Paycom Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

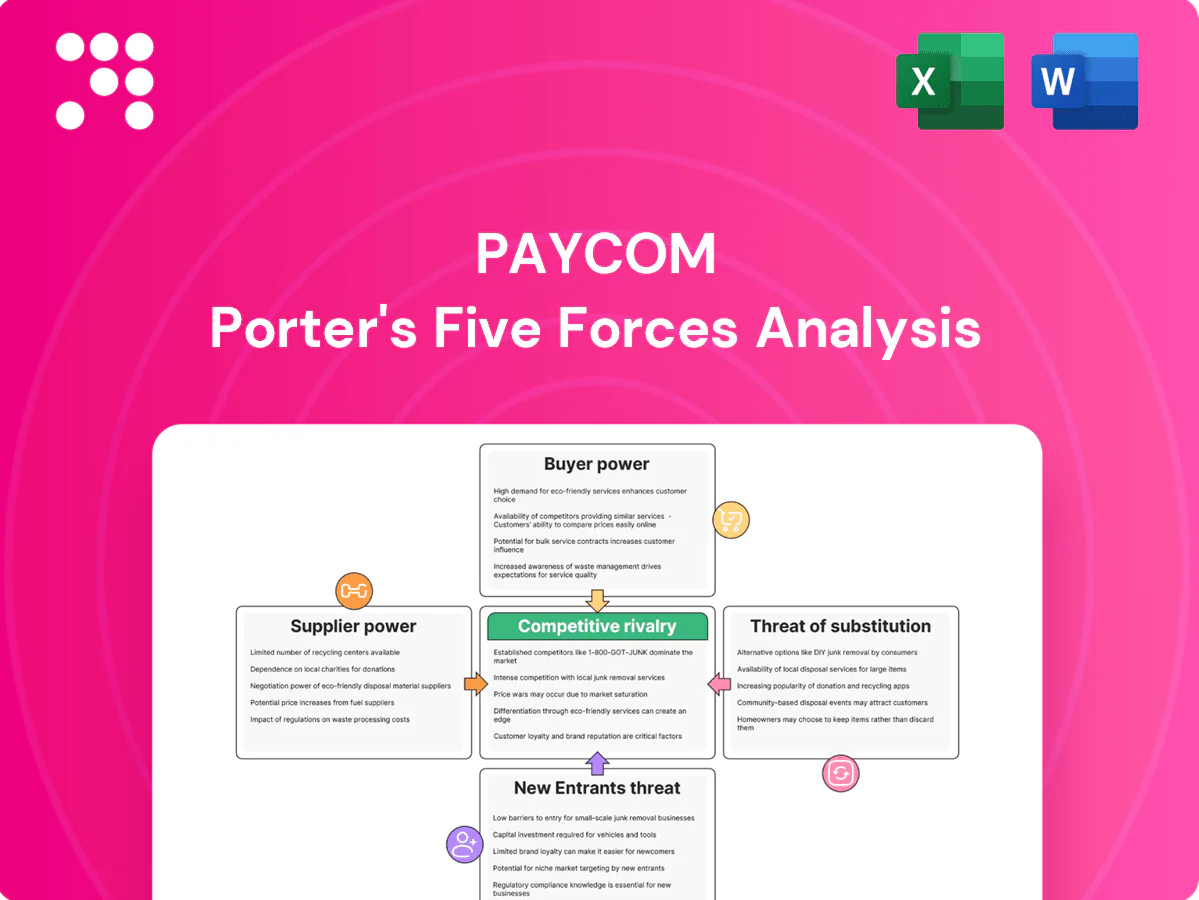

Paycom faces moderate buyer power, high rivalry among payroll/HCM vendors, and a manageable threat from new entrants due to regulatory scale advantages; supplier and substitute pressures remain limited but evolving with tech advances. This snapshot highlights core competitive dynamics and strategic levers. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights tailored to Paycom.

Suppliers Bargaining Power

Cloud and hosting vendors

If Paycom relies on third-party cloud or colocation, 2024 hyperscaler concentration (AWS ~32%, Azure ~23%, Google ~11%) gives vendors leverage on pricing and contract terms. Multiyear agreements and cross-region deployment reduce outage and latency risk but maintain uptime dependency. High vendor concentration can raise renewal costs; negotiated SLAs and growing in-house ops mitigate supplier power.

