Parpro Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

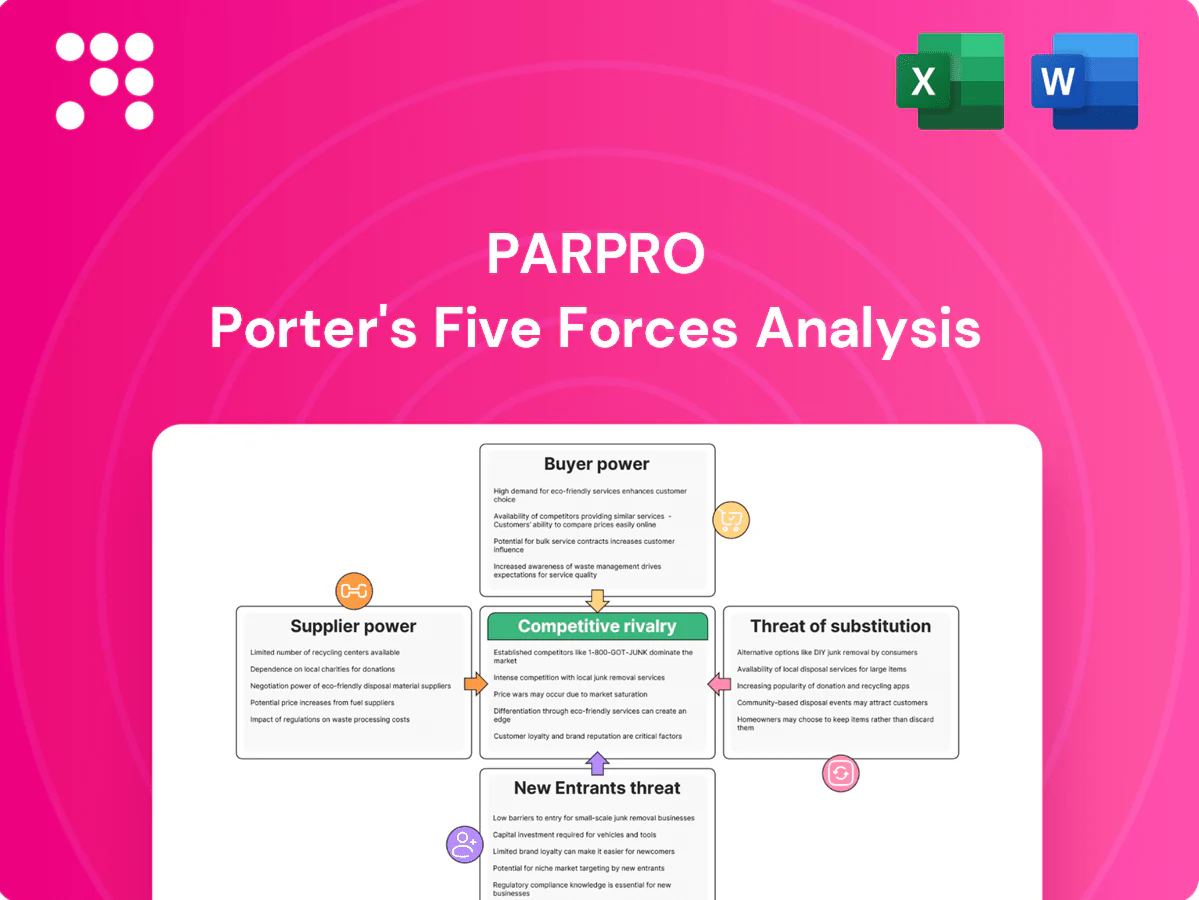

Parpro's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, barriers to entry, and substitute threats to reveal strategic pressure points. It surfaces key risks and opportunities shaping margins and growth. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated CPU and chipset sources

In 2024 CPU and GPU roadmaps remain concentrated among a few vendors—Intel, AMD, NVIDIA and leading ARM SoC suppliers—who together exert >70% influence over platform directions, concentrating supplier power. Allocation cycles and priority access favor large OEMs, pressuring pricing and lead times. Parpro can reduce risk by multi-CPU support, but validation costs raise switching frictions. Long-term supply contracts and demand forecasting cut volatility.

