Perdoceo Education Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

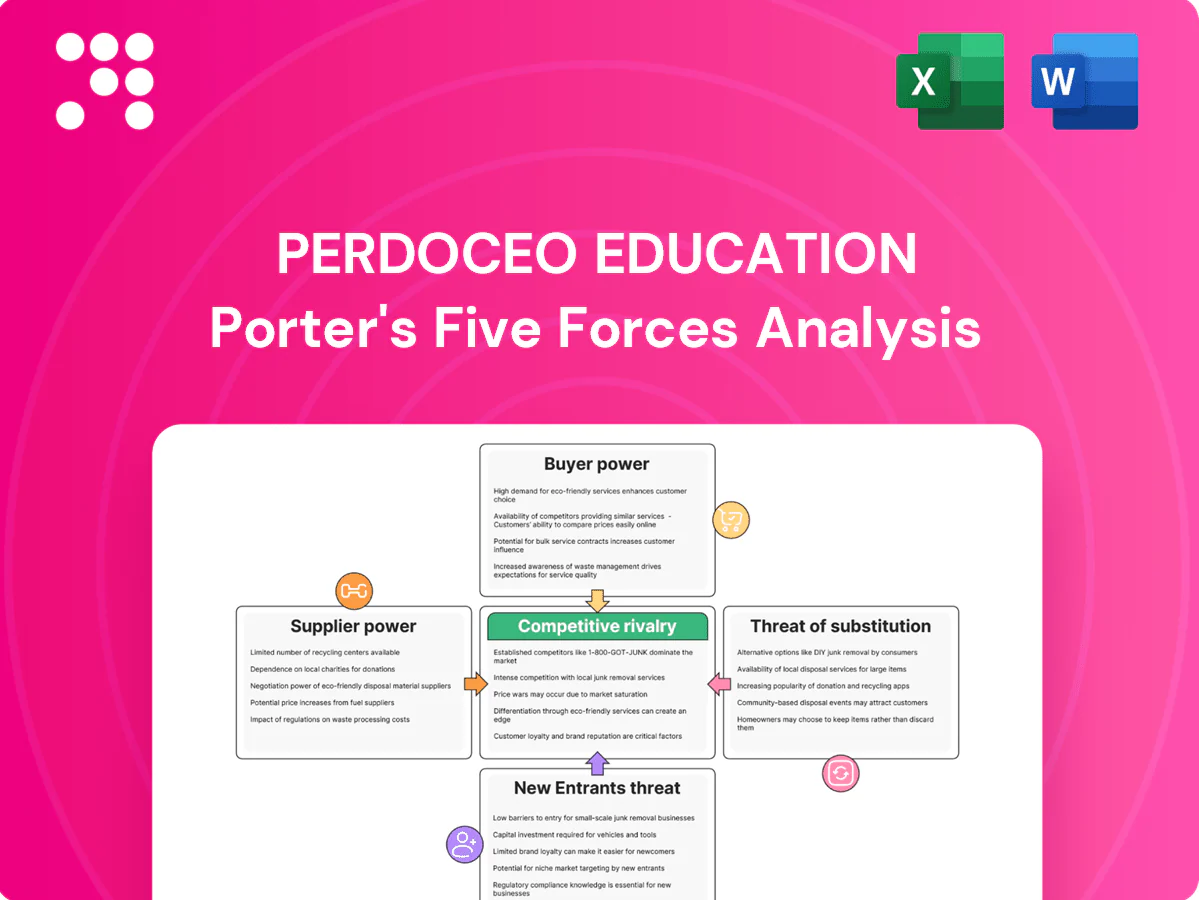

Perdoceo Education faces moderate competitive intensity amid a concentrated for‑profit education sector, high regulatory and accreditation pressure, notable buyer sensitivity on price and outcomes, and rising substitute threats from online platforms and nontraditional providers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Perdoceo Education’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated ed-tech platforms

Perdoceo depends on concentrated LMS, cloud and proctoring vendors where the top three cloud providers held ~66% market share in 2024 and the leading LMS vendors account for roughly 60% of higher‑ed deployments, making switching costly. Vendor consolidation can push fees or tougher terms; multi‑vendor strategies mitigate risk but integration overhead preserves supplier leverage. Long‑term contracts lock pricing yet constrain flexibility.

Specialized faculty and adjunct talent

Qualified instructors in niche healthcare and tech areas are scarce, giving faculty meaningful bargaining power; adjuncts still comprise about 70% of US higher-education teaching staff (2024). Wage inflation and expanded remote options have elevated compensation demands, with average hourly earnings rising ~4% in 2023–24. Standardized online course shells reduce individual dependency, yet program outcomes remain faculty‑dependent. Strict credentialing for clinical and tech roles further narrows supply.

