PDVSA Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

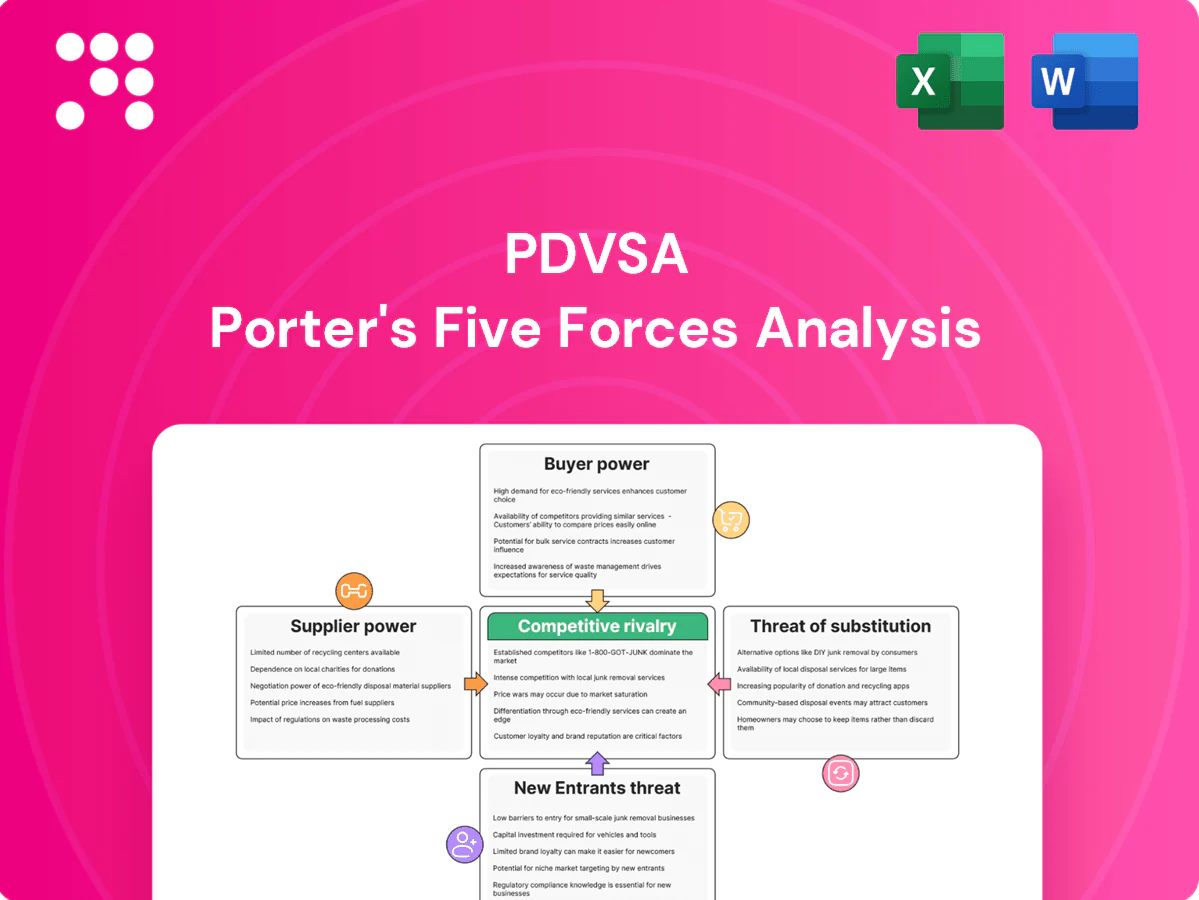

PDVSA's Porter’s Five Forces highlights strong supplier power, heavy regulatory and geopolitical threats, moderate buyer leverage, steep barriers from state control, and limited substitute risk. This snapshot surfaces key strategic pressure points and vulnerabilities for investors and managers. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to PDVSA.

Suppliers Bargaining Power

Concentrated critical service vendors

PDVSA depends on a narrow pool of oilfield services and EPC suppliers willing to operate under sanctions and arrears, constraining options. With Venezuelan crude output around 700 kbpd in 2024 and major Western firms such as Schlumberger, Halliburton and Baker Hughes having curtailed activities, remaining suppliers gain pricing and schedule leverage. Replacement with Russian, Chinese and Iranian contractors often entails trade-offs in quality, timing and compliance.

