Public Bank SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

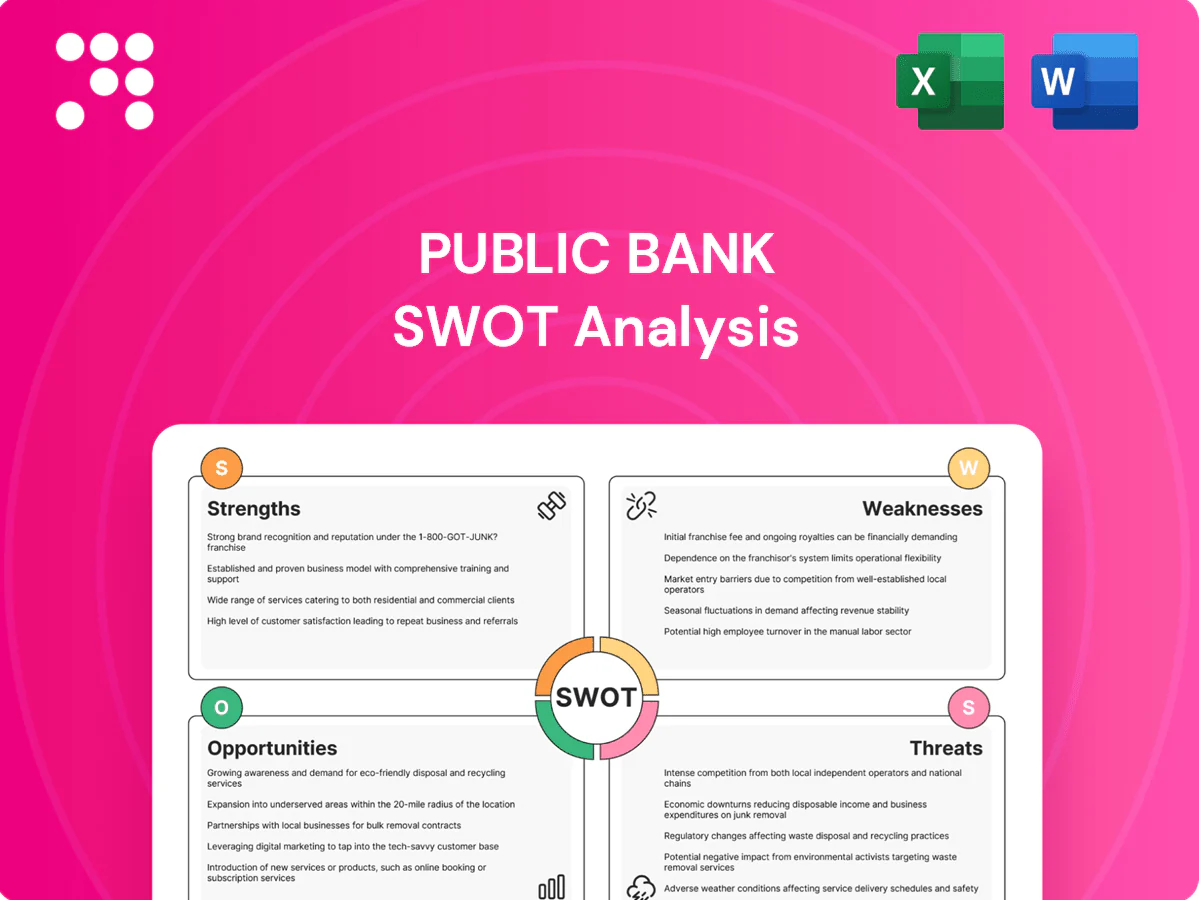

Public Bank’s SWOT analysis highlights robust capital adequacy, high-quality retail loan book, and strong branch network, balanced against digital disruption risks and regional concentration. Discover operational levers and competitive threats in clear, research-backed detail. Want the full strategic picture? Purchase the complete SWOT report for an editable Word and Excel package to plan, pitch, or invest with confidence.

Strengths

Market leadership

Public Bank, founded in 1966, holds a dominant position in Malaysia’s retail and SME banking, with scale that supports low funding costs, pricing power and strong customer trust. Its leadership underpins a premium deposit franchise and stable fee income streams, enhancing resilience across economic cycles. This positioning helps the bank manage margin pressure and credit cycles more effectively than smaller peers.