Banking and payment rails

Payroll funding, tax remittance and ACH settlement require bank partners and payment processors that set fees, cut-off times and risk policies impacting Paycom’s service economics.

Redundancy across multiple banks mitigates single-supplier risk; the ACH network processed about 30.9 billion transactions in 2023 (Nacha), underscoring systemic reliance.

Heightened regulatory scrutiny of payments post-2023 can strengthen supplier bargaining power in certain scenarios.

Compliance and data providers

Up-to-date tax, benefits, and regulatory content often comes from specialized sources. Timely, accurate feeds are critical, giving niche providers leverage; IRS Publication 15-T for 2024 and frequent state updates underscore this reliance. However, multiple vendors and capable in-house compliance teams can substitute. Standardized XML/JSON/EDI formats and automation reduce switching frictions and supplier power.

Software infrastructure tools

Paycom relies on databases, dev tools, analytics and security stacks from major vendors, creating high switching costs for core components, yet intense competition among tool providers keeps margins in check; Paycom reported FY2024 revenue of about $2.2B, enabling volume discounts and enterprise agreements that reduce supplier leverage.

- High switching cost vs limited pricing power

- Enterprise deals/volume discounts

- Open-source (90% enterprise adoption) as credible alternative

Skilled talent supply

Engineering, security, and compliance talent are critical inputs for Paycom; tight 2024 tech labor markets pushed median U.S. software pay toward roughly $120,000 and drove wage inflation and hiring costs, boosting supplier power of labor. Hybrid work and nearshore hiring expanded the usable talent pool, easing some pressure, while strong employer branding and internal training programs reduce external dependency.

- Talent types: engineering, security, compliance

- 2024 median software pay: ~$120,000 (U.S.)

- Hybrid/nearshore: broadened pool, lowered marginal hiring cost

- Mitigants: employer brand, upskilling/internal training

Moderate supplier power: hyperscalers, payment rails and talent drive selective risk

Paycom faces moderate supplier power: hyperscaler concentration (AWS ~32%, Azure ~23%, Google ~11% in 2024) and bank/payment rails (ACH 30.9B txns in 2023) create dependence, but multiyear SLAs, multi-bank redundancy and FY2024 revenue ~$2.2B reduce vulnerability. Niche tax/content feeds and high 2024 median software pay (~$120k) give pockets of leverage; open-source, volume deals and internal upskilling mitigate risk.

| Supplier | Key data | Effect |

|---|---|---|

| Hyperscalers | AWS 32%/Azure 23%/GCP 11% | Pricing leverage |

| Payments/banks | ACH 30.9B (2023) | Operational dependency |

| Talent | Median pay ~$120k (2024) | Cost pressure |

What is included in the product

Tailored Porter’s Five Forces analysis of Paycom uncovering competitive intensity, buyer and supplier power, substitution risks, and entry barriers, with strategic insights on disruptive threats and incumbent protections.

A concise, one-sheet Porter’s Five Forces for Paycom that highlights competitive pressures, customer bargaining power, and regulatory risks—perfect for quick strategic decisions and investor briefings.

Customers Bargaining Power

SMB price sensitivity

SMBs, which make up 99.9% of US firms per SBA 2024, are highly cost-conscious and closely compare payroll and HCM vendors on price and features. Transparent per-employee pricing models intensify negotiations as buyers can easily benchmark offers. Vendors frequently use discounts, bundles and promotional credits to win deals. Economic slowdowns increase price pressure and raise churn risk for vendors.

Switching costs and lock-in

Data migration, tax-year timing and process reconfiguration create high switching frictions for Paycom clients, reinforcing retention as evidenced by Paycoms 2024 revenue of $2.28 billion. Self-service adoption and embedded payroll-to-HR workflows deepen stickiness across payroll cycles. Modern APIs and certified implementation partners gradually lower barriers, while competitors like UKG and Workday actively offer migration support to win deals.

