Bank Pekao PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain strategic clarity with our PESTLE analysis of Bank Pekao—revealing how political shifts, macroeconomic trends, regulation, social dynamics and technological change will shape its trajectory. Ideal for investors and strategists, it's fully sourced and actionable. Purchase the full report to get the complete, editable breakdown instantly.

Political factors

EU policy direction

Poland’s EU membership imposes single-rule banking standards and ECB/ESMA supervisory expectations, affecting Bank Pekao’s capital, reporting and cross-border operations. Cohesion policy and RRF disbursements — about €76.6bn (cohesion 2021–27) and €23.9bn (RRF grants) to Poland — can lift corporate credit demand and fee income. EU shifts to green and digital priorities redirect lending to energy transition and IT with rising alignment costs; reporting complexity increases with each new EU initiative.

Domestic policy and elections

Changes in government priorities can shift taxation, public investment and housing programs, influencing loan growth and asset quality; policy-driven mortgage support in 2024–H1 2025 altered margins and risk pricing. A tighter budget stance pushed Polish 10Y yields toward ~5.0% (H1 2025), affecting bank securities; political continuity reduces uncertainty while transitions raise regulatory and credit-planning risks.

State influence in banking

State strategic interest shapes consolidation, resolution planning and crisis backstops for Bank Pekao, whose assets stood near PLN 300bn in 2024; expectations to lend to priority sectors steer portfolio mix (e.g., preferential corporate/housing exposures), governance scrutiny rises in stress, and perceived policy backing bolsters depositor confidence while compressing competitive dynamics.

Geopolitical risk spillovers

Regional tensions since the full-scale invasion of Ukraine on 24 February 2022 raise risk premia and FX volatility, which compresses margins for Bank Pekao, Poland's second-largest bank by assets as of 2024.

Supply-chain and energy shocks feed through to borrower cash flows, increasing stage 3 loans and operational risk; sanctions regimes have expanded compliance and screening obligations for trade and correspondent banking.

Headline-driven swings in investor sentiment across CEE periodically tighten funding costs and widen bank bond/CDS spreads, pressuring liquidity planning.

- war start date: 24 February 2022

- Bank Pekao: Poland's second-largest bank by assets (2024)

- impact channels: FX volatility, borrower cash flows, compliance load, funding-cost swings

Local government relations

Local government relations shape Bank Pekao’s deposit base and fee income, as municipal deposits and project lending create steady liquidity and fee streams; Pekao, Poland’s second-largest bank by assets, benefits from payment and custody mandates for public entities that produce stable revenues. Public-private partnerships expand infrastructure lending pipelines, while tightened local budgets in 2024 can curb capex and transaction volumes.

- Municipal deposits bolster liquidity

- Payment/custody = steady fees

- PPPs expand lending pipeline

- Budget tightening reduces capex/transactions

EU funds and RRF push bank lending green/digital; 10Y ≈5.0%

Poland’s EU rules and €76.6bn cohesion (2021–27)/€23.9bn RRF grants redirect Bank Pekao lending to green/digital projects and raise reporting costs. Government policy and 2024–H1 2025 mortgage support altered margins; Polish 10Y ≈5.0% (H1 2025) impacts securities. State backing (assets ≈PLN 300bn, 2024) supports deposits but steers priority lending and governance scrutiny.

