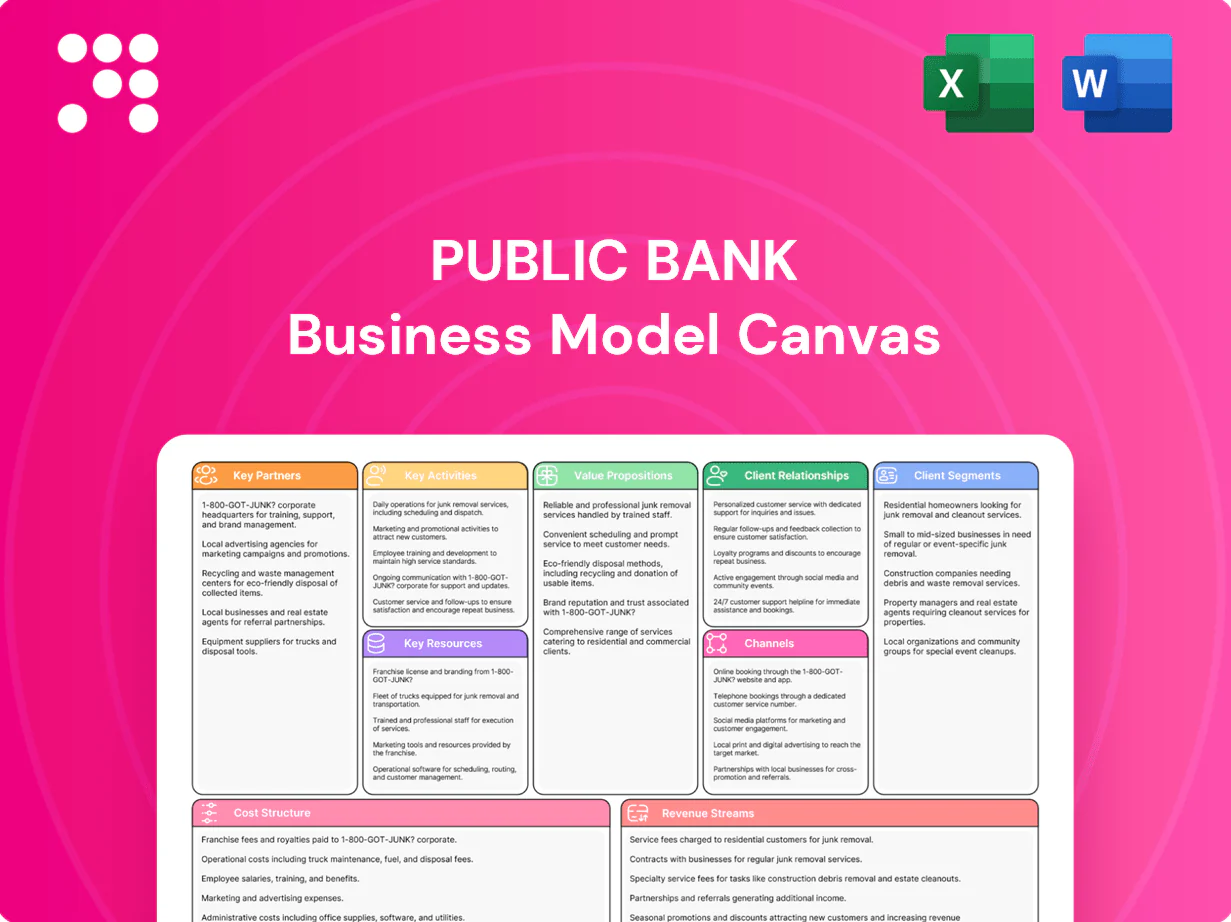

Public Bank Business Model Canvas

Concise Business Model Canvas for a Leading Bank - Download Editable Templates

Unlock the strategic blueprint of Public Bank with our concise Business Model Canvas that maps customer segments, value propositions, revenue streams and key partnerships. This in-depth snapshot reveals how the bank captures market share and sustains margins—ideal for investors, strategists and entrepreneurs. Download the full editable Canvas (Word & Excel) to benchmark, plan and act on proven growth levers.

Partnerships

Central bank, regulators, and Shariah governance bodies

Partnerships with Bank Negara Malaysia, securities regulators and PIDM (deposit protection up to RM250,000 per depositor) ensure compliance, stability and customer protection. Coordination with regulators supports capital adequacy, liquidity management and prudential standards. Shariah committees and external advisors ensure Islamic product compliance, enabling new product approvals and timely regulatory reporting.

