PENN Entertainment Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

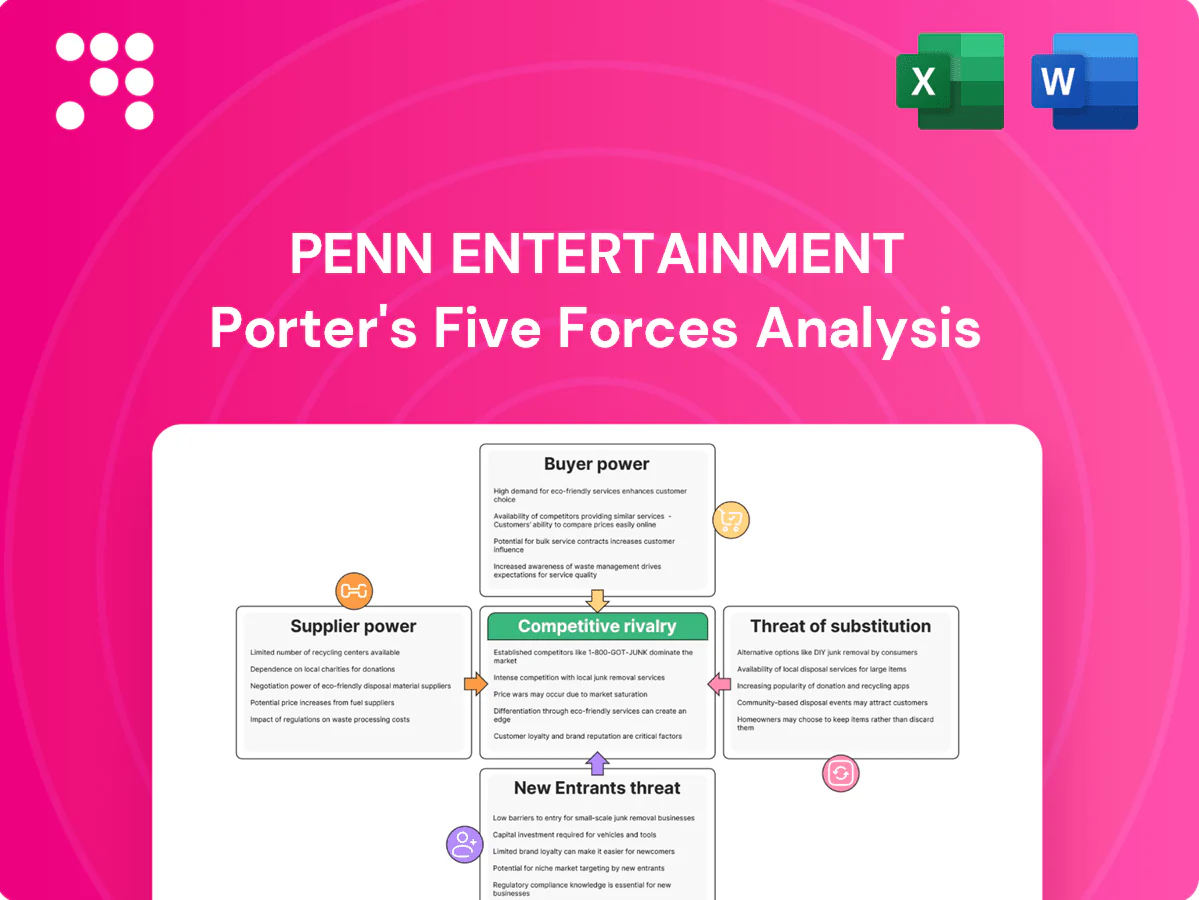

Penn Entertainment faces intense rivalry from regional casinos and national iGaming rivals, rising buyer leverage via promotions, moderate supplier influence for gaming tech/content, and regulatory/legal risks that shape growth prospects. This snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated casino equipment vendors

Land-based operations depend on a concentrated vendor base—IGT, Aristocrat and Light & Wonder account for roughly 60–75% of new slot shipments—giving them pricing power and control over product roadmaps. Long lead times (typically 6–12 months), regulatory certification and integration complexity raise switching costs for operators. PENN leverages scale purchasing and a multi-vendor mix across ~40 properties to mitigate pricing risk but remains exposed to vendor roadmap and supply constraints.