Long-lead critical components

Long-lead critical components give suppliers leverage in tight markets: 2024 industry reports showed industrial-grade memory lead times of 12–20 weeks, power modules 16–24 weeks, and specialized connectors 10–18 weeks. Qualification and compliance constraints limit immediate substitutions and second-source design adds engineering and capex burden. Maintaining buffer inventory raises working capital needs by tying up months of cash, and suppliers often impose NCNR terms, shifting risk to Parpro.

Display panels and rugged enclosures

Industrial display panel and rugged enclosure supply remains relatively fragmented, moderating supplier power despite dominance of large fabs in consumer panels. Custom mechanicals and optical specs create lock-in across product lifecycles, with UL/IP certification often taking 6–12 months and costs commonly exceeding $50,000. Tooling investments and certification make switches costly; volume commitments can secure 10–25% price breaks but reduce flexibility.

Software stacks and OS licensing

Software stacks and OS licensing (Windows IoT, Linux distributions) materially affect BOM and support costs: Windows IoT LTSC offers up to 10 years of support (2024), Ubuntu LTS provides 5 years, and driver ecosystems drive recurring R&D and warranty spend. Switching OS/middleware requires retraining, recertification and customer requalification, granting moderate leverage to software vendors. Security patch cadence and LTSC terms shape lifecycle promises; negotiated enterprise licenses often cut list prices by ~20–40%.

- Windows IoT: up to 10y LTSC (2024)

- Linux: 5y LTS common (Ubuntu)

- Switch costs: retrain, recert, requalify

- Enterprise discounts: ~20–40%

Upstream PCB fabs and EMS capacity

- Geographic concentration: ~66% of PCB fabs in China (2024)

- Lead times: 6–10 weeks typical (2024)

- Market size: EMS >500B USD (2024)

- Mitigants: dual-region sourcing, DFX

Supply: CPUs/GPUs > 70%, 12–24wk waits, ~66%

Supplier power is high: CPU/GPU vendors control >70% platform direction (2024), long-lead parts drive 12–24 week waits, and PCB fabs concentrated ~66% in China. Switching costs (validation, certification, tooling) and NCNR terms raise friction; long-term contracts, multi-sourcing and buffer stock are primary mitigants.

| Metric | 2024 |

|---|---|

| CPU/GPU market influence | >70% |

| Memory lead times | 12–20 wks |

| PCB fabs in China | ~66% |

| EMS market | >500B USD |

What is included in the product

Concise Porter's Five Forces assessment tailored for Parpro, uncovering competitive intensity, buyer/supplier leverage, substitution risks, and entry barriers with strategic implications for pricing and profitability.

A compact, customizable Parpro Porter's Five Forces tool that turns complex competitive dynamics into actionable insights—visual radar, editable inputs, and slide-ready summaries relieve decision-making friction and speed strategic responses.

Customers Bargaining Power

Large OEMs and system integrators

Large OEMs and system integrators in automation, transportation and healthcare run formal RFPs and buy in large volumes, giving them high leverage and enabling benchmarking on price, delivery and specs; in 2024 top OEMs accounted for roughly 35–45% of category purchasing in several mature segments. Framework agreements commonly demand volume discounts and penalty clauses, squeezing margins. Parpro must pivot to TCO-led sell and premium service SLAs to defend margins and retain contracts.

Customization increases stickiness

Tailored designs integrate deeply into customer systems, raising switching costs as firmware, drivers and mechanical fit require requalification that can add 6–12 months and tens to hundreds of thousands USD in validation costs; this materially reduces buyer power post-integration, while upfront NRE pricing and contract terms remain the primary negotiation leverage for purchasers in 2024.

Regulatory and lifecycle requirements

Certifications EN 50155, IEC 60601 and stringent EMC rules plus 5–10+ year availability commitments in rail and medical lifecycles make buyers highly reluctant to change suppliers, since replacements require costly revalidation and downtime that can take weeks to months.

