Peabody PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political regulation, commodity cycles, and environmental pressures are reshaping Peabody’s strategic outlook in our concise PESTLE snapshot. This analysis highlights risks and opportunities investors and strategists need now. Purchase the full PESTLE for the complete, actionable breakdown and ready-to-use insights.

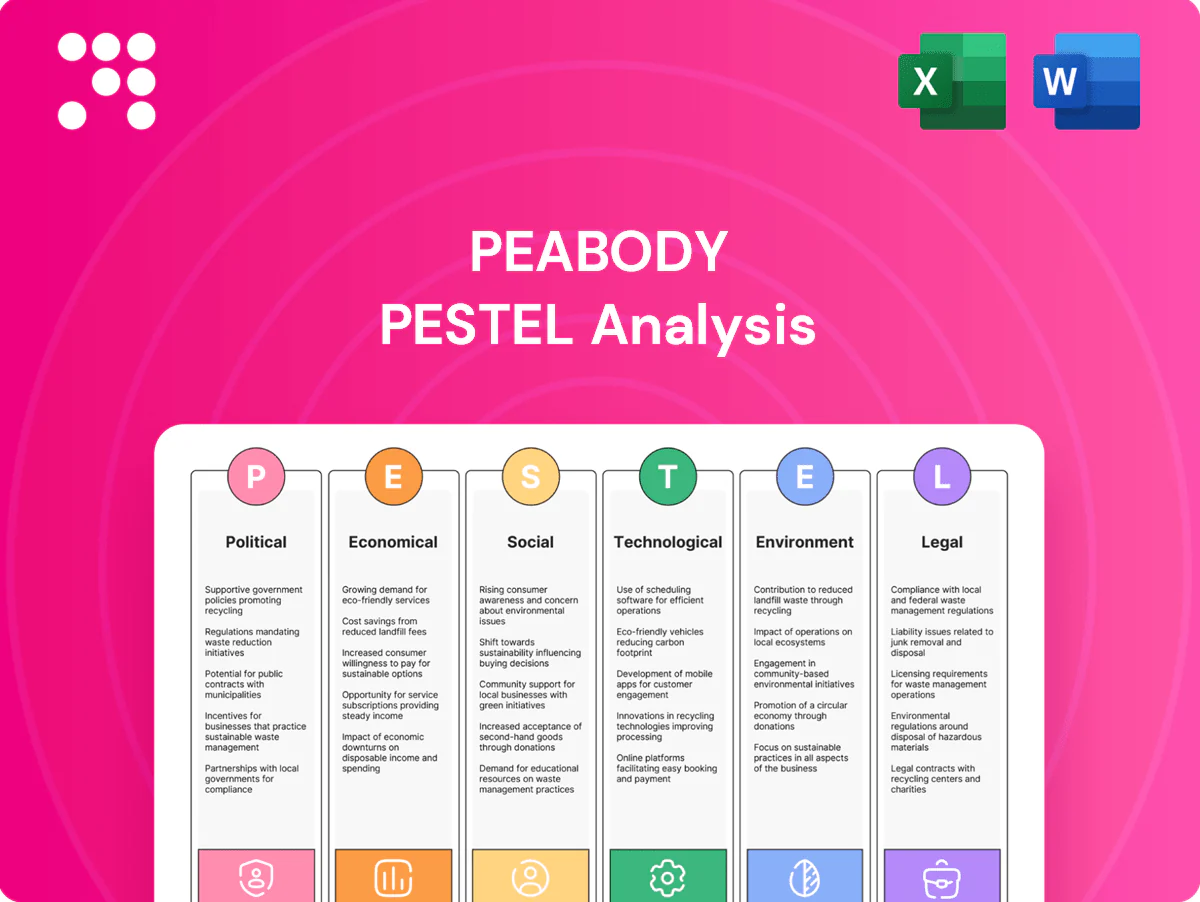

Political factors

US-Australia energy policy shifts

US and Australian policy shifts — including the US Inflation Reduction Act's roughly 369 billion dollar energy incentives — materially affect coal demand, permitting and subsidies for alternatives; US coal-fired generation was about 19% of electricity in 2023, pressuring thermal markets. Elections can rapidly pivot between energy security and decarbonization, forcing Peabody to scenario-plan budgets and capital allocations. Active engagement with federal and state agencies mitigates permitting and policy risk.