Demand for integration

Buyers expect seamless connections to accounting, benefits and ERP tools; Paycom reported $2.10B revenue in FY2024, making integration depth a key negotiation lever on price and roadmap prioritization. Open APIs lower vendor lock-in but raise expectations — 89% of organizations in MuleSoft’s 2024 Connectivity Benchmark say integration is critical, and lack of integrations triggers vendor reviews and churn risk.

Service quality and SLAs

Payroll accuracy and tax compliance are mission-critical for customers, so buyers demand strong SLAs (commonly 99.9% uptime in 2024), fast support response times, and explicit penalties or service credits for failures. Service incidents often trigger concessions or credits, directly affecting short-term bargaining power. High historical reliability and low incident rates therefore weaken buyer leverage at renewal.

- Payroll accuracy: mission-critical

- 2024 SLA benchmark: 99.9% uptime

- Incidents → concessions/credits

- High reliability lowers renewal leverage

Multi-vendor alternatives

Customers increasingly mix point solutions for time tracking, benefits and recruiting, creating multi-vendor alternatives that raise buyer bargaining power; in 2024 this trend accelerated among midmarket and enterprise buyers. Suite convenience, unified data and lower TCO often outweigh piecemeal savings, reducing churn despite higher vendor leverage.

- Multi-vendor pressure: increases negotiation

- Suite advantage: unified data, lower admin costs

- TCO: consolidation often cheaper long-term

SMB price pressure and switching costs support suite revenue $2.28B

SMB buyers (99.9% of US firms) are price-sensitive and benchmark per-employee pricing, increasing negotiation leverage. High switching costs—data migration, tax-year timing—limit churn and support Paycom’s $2.28B 2024 revenue, reducing buyer power. Integration demands (89% cite connectivity critical) and 99.9% SLA expectations raise buyer demands, though suites lower long-term TCO.

| Metric | 2024 |

|---|---|

| US SMB share | 99.9% |

| Paycom revenue | $2.28B |

| Connectivity critical | 89% |

| SLA benchmark | 99.9% uptime |

Same Document Delivered

Paycom Porter's Five Forces Analysis

This preview is the exact Paycom Porter’s Five Forces analysis you’ll receive after purchase—fully written, formatted, and ready to use. It covers rivalry, supplier and buyer power, threat of entrants, and substitutes with actionable insights. No placeholders or mockups. Purchase grants instant access to this same document.

Go Beyond the Preview—Access the Full Strategic Report

Paycom faces moderate buyer power, high rivalry among payroll/HCM vendors, and a manageable threat from new entrants due to regulatory scale advantages; supplier and substitute pressures remain limited but evolving with tech advances. This snapshot highlights core competitive dynamics and strategic levers. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights tailored to Paycom.

Suppliers Bargaining Power

Cloud and hosting vendors

If Paycom relies on third-party cloud or colocation, 2024 hyperscaler concentration (AWS ~32%, Azure ~23%, Google ~11%) gives vendors leverage on pricing and contract terms. Multiyear agreements and cross-region deployment reduce outage and latency risk but maintain uptime dependency. High vendor concentration can raise renewal costs; negotiated SLAs and growing in-house ops mitigate supplier power.

Banking and payment rails

Payroll funding, tax remittance and ACH settlement require bank partners and payment processors that set fees, cut-off times and risk policies impacting Paycom’s service economics.

Redundancy across multiple banks mitigates single-supplier risk; the ACH network processed about 30.9 billion transactions in 2023 (Nacha), underscoring systemic reliance.

Heightened regulatory scrutiny of payments post-2023 can strengthen supplier bargaining power in certain scenarios.

Compliance and data providers

Up-to-date tax, benefits, and regulatory content often comes from specialized sources. Timely, accurate feeds are critical, giving niche providers leverage; IRS Publication 15-T for 2024 and frequent state updates underscore this reliance. However, multiple vendors and capable in-house compliance teams can substitute. Standardized XML/JSON/EDI formats and automation reduce switching frictions and supplier power.