This stickiness shifts bargaining power toward Parpro on incumbent programs, though buyers still demand last-time-buy flexibility and formal EOL notices to manage inventory and risk.

Spec parity and price transparency

Many embedded PC vendors offered near-spec parity in 2024, and public datasheets plus benchmark databases such as SPEC and PassMark enabled direct side-by-side comparisons, driving buyers to shop primarily on price. Buyers increasingly threaten dual-sourcing for volume discounts, forcing vendors to justify any premium through measurable value-added services like extended support, certified integrations, or custom firmware. Transparent component sourcing and distributor price listings keep margins under pressure.

- Spec parity: public datasheets + SPEC/PassMark (2024)

- Price transparency: distributor catalogs accessible online

- Dual-sourcing threat: common buyer negotiation tactic

- Premium justification: must be tied to measurable services

Service, SLAs, and TCO pressures

Buyers push for extended warranties, on-site support, and strict SLAs, with 2024 buyer surveys showing uptime targets of 99.9% or higher commonly demanded.

They evaluate downtime risk and field maintainability—since outages can cost enterprises six-figure sums per day—shaping tougher negotiation terms.

Strong after-sales performance lowers price sensitivity, while weak support immediately increases buyer bargaining power and contract concessions.

- Extended warranties demanded

- On-site support priority

- SLAs commonly 99.9%+ uptime

- Downtime = six-figure daily risk

- After-sales reduces price pressure

RFP leverage vs incumbent lock-in: top OEMs 35–45%, validation 6–12m, SLAs 99.9%+

Buyers hold strong upfront leverage via RFPs and volume (top OEMs 35–45% share in mature segments, 2024), but incumbent stickiness from certifications and integrations (validation 6–12 months, validation costs tens–hundreds k USD) shifts power to Parpro on live programs. Price pressure rises from spec parity and transparent benchmarks; buyers demand 99.9%+ SLAs and threaten dual-sourcing.

| Metric | 2024 |

|---|---|

| Top OEM share | 35–45% |

| Validation time | 6–12 months |

| Validation cost | 10^4–10^5+ USD |

| Uptime SLAs | 99.9%+ |

Same Document Delivered

Parpro Porter's Five Forces Analysis

This preview shows the exact Parpro Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document here is fully formatted, professionally written, and ready for download and use the moment you buy. You're getting the final deliverable as displayed, with no further setup required.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Parpro's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, barriers to entry, and substitute threats to reveal strategic pressure points. It surfaces key risks and opportunities shaping margins and growth. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated CPU and chipset sources

In 2024 CPU and GPU roadmaps remain concentrated among a few vendors—Intel, AMD, NVIDIA and leading ARM SoC suppliers—who together exert >70% influence over platform directions, concentrating supplier power. Allocation cycles and priority access favor large OEMs, pressuring pricing and lead times. Parpro can reduce risk by multi-CPU support, but validation costs raise switching frictions. Long-term supply contracts and demand forecasting cut volatility.

Long-lead critical components

Long-lead critical components give suppliers leverage in tight markets: 2024 industry reports showed industrial-grade memory lead times of 12–20 weeks, power modules 16–24 weeks, and specialized connectors 10–18 weeks. Qualification and compliance constraints limit immediate substitutions and second-source design adds engineering and capex burden. Maintaining buffer inventory raises working capital needs by tying up months of cash, and suppliers often impose NCNR terms, shifting risk to Parpro.

Display panels and rugged enclosures

Industrial display panel and rugged enclosure supply remains relatively fragmented, moderating supplier power despite dominance of large fabs in consumer panels. Custom mechanicals and optical specs create lock-in across product lifecycles, with UL/IP certification often taking 6–12 months and costs commonly exceeding $50,000. Tooling investments and certification make switches costly; volume commitments can secure 10–25% price breaks but reduce flexibility.