| Indicator | Value |

|---|---|

| Cohesion 2021–27 | €76.6bn |

| RRF grants to Poland | €23.9bn |

| Polish 10Y (H1 2025) | ≈5.0% |

| Pekao assets (2024) | ≈PLN 300bn |

What is included in the product

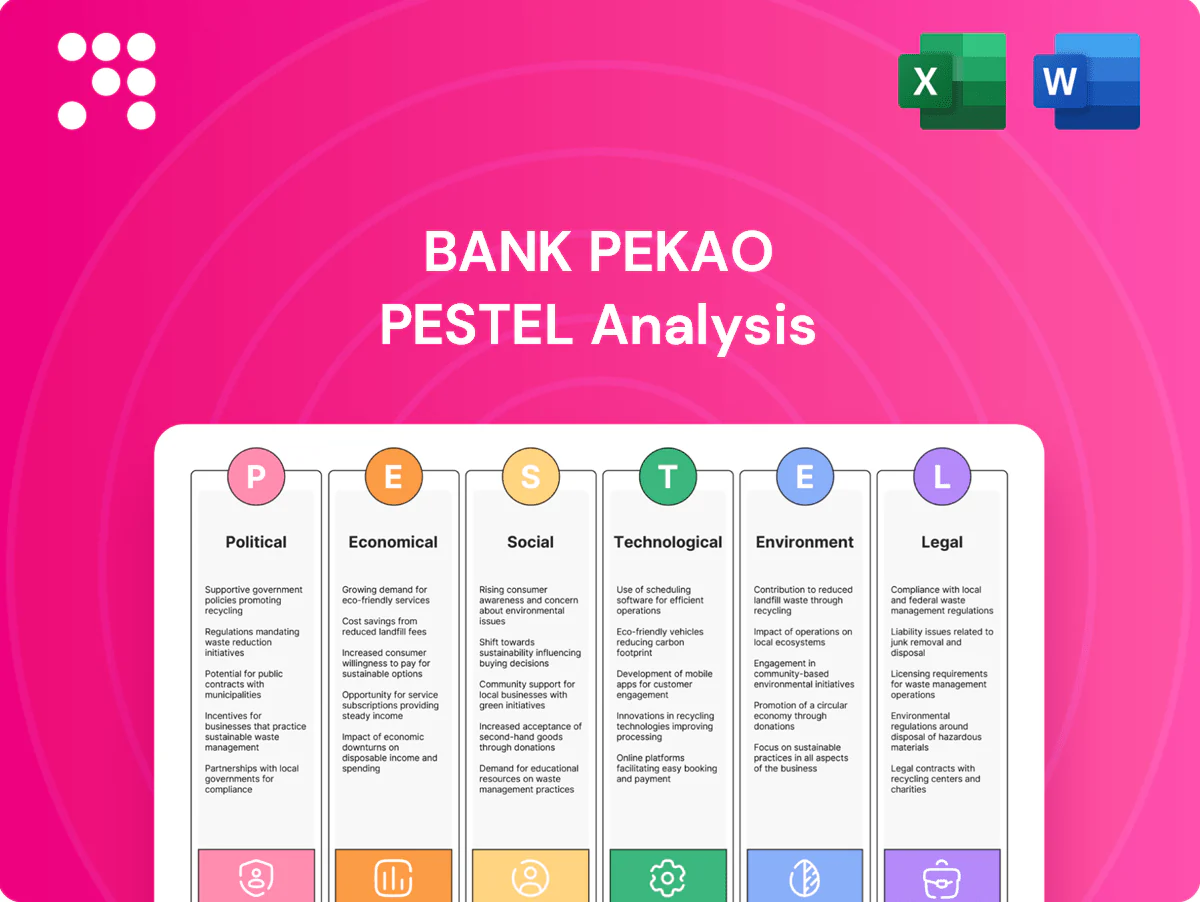

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Bank Pekao, with data‑backed trends and region-specific examples to identify risks and opportunities. Designed for executives and investors to support strategy, scenario planning and investor communications.

Visually segmented by PESTEL categories, the Bank Pekao PESTLE analysis lets teams quickly interpret external risks at a glance and drop concise insights into presentations. Easily shareable and editable, it speeds alignment across departments and supports faster, evidence-based planning.

Economic factors

Interest rate cycle

NBP policy rate movements (peaking near 6.75% in 2023 and easing to about 5.75% by mid‑2025) directly compress Bank Pekao’s net interest margins and shape credit appetite. Rapid shift from high inflation to disinflation forced loan repricing and raised deposit betas, tightening NIM. Asset repricing lags produce NIM volatility, while lower rate paths improve mortgage affordability and raise prepayment risk as effective rates fall.

Polish GDP and labor market

Poland's GDP expanded about 2.5% in 2024, supporting domestic consumption that underpins Bank Pekao's retail volumes.

Tight labor markets with unemployment near 2.8% and nominal wage growth around 8–9% bolster loan servicing and credit quality but add inflationary pressure.

Corporate investment cycles—muted in 2024—drive SME and large-cap lending demand, while any slowdown raises cost of risk and provisioning needs for the bank.