Brand and media licensor dependence

ESPN BET licensing concentrates power with a marquee media partner after Penn launched the ESPN BET joint venture in 2023, tying brand guidelines, co‑marketing cadence and contractual terms that can limit pricing flexibility and margins. Any change in ESPN/Disney priorities or renewal pricing would pressure economics, while Penn offsets via its Hollywood brand and proprietary tech; ESPN remains a primary demand funnel.

Data, trading, and geolocation providers

Sportsbook integrity and pricing rely on feeds from Sportradar/Genius and geolocation from GeoComply, a concentrated supplier base that raises supplier power; typical sportsbook hold rates run about 5–8%, so feed outages or price increases can materially hit margins. Outages have caused measurable hold volatility across operators, and regulatory fines from geolocation failures can be substantial. Building in-house capabilities and dual-sourcing reduces this mission-critical single-supplier risk.

Payments and fintech gateways

Real estate landlords and labor

- Leases concentrate property risk and fixed costs

- Union contracts boost labor bargaining power

- 2024 wage inflation (~5% YoY) pressures margins

- Long-term deals temper volatility but restrict flexibility

Concentrated suppliers and payment fees squeeze operator margins amid long slot lead times

Supplier power is high: 60–75% of new slots from IGT/Aristocrat/Light & Wonder, long lead times (6–12 months) and certification raise switching costs. Media and data partners (ESPN, Sportradar, GeoComply) concentrate pricing and outage risk, while PSPs drive payment costs (~1.5–3% card fees, $20–50 chargebacks). PENN offsets via scale, multi-vendor sourcing and in‑house tech.

| Metric | 2024 |

|---|---|

| Slot vendor share | 60–75% |

| Lead times | 6–12 months |

| Card fees | 1.5–3% |

| Chargeback | $20–50 |

What is included in the product

Tailored Porter’s Five Forces analysis of PENN Entertainment highlighting competitive rivalry, buyer and supplier leverage, threat of new entrants and substitutes, and regulatory/disruptive risks; evaluates how these forces shape pricing power, margins, and strategic defenses for PENN in U.S. gaming and online wagering markets.

A clear, one-sheet Porter’s Five Forces for PENN Entertainment—condensing competitive pressures into an at-a-glance scorecard for faster strategic decisions. Swap in updated data or duplicate tabs for pre/post-regulation or new-entrant scenarios to keep analysis current and boardroom-ready.

Customers Bargaining Power

Low switching costs in digital

Low switching costs let online bettors hop between apps for odds, promos and UX, intensifying comparison shopping via app-store visibility and bonus offers and elevating buyer power that compresses sportsbook gross margins. PENN leans on its ESPN Bet JV (announced 2023, active in 2024) plus deeper product breadth and loyalty programs to protect share and pricing power.

High-value VIP and omnichannel guests

A small cohort of VIPs continues to drive a disproportionate share of PENN’s GGR, with 2024 company filings noting high-value players represent a material portion of gaming revenue. Host services, generous comps and bespoke credit limits give these buyers significant leverage over pricing and service. Omnichannel integration ties retail play to digital wallets, partially reducing churn, while targeted CRM programs are critical to preserving per-customer economics.

Regional retail guests are fragmented

Most casino patrons are numerous and locally anchored, lowering individual bargaining power; PENN operated 43 regional properties in 2024, concentrating foot traffic locally. Travel time and habitual visits reduce immediate switching, while targeted promotions and entertainment lineups sway visitation frequency. Consistent service quality and regular events help stabilize demand.

Price and promo sensitivity

Free bets, cash back, and tier multipliers drive perceived value and force customers to compare aggregate offers across odds, hold, and rewards; over-promotion erodes EBITDA if not yield-managed. Buyers increasingly shop total value, pressuring margins. PENN must enforce disciplined promo ROI and adopt dynamic segmentation to protect win rates.

Information-rich comparison environment

Information-rich comparison tools—odds screens, tip services and Reddit communities—let bettors hunt edges and compare RTP, hold and lines, raising customer bargaining power; 93% of consumers consult reviews (2024) and negative experiences spread rapidly across social channels. Robust CX and responsible-gaming tools create trust moats that blunt churn and reputational damage.