Software stacks and OS licensing

Software stacks and OS licensing (Windows IoT, Linux distributions) materially affect BOM and support costs: Windows IoT LTSC offers up to 10 years of support (2024), Ubuntu LTS provides 5 years, and driver ecosystems drive recurring R&D and warranty spend. Switching OS/middleware requires retraining, recertification and customer requalification, granting moderate leverage to software vendors. Security patch cadence and LTSC terms shape lifecycle promises; negotiated enterprise licenses often cut list prices by ~20–40%.

- Windows IoT: up to 10y LTSC (2024)

- Linux: 5y LTS common (Ubuntu)

- Switch costs: retrain, recert, requalify

- Enterprise discounts: ~20–40%

Upstream PCB fabs and EMS capacity

- Geographic concentration: ~66% of PCB fabs in China (2024)

- Lead times: 6–10 weeks typical (2024)

- Market size: EMS >500B USD (2024)

- Mitigants: dual-region sourcing, DFX

Supply: CPUs/GPUs > 70%, 12–24wk waits, ~66%

Supplier power is high: CPU/GPU vendors control >70% platform direction (2024), long-lead parts drive 12–24 week waits, and PCB fabs concentrated ~66% in China. Switching costs (validation, certification, tooling) and NCNR terms raise friction; long-term contracts, multi-sourcing and buffer stock are primary mitigants.

| Metric | 2024 |

|---|---|

| CPU/GPU market influence | >70% |

| Memory lead times | 12–20 wks |

| PCB fabs in China | ~66% |

| EMS market | >500B USD |

What is included in the product

Concise Porter's Five Forces assessment tailored for Parpro, uncovering competitive intensity, buyer/supplier leverage, substitution risks, and entry barriers with strategic implications for pricing and profitability.

A compact, customizable Parpro Porter's Five Forces tool that turns complex competitive dynamics into actionable insights—visual radar, editable inputs, and slide-ready summaries relieve decision-making friction and speed strategic responses.

Customers Bargaining Power

Large OEMs and system integrators

Large OEMs and system integrators in automation, transportation and healthcare run formal RFPs and buy in large volumes, giving them high leverage and enabling benchmarking on price, delivery and specs; in 2024 top OEMs accounted for roughly 35–45% of category purchasing in several mature segments. Framework agreements commonly demand volume discounts and penalty clauses, squeezing margins. Parpro must pivot to TCO-led sell and premium service SLAs to defend margins and retain contracts.

Customization increases stickiness

Tailored designs integrate deeply into customer systems, raising switching costs as firmware, drivers and mechanical fit require requalification that can add 6–12 months and tens to hundreds of thousands USD in validation costs; this materially reduces buyer power post-integration, while upfront NRE pricing and contract terms remain the primary negotiation leverage for purchasers in 2024.

Regulatory and lifecycle requirements

Certifications EN 50155, IEC 60601 and stringent EMC rules plus 5–10+ year availability commitments in rail and medical lifecycles make buyers highly reluctant to change suppliers, since replacements require costly revalidation and downtime that can take weeks to months.

This stickiness shifts bargaining power toward Parpro on incumbent programs, though buyers still demand last-time-buy flexibility and formal EOL notices to manage inventory and risk.

Spec parity and price transparency

Many embedded PC vendors offered near-spec parity in 2024, and public datasheets plus benchmark databases such as SPEC and PassMark enabled direct side-by-side comparisons, driving buyers to shop primarily on price. Buyers increasingly threaten dual-sourcing for volume discounts, forcing vendors to justify any premium through measurable value-added services like extended support, certified integrations, or custom firmware. Transparent component sourcing and distributor price listings keep margins under pressure.

- Spec parity: public datasheets + SPEC/PassMark (2024)

- Price transparency: distributor catalogs accessible online

- Dual-sourcing threat: common buyer negotiation tactic

- Premium justification: must be tied to measurable services

Service, SLAs, and TCO pressures

Buyers push for extended warranties, on-site support, and strict SLAs, with 2024 buyer surveys showing uptime targets of 99.9% or higher commonly demanded.

They evaluate downtime risk and field maintainability—since outages can cost enterprises six-figure sums per day—shaping tougher negotiation terms.