Housing market dynamics

Mortgage growth for Bank Pekao hinges on affordability, supply bottlenecks and policy support as Poland's mortgage debt stood near 22% of GDP in 2024 (NBP), while resilient prices have kept collateral values stable. Sharp rate shocks would tighten DTI headroom for borrowers and test credit losses. Prolonged new-build timelines compress disbursement profiles, and demand for energy-efficient homes is driving interest in green mortgage products.

FX and funding conditions

PLN volatility (EUR/PLN ~4.45 in July 2025) drives imported inflation, raises corporates’ hedging demand and can trigger capital flow reversals; access to wholesale markets dictates term funding costs and timing for MREL issuances. A stable deposit base anchors Pekao’s liquidity and pricing power, while CEE risk appetite (Poland 5y CDS ~70 bps, Jul 2025) widens or tightens bank spreads.

- PLN volatility → imported inflation, hedging demand

- Wholesale access → term funding cost, MREL windows

- Stable deposits → liquidity, pricing power

- CEE investor risk appetite → spreads (5y CDS ~70 bps)

EU funds absorption

Effective absorption of EU funds (Poland: cohesion ~€76.1bn 2021–27; RRF ~€23.9bn) can catalyze Bank Pekao’s credit, payments and advisory revenue by financing corporate capex and public projects; infrastructure and digital investments expand corporate lending pipelines and transaction volumes; disbursement delays defer loan growth and fee income; co‑financing needs create structured finance and syndication opportunities.

- Credit growth: higher demand for project loans

- Fees/payments: increased transactions and advisory mandates

- Risk: delayed disbursements → postponed NII and fee recognition

EU funds and RRF push bank lending green/digital; 10Y ≈5.0%

NBP policy easing to ~5.75% (mid‑2025) compresses NIM but boosts mortgage affordability and prepayment risk. Poland GDP ~2.5% (2024) supports retail volumes; unemployment ~2.8% and wage growth 8–9% help credit quality yet sustain inflationary pressure. PLN ~4.45/EUR (Jul 2025) and 5y CDS ~70bps affect funding costs and spreads.

| Metric | Value |

|---|---|

| NBP rate | ~5.75% (mid‑2025) |

| GDP growth | ~2.5% (2024) |

| Unemployment | ~2.8% |

| EUR/PLN | ~4.45 (Jul 2025) |

Same Document Delivered

Bank Pekao PESTLE Analysis

The Bank Pekao PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the real file you’re buying, delivered exactly as displayed with no placeholders or teasers. After payment you’ll instantly download the same finished document shown in the preview.

Your Shortcut to Market Insight Starts Here

Gain strategic clarity with our PESTLE analysis of Bank Pekao—revealing how political shifts, macroeconomic trends, regulation, social dynamics and technological change will shape its trajectory. Ideal for investors and strategists, it's fully sourced and actionable. Purchase the full report to get the complete, editable breakdown instantly.

Political factors

EU policy direction

Poland’s EU membership imposes single-rule banking standards and ECB/ESMA supervisory expectations, affecting Bank Pekao’s capital, reporting and cross-border operations. Cohesion policy and RRF disbursements — about €76.6bn (cohesion 2021–27) and €23.9bn (RRF grants) to Poland — can lift corporate credit demand and fee income. EU shifts to green and digital priorities redirect lending to energy transition and IT with rising alignment costs; reporting complexity increases with each new EU initiative.

Domestic policy and elections

Changes in government priorities can shift taxation, public investment and housing programs, influencing loan growth and asset quality; policy-driven mortgage support in 2024–H1 2025 altered margins and risk pricing. A tighter budget stance pushed Polish 10Y yields toward ~5.0% (H1 2025), affecting bank securities; political continuity reduces uncertainty while transitions raise regulatory and credit-planning risks.

State influence in banking

State strategic interest shapes consolidation, resolution planning and crisis backstops for Bank Pekao, whose assets stood near PLN 300bn in 2024; expectations to lend to priority sectors steer portfolio mix (e.g., preferential corporate/housing exposures), governance scrutiny rises in stress, and perceived policy backing bolsters depositor confidence while compressing competitive dynamics.

Geopolitical risk spillovers

Regional tensions since the full-scale invasion of Ukraine on 24 February 2022 raise risk premia and FX volatility, which compresses margins for Bank Pekao, Poland's second-largest bank by assets as of 2024.

