Public Bank Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Public Bank faces intense competitive rivalry, moderate buyer power, limited supplier leverage, emerging fintech substitutes, and regulatory barriers that shape its margins and growth prospects. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Sticky low-cost deposits as key funding

Public Bank relies on granular retail and SME deposits—CASA around 66% in 2024—providing low-cost, sticky funding that limits supplier power. In tightening cycles depositors push for higher rates or shift to yield-rich alternatives, modestly lifting funding costs. Strong brand and service quality help retain balances, though digital rate-shopping raises sensitivity. A diversified deposit mix reduces reliance on any single funding source.

Wholesale funding and interbank liquidity

Access to interbank markets and wholesale debt supplements deposits but hands pricing power to market participants; 3-month interbank spreads in 2024 widened by ~40–60bps in risk-off episodes, shortening tenors and raising supplier leverage. Public Bank’s strong metrics—CET1 ~13.8% and LCR ~146% in 2024—mitigate stress, yet exposure to market cycles remains. Proactive liquidity buffers and diversified tenors curb concentration risk.

Technology vendors and core banking platforms

Core systems, payment rails and cybersecurity vendors exert switching-cost power as core banking replacements typically take 12–36 months and carry high operational risk; IBM reported the 2023 global average cost of a data breach at $4.45m, underlining cybersecurity stakes. Public Bank can leverage scale and multi-vendor sourcing and build in-house capabilities and strategic partnerships to temper vendor lock-in despite integration complexity.

Skilled labor and compliance expertise

Talent in risk, digital, analytics and Shariah governance is scarce, giving specialist staff strong bargaining power and enabling poaching across Malaysian banks.

Wage inflation and sectoral hiring competition raise operating costs, though Public Bank’s employer brand and formal training pipelines improve retention.

Ongoing automation and process redesign can progressively reduce reliance on scarce specialists and ease margin pressure.

- Supplier power: skilled employees

- Cost pressure: wage inflation, poaching

- Mitigants: employer brand, training

- Long term: automation, redesign

Payment networks and ecosystem partners

- Card schemes market power

- DuitNow: central instant-pay rail

- Fees compress margins (0.2–2.5%)

- Public Bank scale aids negotiation

- Open-API reduces single-partner risk

Supplier power moderate: CASA 66%, wholesale spreads +40-60bps

Supplier power is moderate: stable low‑cost funding (CASA ~66% in 2024) and strong metrics (CET1 ~13.8%, LCR ~146%) limit depositor leverage, but interbank spreads widened ~40–60bps in 2024 raising wholesale cost; vendor lock‑in and cybersecurity risk (avg breach cost $4.45m in 2023) and scarce specialist talent push costs; card fees 0.2–2.5% and open‑API/DuitNow reduce single‑partner dependence.