Content and licensing dependencies

Third-party courseware, simulations and vendor certifications are often must-have inputs for Perdoceo programs, and the global e-learning market exceeded 300 billion in 2023 with ~9% CAGR, reflecting heavy supplier influence. Vendor-specific content refresh cycles force periodic upgrades and add costs. Proprietary curricula reduce dependence but still require external licenses to meet industry standards. Bundled pricing models compress negotiation leverage.

Accreditation and compliance bodies

Regional and national accreditors and regulators function as quasi-suppliers of market access for Perdoceo, since accreditation status directly determines eligibility for federal student aid and the size of the enrollment funnel.

Compliance changes in 2024 have continued to force costly system and process updates, raising operating risk and capex needs for reporting and academic controls.

Limited alternative accrediting pathways heighten these bodies' bargaining power despite non-commercial motives, meaning regulatory decisions can quickly affect revenue streams tied to federal aid.

- Accreditation impact

- Federal aid dependency

- Compliance-driven costs

- Limited alternatives

Marketing channels and lead generators

Digital ad platforms and select affiliates control access to the majority of student leads, with auction-based channels accounting for over 60% of recruitment spend and CPCs rising roughly 15% in 2024; privacy changes (ID deprecations) have further pushed acquisition costs higher. Diversifying to organic, referral and employer pathways reduces dependency but typically requires 6–12 months to scale. Performance-based contracts can align incentives but may concentrate 20–50% of volume in a few channels, increasing supplier power.

- >60% recruitment spend via auctioned digital channels (2024)

- CPC +15% YoY (2024)

- Organic/referral ramp 6–12 months

- Performance contracts can concentrate 20–50% of volume

High supplier concentration and faculty scarcity squeeze online education margins

Supplier concentration: top‑3 cloud 66% / LMS ~60% (2024). Faculty scarcity: adjuncts ~70% of teaching staff; wage pressure +4% (2023–24). Content/vendors: global e‑learning >$300B (2023), ~9% CAGR. Recruitment: auctioned channels >60% spend; CPC +15% (2024). Accreditation controls federal aid access, raising switching costs.

| Metric | 2024 value |

|---|---|

| Top‑3 cloud share | 66% |

| LMS share | ~60% |

| Adjuncts | 70% |

| CPC YoY | +15% |

What is included in the product

Concise Porter's Five Forces analysis for Perdoceo Education, revealing competitive intensity, buyer/supplier leverage, threat of substitutes and entrants, plus strategic implications for pricing, margins and growth.

A concise one-sheet Porter's Five Forces for Perdoceo Education that highlights competitive pressures, regulatory risk, and supplier/buyer leverage—ready to drop into decks or reports to speed strategic decision-making and relieve analysis bottlenecks.

Customers Bargaining Power

Price-sensitive adult learners

Working adults weigh Perdoceo tuition against measurable employability gains, with 50% of surveyed adult learners in 2024 naming cost as their primary decision factor, creating strong price pressure. Online comparison tools and transparent outcome data heighten sensitivity by exposing ROI differences across programs. Scholarships and transfer-credit policies materially shift enrollment choices, while flexible pacing and modality act as non-price bargaining levers.

Low switching costs online

Low switching costs let students move programs between terms with modest friction, contributing to an estimated annual churn near 25% in online adult education providers in 2024. Uneven credit transfer policies reduce stickiness for many Perdoceo students, while trial courses and stackable credentials have grown adoption, enabling exits after short modules. Reputation and enhanced student support remain key retention levers, materially affecting enrollment stability.

Outcome-driven decision-making

Buyers now prioritize placement rates, licensure pass rates and ROI, with 72% of prospective students in 2024 citing employment outcomes as their top selection criterion; poor outcomes shift demand rapidly to competitors. Publishing outcomes data has improved transparency but raises regulatory and reputational accountability as seen in increased scrutiny of for-profit providers. Strategic employer partnerships (e.g., credentialing agreements) validate value propositions and materially reduce buyer bargaining power.

Alternative financing expectations

Students increasingly expect scholarships, flexible payment plans and employer tuition assistance; about 6 million students received Pell Grants in 2024, which lowers immediate out-of-pocket cost but increases regulatory and outcome scrutiny for providers. Income-aligned repayment and micro-payment models boost buyer leverage, while faster, easier aid processing becomes a differentiator in enrollment decisions.

- Expectations: scholarships, payment plans, employer aid

- Federal aid: ~6M Pell recipients (2024) → scrutiny

- Payment models: income-aligned, micro-payments increase leverage

- Ops: aid-processing speed = competitive factor

Information-rich comparisons

Ratings, reviews and program-ranking sites give Perdoceo buyers direct leverage by making outcomes and complaints visible; transparent pricing and syllabus access allow fast apples-to-apples checks. Negative sentiment can cascade on social and review platforms, increasing pressure for discounts or program enhancements. Strong, responsive student services and clear outcome reporting reduce raw price sensitivity by preserving perceived value.