- Odds transparency

- RTP/hold visibility

- Social review risk

- CX & responsible-gaming

Low switching costs lift buyer power; VIPs and promo wars force tighter promo ROI

Low switching costs raise buyer power across digital channels; PENN counters with ESPN Bet JV (active 2024), loyalty programs and omnichannel ties. Company filings (2024) flag VIPs as a material share of GGR, giving them outsized leverage. Promo arms-races and review-driven churn force strict promo ROI and segmentation to protect hold.

| Metric | Value (2024) |

|---|---|

| Regional properties | 43 |

| ESPN Bet JV | Active |

| VIPs | Material share of GGR (filings) |

| Consumers consulting reviews | 93% |

What You See Is What You Get

PENN Entertainment Porter's Five Forces Analysis

This preview shows the exact PENN Entertainment Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples. It is the full, professionally formatted report ready for download and use. Upon payment you’ll get instant access to this identical file.

Go Beyond the Preview—Access the Full Strategic Report

Penn Entertainment faces intense rivalry from regional casinos and national iGaming rivals, rising buyer leverage via promotions, moderate supplier influence for gaming tech/content, and regulatory/legal risks that shape growth prospects. This snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated casino equipment vendors

Land-based operations depend on a concentrated vendor base—IGT, Aristocrat and Light & Wonder account for roughly 60–75% of new slot shipments—giving them pricing power and control over product roadmaps. Long lead times (typically 6–12 months), regulatory certification and integration complexity raise switching costs for operators. PENN leverages scale purchasing and a multi-vendor mix across ~40 properties to mitigate pricing risk but remains exposed to vendor roadmap and supply constraints.

Brand and media licensor dependence

ESPN BET licensing concentrates power with a marquee media partner after Penn launched the ESPN BET joint venture in 2023, tying brand guidelines, co‑marketing cadence and contractual terms that can limit pricing flexibility and margins. Any change in ESPN/Disney priorities or renewal pricing would pressure economics, while Penn offsets via its Hollywood brand and proprietary tech; ESPN remains a primary demand funnel.

Data, trading, and geolocation providers

Sportsbook integrity and pricing rely on feeds from Sportradar/Genius and geolocation from GeoComply, a concentrated supplier base that raises supplier power; typical sportsbook hold rates run about 5–8%, so feed outages or price increases can materially hit margins. Outages have caused measurable hold volatility across operators, and regulatory fines from geolocation failures can be substantial. Building in-house capabilities and dual-sourcing reduces this mission-critical single-supplier risk.

Payments and fintech gateways

Real estate landlords and labor

- Leases concentrate property risk and fixed costs

- Union contracts boost labor bargaining power

- 2024 wage inflation (~5% YoY) pressures margins

- Long-term deals temper volatility but restrict flexibility

Concentrated suppliers and payment fees squeeze operator margins amid long slot lead times

Supplier power is high: 60–75% of new slots from IGT/Aristocrat/Light & Wonder, long lead times (6–12 months) and certification raise switching costs. Media and data partners (ESPN, Sportradar, GeoComply) concentrate pricing and outage risk, while PSPs drive payment costs (~1.5–3% card fees, $20–50 chargebacks). PENN offsets via scale, multi-vendor sourcing and in‑house tech.

| Metric | 2024 |

|---|---|

| Slot vendor share | 60–75% |

| Lead times | 6–12 months |

| Card fees | 1.5–3% |

| Chargeback | $20–50 |

What is included in the product

Tailored Porter’s Five Forces analysis of PENN Entertainment highlighting competitive rivalry, buyer and supplier leverage, threat of new entrants and substitutes, and regulatory/disruptive risks; evaluates how these forces shape pricing power, margins, and strategic defenses for PENN in U.S. gaming and online wagering markets.

A clear, one-sheet Porter’s Five Forces for PENN Entertainment—condensing competitive pressures into an at-a-glance scorecard for faster strategic decisions. Swap in updated data or duplicate tabs for pre/post-regulation or new-entrant scenarios to keep analysis current and boardroom-ready.