Global payment networks and switching providers

Alliances with Visa, Mastercard, UnionPay, domestic switches and payment gateways power cards, merchant acquiring and digital payments; Visa and Mastercard together process over 300 billion transactions annually (2023–24), boosting volume and acceptance. Co-branding, tokenization and network token services enhance security and POS/app acceptance. Network incentives and routing optimization lower costs and expand merchant reach, while integrations enable contactless, QR and cross-border payments.

Technology, fintech, cybersecurity, and cloud vendors

Core-banking, cloud, AI/analytics and security partners accelerate digital transformation; banks tap the $620B global cloud services market in 2024 to modernize cores. Fintech collaborations add eKYC, alternative data and embedded finance as fintech funding topped about $70B in 2024, while cyber vendors counter rising cybercrime costs (>$8T annually) and reduce fraud; joint development cuts time-to-market and cost-to-serve.

Correspondent banks and capital markets partners

Correspondent banks supply cross-border payments, trade finance and FX liquidity, linking to a $7.5 trillion daily FX market (BIS 2022) and SWIFT flows near 40 million messages/day (2024). Investment banks and brokers underwrite, distribute and price debt issuance; custodians provide asset servicing for wealth clients, expanding geographic reach and product breadth.

- Correspondent banks: cross-border payments, trade finance, FX liquidity

- Investment banks/brokers: underwriting, distribution, debt issuance

- Custodians: custody and asset servicing for wealth clients

Insurance and takaful providers

Bancassurance and takaful partners expand retail and SME protection; Malaysia’s bancassurance channel accounted for about 30% of new business premiums in 2024, boosting product reach and bundled coverage. Revenue-sharing agreements strengthen Public Bank’s non-interest income via upfront commissions and ongoing trail fees. Bundled bank-insurance packages increase customer stickiness and cross-sell rates while compliance alignment enforces fair disclosure and suitability standards.

- 2024 bancassurance share ~30%

- Enhances non-interest income via revenue-sharing

- Product bundles raise retention and coverage

- Compliance ensures disclosure and suitability

Payments, cloud AI & bancassurance boost stability; deposit cover RM250,000

Regulators/PIDM ensure stability and depositor protection (RM250,000 limit); card networks (Visa/Mastercard/UnionPay) drive payments (300B+ transactions 2023–24). Cloud/AI and fintech partners accelerate digitalization (global cloud market $620B; fintech funding ~$70B in 2024). Bancassurance/takaful supply ~30% of new premiums (2024), boosting non-interest income.

| Partner | Role | 2024 metric |

|---|---|---|

| Regulators/PIDM | Stability/compliance | RM250,000 cover |

| Card networks | Payments/acceptance | 300B+ txns |

| Cloud/fintech | Digital platforms | $620B cloud; $70B fintech |

| Bancassurance | Protection sales | ~30% premiums |

What is included in the product

A concise, pre-built Business Model Canvas for Public Bank detailing customer segments, value propositions, channels, revenue streams, key activities, resources, partners, cost structure, and customer relations aligned to real-world banking operations. Ideal for presentations, investor discussions, and strategic analysis with integrated competitive advantage and SWOT insights.

High-level view of the Public Bank’s business model with editable cells, easing pain points around regulatory compliance, stakeholder alignment, and legacy process mapping; perfect for rapid scenario testing and governance-ready presentations.

Activities

Deposit gathering and lending origination

Acquire low-cost deposits (CASA ~54% in 2024) and originate retail, SME and corporate loans with optimized pricing, underwriting and faster turnaround to boost yield; maintain prudent credit standards to keep NPLs around 0.6% and preserve asset quality; continuously rebalance loan mix toward higher risk-adjusted returns, expanding SME and mortgage exposure while managing capital and LCR metrics.

Risk management, compliance, and credit monitoring

Operate enterprise risk frameworks across credit, market, liquidity and operational risks aligned to Basel III (CET1 minimum 4.5%) and Bank Negara Malaysia requirements, linking limits to stress-test outputs. Execute AML/CFT, KYC and conduct controls under Malaysia's AMLA 2001 and FATF recommendations with transaction monitoring and SAR reporting. Monitor early-warning signals to remediate exposures and ensure regulatory reporting accuracy and timeliness on monthly and quarterly cycles.