Diversified offerings

Public Bank, founded 1966 and now 59 years in operation, spans retail, commercial, Islamic (Public Islamic), investment banking and insurance, positioning it among Malaysia’s top three banks by market capitalization; this breadth smooths earnings and widens cross-selling potential. Islamic banking deepens reach into fast‑growing Shariah segments, while multiple products raise lifetime customer value and retention through fee and non‑interest income diversification.

Prudent risk culture

Public Bank’s prudent risk culture — a conservative underwriting approach and disciplined credit risk management — sustains low NPLs (around 0.4% in 2024) and strong asset quality. Robust capital and liquidity buffers (CAR ~18.2%, CET1 ~15.6%, LCR >140% in 2024) support growth and absorb shocks. Sound governance enhances regulator and investor confidence, reducing credit costs and earnings volatility.

Extensive distribution

Public Bank’s extensive branch and ATM network strengthens accessibility and deposit gathering by providing widespread physical touchpoints that complement its digital channels for true omnichannel service, enhancing convenience for retail and SME clients. Domestic density and regional outposts bolster brand visibility and support cash-based transactions and deep SME relationships across local markets.

- Branch/ATM network: enhances accessibility

- Omnichannel: physical + digital complementarity

- Domestic density: boosts brand visibility

- SME & cash servicing: strengthens client ties

Cost and efficiency focus

Process discipline and scale give Public Bank an industry-leading cost-to-income ratio in the low-30s, enabling efficient operations and attractive margins in core lending (NIM around 2.4% versus domestic peers). Productivity gains have financed ongoing digital investment, preserving capital for growth while allowing pricing flexibility without eroding profitability.

- Low-30s cost-to-income

- NIM ~2.4%

- Productivity-funded digital spend

- Pricing flexibility without margin compression

Scale and deposit strength enable low funding costs, conservative underwriting and ~0.4% NPL

Public Bank’s scale and trusted brand drive low funding costs, strong deposit franchise and resilient fee income. Diversified footprint (retail, SME, Islamic, insurance) supports cross‑sell and stable earnings. Conservative underwriting yields low NPLs and strong capital buffers, enabling profitable growth and pricing flexibility.

| Metric | 2024 |

|---|---|

| NPL | ~0.4% |

| CAR | ~18.2% |

| CET1 | ~15.6% |

| NIM | ~2.4% |

| Cost/Income | Low‑30s% |

What is included in the product

Provides a concise SWOT analysis of Public Bank, highlighting its core strengths and operational weaknesses while outlining market opportunities and external threats shaping the bank’s strategic position.

Provides a compact, visual SWOT tailored to Public Bank for rapid alignment and decision-making; editable format lets teams update risks, strengths and strategic actions quickly for stakeholder reports and executive briefings.

Weaknesses

Home-market concentration

Public Bank’s earnings remain concentrated in Malaysia, leaving performance tightly linked to local economic cycles and policy shifts such as interest-rate changes and fiscal measures.

This home-market concentration raises exposure to sectoral downturns in domestic property, consumer and SME lending, which can materially swing net interest income and asset quality.

Currency and regional diversification lag larger ASEAN peers, amplifying cyclical earnings volatility when Malaysia faces headwinds.

Interest income reliance

Net interest income accounts for the majority of Public Bank’s revenue, comprising over 60% of core income, leaving limited diversification. Rate compression and slower loan growth in 2024 have pressured margins, with industry NIMs around 2.0% in Malaysia. Fee-based and wealth management revenues lag global peers, constraining resilience in low-rate environments.

Legacy branch footprint

Legacy branch footprint elevates fixed costs as in-branch traffic has dropped c.45% since 2019, forcing higher cost-per-transaction and pressure on operating margins; optimizing hundreds of branches without harming service quality is operationally complex. Slow rationalization—often taking 12–36 months—can damp efficiency gains and delay new digital journeys, pushing transformation costs up and ROI timelines out by a year or more.

Digital speed gaps

Digital speed gaps: fintechs iterate faster on UX and embedded finance while legacy systems at Public Bank slow product rollout and personalization; uneven omnichannel integration risks eroding younger-customer acquisition and engagement.

- Legacy systems limit personalization

- Slower product rollout vs fintechs

- Uneven channel integration

- Risks losing younger cohorts

Investment banking scale

As of FY2024, Public Bank's capital-markets and high-end wealth capabilities remain modest versus global banks, with investment banking and capital-markets fees forming a small proportion of group non-interest income.

Limited regional deal-flow exposure constrains fee upside, while corporate clients often multi-bank for advanced products, reducing wallet share in complex mandates.

