average remittance cost (2023) prompting churn. SMEs (≈90% of firms; ~50% employment) and >$1m monthly flows secure tighter spreads; business travel rebound (~$1.1T in 2024) raises demand for SLAs. 63% of consumers (2024) prioritize real-time tracking, making UX and service key retention levers.

| Metric | Value |

|---|---|

| Avg remittance cost (2023) | 6.3% |

| SME share of firms | ≈90% |

| Business travel (2024) | $1.1T |

| Consumers preferring real-time (2024) | 63% |

Preview Before You Purchase

Paul Merchants Porter's Five Forces Analysis

This preview shows the exact Paul Merchants Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the final, professionally formatted file, ready for download and use the moment you buy. You're viewing the same deliverable that will be available to you instantly after payment.