- Reviews amplify buyer leverage

- Transparent pricing enables comparisons

- Service responsiveness mitigates discount pressure

Buyers press price & outcomes: 50% cost, 72% outcome

Buyers exert strong price and outcome pressure: 50% cite cost as top factor and 72% prioritize employment outcomes in 2024. Low switching costs drive ~25% annual churn among online adult learners, raising retention spend. ~6M Pell recipients amplify regulatory scrutiny while employer tuition and flexible payment models reduce buyer price leverage.

| Metric | 2024 | Impact |

|---|---|---|

| Cost priority | 50% | ↑ Price pressure |

| Outcome focus | 72% | ↑ Reputation risk |

| Churn | 25% | ↑ Retention cost |

| Pell recipients | 6M | ↑ Scrutiny |

Preview the Actual Deliverable

Perdoceo Education Porter's Five Forces Analysis

This preview shows the exact Perdoceo Education Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready to use. No mockups, no placeholders: the file displayed here is the deliverable available for instant download upon payment. Use it as-is for strategic planning, valuation inputs, or client presentations.

Go Beyond the Preview—Access the Full Strategic Report

Perdoceo Education faces moderate competitive intensity amid a concentrated for‑profit education sector, high regulatory and accreditation pressure, notable buyer sensitivity on price and outcomes, and rising substitute threats from online platforms and nontraditional providers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Perdoceo Education’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated ed-tech platforms

Perdoceo depends on concentrated LMS, cloud and proctoring vendors where the top three cloud providers held ~66% market share in 2024 and the leading LMS vendors account for roughly 60% of higher‑ed deployments, making switching costly. Vendor consolidation can push fees or tougher terms; multi‑vendor strategies mitigate risk but integration overhead preserves supplier leverage. Long‑term contracts lock pricing yet constrain flexibility.

Specialized faculty and adjunct talent

Qualified instructors in niche healthcare and tech areas are scarce, giving faculty meaningful bargaining power; adjuncts still comprise about 70% of US higher-education teaching staff (2024). Wage inflation and expanded remote options have elevated compensation demands, with average hourly earnings rising ~4% in 2023–24. Standardized online course shells reduce individual dependency, yet program outcomes remain faculty‑dependent. Strict credentialing for clinical and tech roles further narrows supply.

Content and licensing dependencies

Third-party courseware, simulations and vendor certifications are often must-have inputs for Perdoceo programs, and the global e-learning market exceeded 300 billion in 2023 with ~9% CAGR, reflecting heavy supplier influence. Vendor-specific content refresh cycles force periodic upgrades and add costs. Proprietary curricula reduce dependence but still require external licenses to meet industry standards. Bundled pricing models compress negotiation leverage.

Accreditation and compliance bodies

Regional and national accreditors and regulators function as quasi-suppliers of market access for Perdoceo, since accreditation status directly determines eligibility for federal student aid and the size of the enrollment funnel.

Compliance changes in 2024 have continued to force costly system and process updates, raising operating risk and capex needs for reporting and academic controls.

Limited alternative accrediting pathways heighten these bodies' bargaining power despite non-commercial motives, meaning regulatory decisions can quickly affect revenue streams tied to federal aid.

- Accreditation impact

- Federal aid dependency

- Compliance-driven costs

- Limited alternatives

Marketing channels and lead generators

Digital ad platforms and select affiliates control access to the majority of student leads, with auction-based channels accounting for over 60% of recruitment spend and CPCs rising roughly 15% in 2024; privacy changes (ID deprecations) have further pushed acquisition costs higher. Diversifying to organic, referral and employer pathways reduces dependency but typically requires 6–12 months to scale. Performance-based contracts can align incentives but may concentrate 20–50% of volume in a few channels, increasing supplier power.

- >60% recruitment spend via auctioned digital channels (2024)

- CPC +15% YoY (2024)

- Organic/referral ramp 6–12 months

- Performance contracts can concentrate 20–50% of volume

High supplier concentration and faculty scarcity squeeze online education margins

Supplier concentration: top‑3 cloud 66% / LMS ~60% (2024). Faculty scarcity: adjuncts ~70% of teaching staff; wage pressure +4% (2023–24). Content/vendors: global e‑learning >$300B (2023), ~9% CAGR. Recruitment: auctioned channels >60% spend; CPC +15% (2024). Accreditation controls federal aid access, raising switching costs.

| Metric | 2024 value |

|---|---|

| Top‑3 cloud share | 66% |

| LMS share | ~60% |

| Adjuncts | 70% |

| CPC YoY | +15% |

What is included in the product

Concise Porter's Five Forces analysis for Perdoceo Education, revealing competitive intensity, buyer/supplier leverage, threat of substitutes and entrants, plus strategic implications for pricing, margins and growth.