Software infrastructure tools

Paycom relies on databases, dev tools, analytics and security stacks from major vendors, creating high switching costs for core components, yet intense competition among tool providers keeps margins in check; Paycom reported FY2024 revenue of about $2.2B, enabling volume discounts and enterprise agreements that reduce supplier leverage.

- High switching cost vs limited pricing power

- Enterprise deals/volume discounts

- Open-source (90% enterprise adoption) as credible alternative

Skilled talent supply

Engineering, security, and compliance talent are critical inputs for Paycom; tight 2024 tech labor markets pushed median U.S. software pay toward roughly $120,000 and drove wage inflation and hiring costs, boosting supplier power of labor. Hybrid work and nearshore hiring expanded the usable talent pool, easing some pressure, while strong employer branding and internal training programs reduce external dependency.

- Talent types: engineering, security, compliance

- 2024 median software pay: ~$120,000 (U.S.)

- Hybrid/nearshore: broadened pool, lowered marginal hiring cost

- Mitigants: employer brand, upskilling/internal training

Moderate supplier power: hyperscalers, payment rails and talent drive selective risk

Paycom faces moderate supplier power: hyperscaler concentration (AWS ~32%, Azure ~23%, Google ~11% in 2024) and bank/payment rails (ACH 30.9B txns in 2023) create dependence, but multiyear SLAs, multi-bank redundancy and FY2024 revenue ~$2.2B reduce vulnerability. Niche tax/content feeds and high 2024 median software pay (~$120k) give pockets of leverage; open-source, volume deals and internal upskilling mitigate risk.

| Supplier | Key data | Effect |

|---|---|---|

| Hyperscalers | AWS 32%/Azure 23%/GCP 11% | Pricing leverage |

| Payments/banks | ACH 30.9B (2023) | Operational dependency |

| Talent | Median pay ~$120k (2024) | Cost pressure |

What is included in the product

Tailored Porter’s Five Forces analysis of Paycom uncovering competitive intensity, buyer and supplier power, substitution risks, and entry barriers, with strategic insights on disruptive threats and incumbent protections.

A concise, one-sheet Porter’s Five Forces for Paycom that highlights competitive pressures, customer bargaining power, and regulatory risks—perfect for quick strategic decisions and investor briefings.

Customers Bargaining Power

SMB price sensitivity

SMBs, which make up 99.9% of US firms per SBA 2024, are highly cost-conscious and closely compare payroll and HCM vendors on price and features. Transparent per-employee pricing models intensify negotiations as buyers can easily benchmark offers. Vendors frequently use discounts, bundles and promotional credits to win deals. Economic slowdowns increase price pressure and raise churn risk for vendors.

Switching costs and lock-in

Data migration, tax-year timing and process reconfiguration create high switching frictions for Paycom clients, reinforcing retention as evidenced by Paycoms 2024 revenue of $2.28 billion. Self-service adoption and embedded payroll-to-HR workflows deepen stickiness across payroll cycles. Modern APIs and certified implementation partners gradually lower barriers, while competitors like UKG and Workday actively offer migration support to win deals.

Demand for integration

Buyers expect seamless connections to accounting, benefits and ERP tools; Paycom reported $2.10B revenue in FY2024, making integration depth a key negotiation lever on price and roadmap prioritization. Open APIs lower vendor lock-in but raise expectations — 89% of organizations in MuleSoft’s 2024 Connectivity Benchmark say integration is critical, and lack of integrations triggers vendor reviews and churn risk.

Service quality and SLAs

Payroll accuracy and tax compliance are mission-critical for customers, so buyers demand strong SLAs (commonly 99.9% uptime in 2024), fast support response times, and explicit penalties or service credits for failures. Service incidents often trigger concessions or credits, directly affecting short-term bargaining power. High historical reliability and low incident rates therefore weaken buyer leverage at renewal.

- Payroll accuracy: mission-critical

- 2024 SLA benchmark: 99.9% uptime

- Incidents → concessions/credits

- High reliability lowers renewal leverage

Multi-vendor alternatives

Customers increasingly mix point solutions for time tracking, benefits and recruiting, creating multi-vendor alternatives that raise buyer bargaining power; in 2024 this trend accelerated among midmarket and enterprise buyers. Suite convenience, unified data and lower TCO often outweigh piecemeal savings, reducing churn despite higher vendor leverage.