- Modest capital-markets fees

- Limited regional deal flow

- Clients multi-bank for complex products

- Lower wallet share in mandates

Malaysia-centric bank: NII-heavy, rate-sensitive earnings, high branch cost and weak fee growth

Public Bank’s earnings are highly Malaysia‑centric, with net interest income forming over 60% of core income and NIMs near 2.0% in 2024, exposing results to local rate cycles. Concentration raises sensitivity to domestic property, consumer and SME downturns, while branch-heavy operations (in‑branch traffic down c.45% since 2019) keep fixed costs high. Digital and capital‑markets capabilities lag regional peers, limiting fee diversification.

| Metric | Value (FY2024) |

|---|---|

| NII share of core income | >60% |

| Net interest margin (NIM) | ≈2.0% |

| In‑branch traffic change vs 2019 | −c.45% |

Full Version Awaits

Public Bank SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. You're viewing a live preview of the same file included in your download—full content becomes available after checkout.

Go Beyond the Preview—Access the Full Strategic Report

Public Bank’s SWOT analysis highlights robust capital adequacy, high-quality retail loan book, and strong branch network, balanced against digital disruption risks and regional concentration. Discover operational levers and competitive threats in clear, research-backed detail. Want the full strategic picture? Purchase the complete SWOT report for an editable Word and Excel package to plan, pitch, or invest with confidence.

Strengths

Market leadership

Public Bank, founded in 1966, holds a dominant position in Malaysia’s retail and SME banking, with scale that supports low funding costs, pricing power and strong customer trust. Its leadership underpins a premium deposit franchise and stable fee income streams, enhancing resilience across economic cycles. This positioning helps the bank manage margin pressure and credit cycles more effectively than smaller peers.

Diversified offerings

Public Bank, founded 1966 and now 59 years in operation, spans retail, commercial, Islamic (Public Islamic), investment banking and insurance, positioning it among Malaysia’s top three banks by market capitalization; this breadth smooths earnings and widens cross-selling potential. Islamic banking deepens reach into fast‑growing Shariah segments, while multiple products raise lifetime customer value and retention through fee and non‑interest income diversification.

Prudent risk culture

Public Bank’s prudent risk culture — a conservative underwriting approach and disciplined credit risk management — sustains low NPLs (around 0.4% in 2024) and strong asset quality. Robust capital and liquidity buffers (CAR ~18.2%, CET1 ~15.6%, LCR >140% in 2024) support growth and absorb shocks. Sound governance enhances regulator and investor confidence, reducing credit costs and earnings volatility.

Extensive distribution

Public Bank’s extensive branch and ATM network strengthens accessibility and deposit gathering by providing widespread physical touchpoints that complement its digital channels for true omnichannel service, enhancing convenience for retail and SME clients. Domestic density and regional outposts bolster brand visibility and support cash-based transactions and deep SME relationships across local markets.

- Branch/ATM network: enhances accessibility

- Omnichannel: physical + digital complementarity

- Domestic density: boosts brand visibility

- SME & cash servicing: strengthens client ties

Cost and efficiency focus

Process discipline and scale give Public Bank an industry-leading cost-to-income ratio in the low-30s, enabling efficient operations and attractive margins in core lending (NIM around 2.4% versus domestic peers). Productivity gains have financed ongoing digital investment, preserving capital for growth while allowing pricing flexibility without eroding profitability.

- Low-30s cost-to-income

- NIM ~2.4%

- Productivity-funded digital spend

- Pricing flexibility without margin compression

Scale and deposit strength enable low funding costs, conservative underwriting and ~0.4% NPL

Public Bank’s scale and trusted brand drive low funding costs, strong deposit franchise and resilient fee income. Diversified footprint (retail, SME, Islamic, insurance) supports cross‑sell and stable earnings. Conservative underwriting yields low NPLs and strong capital buffers, enabling profitable growth and pricing flexibility.

| Metric | 2024 |

|---|---|

| NPL | ~0.4% |

| CAR | ~18.2% |

| CET1 | ~15.6% |

| NIM | ~2.4% |

| Cost/Income | Low‑30s% |

What is included in the product

Provides a concise SWOT analysis of Public Bank, highlighting its core strengths and operational weaknesses while outlining market opportunities and external threats shaping the bank’s strategic position.

Provides a compact, visual SWOT tailored to Public Bank for rapid alignment and decision-making; editable format lets teams update risks, strengths and strategic actions quickly for stakeholder reports and executive briefings.

Weaknesses

Home-market concentration

Public Bank’s earnings remain concentrated in Malaysia, leaving performance tightly linked to local economic cycles and policy shifts such as interest-rate changes and fiscal measures.