| Supplier | Impact | 2024 data |

|---|---|---|

| Depositors | Low cost, sticky | CASA 66% |

| Wholesale | Pricing risk | Spreads +40–60bps |

| Vendors | Switching cost | Avg breach $4.45m |

| Talent | Wage pressure | High poaching |

| Card rails | Fee pressure | 0.2–2.5% |

What is included in the product

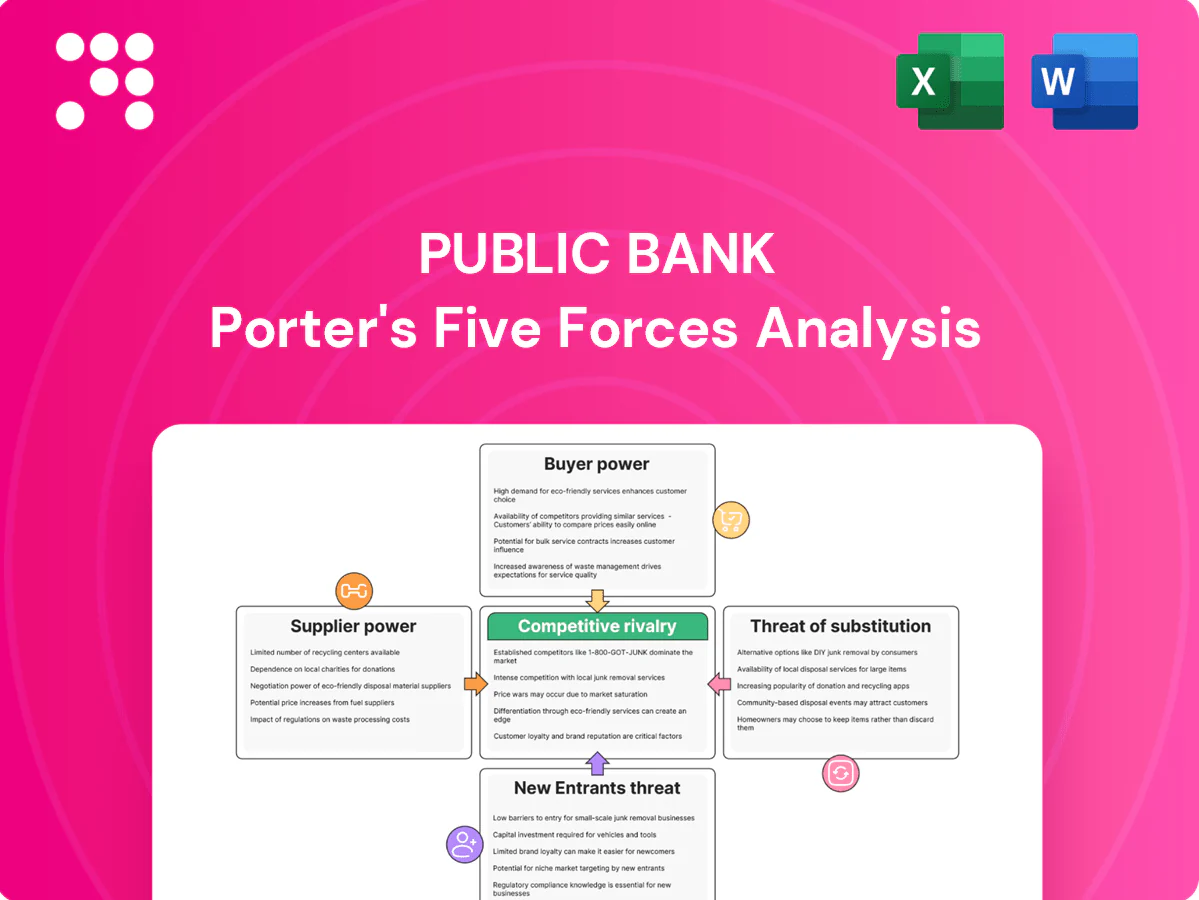

Concise Porter’s Five Forces for Public Bank, identifying competitive rivalry, buyer/supplier power, threat of entrants and substitutes, plus disruptive trends and strategic levers to protect margin and market share.

A one-sheet Porter's Five Forces for Public Bank that visualizes competitive pressures with adjustable ratings and a radar chart—ideal for quick strategic decisions, slide-ready, easy to customize with your own data and integrate into reports.

Customers Bargaining Power

Retail customers with low switching frictions

Digital onboarding and e-KYC have lowered switching frictions, making customers more price and service sensitive as mobile channel usage rises; Public Bank reports over 5 million active digital users in 2024. Rate-comparison apps and instant transfers (DuitNow network scale) increase transparency and churn risk. Public Bank leverages service reliability, a ~260-branch footprint, and bundled products to defend margins. Loyalty programs and ecosystem tie-ins boost customer stickiness.

SMEs bargaining on credit terms

SMEs, which account for over 97% of Malaysian firms and roughly 38% of GDP (2023), actively negotiate rates, collateral and fees across multiple banks, squeezing margins. The rise of invoice financing and P2P platforms increases SME leverage versus traditional lenders. Faster approvals and tailored relationship banking often offset pure price competition. Deep sector knowledge and advisory services strengthen ties and reduce churn.