Strong after-sales performance lowers price sensitivity, while weak support immediately increases buyer bargaining power and contract concessions.

- Extended warranties demanded

- On-site support priority

- SLAs commonly 99.9%+ uptime

- Downtime = six-figure daily risk

- After-sales reduces price pressure

RFP leverage vs incumbent lock-in: top OEMs 35–45%, validation 6–12m, SLAs 99.9%+

Buyers hold strong upfront leverage via RFPs and volume (top OEMs 35–45% share in mature segments, 2024), but incumbent stickiness from certifications and integrations (validation 6–12 months, validation costs tens–hundreds k USD) shifts power to Parpro on live programs. Price pressure rises from spec parity and transparent benchmarks; buyers demand 99.9%+ SLAs and threaten dual-sourcing.

| Metric | 2024 |

|---|---|

| Top OEM share | 35–45% |

| Validation time | 6–12 months |

| Validation cost | 10^4–10^5+ USD |

| Uptime SLAs | 99.9%+ |

Same Document Delivered

Parpro Porter's Five Forces Analysis

This preview shows the exact Parpro Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document here is fully formatted, professionally written, and ready for download and use the moment you buy. You're getting the final deliverable as displayed, with no further setup required.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Parpro's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, barriers to entry, and substitute threats to reveal strategic pressure points. It surfaces key risks and opportunities shaping margins and growth. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated CPU and chipset sources

In 2024 CPU and GPU roadmaps remain concentrated among a few vendors—Intel, AMD, NVIDIA and leading ARM SoC suppliers—who together exert >70% influence over platform directions, concentrating supplier power. Allocation cycles and priority access favor large OEMs, pressuring pricing and lead times. Parpro can reduce risk by multi-CPU support, but validation costs raise switching frictions. Long-term supply contracts and demand forecasting cut volatility.

Long-lead critical components

Long-lead critical components give suppliers leverage in tight markets: 2024 industry reports showed industrial-grade memory lead times of 12–20 weeks, power modules 16–24 weeks, and specialized connectors 10–18 weeks. Qualification and compliance constraints limit immediate substitutions and second-source design adds engineering and capex burden. Maintaining buffer inventory raises working capital needs by tying up months of cash, and suppliers often impose NCNR terms, shifting risk to Parpro.

Display panels and rugged enclosures

Industrial display panel and rugged enclosure supply remains relatively fragmented, moderating supplier power despite dominance of large fabs in consumer panels. Custom mechanicals and optical specs create lock-in across product lifecycles, with UL/IP certification often taking 6–12 months and costs commonly exceeding $50,000. Tooling investments and certification make switches costly; volume commitments can secure 10–25% price breaks but reduce flexibility.

Software stacks and OS licensing

Software stacks and OS licensing (Windows IoT, Linux distributions) materially affect BOM and support costs: Windows IoT LTSC offers up to 10 years of support (2024), Ubuntu LTS provides 5 years, and driver ecosystems drive recurring R&D and warranty spend. Switching OS/middleware requires retraining, recertification and customer requalification, granting moderate leverage to software vendors. Security patch cadence and LTSC terms shape lifecycle promises; negotiated enterprise licenses often cut list prices by ~20–40%.

- Windows IoT: up to 10y LTSC (2024)

- Linux: 5y LTS common (Ubuntu)

- Switch costs: retrain, recert, requalify

- Enterprise discounts: ~20–40%

Upstream PCB fabs and EMS capacity

- Geographic concentration: ~66% of PCB fabs in China (2024)

- Lead times: 6–10 weeks typical (2024)

- Market size: EMS >500B USD (2024)

- Mitigants: dual-region sourcing, DFX

Supply: CPUs/GPUs > 70%, 12–24wk waits, ~66%

Supplier power is high: CPU/GPU vendors control >70% platform direction (2024), long-lead parts drive 12–24 week waits, and PCB fabs concentrated ~66% in China. Switching costs (validation, certification, tooling) and NCNR terms raise friction; long-term contracts, multi-sourcing and buffer stock are primary mitigants.

| Metric | 2024 |

|---|---|

| CPU/GPU market influence | >70% |

| Memory lead times | 12–20 wks |

| PCB fabs in China | ~66% |

| EMS market | >500B USD |

What is included in the product

Concise Porter's Five Forces assessment tailored for Parpro, uncovering competitive intensity, buyer/supplier leverage, substitution risks, and entry barriers with strategic implications for pricing and profitability.