Supply-chain and energy shocks feed through to borrower cash flows, increasing stage 3 loans and operational risk; sanctions regimes have expanded compliance and screening obligations for trade and correspondent banking.

Headline-driven swings in investor sentiment across CEE periodically tighten funding costs and widen bank bond/CDS spreads, pressuring liquidity planning.

- war start date: 24 February 2022

- Bank Pekao: Poland's second-largest bank by assets (2024)

- impact channels: FX volatility, borrower cash flows, compliance load, funding-cost swings

Local government relations

Local government relations shape Bank Pekao’s deposit base and fee income, as municipal deposits and project lending create steady liquidity and fee streams; Pekao, Poland’s second-largest bank by assets, benefits from payment and custody mandates for public entities that produce stable revenues. Public-private partnerships expand infrastructure lending pipelines, while tightened local budgets in 2024 can curb capex and transaction volumes.

- Municipal deposits bolster liquidity

- Payment/custody = steady fees

- PPPs expand lending pipeline

- Budget tightening reduces capex/transactions

EU funds and RRF push bank lending green/digital; 10Y ≈5.0%

Poland’s EU rules and €76.6bn cohesion (2021–27)/€23.9bn RRF grants redirect Bank Pekao lending to green/digital projects and raise reporting costs. Government policy and 2024–H1 2025 mortgage support altered margins; Polish 10Y ≈5.0% (H1 2025) impacts securities. State backing (assets ≈PLN 300bn, 2024) supports deposits but steers priority lending and governance scrutiny.

| Indicator | Value |

|---|---|

| Cohesion 2021–27 | €76.6bn |

| RRF grants to Poland | €23.9bn |

| Polish 10Y (H1 2025) | ≈5.0% |

| Pekao assets (2024) | ≈PLN 300bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Bank Pekao, with data‑backed trends and region-specific examples to identify risks and opportunities. Designed for executives and investors to support strategy, scenario planning and investor communications.

Visually segmented by PESTEL categories, the Bank Pekao PESTLE analysis lets teams quickly interpret external risks at a glance and drop concise insights into presentations. Easily shareable and editable, it speeds alignment across departments and supports faster, evidence-based planning.

Economic factors

Interest rate cycle

NBP policy rate movements (peaking near 6.75% in 2023 and easing to about 5.75% by mid‑2025) directly compress Bank Pekao’s net interest margins and shape credit appetite. Rapid shift from high inflation to disinflation forced loan repricing and raised deposit betas, tightening NIM. Asset repricing lags produce NIM volatility, while lower rate paths improve mortgage affordability and raise prepayment risk as effective rates fall.

Polish GDP and labor market

Poland's GDP expanded about 2.5% in 2024, supporting domestic consumption that underpins Bank Pekao's retail volumes.

Tight labor markets with unemployment near 2.8% and nominal wage growth around 8–9% bolster loan servicing and credit quality but add inflationary pressure.

Corporate investment cycles—muted in 2024—drive SME and large-cap lending demand, while any slowdown raises cost of risk and provisioning needs for the bank.

Housing market dynamics

Mortgage growth for Bank Pekao hinges on affordability, supply bottlenecks and policy support as Poland's mortgage debt stood near 22% of GDP in 2024 (NBP), while resilient prices have kept collateral values stable. Sharp rate shocks would tighten DTI headroom for borrowers and test credit losses. Prolonged new-build timelines compress disbursement profiles, and demand for energy-efficient homes is driving interest in green mortgage products.

FX and funding conditions

PLN volatility (EUR/PLN ~4.45 in July 2025) drives imported inflation, raises corporates’ hedging demand and can trigger capital flow reversals; access to wholesale markets dictates term funding costs and timing for MREL issuances. A stable deposit base anchors Pekao’s liquidity and pricing power, while CEE risk appetite (Poland 5y CDS ~70 bps, Jul 2025) widens or tightens bank spreads.

- PLN volatility → imported inflation, hedging demand

- Wholesale access → term funding cost, MREL windows

- Stable deposits → liquidity, pricing power

- CEE investor risk appetite → spreads (5y CDS ~70 bps)

EU funds absorption

Effective absorption of EU funds (Poland: cohesion ~€76.1bn 2021–27; RRF ~€23.9bn) can catalyze Bank Pekao’s credit, payments and advisory revenue by financing corporate capex and public projects; infrastructure and digital investments expand corporate lending pipelines and transaction volumes; disbursement delays defer loan growth and fee income; co‑financing needs create structured finance and syndication opportunities.