Corporate clients with multi-banking

Larger corporates now split mandates across 3–5 banks to optimize pricing and counterparty risk, raising buyer power in 2024. They demand bespoke cash management, trade finance, and treasury solutions tailored to complex global flows. Public Bank must compete on SLA, systems integration, and risk appetite rather than price alone. Cross-selling and wallet-share strategies are essential to retain mandates and grow share of client balances.

Islamic banking clientele expectations

Shariah-compliant customers increasingly benchmark product authenticity, pricing and Shariah governance; Bank Negara Malaysia reported Islamic banking assets represented about 37% of Malaysia’s banking system in 2023, raising customer expectations. Availability of equivalent offerings across peers increases buyer choice, while Public Bank’s Islamic window competes on product breadth and institutional credibility. Clear product structures and third‑party certifications reduce sensitivity to minor price gaps.

- Customer focus: authenticity, governance, pricing

- Market context: Islamic assets ~37% of system (2023)

- Public Bank strengths: product breadth, credibility

- Price elasticity: lowered by transparency and certifications

Fee sensitivity in a transparent market

Regulated disclosures and online reviews have made fees highly visible, driving fee sensitivity—industry surveys in 2024 showed roughly 72% of retail customers compare bank charges before switching. Customers increasingly push back on maintenance, FX and transfer charges, pressuring margins; Public Bank counters with value-added features and tiered bundles and uses data-driven personalization to justify fees by improving relevance and uptake.

- 72% fee comparison (2024)

- Tiered bundles for retention

- Personalization to justify fees

Digital onboarding and >5m users boost SME price power; bank leans on 260 branches

Digital onboarding and e‑KYC cut switching frictions; Public Bank reports >5m active digital users in 2024, raising price/service sensitivity. SMEs (97% of firms; ~38% of GDP in 2023) and corporates (split mandates across 3–5 banks) increase bargaining power, while Islamic asset growth (~37% in 2023) and visible fees (72% compare charges in 2024) shape negotiations; Public Bank defends via 260 branches, bundles and advisory.

| Metric | Value |

|---|---|

| Public Bank digital users (2024) | >5,000,000 |

| Branches | ~260 |

| SME share (firms) | 97% |

| SME GDP contribution (2023) | ~38% |

| Islamic assets (Malaysia, 2023) | ~37% |

| Retail fee comparison (2024) | 72% |

Same Document Delivered

Public Bank Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Public Bank Porter's Five Forces Analysis in this file is fully formatted, comprehensive, and ready for immediate download and use. You're getting the final deliverable, instantly accessible after payment.

Go Beyond the Preview—Access the Full Strategic Report

Public Bank faces intense competitive rivalry, moderate buyer power, limited supplier leverage, emerging fintech substitutes, and regulatory barriers that shape its margins and growth prospects. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Sticky low-cost deposits as key funding

Public Bank relies on granular retail and SME deposits—CASA around 66% in 2024—providing low-cost, sticky funding that limits supplier power. In tightening cycles depositors push for higher rates or shift to yield-rich alternatives, modestly lifting funding costs. Strong brand and service quality help retain balances, though digital rate-shopping raises sensitivity. A diversified deposit mix reduces reliance on any single funding source.

Wholesale funding and interbank liquidity

Access to interbank markets and wholesale debt supplements deposits but hands pricing power to market participants; 3-month interbank spreads in 2024 widened by ~40–60bps in risk-off episodes, shortening tenors and raising supplier leverage. Public Bank’s strong metrics—CET1 ~13.8% and LCR ~146% in 2024—mitigate stress, yet exposure to market cycles remains. Proactive liquidity buffers and diversified tenors curb concentration risk.

Technology vendors and core banking platforms

Core systems, payment rails and cybersecurity vendors exert switching-cost power as core banking replacements typically take 12–36 months and carry high operational risk; IBM reported the 2023 global average cost of a data breach at $4.45m, underlining cybersecurity stakes. Public Bank can leverage scale and multi-vendor sourcing and build in-house capabilities and strategic partnerships to temper vendor lock-in despite integration complexity.

Skilled labor and compliance expertise

Talent in risk, digital, analytics and Shariah governance is scarce, giving specialist staff strong bargaining power and enabling poaching across Malaysian banks.