Diluent and chemicals dependency

Extra-heavy Orinoco crude requires large diluent volumes, typically 30-50% naphtha or light condensate, creating strong supplier leverage. Limited sourcing routes and US/secondary sanctions since 2019 elevate counterparty risk and supplier power. Diluent shortages directly curtail throughput and exportable volumes; PDVSA exports hovered near 600 kb/d in 2024 as prepayment and premium terms became common in tight windows.

Power, logistics, and maintenance constraints

Unreliable electricity, port congestion, and compromised pipeline integrity force PDVSA to depend on scarce maintenance contractors and imported spare parts, squeezing operations while crude output averaged about 800 kb/d in 2024 per OPEC secondary sources. Suppliers of turbines, pumps, and control systems gained leverage amid chronic shortages, with lead times commonly stretching 6–9 months and downtime costs rising. Vendors can and do prioritize other clients unless paid premiums, reportedly up to 30% in some 2024 procurement cases.

Capital and technology from JV partners

International JV partners supply drilling technology, capital and offtake solutions to PDVSA, crucial as Venezuela averaged about 1.2 million b/d in 2024; their bargaining power rises when PDVSA liquidity is strained and sanctions limit alternate investors. Contracts commonly include preferential offtake or repayment-in-oil, and technology transfers often entail stringent operational control.

- Drilling tech & capital: leverage for partners

- 2024 production ≈ 1.2 million b/d: dependence driver

- Terms: preferential offtake / repayment-in-oil common

- Tech transfer: tied to operational control

FX, sanctions, and payment risk premia

Suppliers price in hard currency and charge sanctions-related risk premia after US sanctions on PDVSA began in 2019; by 2024 many vendors required oil-linked or barter terms and delayed payment tolerances, shrinking PDVSA’s flexibility.

Compliance burdens and banking de-risking in 2024 further narrowed the supplier pool, increasing concentration and magnifying supplier power over time.

- Hard-currency pricing

- Sanctions risk premia

- Barter/oil settlements

- Supplier concentration

Venezuelan oil: suppliers demand prepayment, 2024 output 700-800 kb/d

PDVSA faces high supplier power due to a narrowed pool of sanction-tolerant oilfield and diluent suppliers, forcing hard-currency, prepayment or oil-for-service terms. 2024 production ≈700–800 kb/d with exports ~600 kb/d, so diluent and maintenance shortages directly cut throughput. Lead times 6–9 months and premiums up to 30% magnify bargaining leverage.

| Metric | 2024 Value |

|---|---|

| Production | 700–800 kb/d |

| Exports | ~600 kb/d |

| Lead times | 6–9 months |

| Supplier premium | up to 30% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored exclusively for PDVSA, uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and regulatory and geopolitical risks shaping pricing, profitability, and strategic positioning.

Concise Porter's Five Forces analysis for PDVSA—one-sheet clarity to pinpoint competitive pressures and regulatory risks, ready to drop into decks and stress-test scenarios without complex setup.

Customers Bargaining Power

Limited qualified buyers for heavy crude

PDVSA’s extra-heavy blends (API < 10) can only be processed by complex coking refineries, concentrating demand among fewer than 30 global facilities in 2024. This limited pool lets compatible buyers push wider differentials—averaging near $12/bbl below Brent in parts of 2024—while buyers with coker capacity extract stronger commercial terms. The concentration makes PDVSA highly sensitive to any buyer exit, risking sharp revenue swings.

Sanctions-driven discounting

Restrictions funnel roughly 0.8 mb/d of PDVSA volumes into a small pool of sanction-tolerant buyers, who extract steep discounts—reported up to $25/bbl in 2023–24—and demand flexible terms to offset legal and reputational risk. Oil-for-debt and transshipment deals further erode pricing power, concentrating sales and lowering negotiating leverage. Netbacks are volatile and commonly 15–30% below regional benchmarks.

China-linked offtake and debt service

China-linked oil-backed loans create quasi-captive offtake for PDVSA, embedding take-or-pay dynamics at discounted prices and tying volumes to debt service obligations in 2024. Renegotiations since 2022 have often preserved lender-offtaker priority, constraining PDVSA’s ability to shift barrels to higher-margin buyers. Volume commitments reduce export optionality while payment netting mechanisms limit cash inflows and working capital flexibility.