Customers Bargaining Power

Low switching costs in digital

Low switching costs let online bettors hop between apps for odds, promos and UX, intensifying comparison shopping via app-store visibility and bonus offers and elevating buyer power that compresses sportsbook gross margins. PENN leans on its ESPN Bet JV (announced 2023, active in 2024) plus deeper product breadth and loyalty programs to protect share and pricing power.

High-value VIP and omnichannel guests

A small cohort of VIPs continues to drive a disproportionate share of PENN’s GGR, with 2024 company filings noting high-value players represent a material portion of gaming revenue. Host services, generous comps and bespoke credit limits give these buyers significant leverage over pricing and service. Omnichannel integration ties retail play to digital wallets, partially reducing churn, while targeted CRM programs are critical to preserving per-customer economics.

Regional retail guests are fragmented

Most casino patrons are numerous and locally anchored, lowering individual bargaining power; PENN operated 43 regional properties in 2024, concentrating foot traffic locally. Travel time and habitual visits reduce immediate switching, while targeted promotions and entertainment lineups sway visitation frequency. Consistent service quality and regular events help stabilize demand.

Price and promo sensitivity

Free bets, cash back, and tier multipliers drive perceived value and force customers to compare aggregate offers across odds, hold, and rewards; over-promotion erodes EBITDA if not yield-managed. Buyers increasingly shop total value, pressuring margins. PENN must enforce disciplined promo ROI and adopt dynamic segmentation to protect win rates.

Information-rich comparison environment

Information-rich comparison tools—odds screens, tip services and Reddit communities—let bettors hunt edges and compare RTP, hold and lines, raising customer bargaining power; 93% of consumers consult reviews (2024) and negative experiences spread rapidly across social channels. Robust CX and responsible-gaming tools create trust moats that blunt churn and reputational damage.

- Odds transparency

- RTP/hold visibility

- Social review risk

- CX & responsible-gaming

Low switching costs lift buyer power; VIPs and promo wars force tighter promo ROI

Low switching costs raise buyer power across digital channels; PENN counters with ESPN Bet JV (active 2024), loyalty programs and omnichannel ties. Company filings (2024) flag VIPs as a material share of GGR, giving them outsized leverage. Promo arms-races and review-driven churn force strict promo ROI and segmentation to protect hold.

| Metric | Value (2024) |

|---|---|

| Regional properties | 43 |

| ESPN Bet JV | Active |

| VIPs | Material share of GGR (filings) |

| Consumers consulting reviews | 93% |

What You See Is What You Get

PENN Entertainment Porter's Five Forces Analysis

This preview shows the exact PENN Entertainment Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples. It is the full, professionally formatted report ready for download and use. Upon payment you’ll get instant access to this identical file.

Description

Go Beyond the Preview—Access the Full Strategic Report

Penn Entertainment faces intense rivalry from regional casinos and national iGaming rivals, rising buyer leverage via promotions, moderate supplier influence for gaming tech/content, and regulatory/legal risks that shape growth prospects. This snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated casino equipment vendors

Land-based operations depend on a concentrated vendor base—IGT, Aristocrat and Light & Wonder account for roughly 60–75% of new slot shipments—giving them pricing power and control over product roadmaps. Long lead times (typically 6–12 months), regulatory certification and integration complexity raise switching costs for operators. PENN leverages scale purchasing and a multi-vendor mix across ~40 properties to mitigate pricing risk but remains exposed to vendor roadmap and supply constraints.

Brand and media licensor dependence

ESPN BET licensing concentrates power with a marquee media partner after Penn launched the ESPN BET joint venture in 2023, tying brand guidelines, co‑marketing cadence and contractual terms that can limit pricing flexibility and margins. Any change in ESPN/Disney priorities or renewal pricing would pressure economics, while Penn offsets via its Hollywood brand and proprietary tech; ESPN remains a primary demand funnel.

Data, trading, and geolocation providers

Sportsbook integrity and pricing rely on feeds from Sportradar/Genius and geolocation from GeoComply, a concentrated supplier base that raises supplier power; typical sportsbook hold rates run about 5–8%, so feed outages or price increases can materially hit margins. Outages have caused measurable hold volatility across operators, and regulatory fines from geolocation failures can be substantial. Building in-house capabilities and dual-sourcing reduces this mission-critical single-supplier risk.