Wage inflation and sectoral hiring competition raise operating costs, though Public Bank’s employer brand and formal training pipelines improve retention.

Ongoing automation and process redesign can progressively reduce reliance on scarce specialists and ease margin pressure.

- Supplier power: skilled employees

- Cost pressure: wage inflation, poaching

- Mitigants: employer brand, training

- Long term: automation, redesign

Payment networks and ecosystem partners

- Card schemes market power

- DuitNow: central instant-pay rail

- Fees compress margins (0.2–2.5%)

- Public Bank scale aids negotiation

- Open-API reduces single-partner risk

Supplier power moderate: CASA 66%, wholesale spreads +40-60bps

Supplier power is moderate: stable low‑cost funding (CASA ~66% in 2024) and strong metrics (CET1 ~13.8%, LCR ~146%) limit depositor leverage, but interbank spreads widened ~40–60bps in 2024 raising wholesale cost; vendor lock‑in and cybersecurity risk (avg breach cost $4.45m in 2023) and scarce specialist talent push costs; card fees 0.2–2.5% and open‑API/DuitNow reduce single‑partner dependence.

| Supplier | Impact | 2024 data |

|---|---|---|

| Depositors | Low cost, sticky | CASA 66% |

| Wholesale | Pricing risk | Spreads +40–60bps |

| Vendors | Switching cost | Avg breach $4.45m |

| Talent | Wage pressure | High poaching |

| Card rails | Fee pressure | 0.2–2.5% |

What is included in the product

Concise Porter’s Five Forces for Public Bank, identifying competitive rivalry, buyer/supplier power, threat of entrants and substitutes, plus disruptive trends and strategic levers to protect margin and market share.

A one-sheet Porter's Five Forces for Public Bank that visualizes competitive pressures with adjustable ratings and a radar chart—ideal for quick strategic decisions, slide-ready, easy to customize with your own data and integrate into reports.

Customers Bargaining Power

Retail customers with low switching frictions

Digital onboarding and e-KYC have lowered switching frictions, making customers more price and service sensitive as mobile channel usage rises; Public Bank reports over 5 million active digital users in 2024. Rate-comparison apps and instant transfers (DuitNow network scale) increase transparency and churn risk. Public Bank leverages service reliability, a ~260-branch footprint, and bundled products to defend margins. Loyalty programs and ecosystem tie-ins boost customer stickiness.

SMEs bargaining on credit terms

SMEs, which account for over 97% of Malaysian firms and roughly 38% of GDP (2023), actively negotiate rates, collateral and fees across multiple banks, squeezing margins. The rise of invoice financing and P2P platforms increases SME leverage versus traditional lenders. Faster approvals and tailored relationship banking often offset pure price competition. Deep sector knowledge and advisory services strengthen ties and reduce churn.

Corporate clients with multi-banking

Larger corporates now split mandates across 3–5 banks to optimize pricing and counterparty risk, raising buyer power in 2024. They demand bespoke cash management, trade finance, and treasury solutions tailored to complex global flows. Public Bank must compete on SLA, systems integration, and risk appetite rather than price alone. Cross-selling and wallet-share strategies are essential to retain mandates and grow share of client balances.

Islamic banking clientele expectations

Shariah-compliant customers increasingly benchmark product authenticity, pricing and Shariah governance; Bank Negara Malaysia reported Islamic banking assets represented about 37% of Malaysia’s banking system in 2023, raising customer expectations. Availability of equivalent offerings across peers increases buyer choice, while Public Bank’s Islamic window competes on product breadth and institutional credibility. Clear product structures and third‑party certifications reduce sensitivity to minor price gaps.

- Customer focus: authenticity, governance, pricing

- Market context: Islamic assets ~37% of system (2023)

- Public Bank strengths: product breadth, credibility

- Price elasticity: lowered by transparency and certifications

Fee sensitivity in a transparent market

Regulated disclosures and online reviews have made fees highly visible, driving fee sensitivity—industry surveys in 2024 showed roughly 72% of retail customers compare bank charges before switching. Customers increasingly push back on maintenance, FX and transfer charges, pressuring margins; Public Bank counters with value-added features and tiered bundles and uses data-driven personalization to justify fees by improving relevance and uptake.