Domestic price controls

Domestic buyers face regulated fuel prices and intermittent supply that curb PDVSA’s ability to pass rising costs; in 2024 PDVSA reported continued under-recovery on local sales, with political mandates often overriding commercial terms, shifting losses onto export operations while demand inelasticity limits revenue relief.

- Regulated prices constrain pass-through

- Political mandates > market terms

- Under-recovery shifted to exports (noted in 2024)

- Inelastic domestic demand limits revenue upside

Competing discounted barrels

Competing discounted barrels from Russia (seaborne exports ~5–6 mb/d) and Iran (rebound toward ~0.8–1.0 mb/d in 2023–24) sold $8–20/bbl below Brent compete for the same marginal buyers, letting purchasers force PDVSA to tighten differentials; freight and quality adjustments (typically $1–5/bbl) further erode PDVSA pricing, shifting bargaining power toward buyers in glutted shadow markets.

- Discounts: $8–20/bbl vs Brent

- Russian seaborne: ~5–6 mb/d

- Iranian rebound: ~0.8–1.0 mb/d

- Freight/quality drag: $1–5/bbl

Buyers leverage sinks state crude prices to -$12 - $25/bbl; ~0.8 mb/d

Buyers hold strong leverage: <30 global cokers process PDVSA extra-heavy crudes, pushing differentials near -$12/bbl in 2024 and extracting discounts up to -$25/bbl from sanction-tolerant offtakers; ~0.8 mb/d is funneled to these buyers. Take-or-pay China-linked loans and regulated domestic under-recoveries (netbacks 15–30% below benchmarks) further limit PDVSA pricing flexibility.

| Metric | 2024 value |

|---|---|

| Compatible cokers | <30 |

| Avg differential | ~ -$12/bbl |

| Max discount reported | ~ -$25/bbl |

| Sanction-tolerant flow | ~0.8 mb/d |

| Netback gap vs regional | 15–30% |

Preview the Actual Deliverable

PDVSA Porter's Five Forces Analysis

This preview shows the exact PDVSA Porter’s Five Forces analysis you’ll receive immediately after purchase: a concise, professionally formatted assessment of competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and industry dynamics. No placeholders or samples—this file is ready for immediate download and use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

PDVSA's Porter’s Five Forces highlights strong supplier power, heavy regulatory and geopolitical threats, moderate buyer leverage, steep barriers from state control, and limited substitute risk. This snapshot surfaces key strategic pressure points and vulnerabilities for investors and managers. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to PDVSA.

Suppliers Bargaining Power

Concentrated critical service vendors

PDVSA depends on a narrow pool of oilfield services and EPC suppliers willing to operate under sanctions and arrears, constraining options. With Venezuelan crude output around 700 kbpd in 2024 and major Western firms such as Schlumberger, Halliburton and Baker Hughes having curtailed activities, remaining suppliers gain pricing and schedule leverage. Replacement with Russian, Chinese and Iranian contractors often entails trade-offs in quality, timing and compliance.

Diluent and chemicals dependency

Extra-heavy Orinoco crude requires large diluent volumes, typically 30-50% naphtha or light condensate, creating strong supplier leverage. Limited sourcing routes and US/secondary sanctions since 2019 elevate counterparty risk and supplier power. Diluent shortages directly curtail throughput and exportable volumes; PDVSA exports hovered near 600 kb/d in 2024 as prepayment and premium terms became common in tight windows.

Power, logistics, and maintenance constraints

Unreliable electricity, port congestion, and compromised pipeline integrity force PDVSA to depend on scarce maintenance contractors and imported spare parts, squeezing operations while crude output averaged about 800 kb/d in 2024 per OPEC secondary sources. Suppliers of turbines, pumps, and control systems gained leverage amid chronic shortages, with lead times commonly stretching 6–9 months and downtime costs rising. Vendors can and do prioritize other clients unless paid premiums, reportedly up to 30% in some 2024 procurement cases.