- Credit growth: higher demand for project loans

- Fees/payments: increased transactions and advisory mandates

- Risk: delayed disbursements → postponed NII and fee recognition

EU funds and RRF push bank lending green/digital; 10Y ≈5.0%

NBP policy easing to ~5.75% (mid‑2025) compresses NIM but boosts mortgage affordability and prepayment risk. Poland GDP ~2.5% (2024) supports retail volumes; unemployment ~2.8% and wage growth 8–9% help credit quality yet sustain inflationary pressure. PLN ~4.45/EUR (Jul 2025) and 5y CDS ~70bps affect funding costs and spreads.

| Metric | Value |

|---|---|

| NBP rate | ~5.75% (mid‑2025) |

| GDP growth | ~2.5% (2024) |

| Unemployment | ~2.8% |

| EUR/PLN | ~4.45 (Jul 2025) |

Same Document Delivered

Bank Pekao PESTLE Analysis

The Bank Pekao PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the real file you’re buying, delivered exactly as displayed with no placeholders or teasers. After payment you’ll instantly download the same finished document shown in the preview.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Gain strategic clarity with our PESTLE analysis of Bank Pekao—revealing how political shifts, macroeconomic trends, regulation, social dynamics and technological change will shape its trajectory. Ideal for investors and strategists, it's fully sourced and actionable. Purchase the full report to get the complete, editable breakdown instantly.

Political factors

EU policy direction

Poland’s EU membership imposes single-rule banking standards and ECB/ESMA supervisory expectations, affecting Bank Pekao’s capital, reporting and cross-border operations. Cohesion policy and RRF disbursements — about €76.6bn (cohesion 2021–27) and €23.9bn (RRF grants) to Poland — can lift corporate credit demand and fee income. EU shifts to green and digital priorities redirect lending to energy transition and IT with rising alignment costs; reporting complexity increases with each new EU initiative.

Domestic policy and elections

Changes in government priorities can shift taxation, public investment and housing programs, influencing loan growth and asset quality; policy-driven mortgage support in 2024–H1 2025 altered margins and risk pricing. A tighter budget stance pushed Polish 10Y yields toward ~5.0% (H1 2025), affecting bank securities; political continuity reduces uncertainty while transitions raise regulatory and credit-planning risks.

State influence in banking

State strategic interest shapes consolidation, resolution planning and crisis backstops for Bank Pekao, whose assets stood near PLN 300bn in 2024; expectations to lend to priority sectors steer portfolio mix (e.g., preferential corporate/housing exposures), governance scrutiny rises in stress, and perceived policy backing bolsters depositor confidence while compressing competitive dynamics.

Geopolitical risk spillovers

Regional tensions since the full-scale invasion of Ukraine on 24 February 2022 raise risk premia and FX volatility, which compresses margins for Bank Pekao, Poland's second-largest bank by assets as of 2024.

Supply-chain and energy shocks feed through to borrower cash flows, increasing stage 3 loans and operational risk; sanctions regimes have expanded compliance and screening obligations for trade and correspondent banking.

Headline-driven swings in investor sentiment across CEE periodically tighten funding costs and widen bank bond/CDS spreads, pressuring liquidity planning.

- war start date: 24 February 2022

- Bank Pekao: Poland's second-largest bank by assets (2024)

- impact channels: FX volatility, borrower cash flows, compliance load, funding-cost swings

Local government relations

Local government relations shape Bank Pekao’s deposit base and fee income, as municipal deposits and project lending create steady liquidity and fee streams; Pekao, Poland’s second-largest bank by assets, benefits from payment and custody mandates for public entities that produce stable revenues. Public-private partnerships expand infrastructure lending pipelines, while tightened local budgets in 2024 can curb capex and transaction volumes.