- Multi-vendor pressure: increases negotiation

- Suite advantage: unified data, lower admin costs

- TCO: consolidation often cheaper long-term

SMB price pressure and switching costs support suite revenue $2.28B

SMB buyers (99.9% of US firms) are price-sensitive and benchmark per-employee pricing, increasing negotiation leverage. High switching costs—data migration, tax-year timing—limit churn and support Paycom’s $2.28B 2024 revenue, reducing buyer power. Integration demands (89% cite connectivity critical) and 99.9% SLA expectations raise buyer demands, though suites lower long-term TCO.

| Metric | 2024 |

|---|---|

| US SMB share | 99.9% |

| Paycom revenue | $2.28B |

| Connectivity critical | 89% |

| SLA benchmark | 99.9% uptime |

Same Document Delivered

Paycom Porter's Five Forces Analysis

This preview is the exact Paycom Porter’s Five Forces analysis you’ll receive after purchase—fully written, formatted, and ready to use. It covers rivalry, supplier and buyer power, threat of entrants, and substitutes with actionable insights. No placeholders or mockups. Purchase grants instant access to this same document.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Paycom faces moderate buyer power, high rivalry among payroll/HCM vendors, and a manageable threat from new entrants due to regulatory scale advantages; supplier and substitute pressures remain limited but evolving with tech advances. This snapshot highlights core competitive dynamics and strategic levers. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights tailored to Paycom.

Suppliers Bargaining Power

Cloud and hosting vendors

If Paycom relies on third-party cloud or colocation, 2024 hyperscaler concentration (AWS ~32%, Azure ~23%, Google ~11%) gives vendors leverage on pricing and contract terms. Multiyear agreements and cross-region deployment reduce outage and latency risk but maintain uptime dependency. High vendor concentration can raise renewal costs; negotiated SLAs and growing in-house ops mitigate supplier power.

Banking and payment rails

Payroll funding, tax remittance and ACH settlement require bank partners and payment processors that set fees, cut-off times and risk policies impacting Paycom’s service economics.

Redundancy across multiple banks mitigates single-supplier risk; the ACH network processed about 30.9 billion transactions in 2023 (Nacha), underscoring systemic reliance.

Heightened regulatory scrutiny of payments post-2023 can strengthen supplier bargaining power in certain scenarios.

Compliance and data providers

Up-to-date tax, benefits, and regulatory content often comes from specialized sources. Timely, accurate feeds are critical, giving niche providers leverage; IRS Publication 15-T for 2024 and frequent state updates underscore this reliance. However, multiple vendors and capable in-house compliance teams can substitute. Standardized XML/JSON/EDI formats and automation reduce switching frictions and supplier power.

Software infrastructure tools

Paycom relies on databases, dev tools, analytics and security stacks from major vendors, creating high switching costs for core components, yet intense competition among tool providers keeps margins in check; Paycom reported FY2024 revenue of about $2.2B, enabling volume discounts and enterprise agreements that reduce supplier leverage.

- High switching cost vs limited pricing power

- Enterprise deals/volume discounts

- Open-source (90% enterprise adoption) as credible alternative

Skilled talent supply

Engineering, security, and compliance talent are critical inputs for Paycom; tight 2024 tech labor markets pushed median U.S. software pay toward roughly $120,000 and drove wage inflation and hiring costs, boosting supplier power of labor. Hybrid work and nearshore hiring expanded the usable talent pool, easing some pressure, while strong employer branding and internal training programs reduce external dependency.

- Talent types: engineering, security, compliance

- 2024 median software pay: ~$120,000 (U.S.)