Payments and fintech gateways

Real estate landlords and labor

- Leases concentrate property risk and fixed costs

- Union contracts boost labor bargaining power

- 2024 wage inflation (~5% YoY) pressures margins

- Long-term deals temper volatility but restrict flexibility

Concentrated suppliers and payment fees squeeze operator margins amid long slot lead times

Supplier power is high: 60–75% of new slots from IGT/Aristocrat/Light & Wonder, long lead times (6–12 months) and certification raise switching costs. Media and data partners (ESPN, Sportradar, GeoComply) concentrate pricing and outage risk, while PSPs drive payment costs (~1.5–3% card fees, $20–50 chargebacks). PENN offsets via scale, multi-vendor sourcing and in‑house tech.

| Metric | 2024 |

|---|---|

| Slot vendor share | 60–75% |

| Lead times | 6–12 months |

| Card fees | 1.5–3% |

| Chargeback | $20–50 |

What is included in the product

Tailored Porter’s Five Forces analysis of PENN Entertainment highlighting competitive rivalry, buyer and supplier leverage, threat of new entrants and substitutes, and regulatory/disruptive risks; evaluates how these forces shape pricing power, margins, and strategic defenses for PENN in U.S. gaming and online wagering markets.

A clear, one-sheet Porter’s Five Forces for PENN Entertainment—condensing competitive pressures into an at-a-glance scorecard for faster strategic decisions. Swap in updated data or duplicate tabs for pre/post-regulation or new-entrant scenarios to keep analysis current and boardroom-ready.

Customers Bargaining Power

Low switching costs in digital

Low switching costs let online bettors hop between apps for odds, promos and UX, intensifying comparison shopping via app-store visibility and bonus offers and elevating buyer power that compresses sportsbook gross margins. PENN leans on its ESPN Bet JV (announced 2023, active in 2024) plus deeper product breadth and loyalty programs to protect share and pricing power.

High-value VIP and omnichannel guests

A small cohort of VIPs continues to drive a disproportionate share of PENN’s GGR, with 2024 company filings noting high-value players represent a material portion of gaming revenue. Host services, generous comps and bespoke credit limits give these buyers significant leverage over pricing and service. Omnichannel integration ties retail play to digital wallets, partially reducing churn, while targeted CRM programs are critical to preserving per-customer economics.

Regional retail guests are fragmented

Most casino patrons are numerous and locally anchored, lowering individual bargaining power; PENN operated 43 regional properties in 2024, concentrating foot traffic locally. Travel time and habitual visits reduce immediate switching, while targeted promotions and entertainment lineups sway visitation frequency. Consistent service quality and regular events help stabilize demand.

Price and promo sensitivity

Free bets, cash back, and tier multipliers drive perceived value and force customers to compare aggregate offers across odds, hold, and rewards; over-promotion erodes EBITDA if not yield-managed. Buyers increasingly shop total value, pressuring margins. PENN must enforce disciplined promo ROI and adopt dynamic segmentation to protect win rates.

Information-rich comparison environment

Information-rich comparison tools—odds screens, tip services and Reddit communities—let bettors hunt edges and compare RTP, hold and lines, raising customer bargaining power; 93% of consumers consult reviews (2024) and negative experiences spread rapidly across social channels. Robust CX and responsible-gaming tools create trust moats that blunt churn and reputational damage.

- Odds transparency

- RTP/hold visibility

- Social review risk

- CX & responsible-gaming

Low switching costs lift buyer power; VIPs and promo wars force tighter promo ROI

Low switching costs raise buyer power across digital channels; PENN counters with ESPN Bet JV (active 2024), loyalty programs and omnichannel ties. Company filings (2024) flag VIPs as a material share of GGR, giving them outsized leverage. Promo arms-races and review-driven churn force strict promo ROI and segmentation to protect hold.

| Metric | Value (2024) |

|---|---|

| Regional properties | 43 |

| ESPN Bet JV | Active |

| VIPs | Material share of GGR (filings) |

| Consumers consulting reviews | 93% |

What You See Is What You Get

PENN Entertainment Porter's Five Forces Analysis

This preview shows the exact PENN Entertainment Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples. It is the full, professionally formatted report ready for download and use. Upon payment you’ll get instant access to this identical file.