Digital product development and data analytics

Build and enhance mobile, internet and API banking platforms to support over 70% digital transaction volume and 24/7 service availability, driving scale and cost-efficiency. Use analytics for personalization, dynamic pricing and fraud detection, reducing false positives and improving conversion by up to 25% in 2024 deployments. Implement eKYC and seamless onboarding to cut account-opening time to under five minutes and lift activation rates; iterate using customer feedback and A/B testing to improve UX and adoption continuously.

Treasury, funding, and asset-liability management

Treasury manages liquidity buffers and funding mix to keep the Basel III Liquidity Coverage Ratio above 100%, limits interest-rate risk through duration and hedging, and conducts investments, FX dealing, and forwards to optimize net interest margin and capital usage. Regular (annual and ad-hoc) stress tests model severe scenarios to ensure resilience and inform capital planning.

Trade finance, cash management, and payments operations

Deliver LCs, guarantees, supply chain finance and receivables solutions addressing a global trade finance gap estimated at about 1.7 trillion USD (ICC, 2023), while providing collections, payroll and liquidity sweeping for corporates. Operate payment rails efficiently and securely with straight-through processing targets exceeding 95% and same‑day turnaround SLAs to minimize working capital strain.

- Trade finance: LCs, guarantees, SCF, receivables

- Cash mgmt: collections, payroll, liquidity sweeping

- Payments ops: secure rails, >95% STP, same‑day SLAs

Scale loans; CASA 54%, NPLs 0.6%, >70% digital

Acquire low-cost deposits (CASA 54% in 2024) and grow retail, SME and corporate loans while keeping NPLs ~0.6% and managing capital/LCR. Run Basel III-aligned risk, AML/CFT and stress testing. Scale digital channels (>70% transactions, eKYC <5 min) and Treasury keeps LCR >100% and hedging. Provide trade finance, SCF and >95% STP payments.

| Metric | 2024 |

|---|---|

| CASA | 54% |

| NPLs | 0.6% |

| Digital txns | >70% |

| eKYC onboarding | <5 min |

| LCR | >100% |

Full Document Unlocks After Purchase

Business Model Canvas

The Public Bank Business Model Canvas shown here is the genuine deliverable, not a mockup—it's a direct snapshot of the exact file you’ll receive after purchase. When you complete your order, you’ll get full access to this same, professionally formatted document ready for editing and presentation. The download includes the complete Business Model Canvas in Word and Excel formats, with all content and pages intact.

Concise Business Model Canvas for a Leading Bank - Download Editable Templates

Unlock the strategic blueprint of Public Bank with our concise Business Model Canvas that maps customer segments, value propositions, revenue streams and key partnerships. This in-depth snapshot reveals how the bank captures market share and sustains margins—ideal for investors, strategists and entrepreneurs. Download the full editable Canvas (Word & Excel) to benchmark, plan and act on proven growth levers.

Partnerships

Central bank, regulators, and Shariah governance bodies

Partnerships with Bank Negara Malaysia, securities regulators and PIDM (deposit protection up to RM250,000 per depositor) ensure compliance, stability and customer protection. Coordination with regulators supports capital adequacy, liquidity management and prudential standards. Shariah committees and external advisors ensure Islamic product compliance, enabling new product approvals and timely regulatory reporting.

Global payment networks and switching providers

Alliances with Visa, Mastercard, UnionPay, domestic switches and payment gateways power cards, merchant acquiring and digital payments; Visa and Mastercard together process over 300 billion transactions annually (2023–24), boosting volume and acceptance. Co-branding, tokenization and network token services enhance security and POS/app acceptance. Network incentives and routing optimization lower costs and expand merchant reach, while integrations enable contactless, QR and cross-border payments.

Technology, fintech, cybersecurity, and cloud vendors

Core-banking, cloud, AI/analytics and security partners accelerate digital transformation; banks tap the $620B global cloud services market in 2024 to modernize cores. Fintech collaborations add eKYC, alternative data and embedded finance as fintech funding topped about $70B in 2024, while cyber vendors counter rising cybercrime costs (>$8T annually) and reduce fraud; joint development cuts time-to-market and cost-to-serve.

Correspondent banks and capital markets partners

Correspondent banks supply cross-border payments, trade finance and FX liquidity, linking to a $7.5 trillion daily FX market (BIS 2022) and SWIFT flows near 40 million messages/day (2024). Investment banks and brokers underwrite, distribute and price debt issuance; custodians provide asset servicing for wealth clients, expanding geographic reach and product breadth.