Capital and technology from JV partners

International JV partners supply drilling technology, capital and offtake solutions to PDVSA, crucial as Venezuela averaged about 1.2 million b/d in 2024; their bargaining power rises when PDVSA liquidity is strained and sanctions limit alternate investors. Contracts commonly include preferential offtake or repayment-in-oil, and technology transfers often entail stringent operational control.

- Drilling tech & capital: leverage for partners

- 2024 production ≈ 1.2 million b/d: dependence driver

- Terms: preferential offtake / repayment-in-oil common

- Tech transfer: tied to operational control

FX, sanctions, and payment risk premia

Suppliers price in hard currency and charge sanctions-related risk premia after US sanctions on PDVSA began in 2019; by 2024 many vendors required oil-linked or barter terms and delayed payment tolerances, shrinking PDVSA’s flexibility.

Compliance burdens and banking de-risking in 2024 further narrowed the supplier pool, increasing concentration and magnifying supplier power over time.

- Hard-currency pricing

- Sanctions risk premia

- Barter/oil settlements

- Supplier concentration

Venezuelan oil: suppliers demand prepayment, 2024 output 700-800 kb/d

PDVSA faces high supplier power due to a narrowed pool of sanction-tolerant oilfield and diluent suppliers, forcing hard-currency, prepayment or oil-for-service terms. 2024 production ≈700–800 kb/d with exports ~600 kb/d, so diluent and maintenance shortages directly cut throughput. Lead times 6–9 months and premiums up to 30% magnify bargaining leverage.

| Metric | 2024 Value |

|---|---|

| Production | 700–800 kb/d |

| Exports | ~600 kb/d |

| Lead times | 6–9 months |

| Supplier premium | up to 30% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored exclusively for PDVSA, uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and regulatory and geopolitical risks shaping pricing, profitability, and strategic positioning.

Concise Porter's Five Forces analysis for PDVSA—one-sheet clarity to pinpoint competitive pressures and regulatory risks, ready to drop into decks and stress-test scenarios without complex setup.

Customers Bargaining Power

Limited qualified buyers for heavy crude

PDVSA’s extra-heavy blends (API < 10) can only be processed by complex coking refineries, concentrating demand among fewer than 30 global facilities in 2024. This limited pool lets compatible buyers push wider differentials—averaging near $12/bbl below Brent in parts of 2024—while buyers with coker capacity extract stronger commercial terms. The concentration makes PDVSA highly sensitive to any buyer exit, risking sharp revenue swings.

Sanctions-driven discounting

Restrictions funnel roughly 0.8 mb/d of PDVSA volumes into a small pool of sanction-tolerant buyers, who extract steep discounts—reported up to $25/bbl in 2023–24—and demand flexible terms to offset legal and reputational risk. Oil-for-debt and transshipment deals further erode pricing power, concentrating sales and lowering negotiating leverage. Netbacks are volatile and commonly 15–30% below regional benchmarks.

China-linked offtake and debt service

China-linked oil-backed loans create quasi-captive offtake for PDVSA, embedding take-or-pay dynamics at discounted prices and tying volumes to debt service obligations in 2024. Renegotiations since 2022 have often preserved lender-offtaker priority, constraining PDVSA’s ability to shift barrels to higher-margin buyers. Volume commitments reduce export optionality while payment netting mechanisms limit cash inflows and working capital flexibility.

Domestic price controls

Domestic buyers face regulated fuel prices and intermittent supply that curb PDVSA’s ability to pass rising costs; in 2024 PDVSA reported continued under-recovery on local sales, with political mandates often overriding commercial terms, shifting losses onto export operations while demand inelasticity limits revenue relief.

- Regulated prices constrain pass-through

- Political mandates > market terms

- Under-recovery shifted to exports (noted in 2024)

- Inelastic domestic demand limits revenue upside

Competing discounted barrels

Competing discounted barrels from Russia (seaborne exports ~5–6 mb/d) and Iran (rebound toward ~0.8–1.0 mb/d in 2023–24) sold $8–20/bbl below Brent compete for the same marginal buyers, letting purchasers force PDVSA to tighten differentials; freight and quality adjustments (typically $1–5/bbl) further erode PDVSA pricing, shifting bargaining power toward buyers in glutted shadow markets.