Permitting and federal-state dynamics

Complex, multi-layered federal, state and local approvals routinely delay Peabody mine plans and expansions, with regulatory scrutiny intensifying in 2024 and adding months to project timelines. Stricter environmental assessments have extended review windows and raised compliance costs, pressuring project IRRs. Proactive stakeholder mapping and phased submissions demonstrably reduce bottlenecks. Maintaining high compliance KPIs builds regulator trust and smooths approvals.

Trade relations with Asian buyers

Seaborne thermal and metallurgical volumes are highly exposed to stable ties with Japan, South Korea, India and Southeast Asia, which together take roughly three quarters of global seaborne coal trade. Tariffs, quotas or diplomatic rifts can quickly reroute flows and compress pricing. Peabody's diversified offtake and flexible contracting mitigate disruption. Active monitoring of regional trade agreements (RCEP, bilateral pacts) hedges market-access risk.

Maritime security and logistics corridors

Geopolitical tension in key sea lanes — notably Red Sea incidents in 2023–24 and Panama Canal drought-related restrictions in 2023–25 — elevated freight-rate volatility and reliability risk, with war-risk surcharges reported up to $50,000–$200,000 per voyage for affected routings. Disruptions in the Indo-Pacific or Suez materially alter voyage economics; chartering optionality across ports sustains exports while insurance and routing contingencies ensure continuity.

- Freight volatility: war-risk surcharges up to $50k–$200k

- Canal constraints: Panama drought restrictions 2023–25

- Chartering: flexibility across ports mitigates downtime

- Insure/reroute: essential to maintain export flows

Government support for transition

- Public funds: IRA 369B; IIJA grid 65B

- Steel decarb incentives: shifting met-coal demand

- Retraining programs: workforce & community stability

- Policy intelligence: asset-life & divestment timing

IRA/IIJA hit coal demand; US coal 19% (2023); war-risk fees $50k–$200k

US IRA 369B and IIJA 65B shift incentives away from coal; US coal 19% of power in 2023 pressures thermal demand. Seaborne trade ~75% tied to Japan/Korea/India/SE Asia; geopolitical shocks (Red Sea, Panama drought) drove war-risk surcharges $50k–$200k per voyage, raising export costs and forcing contracting flexibility.

| Factor | Metric | Impact |

|---|---|---|

| IRA | $369B | Incentives tilt to clean energy |

| IIJA | $65B | Grid resilience, lower coal demand |

| US coal share | 19% (2023) | Thermal market pressure |

| Seaborne share | ~75% | Export exposure |

| War-risk | $50k–$200k | Freight cost volatility |

What is included in the product

Provides a concise PESTLE review of Peabody, examining Political, Economic, Social, Technological, Environmental and Legal forces with data-backed trends and region-specific regulatory context; designed to identify threats, opportunities and strategic scenarios for executives, investors and consultants, and delivered in clean, report-ready format with forward-looking insights for planning and funding decisions.

Condensed Peabody PESTLE analysis that distills regulatory, environmental, economic and geopolitical risks into a single, shareable summary for fast decision-making; ideal for slides or team briefings and easily annotated with local or business-line notes.

Economic factors

Coal price volatility

Thermal and metallurgical coal prices swing with weather, inventory cycles and steel output; Newcastle thermal averaged about $120–140/t in 2024 while PRB spot traded near $12–18/short ton. Peabody's earnings leverage magnifies cycles—adjusted EBITDA has swung >50% YoY in recent up/downturns. Hedging and flexible contracts smooth cash-flow volatility. A portfolio split across PRB, seaborne thermal and met grades tempers price swings.

FX and commodity inputs

Movements in USD/AUD (AUD averaged about US$0.66 in 2024 and ~US$0.64 in early 2025) materially affect Peabody’s Australian cost competitiveness and translated USD earnings. Diesel, explosives and steel — with diesel up ~12% y/y in 2024 and hot‑rolled coil near US$700/t — are major drivers of mining unit costs. Rising inflation (Australia CPI ~3.4% in 2024) lifts unit costs and increases reclamation liabilities. Procurement strategies and long‑term supply contracts help stabilize margins by locking prices and supply.

Freight and logistics costs

Bulk shipping rates and rail availability directly shape Peabody’s delivered costs to customers, with BNSF and Union Pacific handling roughly 70% of US coal rail haul and setting pricing and capacity dynamics. Congestion or labor disruptions at key ports and rail networks have repeatedly reduced reliability and raised demurrage and dwell costs. Take-or-pay rail and port contracts provide revenue certainty but limit operational flexibility and can lock in fixed logistics costs. Active logistics management and routing optimization preserve netbacks by minimizing empty miles, dwell and demurrage.