- Municipal deposits bolster liquidity

- Payment/custody = steady fees

- PPPs expand lending pipeline

- Budget tightening reduces capex/transactions

EU funds and RRF push bank lending green/digital; 10Y ≈5.0%

Poland’s EU rules and €76.6bn cohesion (2021–27)/€23.9bn RRF grants redirect Bank Pekao lending to green/digital projects and raise reporting costs. Government policy and 2024–H1 2025 mortgage support altered margins; Polish 10Y ≈5.0% (H1 2025) impacts securities. State backing (assets ≈PLN 300bn, 2024) supports deposits but steers priority lending and governance scrutiny.

| Indicator | Value |

|---|---|

| Cohesion 2021–27 | €76.6bn |

| RRF grants to Poland | €23.9bn |

| Polish 10Y (H1 2025) | ≈5.0% |

| Pekao assets (2024) | ≈PLN 300bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Bank Pekao, with data‑backed trends and region-specific examples to identify risks and opportunities. Designed for executives and investors to support strategy, scenario planning and investor communications.

Visually segmented by PESTEL categories, the Bank Pekao PESTLE analysis lets teams quickly interpret external risks at a glance and drop concise insights into presentations. Easily shareable and editable, it speeds alignment across departments and supports faster, evidence-based planning.

Economic factors

Interest rate cycle

NBP policy rate movements (peaking near 6.75% in 2023 and easing to about 5.75% by mid‑2025) directly compress Bank Pekao’s net interest margins and shape credit appetite. Rapid shift from high inflation to disinflation forced loan repricing and raised deposit betas, tightening NIM. Asset repricing lags produce NIM volatility, while lower rate paths improve mortgage affordability and raise prepayment risk as effective rates fall.

Polish GDP and labor market

Poland's GDP expanded about 2.5% in 2024, supporting domestic consumption that underpins Bank Pekao's retail volumes.

Tight labor markets with unemployment near 2.8% and nominal wage growth around 8–9% bolster loan servicing and credit quality but add inflationary pressure.

Corporate investment cycles—muted in 2024—drive SME and large-cap lending demand, while any slowdown raises cost of risk and provisioning needs for the bank.

Housing market dynamics

Mortgage growth for Bank Pekao hinges on affordability, supply bottlenecks and policy support as Poland's mortgage debt stood near 22% of GDP in 2024 (NBP), while resilient prices have kept collateral values stable. Sharp rate shocks would tighten DTI headroom for borrowers and test credit losses. Prolonged new-build timelines compress disbursement profiles, and demand for energy-efficient homes is driving interest in green mortgage products.

FX and funding conditions

PLN volatility (EUR/PLN ~4.45 in July 2025) drives imported inflation, raises corporates’ hedging demand and can trigger capital flow reversals; access to wholesale markets dictates term funding costs and timing for MREL issuances. A stable deposit base anchors Pekao’s liquidity and pricing power, while CEE risk appetite (Poland 5y CDS ~70 bps, Jul 2025) widens or tightens bank spreads.

- PLN volatility → imported inflation, hedging demand

- Wholesale access → term funding cost, MREL windows

- Stable deposits → liquidity, pricing power

- CEE investor risk appetite → spreads (5y CDS ~70 bps)

EU funds absorption

Effective absorption of EU funds (Poland: cohesion ~€76.1bn 2021–27; RRF ~€23.9bn) can catalyze Bank Pekao’s credit, payments and advisory revenue by financing corporate capex and public projects; infrastructure and digital investments expand corporate lending pipelines and transaction volumes; disbursement delays defer loan growth and fee income; co‑financing needs create structured finance and syndication opportunities.

- Credit growth: higher demand for project loans

- Fees/payments: increased transactions and advisory mandates

- Risk: delayed disbursements → postponed NII and fee recognition

EU funds and RRF push bank lending green/digital; 10Y ≈5.0%

NBP policy easing to ~5.75% (mid‑2025) compresses NIM but boosts mortgage affordability and prepayment risk. Poland GDP ~2.5% (2024) supports retail volumes; unemployment ~2.8% and wage growth 8–9% help credit quality yet sustain inflationary pressure. PLN ~4.45/EUR (Jul 2025) and 5y CDS ~70bps affect funding costs and spreads.

| Metric | Value |

|---|---|

| NBP rate | ~5.75% (mid‑2025) |

| GDP growth | ~2.5% (2024) |

| Unemployment | ~2.8% |

| EUR/PLN | ~4.45 (Jul 2025) |

Same Document Delivered

Bank Pekao PESTLE Analysis

The Bank Pekao PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the real file you’re buying, delivered exactly as displayed with no placeholders or teasers. After payment you’ll instantly download the same finished document shown in the preview.