- Correspondent banks: cross-border payments, trade finance, FX liquidity

- Investment banks/brokers: underwriting, distribution, debt issuance

- Custodians: custody and asset servicing for wealth clients

Insurance and takaful providers

Bancassurance and takaful partners expand retail and SME protection; Malaysia’s bancassurance channel accounted for about 30% of new business premiums in 2024, boosting product reach and bundled coverage. Revenue-sharing agreements strengthen Public Bank’s non-interest income via upfront commissions and ongoing trail fees. Bundled bank-insurance packages increase customer stickiness and cross-sell rates while compliance alignment enforces fair disclosure and suitability standards.

- 2024 bancassurance share ~30%

- Enhances non-interest income via revenue-sharing

- Product bundles raise retention and coverage

- Compliance ensures disclosure and suitability

Payments, cloud AI & bancassurance boost stability; deposit cover RM250,000

Regulators/PIDM ensure stability and depositor protection (RM250,000 limit); card networks (Visa/Mastercard/UnionPay) drive payments (300B+ transactions 2023–24). Cloud/AI and fintech partners accelerate digitalization (global cloud market $620B; fintech funding ~$70B in 2024). Bancassurance/takaful supply ~30% of new premiums (2024), boosting non-interest income.

| Partner | Role | 2024 metric |

|---|---|---|

| Regulators/PIDM | Stability/compliance | RM250,000 cover |

| Card networks | Payments/acceptance | 300B+ txns |

| Cloud/fintech | Digital platforms | $620B cloud; $70B fintech |

| Bancassurance | Protection sales | ~30% premiums |

What is included in the product

A concise, pre-built Business Model Canvas for Public Bank detailing customer segments, value propositions, channels, revenue streams, key activities, resources, partners, cost structure, and customer relations aligned to real-world banking operations. Ideal for presentations, investor discussions, and strategic analysis with integrated competitive advantage and SWOT insights.

High-level view of the Public Bank’s business model with editable cells, easing pain points around regulatory compliance, stakeholder alignment, and legacy process mapping; perfect for rapid scenario testing and governance-ready presentations.

Activities

Deposit gathering and lending origination

Acquire low-cost deposits (CASA ~54% in 2024) and originate retail, SME and corporate loans with optimized pricing, underwriting and faster turnaround to boost yield; maintain prudent credit standards to keep NPLs around 0.6% and preserve asset quality; continuously rebalance loan mix toward higher risk-adjusted returns, expanding SME and mortgage exposure while managing capital and LCR metrics.

Risk management, compliance, and credit monitoring

Operate enterprise risk frameworks across credit, market, liquidity and operational risks aligned to Basel III (CET1 minimum 4.5%) and Bank Negara Malaysia requirements, linking limits to stress-test outputs. Execute AML/CFT, KYC and conduct controls under Malaysia's AMLA 2001 and FATF recommendations with transaction monitoring and SAR reporting. Monitor early-warning signals to remediate exposures and ensure regulatory reporting accuracy and timeliness on monthly and quarterly cycles.

Digital product development and data analytics

Build and enhance mobile, internet and API banking platforms to support over 70% digital transaction volume and 24/7 service availability, driving scale and cost-efficiency. Use analytics for personalization, dynamic pricing and fraud detection, reducing false positives and improving conversion by up to 25% in 2024 deployments. Implement eKYC and seamless onboarding to cut account-opening time to under five minutes and lift activation rates; iterate using customer feedback and A/B testing to improve UX and adoption continuously.

Treasury, funding, and asset-liability management

Treasury manages liquidity buffers and funding mix to keep the Basel III Liquidity Coverage Ratio above 100%, limits interest-rate risk through duration and hedging, and conducts investments, FX dealing, and forwards to optimize net interest margin and capital usage. Regular (annual and ad-hoc) stress tests model severe scenarios to ensure resilience and inform capital planning.

Trade finance, cash management, and payments operations

Deliver LCs, guarantees, supply chain finance and receivables solutions addressing a global trade finance gap estimated at about 1.7 trillion USD (ICC, 2023), while providing collections, payroll and liquidity sweeping for corporates. Operate payment rails efficiently and securely with straight-through processing targets exceeding 95% and same‑day turnaround SLAs to minimize working capital strain.