This home-market concentration raises exposure to sectoral downturns in domestic property, consumer and SME lending, which can materially swing net interest income and asset quality.

Currency and regional diversification lag larger ASEAN peers, amplifying cyclical earnings volatility when Malaysia faces headwinds.

Interest income reliance

Net interest income accounts for the majority of Public Bank’s revenue, comprising over 60% of core income, leaving limited diversification. Rate compression and slower loan growth in 2024 have pressured margins, with industry NIMs around 2.0% in Malaysia. Fee-based and wealth management revenues lag global peers, constraining resilience in low-rate environments.

Legacy branch footprint

Legacy branch footprint elevates fixed costs as in-branch traffic has dropped c.45% since 2019, forcing higher cost-per-transaction and pressure on operating margins; optimizing hundreds of branches without harming service quality is operationally complex. Slow rationalization—often taking 12–36 months—can damp efficiency gains and delay new digital journeys, pushing transformation costs up and ROI timelines out by a year or more.

Digital speed gaps

Digital speed gaps: fintechs iterate faster on UX and embedded finance while legacy systems at Public Bank slow product rollout and personalization; uneven omnichannel integration risks eroding younger-customer acquisition and engagement.

- Legacy systems limit personalization

- Slower product rollout vs fintechs

- Uneven channel integration

- Risks losing younger cohorts

Investment banking scale

As of FY2024, Public Bank's capital-markets and high-end wealth capabilities remain modest versus global banks, with investment banking and capital-markets fees forming a small proportion of group non-interest income.

Limited regional deal-flow exposure constrains fee upside, while corporate clients often multi-bank for advanced products, reducing wallet share in complex mandates.

- Modest capital-markets fees

- Limited regional deal flow

- Clients multi-bank for complex products

- Lower wallet share in mandates

Malaysia-centric bank: NII-heavy, rate-sensitive earnings, high branch cost and weak fee growth

Public Bank’s earnings are highly Malaysia‑centric, with net interest income forming over 60% of core income and NIMs near 2.0% in 2024, exposing results to local rate cycles. Concentration raises sensitivity to domestic property, consumer and SME downturns, while branch-heavy operations (in‑branch traffic down c.45% since 2019) keep fixed costs high. Digital and capital‑markets capabilities lag regional peers, limiting fee diversification.

| Metric | Value (FY2024) |

|---|---|

| NII share of core income | >60% |

| Net interest margin (NIM) | ≈2.0% |

| In‑branch traffic change vs 2019 | −c.45% |

Full Version Awaits

Public Bank SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. You're viewing a live preview of the same file included in your download—full content becomes available after checkout.

Description

Go Beyond the Preview—Access the Full Strategic Report

Public Bank’s SWOT analysis highlights robust capital adequacy, high-quality retail loan book, and strong branch network, balanced against digital disruption risks and regional concentration. Discover operational levers and competitive threats in clear, research-backed detail. Want the full strategic picture? Purchase the complete SWOT report for an editable Word and Excel package to plan, pitch, or invest with confidence.

Strengths

Market leadership

Public Bank, founded in 1966, holds a dominant position in Malaysia’s retail and SME banking, with scale that supports low funding costs, pricing power and strong customer trust. Its leadership underpins a premium deposit franchise and stable fee income streams, enhancing resilience across economic cycles. This positioning helps the bank manage margin pressure and credit cycles more effectively than smaller peers.

Diversified offerings

Public Bank, founded 1966 and now 59 years in operation, spans retail, commercial, Islamic (Public Islamic), investment banking and insurance, positioning it among Malaysia’s top three banks by market capitalization; this breadth smooths earnings and widens cross-selling potential. Islamic banking deepens reach into fast‑growing Shariah segments, while multiple products raise lifetime customer value and retention through fee and non‑interest income diversification.

Prudent risk culture

Public Bank’s prudent risk culture — a conservative underwriting approach and disciplined credit risk management — sustains low NPLs (around 0.4% in 2024) and strong asset quality. Robust capital and liquidity buffers (CAR ~18.2%, CET1 ~15.6%, LCR >140% in 2024) support growth and absorb shocks. Sound governance enhances regulator and investor confidence, reducing credit costs and earnings volatility.

Extensive distribution

Public Bank’s extensive branch and ATM network strengthens accessibility and deposit gathering by providing widespread physical touchpoints that complement its digital channels for true omnichannel service, enhancing convenience for retail and SME clients. Domestic density and regional outposts bolster brand visibility and support cash-based transactions and deep SME relationships across local markets.