Power and steel demand cycles

Peabody faces thermal coal burn tied to electricity demand and fuel mix: US electricity use rose ~0.8% in 2024 (EIA) while Henry Hub averaged about $2.87/MMBtu in 2024, and hydro/nuclear outages swing dispatch and thermal burn; metallurgical demand tracks global crude steel ~1.9 billion t in 2024 (World Steel Association). Monitoring blast-furnace vs EAF share guides pricing and quality premia; counterparty credit risk rises in steel downturns.

- Electricity demand: US +0.8% (2024)

- Gas price: Henry Hub ~$2.87/MMBtu (2024)

- Steel output: ~1.9bn t (2024)

- Strategy: track BF vs EAF, tighten credit in downturns

Capital access and balance sheet

Rising rates (US fed funds ~5.25–5.50% mid‑2025) and widening ESG screens constrain low‑cost financing for thermal coal, forcing higher borrowing costs and fewer lender options for Peabody.

Strong free cash flow funds reclamation, dividends and buybacks while maintaining low leverage (net debt/EBITDA under 1x in 2024) improves resilience across cycles; disciplined capex protects returns amid uncertain demand.

- Rates: fed funds ~5.25–5.50% (mid‑2025)

- Leverage: net debt/EBITDA <1x (2024)

- Uses: reclamation, dividends, buybacks funded from FCF

- Capex: disciplined to protect returns vs demand uncertainty

IRA/IIJA hit coal demand; US coal 19% (2023); war-risk fees $50k–$200k

Coal prices (Newcastle ~$120–140/t 2024; PRB ~$12–18/short ton) and FX (AUD ~US$0.64–0.66) drive earnings volatility; hedges and portfolio mix reduce swings. Input costs (diesel +~12% y/y 2024; Aus CPI ~3.4%) and logistics constrain margins. Strong FCF and net debt/EBITDA <1x (2024) support reclamation, dividends and disciplined capex.

| Metric | 2024/2025 |

|---|---|

| Newcastle | $120–140/t (2024) |

| PRB | $12–18/st (2024) |

| Henry Hub | $2.87/MMBtu (2024) |

| Fed funds | 5.25–5.50% (mid‑2025) |

Full Version Awaits

Peabody PESTLE Analysis

This Peabody PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The layout, content, and insights shown here match the final downloadable file, with no placeholders or surprises. After payment you’ll be able to download this same finished report immediately.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political regulation, commodity cycles, and environmental pressures are reshaping Peabody’s strategic outlook in our concise PESTLE snapshot. This analysis highlights risks and opportunities investors and strategists need now. Purchase the full PESTLE for the complete, actionable breakdown and ready-to-use insights.

Political factors

US-Australia energy policy shifts

US and Australian policy shifts — including the US Inflation Reduction Act's roughly 369 billion dollar energy incentives — materially affect coal demand, permitting and subsidies for alternatives; US coal-fired generation was about 19% of electricity in 2023, pressuring thermal markets. Elections can rapidly pivot between energy security and decarbonization, forcing Peabody to scenario-plan budgets and capital allocations. Active engagement with federal and state agencies mitigates permitting and policy risk.

Permitting and federal-state dynamics

Complex, multi-layered federal, state and local approvals routinely delay Peabody mine plans and expansions, with regulatory scrutiny intensifying in 2024 and adding months to project timelines. Stricter environmental assessments have extended review windows and raised compliance costs, pressuring project IRRs. Proactive stakeholder mapping and phased submissions demonstrably reduce bottlenecks. Maintaining high compliance KPIs builds regulator trust and smooths approvals.

Trade relations with Asian buyers

Seaborne thermal and metallurgical volumes are highly exposed to stable ties with Japan, South Korea, India and Southeast Asia, which together take roughly three quarters of global seaborne coal trade. Tariffs, quotas or diplomatic rifts can quickly reroute flows and compress pricing. Peabody's diversified offtake and flexible contracting mitigate disruption. Active monitoring of regional trade agreements (RCEP, bilateral pacts) hedges market-access risk.

Maritime security and logistics corridors

Geopolitical tension in key sea lanes — notably Red Sea incidents in 2023–24 and Panama Canal drought-related restrictions in 2023–25 — elevated freight-rate volatility and reliability risk, with war-risk surcharges reported up to $50,000–$200,000 per voyage for affected routings. Disruptions in the Indo-Pacific or Suez materially alter voyage economics; chartering optionality across ports sustains exports while insurance and routing contingencies ensure continuity.