- 72% fee comparison (2024)

- Tiered bundles for retention

- Personalization to justify fees

Digital onboarding and >5m users boost SME price power; bank leans on 260 branches

Digital onboarding and e‑KYC cut switching frictions; Public Bank reports >5m active digital users in 2024, raising price/service sensitivity. SMEs (97% of firms; ~38% of GDP in 2023) and corporates (split mandates across 3–5 banks) increase bargaining power, while Islamic asset growth (~37% in 2023) and visible fees (72% compare charges in 2024) shape negotiations; Public Bank defends via 260 branches, bundles and advisory.

| Metric | Value |

|---|---|

| Public Bank digital users (2024) | >5,000,000 |

| Branches | ~260 |

| SME share (firms) | 97% |

| SME GDP contribution (2023) | ~38% |

| Islamic assets (Malaysia, 2023) | ~37% |

| Retail fee comparison (2024) | 72% |

Same Document Delivered

Public Bank Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Public Bank Porter's Five Forces Analysis in this file is fully formatted, comprehensive, and ready for immediate download and use. You're getting the final deliverable, instantly accessible after payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Public Bank faces intense competitive rivalry, moderate buyer power, limited supplier leverage, emerging fintech substitutes, and regulatory barriers that shape its margins and growth prospects. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Sticky low-cost deposits as key funding

Public Bank relies on granular retail and SME deposits—CASA around 66% in 2024—providing low-cost, sticky funding that limits supplier power. In tightening cycles depositors push for higher rates or shift to yield-rich alternatives, modestly lifting funding costs. Strong brand and service quality help retain balances, though digital rate-shopping raises sensitivity. A diversified deposit mix reduces reliance on any single funding source.

Wholesale funding and interbank liquidity

Access to interbank markets and wholesale debt supplements deposits but hands pricing power to market participants; 3-month interbank spreads in 2024 widened by ~40–60bps in risk-off episodes, shortening tenors and raising supplier leverage. Public Bank’s strong metrics—CET1 ~13.8% and LCR ~146% in 2024—mitigate stress, yet exposure to market cycles remains. Proactive liquidity buffers and diversified tenors curb concentration risk.

Technology vendors and core banking platforms

Core systems, payment rails and cybersecurity vendors exert switching-cost power as core banking replacements typically take 12–36 months and carry high operational risk; IBM reported the 2023 global average cost of a data breach at $4.45m, underlining cybersecurity stakes. Public Bank can leverage scale and multi-vendor sourcing and build in-house capabilities and strategic partnerships to temper vendor lock-in despite integration complexity.

Skilled labor and compliance expertise

Talent in risk, digital, analytics and Shariah governance is scarce, giving specialist staff strong bargaining power and enabling poaching across Malaysian banks.

Wage inflation and sectoral hiring competition raise operating costs, though Public Bank’s employer brand and formal training pipelines improve retention.

Ongoing automation and process redesign can progressively reduce reliance on scarce specialists and ease margin pressure.

- Supplier power: skilled employees

- Cost pressure: wage inflation, poaching

- Mitigants: employer brand, training

- Long term: automation, redesign

Payment networks and ecosystem partners

- Card schemes market power

- DuitNow: central instant-pay rail

- Fees compress margins (0.2–2.5%)

- Public Bank scale aids negotiation

- Open-API reduces single-partner risk

Supplier power moderate: CASA 66%, wholesale spreads +40-60bps

Supplier power is moderate: stable low‑cost funding (CASA ~66% in 2024) and strong metrics (CET1 ~13.8%, LCR ~146%) limit depositor leverage, but interbank spreads widened ~40–60bps in 2024 raising wholesale cost; vendor lock‑in and cybersecurity risk (avg breach cost $4.45m in 2023) and scarce specialist talent push costs; card fees 0.2–2.5% and open‑API/DuitNow reduce single‑partner dependence.

| Supplier | Impact | 2024 data |

|---|---|---|

| Depositors | Low cost, sticky | CASA 66% |

| Wholesale | Pricing risk | Spreads +40–60bps |

| Vendors | Switching cost | Avg breach $4.45m |

| Talent | Wage pressure | High poaching |

| Card rails | Fee pressure | 0.2–2.5% |

What is included in the product

Concise Porter’s Five Forces for Public Bank, identifying competitive rivalry, buyer/supplier power, threat of entrants and substitutes, plus disruptive trends and strategic levers to protect margin and market share.