- Branch/ATM network: enhances accessibility

- Omnichannel: physical + digital complementarity

- Domestic density: boosts brand visibility

- SME & cash servicing: strengthens client ties

Cost and efficiency focus

Process discipline and scale give Public Bank an industry-leading cost-to-income ratio in the low-30s, enabling efficient operations and attractive margins in core lending (NIM around 2.4% versus domestic peers). Productivity gains have financed ongoing digital investment, preserving capital for growth while allowing pricing flexibility without eroding profitability.

- Low-30s cost-to-income

- NIM ~2.4%

- Productivity-funded digital spend

- Pricing flexibility without margin compression

Scale and deposit strength enable low funding costs, conservative underwriting and ~0.4% NPL

Public Bank’s scale and trusted brand drive low funding costs, strong deposit franchise and resilient fee income. Diversified footprint (retail, SME, Islamic, insurance) supports cross‑sell and stable earnings. Conservative underwriting yields low NPLs and strong capital buffers, enabling profitable growth and pricing flexibility.

| Metric | 2024 |

|---|---|

| NPL | ~0.4% |

| CAR | ~18.2% |

| CET1 | ~15.6% |

| NIM | ~2.4% |

| Cost/Income | Low‑30s% |

What is included in the product

Provides a concise SWOT analysis of Public Bank, highlighting its core strengths and operational weaknesses while outlining market opportunities and external threats shaping the bank’s strategic position.

Provides a compact, visual SWOT tailored to Public Bank for rapid alignment and decision-making; editable format lets teams update risks, strengths and strategic actions quickly for stakeholder reports and executive briefings.

Weaknesses

Home-market concentration

Public Bank’s earnings remain concentrated in Malaysia, leaving performance tightly linked to local economic cycles and policy shifts such as interest-rate changes and fiscal measures.

This home-market concentration raises exposure to sectoral downturns in domestic property, consumer and SME lending, which can materially swing net interest income and asset quality.

Currency and regional diversification lag larger ASEAN peers, amplifying cyclical earnings volatility when Malaysia faces headwinds.

Interest income reliance

Net interest income accounts for the majority of Public Bank’s revenue, comprising over 60% of core income, leaving limited diversification. Rate compression and slower loan growth in 2024 have pressured margins, with industry NIMs around 2.0% in Malaysia. Fee-based and wealth management revenues lag global peers, constraining resilience in low-rate environments.

Legacy branch footprint

Legacy branch footprint elevates fixed costs as in-branch traffic has dropped c.45% since 2019, forcing higher cost-per-transaction and pressure on operating margins; optimizing hundreds of branches without harming service quality is operationally complex. Slow rationalization—often taking 12–36 months—can damp efficiency gains and delay new digital journeys, pushing transformation costs up and ROI timelines out by a year or more.

Digital speed gaps

Digital speed gaps: fintechs iterate faster on UX and embedded finance while legacy systems at Public Bank slow product rollout and personalization; uneven omnichannel integration risks eroding younger-customer acquisition and engagement.

- Legacy systems limit personalization

- Slower product rollout vs fintechs

- Uneven channel integration

- Risks losing younger cohorts

Investment banking scale

As of FY2024, Public Bank's capital-markets and high-end wealth capabilities remain modest versus global banks, with investment banking and capital-markets fees forming a small proportion of group non-interest income.

Limited regional deal-flow exposure constrains fee upside, while corporate clients often multi-bank for advanced products, reducing wallet share in complex mandates.

- Modest capital-markets fees

- Limited regional deal flow

- Clients multi-bank for complex products

- Lower wallet share in mandates

Malaysia-centric bank: NII-heavy, rate-sensitive earnings, high branch cost and weak fee growth

Public Bank’s earnings are highly Malaysia‑centric, with net interest income forming over 60% of core income and NIMs near 2.0% in 2024, exposing results to local rate cycles. Concentration raises sensitivity to domestic property, consumer and SME downturns, while branch-heavy operations (in‑branch traffic down c.45% since 2019) keep fixed costs high. Digital and capital‑markets capabilities lag regional peers, limiting fee diversification.

| Metric | Value (FY2024) |

|---|---|

| NII share of core income | >60% |

| Net interest margin (NIM) | ≈2.0% |

| In‑branch traffic change vs 2019 | −c.45% |

Full Version Awaits

Public Bank SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. You're viewing a live preview of the same file included in your download—full content becomes available after checkout.