A compact, customizable Parpro Porter's Five Forces tool that turns complex competitive dynamics into actionable insights—visual radar, editable inputs, and slide-ready summaries relieve decision-making friction and speed strategic responses.

Customers Bargaining Power

Large OEMs and system integrators

Large OEMs and system integrators in automation, transportation and healthcare run formal RFPs and buy in large volumes, giving them high leverage and enabling benchmarking on price, delivery and specs; in 2024 top OEMs accounted for roughly 35–45% of category purchasing in several mature segments. Framework agreements commonly demand volume discounts and penalty clauses, squeezing margins. Parpro must pivot to TCO-led sell and premium service SLAs to defend margins and retain contracts.

Customization increases stickiness

Tailored designs integrate deeply into customer systems, raising switching costs as firmware, drivers and mechanical fit require requalification that can add 6–12 months and tens to hundreds of thousands USD in validation costs; this materially reduces buyer power post-integration, while upfront NRE pricing and contract terms remain the primary negotiation leverage for purchasers in 2024.

Regulatory and lifecycle requirements

Certifications EN 50155, IEC 60601 and stringent EMC rules plus 5–10+ year availability commitments in rail and medical lifecycles make buyers highly reluctant to change suppliers, since replacements require costly revalidation and downtime that can take weeks to months.

This stickiness shifts bargaining power toward Parpro on incumbent programs, though buyers still demand last-time-buy flexibility and formal EOL notices to manage inventory and risk.

Spec parity and price transparency

Many embedded PC vendors offered near-spec parity in 2024, and public datasheets plus benchmark databases such as SPEC and PassMark enabled direct side-by-side comparisons, driving buyers to shop primarily on price. Buyers increasingly threaten dual-sourcing for volume discounts, forcing vendors to justify any premium through measurable value-added services like extended support, certified integrations, or custom firmware. Transparent component sourcing and distributor price listings keep margins under pressure.

- Spec parity: public datasheets + SPEC/PassMark (2024)

- Price transparency: distributor catalogs accessible online

- Dual-sourcing threat: common buyer negotiation tactic

- Premium justification: must be tied to measurable services

Service, SLAs, and TCO pressures

Buyers push for extended warranties, on-site support, and strict SLAs, with 2024 buyer surveys showing uptime targets of 99.9% or higher commonly demanded.

They evaluate downtime risk and field maintainability—since outages can cost enterprises six-figure sums per day—shaping tougher negotiation terms.

Strong after-sales performance lowers price sensitivity, while weak support immediately increases buyer bargaining power and contract concessions.

- Extended warranties demanded

- On-site support priority

- SLAs commonly 99.9%+ uptime

- Downtime = six-figure daily risk

- After-sales reduces price pressure

RFP leverage vs incumbent lock-in: top OEMs 35–45%, validation 6–12m, SLAs 99.9%+

Buyers hold strong upfront leverage via RFPs and volume (top OEMs 35–45% share in mature segments, 2024), but incumbent stickiness from certifications and integrations (validation 6–12 months, validation costs tens–hundreds k USD) shifts power to Parpro on live programs. Price pressure rises from spec parity and transparent benchmarks; buyers demand 99.9%+ SLAs and threaten dual-sourcing.

| Metric | 2024 |

|---|---|

| Top OEM share | 35–45% |

| Validation time | 6–12 months |

| Validation cost | 10^4–10^5+ USD |

| Uptime SLAs | 99.9%+ |

Same Document Delivered

Parpro Porter's Five Forces Analysis

This preview shows the exact Parpro Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document here is fully formatted, professionally written, and ready for download and use the moment you buy. You're getting the final deliverable as displayed, with no further setup required.