- Freight volatility: war-risk surcharges up to $50k–$200k

- Canal constraints: Panama drought restrictions 2023–25

- Chartering: flexibility across ports mitigates downtime

- Insure/reroute: essential to maintain export flows

Government support for transition

- Public funds: IRA 369B; IIJA grid 65B

- Steel decarb incentives: shifting met-coal demand

- Retraining programs: workforce & community stability

- Policy intelligence: asset-life & divestment timing

IRA/IIJA hit coal demand; US coal 19% (2023); war-risk fees $50k–$200k

US IRA 369B and IIJA 65B shift incentives away from coal; US coal 19% of power in 2023 pressures thermal demand. Seaborne trade ~75% tied to Japan/Korea/India/SE Asia; geopolitical shocks (Red Sea, Panama drought) drove war-risk surcharges $50k–$200k per voyage, raising export costs and forcing contracting flexibility.

| Factor | Metric | Impact |

|---|---|---|

| IRA | $369B | Incentives tilt to clean energy |

| IIJA | $65B | Grid resilience, lower coal demand |

| US coal share | 19% (2023) | Thermal market pressure |

| Seaborne share | ~75% | Export exposure |

| War-risk | $50k–$200k | Freight cost volatility |

What is included in the product

Provides a concise PESTLE review of Peabody, examining Political, Economic, Social, Technological, Environmental and Legal forces with data-backed trends and region-specific regulatory context; designed to identify threats, opportunities and strategic scenarios for executives, investors and consultants, and delivered in clean, report-ready format with forward-looking insights for planning and funding decisions.

Condensed Peabody PESTLE analysis that distills regulatory, environmental, economic and geopolitical risks into a single, shareable summary for fast decision-making; ideal for slides or team briefings and easily annotated with local or business-line notes.

Economic factors

Coal price volatility

Thermal and metallurgical coal prices swing with weather, inventory cycles and steel output; Newcastle thermal averaged about $120–140/t in 2024 while PRB spot traded near $12–18/short ton. Peabody's earnings leverage magnifies cycles—adjusted EBITDA has swung >50% YoY in recent up/downturns. Hedging and flexible contracts smooth cash-flow volatility. A portfolio split across PRB, seaborne thermal and met grades tempers price swings.

FX and commodity inputs

Movements in USD/AUD (AUD averaged about US$0.66 in 2024 and ~US$0.64 in early 2025) materially affect Peabody’s Australian cost competitiveness and translated USD earnings. Diesel, explosives and steel — with diesel up ~12% y/y in 2024 and hot‑rolled coil near US$700/t — are major drivers of mining unit costs. Rising inflation (Australia CPI ~3.4% in 2024) lifts unit costs and increases reclamation liabilities. Procurement strategies and long‑term supply contracts help stabilize margins by locking prices and supply.

Freight and logistics costs

Bulk shipping rates and rail availability directly shape Peabody’s delivered costs to customers, with BNSF and Union Pacific handling roughly 70% of US coal rail haul and setting pricing and capacity dynamics. Congestion or labor disruptions at key ports and rail networks have repeatedly reduced reliability and raised demurrage and dwell costs. Take-or-pay rail and port contracts provide revenue certainty but limit operational flexibility and can lock in fixed logistics costs. Active logistics management and routing optimization preserve netbacks by minimizing empty miles, dwell and demurrage.

Power and steel demand cycles

Peabody faces thermal coal burn tied to electricity demand and fuel mix: US electricity use rose ~0.8% in 2024 (EIA) while Henry Hub averaged about $2.87/MMBtu in 2024, and hydro/nuclear outages swing dispatch and thermal burn; metallurgical demand tracks global crude steel ~1.9 billion t in 2024 (World Steel Association). Monitoring blast-furnace vs EAF share guides pricing and quality premia; counterparty credit risk rises in steel downturns.

- Electricity demand: US +0.8% (2024)

- Gas price: Henry Hub ~$2.87/MMBtu (2024)

- Steel output: ~1.9bn t (2024)

- Strategy: track BF vs EAF, tighten credit in downturns

Capital access and balance sheet

Rising rates (US fed funds ~5.25–5.50% mid‑2025) and widening ESG screens constrain low‑cost financing for thermal coal, forcing higher borrowing costs and fewer lender options for Peabody.

Strong free cash flow funds reclamation, dividends and buybacks while maintaining low leverage (net debt/EBITDA under 1x in 2024) improves resilience across cycles; disciplined capex protects returns amid uncertain demand.