- Hybrid/nearshore: broadened pool, lowered marginal hiring cost

- Mitigants: employer brand, upskilling/internal training

Moderate supplier power: hyperscalers, payment rails and talent drive selective risk

Paycom faces moderate supplier power: hyperscaler concentration (AWS ~32%, Azure ~23%, Google ~11% in 2024) and bank/payment rails (ACH 30.9B txns in 2023) create dependence, but multiyear SLAs, multi-bank redundancy and FY2024 revenue ~$2.2B reduce vulnerability. Niche tax/content feeds and high 2024 median software pay (~$120k) give pockets of leverage; open-source, volume deals and internal upskilling mitigate risk.

| Supplier | Key data | Effect |

|---|---|---|

| Hyperscalers | AWS 32%/Azure 23%/GCP 11% | Pricing leverage |

| Payments/banks | ACH 30.9B (2023) | Operational dependency |

| Talent | Median pay ~$120k (2024) | Cost pressure |

What is included in the product

Tailored Porter’s Five Forces analysis of Paycom uncovering competitive intensity, buyer and supplier power, substitution risks, and entry barriers, with strategic insights on disruptive threats and incumbent protections.

A concise, one-sheet Porter’s Five Forces for Paycom that highlights competitive pressures, customer bargaining power, and regulatory risks—perfect for quick strategic decisions and investor briefings.

Customers Bargaining Power

SMB price sensitivity

SMBs, which make up 99.9% of US firms per SBA 2024, are highly cost-conscious and closely compare payroll and HCM vendors on price and features. Transparent per-employee pricing models intensify negotiations as buyers can easily benchmark offers. Vendors frequently use discounts, bundles and promotional credits to win deals. Economic slowdowns increase price pressure and raise churn risk for vendors.

Switching costs and lock-in

Data migration, tax-year timing and process reconfiguration create high switching frictions for Paycom clients, reinforcing retention as evidenced by Paycoms 2024 revenue of $2.28 billion. Self-service adoption and embedded payroll-to-HR workflows deepen stickiness across payroll cycles. Modern APIs and certified implementation partners gradually lower barriers, while competitors like UKG and Workday actively offer migration support to win deals.

Demand for integration

Buyers expect seamless connections to accounting, benefits and ERP tools; Paycom reported $2.10B revenue in FY2024, making integration depth a key negotiation lever on price and roadmap prioritization. Open APIs lower vendor lock-in but raise expectations — 89% of organizations in MuleSoft’s 2024 Connectivity Benchmark say integration is critical, and lack of integrations triggers vendor reviews and churn risk.

Service quality and SLAs

Payroll accuracy and tax compliance are mission-critical for customers, so buyers demand strong SLAs (commonly 99.9% uptime in 2024), fast support response times, and explicit penalties or service credits for failures. Service incidents often trigger concessions or credits, directly affecting short-term bargaining power. High historical reliability and low incident rates therefore weaken buyer leverage at renewal.

- Payroll accuracy: mission-critical

- 2024 SLA benchmark: 99.9% uptime

- Incidents → concessions/credits

- High reliability lowers renewal leverage

Multi-vendor alternatives

Customers increasingly mix point solutions for time tracking, benefits and recruiting, creating multi-vendor alternatives that raise buyer bargaining power; in 2024 this trend accelerated among midmarket and enterprise buyers. Suite convenience, unified data and lower TCO often outweigh piecemeal savings, reducing churn despite higher vendor leverage.

- Multi-vendor pressure: increases negotiation

- Suite advantage: unified data, lower admin costs

- TCO: consolidation often cheaper long-term

SMB price pressure and switching costs support suite revenue $2.28B

SMB buyers (99.9% of US firms) are price-sensitive and benchmark per-employee pricing, increasing negotiation leverage. High switching costs—data migration, tax-year timing—limit churn and support Paycom’s $2.28B 2024 revenue, reducing buyer power. Integration demands (89% cite connectivity critical) and 99.9% SLA expectations raise buyer demands, though suites lower long-term TCO.

| Metric | 2024 |

|---|---|

| US SMB share | 99.9% |

| Paycom revenue | $2.28B |

| Connectivity critical | 89% |

| SLA benchmark | 99.9% uptime |

Same Document Delivered

Paycom Porter's Five Forces Analysis

This preview is the exact Paycom Porter’s Five Forces analysis you’ll receive after purchase—fully written, formatted, and ready to use. It covers rivalry, supplier and buyer power, threat of entrants, and substitutes with actionable insights. No placeholders or mockups. Purchase grants instant access to this same document.