- Trade finance: LCs, guarantees, SCF, receivables

- Cash mgmt: collections, payroll, liquidity sweeping

- Payments ops: secure rails, >95% STP, same‑day SLAs

Scale loans; CASA 54%, NPLs 0.6%, >70% digital

Acquire low-cost deposits (CASA 54% in 2024) and grow retail, SME and corporate loans while keeping NPLs ~0.6% and managing capital/LCR. Run Basel III-aligned risk, AML/CFT and stress testing. Scale digital channels (>70% transactions, eKYC <5 min) and Treasury keeps LCR >100% and hedging. Provide trade finance, SCF and >95% STP payments.

| Metric | 2024 |

|---|---|

| CASA | 54% |

| NPLs | 0.6% |

| Digital txns | >70% |

| eKYC onboarding | <5 min |

| LCR | >100% |

Full Document Unlocks After Purchase

Business Model Canvas

The Public Bank Business Model Canvas shown here is the genuine deliverable, not a mockup—it's a direct snapshot of the exact file you’ll receive after purchase. When you complete your order, you’ll get full access to this same, professionally formatted document ready for editing and presentation. The download includes the complete Business Model Canvas in Word and Excel formats, with all content and pages intact.

Original: $10.00

-65%$10.00

$3.50Description

Concise Business Model Canvas for a Leading Bank - Download Editable Templates

Unlock the strategic blueprint of Public Bank with our concise Business Model Canvas that maps customer segments, value propositions, revenue streams and key partnerships. This in-depth snapshot reveals how the bank captures market share and sustains margins—ideal for investors, strategists and entrepreneurs. Download the full editable Canvas (Word & Excel) to benchmark, plan and act on proven growth levers.

Partnerships

Central bank, regulators, and Shariah governance bodies

Partnerships with Bank Negara Malaysia, securities regulators and PIDM (deposit protection up to RM250,000 per depositor) ensure compliance, stability and customer protection. Coordination with regulators supports capital adequacy, liquidity management and prudential standards. Shariah committees and external advisors ensure Islamic product compliance, enabling new product approvals and timely regulatory reporting.

Global payment networks and switching providers

Alliances with Visa, Mastercard, UnionPay, domestic switches and payment gateways power cards, merchant acquiring and digital payments; Visa and Mastercard together process over 300 billion transactions annually (2023–24), boosting volume and acceptance. Co-branding, tokenization and network token services enhance security and POS/app acceptance. Network incentives and routing optimization lower costs and expand merchant reach, while integrations enable contactless, QR and cross-border payments.

Technology, fintech, cybersecurity, and cloud vendors

Core-banking, cloud, AI/analytics and security partners accelerate digital transformation; banks tap the $620B global cloud services market in 2024 to modernize cores. Fintech collaborations add eKYC, alternative data and embedded finance as fintech funding topped about $70B in 2024, while cyber vendors counter rising cybercrime costs (>$8T annually) and reduce fraud; joint development cuts time-to-market and cost-to-serve.

Correspondent banks and capital markets partners

Correspondent banks supply cross-border payments, trade finance and FX liquidity, linking to a $7.5 trillion daily FX market (BIS 2022) and SWIFT flows near 40 million messages/day (2024). Investment banks and brokers underwrite, distribute and price debt issuance; custodians provide asset servicing for wealth clients, expanding geographic reach and product breadth.

- Correspondent banks: cross-border payments, trade finance, FX liquidity

- Investment banks/brokers: underwriting, distribution, debt issuance

- Custodians: custody and asset servicing for wealth clients

Insurance and takaful providers

Bancassurance and takaful partners expand retail and SME protection; Malaysia’s bancassurance channel accounted for about 30% of new business premiums in 2024, boosting product reach and bundled coverage. Revenue-sharing agreements strengthen Public Bank’s non-interest income via upfront commissions and ongoing trail fees. Bundled bank-insurance packages increase customer stickiness and cross-sell rates while compliance alignment enforces fair disclosure and suitability standards.