- Rates: fed funds ~5.25–5.50% (mid‑2025)

- Leverage: net debt/EBITDA <1x (2024)

- Uses: reclamation, dividends, buybacks funded from FCF

- Capex: disciplined to protect returns vs demand uncertainty

IRA/IIJA hit coal demand; US coal 19% (2023); war-risk fees $50k–$200k

Coal prices (Newcastle ~$120–140/t 2024; PRB ~$12–18/short ton) and FX (AUD ~US$0.64–0.66) drive earnings volatility; hedges and portfolio mix reduce swings. Input costs (diesel +~12% y/y 2024; Aus CPI ~3.4%) and logistics constrain margins. Strong FCF and net debt/EBITDA <1x (2024) support reclamation, dividends and disciplined capex.

| Metric | 2024/2025 |

|---|---|

| Newcastle | $120–140/t (2024) |

| PRB | $12–18/st (2024) |

| Henry Hub | $2.87/MMBtu (2024) |

| Fed funds | 5.25–5.50% (mid‑2025) |

Full Version Awaits

Peabody PESTLE Analysis

This Peabody PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The layout, content, and insights shown here match the final downloadable file, with no placeholders or surprises. After payment you’ll be able to download this same finished report immediately.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political regulation, commodity cycles, and environmental pressures are reshaping Peabody’s strategic outlook in our concise PESTLE snapshot. This analysis highlights risks and opportunities investors and strategists need now. Purchase the full PESTLE for the complete, actionable breakdown and ready-to-use insights.

Political factors

US-Australia energy policy shifts

US and Australian policy shifts — including the US Inflation Reduction Act's roughly 369 billion dollar energy incentives — materially affect coal demand, permitting and subsidies for alternatives; US coal-fired generation was about 19% of electricity in 2023, pressuring thermal markets. Elections can rapidly pivot between energy security and decarbonization, forcing Peabody to scenario-plan budgets and capital allocations. Active engagement with federal and state agencies mitigates permitting and policy risk.

Permitting and federal-state dynamics

Complex, multi-layered federal, state and local approvals routinely delay Peabody mine plans and expansions, with regulatory scrutiny intensifying in 2024 and adding months to project timelines. Stricter environmental assessments have extended review windows and raised compliance costs, pressuring project IRRs. Proactive stakeholder mapping and phased submissions demonstrably reduce bottlenecks. Maintaining high compliance KPIs builds regulator trust and smooths approvals.

Trade relations with Asian buyers

Seaborne thermal and metallurgical volumes are highly exposed to stable ties with Japan, South Korea, India and Southeast Asia, which together take roughly three quarters of global seaborne coal trade. Tariffs, quotas or diplomatic rifts can quickly reroute flows and compress pricing. Peabody's diversified offtake and flexible contracting mitigate disruption. Active monitoring of regional trade agreements (RCEP, bilateral pacts) hedges market-access risk.

Maritime security and logistics corridors

Geopolitical tension in key sea lanes — notably Red Sea incidents in 2023–24 and Panama Canal drought-related restrictions in 2023–25 — elevated freight-rate volatility and reliability risk, with war-risk surcharges reported up to $50,000–$200,000 per voyage for affected routings. Disruptions in the Indo-Pacific or Suez materially alter voyage economics; chartering optionality across ports sustains exports while insurance and routing contingencies ensure continuity.

- Freight volatility: war-risk surcharges up to $50k–$200k

- Canal constraints: Panama drought restrictions 2023–25

- Chartering: flexibility across ports mitigates downtime

- Insure/reroute: essential to maintain export flows

Government support for transition

- Public funds: IRA 369B; IIJA grid 65B

- Steel decarb incentives: shifting met-coal demand

- Retraining programs: workforce & community stability

- Policy intelligence: asset-life & divestment timing

IRA/IIJA hit coal demand; US coal 19% (2023); war-risk fees $50k–$200k

US IRA 369B and IIJA 65B shift incentives away from coal; US coal 19% of power in 2023 pressures thermal demand. Seaborne trade ~75% tied to Japan/Korea/India/SE Asia; geopolitical shocks (Red Sea, Panama drought) drove war-risk surcharges $50k–$200k per voyage, raising export costs and forcing contracting flexibility.

| Factor | Metric | Impact |

|---|---|---|

| IRA | $369B | Incentives tilt to clean energy |

| IIJA | $65B | Grid resilience, lower coal demand |

| US coal share | 19% (2023) | Thermal market pressure |

| Seaborne share | ~75% | Export exposure |

| War-risk | $50k–$200k | Freight cost volatility |

What is included in the product

Provides a concise PESTLE review of Peabody, examining Political, Economic, Social, Technological, Environmental and Legal forces with data-backed trends and region-specific regulatory context; designed to identify threats, opportunities and strategic scenarios for executives, investors and consultants, and delivered in clean, report-ready format with forward-looking insights for planning and funding decisions.