- Discounts: $8–20/bbl vs Brent

- Russian seaborne: ~5–6 mb/d

- Iranian rebound: ~0.8–1.0 mb/d

- Freight/quality drag: $1–5/bbl

Buyers leverage sinks state crude prices to -$12 - $25/bbl; ~0.8 mb/d

Buyers hold strong leverage: <30 global cokers process PDVSA extra-heavy crudes, pushing differentials near -$12/bbl in 2024 and extracting discounts up to -$25/bbl from sanction-tolerant offtakers; ~0.8 mb/d is funneled to these buyers. Take-or-pay China-linked loans and regulated domestic under-recoveries (netbacks 15–30% below benchmarks) further limit PDVSA pricing flexibility.

| Metric | 2024 value |

|---|---|

| Compatible cokers | <30 |

| Avg differential | ~ -$12/bbl |

| Max discount reported | ~ -$25/bbl |

| Sanction-tolerant flow | ~0.8 mb/d |

| Netback gap vs regional | 15–30% |

Preview the Actual Deliverable

PDVSA Porter's Five Forces Analysis

This preview shows the exact PDVSA Porter’s Five Forces analysis you’ll receive immediately after purchase: a concise, professionally formatted assessment of competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and industry dynamics. No placeholders or samples—this file is ready for immediate download and use.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

PDVSA's Porter’s Five Forces highlights strong supplier power, heavy regulatory and geopolitical threats, moderate buyer leverage, steep barriers from state control, and limited substitute risk. This snapshot surfaces key strategic pressure points and vulnerabilities for investors and managers. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to PDVSA.

Suppliers Bargaining Power

Concentrated critical service vendors

PDVSA depends on a narrow pool of oilfield services and EPC suppliers willing to operate under sanctions and arrears, constraining options. With Venezuelan crude output around 700 kbpd in 2024 and major Western firms such as Schlumberger, Halliburton and Baker Hughes having curtailed activities, remaining suppliers gain pricing and schedule leverage. Replacement with Russian, Chinese and Iranian contractors often entails trade-offs in quality, timing and compliance.

Diluent and chemicals dependency

Extra-heavy Orinoco crude requires large diluent volumes, typically 30-50% naphtha or light condensate, creating strong supplier leverage. Limited sourcing routes and US/secondary sanctions since 2019 elevate counterparty risk and supplier power. Diluent shortages directly curtail throughput and exportable volumes; PDVSA exports hovered near 600 kb/d in 2024 as prepayment and premium terms became common in tight windows.

Power, logistics, and maintenance constraints

Unreliable electricity, port congestion, and compromised pipeline integrity force PDVSA to depend on scarce maintenance contractors and imported spare parts, squeezing operations while crude output averaged about 800 kb/d in 2024 per OPEC secondary sources. Suppliers of turbines, pumps, and control systems gained leverage amid chronic shortages, with lead times commonly stretching 6–9 months and downtime costs rising. Vendors can and do prioritize other clients unless paid premiums, reportedly up to 30% in some 2024 procurement cases.

Capital and technology from JV partners

International JV partners supply drilling technology, capital and offtake solutions to PDVSA, crucial as Venezuela averaged about 1.2 million b/d in 2024; their bargaining power rises when PDVSA liquidity is strained and sanctions limit alternate investors. Contracts commonly include preferential offtake or repayment-in-oil, and technology transfers often entail stringent operational control.

- Drilling tech & capital: leverage for partners

- 2024 production ≈ 1.2 million b/d: dependence driver

- Terms: preferential offtake / repayment-in-oil common

- Tech transfer: tied to operational control

FX, sanctions, and payment risk premia

Suppliers price in hard currency and charge sanctions-related risk premia after US sanctions on PDVSA began in 2019; by 2024 many vendors required oil-linked or barter terms and delayed payment tolerances, shrinking PDVSA’s flexibility.

Compliance burdens and banking de-risking in 2024 further narrowed the supplier pool, increasing concentration and magnifying supplier power over time.