A one-sheet Porter's Five Forces for Public Bank that visualizes competitive pressures with adjustable ratings and a radar chart—ideal for quick strategic decisions, slide-ready, easy to customize with your own data and integrate into reports.

Customers Bargaining Power

Retail customers with low switching frictions

Digital onboarding and e-KYC have lowered switching frictions, making customers more price and service sensitive as mobile channel usage rises; Public Bank reports over 5 million active digital users in 2024. Rate-comparison apps and instant transfers (DuitNow network scale) increase transparency and churn risk. Public Bank leverages service reliability, a ~260-branch footprint, and bundled products to defend margins. Loyalty programs and ecosystem tie-ins boost customer stickiness.

SMEs bargaining on credit terms

SMEs, which account for over 97% of Malaysian firms and roughly 38% of GDP (2023), actively negotiate rates, collateral and fees across multiple banks, squeezing margins. The rise of invoice financing and P2P platforms increases SME leverage versus traditional lenders. Faster approvals and tailored relationship banking often offset pure price competition. Deep sector knowledge and advisory services strengthen ties and reduce churn.

Corporate clients with multi-banking

Larger corporates now split mandates across 3–5 banks to optimize pricing and counterparty risk, raising buyer power in 2024. They demand bespoke cash management, trade finance, and treasury solutions tailored to complex global flows. Public Bank must compete on SLA, systems integration, and risk appetite rather than price alone. Cross-selling and wallet-share strategies are essential to retain mandates and grow share of client balances.

Islamic banking clientele expectations

Shariah-compliant customers increasingly benchmark product authenticity, pricing and Shariah governance; Bank Negara Malaysia reported Islamic banking assets represented about 37% of Malaysia’s banking system in 2023, raising customer expectations. Availability of equivalent offerings across peers increases buyer choice, while Public Bank’s Islamic window competes on product breadth and institutional credibility. Clear product structures and third‑party certifications reduce sensitivity to minor price gaps.

- Customer focus: authenticity, governance, pricing

- Market context: Islamic assets ~37% of system (2023)

- Public Bank strengths: product breadth, credibility

- Price elasticity: lowered by transparency and certifications

Fee sensitivity in a transparent market

Regulated disclosures and online reviews have made fees highly visible, driving fee sensitivity—industry surveys in 2024 showed roughly 72% of retail customers compare bank charges before switching. Customers increasingly push back on maintenance, FX and transfer charges, pressuring margins; Public Bank counters with value-added features and tiered bundles and uses data-driven personalization to justify fees by improving relevance and uptake.

- 72% fee comparison (2024)

- Tiered bundles for retention

- Personalization to justify fees

Digital onboarding and >5m users boost SME price power; bank leans on 260 branches

Digital onboarding and e‑KYC cut switching frictions; Public Bank reports >5m active digital users in 2024, raising price/service sensitivity. SMEs (97% of firms; ~38% of GDP in 2023) and corporates (split mandates across 3–5 banks) increase bargaining power, while Islamic asset growth (~37% in 2023) and visible fees (72% compare charges in 2024) shape negotiations; Public Bank defends via 260 branches, bundles and advisory.

| Metric | Value |

|---|---|

| Public Bank digital users (2024) | >5,000,000 |

| Branches | ~260 |

| SME share (firms) | 97% |

| SME GDP contribution (2023) | ~38% |

| Islamic assets (Malaysia, 2023) | ~37% |

| Retail fee comparison (2024) | 72% |

Same Document Delivered

Public Bank Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Public Bank Porter's Five Forces Analysis in this file is fully formatted, comprehensive, and ready for immediate download and use. You're getting the final deliverable, instantly accessible after payment.