Condensed Peabody PESTLE analysis that distills regulatory, environmental, economic and geopolitical risks into a single, shareable summary for fast decision-making; ideal for slides or team briefings and easily annotated with local or business-line notes.

Economic factors

Coal price volatility

Thermal and metallurgical coal prices swing with weather, inventory cycles and steel output; Newcastle thermal averaged about $120–140/t in 2024 while PRB spot traded near $12–18/short ton. Peabody's earnings leverage magnifies cycles—adjusted EBITDA has swung >50% YoY in recent up/downturns. Hedging and flexible contracts smooth cash-flow volatility. A portfolio split across PRB, seaborne thermal and met grades tempers price swings.

FX and commodity inputs

Movements in USD/AUD (AUD averaged about US$0.66 in 2024 and ~US$0.64 in early 2025) materially affect Peabody’s Australian cost competitiveness and translated USD earnings. Diesel, explosives and steel — with diesel up ~12% y/y in 2024 and hot‑rolled coil near US$700/t — are major drivers of mining unit costs. Rising inflation (Australia CPI ~3.4% in 2024) lifts unit costs and increases reclamation liabilities. Procurement strategies and long‑term supply contracts help stabilize margins by locking prices and supply.

Freight and logistics costs

Bulk shipping rates and rail availability directly shape Peabody’s delivered costs to customers, with BNSF and Union Pacific handling roughly 70% of US coal rail haul and setting pricing and capacity dynamics. Congestion or labor disruptions at key ports and rail networks have repeatedly reduced reliability and raised demurrage and dwell costs. Take-or-pay rail and port contracts provide revenue certainty but limit operational flexibility and can lock in fixed logistics costs. Active logistics management and routing optimization preserve netbacks by minimizing empty miles, dwell and demurrage.

Power and steel demand cycles

Peabody faces thermal coal burn tied to electricity demand and fuel mix: US electricity use rose ~0.8% in 2024 (EIA) while Henry Hub averaged about $2.87/MMBtu in 2024, and hydro/nuclear outages swing dispatch and thermal burn; metallurgical demand tracks global crude steel ~1.9 billion t in 2024 (World Steel Association). Monitoring blast-furnace vs EAF share guides pricing and quality premia; counterparty credit risk rises in steel downturns.

- Electricity demand: US +0.8% (2024)

- Gas price: Henry Hub ~$2.87/MMBtu (2024)

- Steel output: ~1.9bn t (2024)

- Strategy: track BF vs EAF, tighten credit in downturns

Capital access and balance sheet

Rising rates (US fed funds ~5.25–5.50% mid‑2025) and widening ESG screens constrain low‑cost financing for thermal coal, forcing higher borrowing costs and fewer lender options for Peabody.

Strong free cash flow funds reclamation, dividends and buybacks while maintaining low leverage (net debt/EBITDA under 1x in 2024) improves resilience across cycles; disciplined capex protects returns amid uncertain demand.

- Rates: fed funds ~5.25–5.50% (mid‑2025)

- Leverage: net debt/EBITDA <1x (2024)

- Uses: reclamation, dividends, buybacks funded from FCF

- Capex: disciplined to protect returns vs demand uncertainty

IRA/IIJA hit coal demand; US coal 19% (2023); war-risk fees $50k–$200k

Coal prices (Newcastle ~$120–140/t 2024; PRB ~$12–18/short ton) and FX (AUD ~US$0.64–0.66) drive earnings volatility; hedges and portfolio mix reduce swings. Input costs (diesel +~12% y/y 2024; Aus CPI ~3.4%) and logistics constrain margins. Strong FCF and net debt/EBITDA <1x (2024) support reclamation, dividends and disciplined capex.

| Metric | 2024/2025 |

|---|---|

| Newcastle | $120–140/t (2024) |

| PRB | $12–18/st (2024) |

| Henry Hub | $2.87/MMBtu (2024) |

| Fed funds | 5.25–5.50% (mid‑2025) |

Full Version Awaits

Peabody PESTLE Analysis

This Peabody PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The layout, content, and insights shown here match the final downloadable file, with no placeholders or surprises. After payment you’ll be able to download this same finished report immediately.