- Hard-currency pricing

- Sanctions risk premia

- Barter/oil settlements

- Supplier concentration

Venezuelan oil: suppliers demand prepayment, 2024 output 700-800 kb/d

PDVSA faces high supplier power due to a narrowed pool of sanction-tolerant oilfield and diluent suppliers, forcing hard-currency, prepayment or oil-for-service terms. 2024 production ≈700–800 kb/d with exports ~600 kb/d, so diluent and maintenance shortages directly cut throughput. Lead times 6–9 months and premiums up to 30% magnify bargaining leverage.

| Metric | 2024 Value |

|---|---|

| Production | 700–800 kb/d |

| Exports | ~600 kb/d |

| Lead times | 6–9 months |

| Supplier premium | up to 30% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored exclusively for PDVSA, uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and regulatory and geopolitical risks shaping pricing, profitability, and strategic positioning.

Concise Porter's Five Forces analysis for PDVSA—one-sheet clarity to pinpoint competitive pressures and regulatory risks, ready to drop into decks and stress-test scenarios without complex setup.

Customers Bargaining Power

Limited qualified buyers for heavy crude

PDVSA’s extra-heavy blends (API < 10) can only be processed by complex coking refineries, concentrating demand among fewer than 30 global facilities in 2024. This limited pool lets compatible buyers push wider differentials—averaging near $12/bbl below Brent in parts of 2024—while buyers with coker capacity extract stronger commercial terms. The concentration makes PDVSA highly sensitive to any buyer exit, risking sharp revenue swings.

Sanctions-driven discounting

Restrictions funnel roughly 0.8 mb/d of PDVSA volumes into a small pool of sanction-tolerant buyers, who extract steep discounts—reported up to $25/bbl in 2023–24—and demand flexible terms to offset legal and reputational risk. Oil-for-debt and transshipment deals further erode pricing power, concentrating sales and lowering negotiating leverage. Netbacks are volatile and commonly 15–30% below regional benchmarks.

China-linked offtake and debt service

China-linked oil-backed loans create quasi-captive offtake for PDVSA, embedding take-or-pay dynamics at discounted prices and tying volumes to debt service obligations in 2024. Renegotiations since 2022 have often preserved lender-offtaker priority, constraining PDVSA’s ability to shift barrels to higher-margin buyers. Volume commitments reduce export optionality while payment netting mechanisms limit cash inflows and working capital flexibility.

Domestic price controls

Domestic buyers face regulated fuel prices and intermittent supply that curb PDVSA’s ability to pass rising costs; in 2024 PDVSA reported continued under-recovery on local sales, with political mandates often overriding commercial terms, shifting losses onto export operations while demand inelasticity limits revenue relief.

- Regulated prices constrain pass-through

- Political mandates > market terms

- Under-recovery shifted to exports (noted in 2024)

- Inelastic domestic demand limits revenue upside

Competing discounted barrels

Competing discounted barrels from Russia (seaborne exports ~5–6 mb/d) and Iran (rebound toward ~0.8–1.0 mb/d in 2023–24) sold $8–20/bbl below Brent compete for the same marginal buyers, letting purchasers force PDVSA to tighten differentials; freight and quality adjustments (typically $1–5/bbl) further erode PDVSA pricing, shifting bargaining power toward buyers in glutted shadow markets.

- Discounts: $8–20/bbl vs Brent

- Russian seaborne: ~5–6 mb/d

- Iranian rebound: ~0.8–1.0 mb/d

- Freight/quality drag: $1–5/bbl

Buyers leverage sinks state crude prices to -$12 - $25/bbl; ~0.8 mb/d

Buyers hold strong leverage: <30 global cokers process PDVSA extra-heavy crudes, pushing differentials near -$12/bbl in 2024 and extracting discounts up to -$25/bbl from sanction-tolerant offtakers; ~0.8 mb/d is funneled to these buyers. Take-or-pay China-linked loans and regulated domestic under-recoveries (netbacks 15–30% below benchmarks) further limit PDVSA pricing flexibility.

| Metric | 2024 value |

|---|---|

| Compatible cokers | <30 |

| Avg differential | ~ -$12/bbl |

| Max discount reported | ~ -$25/bbl |

| Sanction-tolerant flow | ~0.8 mb/d |

| Netback gap vs regional | 15–30% |

Preview the Actual Deliverable

PDVSA Porter's Five Forces Analysis

This preview shows the exact PDVSA Porter’s Five Forces analysis you’ll receive immediately after purchase: a concise, professionally formatted assessment of competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and industry dynamics. No placeholders or samples—this file is ready for immediate download and use.