- 2024 bancassurance share ~30%

- Enhances non-interest income via revenue-sharing

- Product bundles raise retention and coverage

- Compliance ensures disclosure and suitability

Payments, cloud AI & bancassurance boost stability; deposit cover RM250,000

Regulators/PIDM ensure stability and depositor protection (RM250,000 limit); card networks (Visa/Mastercard/UnionPay) drive payments (300B+ transactions 2023–24). Cloud/AI and fintech partners accelerate digitalization (global cloud market $620B; fintech funding ~$70B in 2024). Bancassurance/takaful supply ~30% of new premiums (2024), boosting non-interest income.

| Partner | Role | 2024 metric |

|---|---|---|

| Regulators/PIDM | Stability/compliance | RM250,000 cover |

| Card networks | Payments/acceptance | 300B+ txns |

| Cloud/fintech | Digital platforms | $620B cloud; $70B fintech |

| Bancassurance | Protection sales | ~30% premiums |

What is included in the product

A concise, pre-built Business Model Canvas for Public Bank detailing customer segments, value propositions, channels, revenue streams, key activities, resources, partners, cost structure, and customer relations aligned to real-world banking operations. Ideal for presentations, investor discussions, and strategic analysis with integrated competitive advantage and SWOT insights.

High-level view of the Public Bank’s business model with editable cells, easing pain points around regulatory compliance, stakeholder alignment, and legacy process mapping; perfect for rapid scenario testing and governance-ready presentations.

Activities

Deposit gathering and lending origination

Acquire low-cost deposits (CASA ~54% in 2024) and originate retail, SME and corporate loans with optimized pricing, underwriting and faster turnaround to boost yield; maintain prudent credit standards to keep NPLs around 0.6% and preserve asset quality; continuously rebalance loan mix toward higher risk-adjusted returns, expanding SME and mortgage exposure while managing capital and LCR metrics.

Risk management, compliance, and credit monitoring

Operate enterprise risk frameworks across credit, market, liquidity and operational risks aligned to Basel III (CET1 minimum 4.5%) and Bank Negara Malaysia requirements, linking limits to stress-test outputs. Execute AML/CFT, KYC and conduct controls under Malaysia's AMLA 2001 and FATF recommendations with transaction monitoring and SAR reporting. Monitor early-warning signals to remediate exposures and ensure regulatory reporting accuracy and timeliness on monthly and quarterly cycles.

Digital product development and data analytics

Build and enhance mobile, internet and API banking platforms to support over 70% digital transaction volume and 24/7 service availability, driving scale and cost-efficiency. Use analytics for personalization, dynamic pricing and fraud detection, reducing false positives and improving conversion by up to 25% in 2024 deployments. Implement eKYC and seamless onboarding to cut account-opening time to under five minutes and lift activation rates; iterate using customer feedback and A/B testing to improve UX and adoption continuously.

Treasury, funding, and asset-liability management

Treasury manages liquidity buffers and funding mix to keep the Basel III Liquidity Coverage Ratio above 100%, limits interest-rate risk through duration and hedging, and conducts investments, FX dealing, and forwards to optimize net interest margin and capital usage. Regular (annual and ad-hoc) stress tests model severe scenarios to ensure resilience and inform capital planning.

Trade finance, cash management, and payments operations

Deliver LCs, guarantees, supply chain finance and receivables solutions addressing a global trade finance gap estimated at about 1.7 trillion USD (ICC, 2023), while providing collections, payroll and liquidity sweeping for corporates. Operate payment rails efficiently and securely with straight-through processing targets exceeding 95% and same‑day turnaround SLAs to minimize working capital strain.

- Trade finance: LCs, guarantees, SCF, receivables

- Cash mgmt: collections, payroll, liquidity sweeping

- Payments ops: secure rails, >95% STP, same‑day SLAs

Scale loans; CASA 54%, NPLs 0.6%, >70% digital

Acquire low-cost deposits (CASA 54% in 2024) and grow retail, SME and corporate loans while keeping NPLs ~0.6% and managing capital/LCR. Run Basel III-aligned risk, AML/CFT and stress testing. Scale digital channels (>70% transactions, eKYC <5 min) and Treasury keeps LCR >100% and hedging. Provide trade finance, SCF and >95% STP payments.

| Metric | 2024 |

|---|---|

| CASA | 54% |

| NPLs | 0.6% |

| Digital txns | >70% |

| eKYC onboarding | <5 min |

| LCR | >100% |

Full Document Unlocks After Purchase

Business Model Canvas

The Public Bank Business Model Canvas shown here is the genuine deliverable, not a mockup—it's a direct snapshot of the exact file you’ll receive after purchase. When you complete your order, you’ll get full access to this same, professionally formatted document ready for editing and presentation. The download includes the complete Business Model Canvas in Word and Excel formats, with all content and pages intact.