A concise one-sheet Porter's Five Forces for Perdoceo Education that highlights competitive pressures, regulatory risk, and supplier/buyer leverage—ready to drop into decks or reports to speed strategic decision-making and relieve analysis bottlenecks.

Customers Bargaining Power

Price-sensitive adult learners

Working adults weigh Perdoceo tuition against measurable employability gains, with 50% of surveyed adult learners in 2024 naming cost as their primary decision factor, creating strong price pressure. Online comparison tools and transparent outcome data heighten sensitivity by exposing ROI differences across programs. Scholarships and transfer-credit policies materially shift enrollment choices, while flexible pacing and modality act as non-price bargaining levers.

Low switching costs online

Low switching costs let students move programs between terms with modest friction, contributing to an estimated annual churn near 25% in online adult education providers in 2024. Uneven credit transfer policies reduce stickiness for many Perdoceo students, while trial courses and stackable credentials have grown adoption, enabling exits after short modules. Reputation and enhanced student support remain key retention levers, materially affecting enrollment stability.

Outcome-driven decision-making

Buyers now prioritize placement rates, licensure pass rates and ROI, with 72% of prospective students in 2024 citing employment outcomes as their top selection criterion; poor outcomes shift demand rapidly to competitors. Publishing outcomes data has improved transparency but raises regulatory and reputational accountability as seen in increased scrutiny of for-profit providers. Strategic employer partnerships (e.g., credentialing agreements) validate value propositions and materially reduce buyer bargaining power.

Alternative financing expectations

Students increasingly expect scholarships, flexible payment plans and employer tuition assistance; about 6 million students received Pell Grants in 2024, which lowers immediate out-of-pocket cost but increases regulatory and outcome scrutiny for providers. Income-aligned repayment and micro-payment models boost buyer leverage, while faster, easier aid processing becomes a differentiator in enrollment decisions.

- Expectations: scholarships, payment plans, employer aid

- Federal aid: ~6M Pell recipients (2024) → scrutiny

- Payment models: income-aligned, micro-payments increase leverage

- Ops: aid-processing speed = competitive factor

Information-rich comparisons

Ratings, reviews and program-ranking sites give Perdoceo buyers direct leverage by making outcomes and complaints visible; transparent pricing and syllabus access allow fast apples-to-apples checks. Negative sentiment can cascade on social and review platforms, increasing pressure for discounts or program enhancements. Strong, responsive student services and clear outcome reporting reduce raw price sensitivity by preserving perceived value.

- Reviews amplify buyer leverage

- Transparent pricing enables comparisons

- Service responsiveness mitigates discount pressure

Buyers press price & outcomes: 50% cost, 72% outcome

Buyers exert strong price and outcome pressure: 50% cite cost as top factor and 72% prioritize employment outcomes in 2024. Low switching costs drive ~25% annual churn among online adult learners, raising retention spend. ~6M Pell recipients amplify regulatory scrutiny while employer tuition and flexible payment models reduce buyer price leverage.

| Metric | 2024 | Impact |

|---|---|---|

| Cost priority | 50% | ↑ Price pressure |

| Outcome focus | 72% | ↑ Reputation risk |

| Churn | 25% | ↑ Retention cost |

| Pell recipients | 6M | ↑ Scrutiny |

Preview the Actual Deliverable

Perdoceo Education Porter's Five Forces Analysis

This preview shows the exact Perdoceo Education Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready to use. No mockups, no placeholders: the file displayed here is the deliverable available for instant download upon payment. Use it as-is for strategic planning, valuation inputs, or client presentations.

Description

Go Beyond the Preview—Access the Full Strategic Report

Perdoceo Education faces moderate competitive intensity amid a concentrated for‑profit education sector, high regulatory and accreditation pressure, notable buyer sensitivity on price and outcomes, and rising substitute threats from online platforms and nontraditional providers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Perdoceo Education’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated ed-tech platforms

Perdoceo depends on concentrated LMS, cloud and proctoring vendors where the top three cloud providers held ~66% market share in 2024 and the leading LMS vendors account for roughly 60% of higher‑ed deployments, making switching costly. Vendor consolidation can push fees or tougher terms; multi‑vendor strategies mitigate risk but integration overhead preserves supplier leverage. Long‑term contracts lock pricing yet constrain flexibility.

Specialized faculty and adjunct talent

Qualified instructors in niche healthcare and tech areas are scarce, giving faculty meaningful bargaining power; adjuncts still comprise about 70% of US higher-education teaching staff (2024). Wage inflation and expanded remote options have elevated compensation demands, with average hourly earnings rising ~4% in 2023–24. Standardized online course shells reduce individual dependency, yet program outcomes remain faculty‑dependent. Strict credentialing for clinical and tech roles further narrows supply.

Content and licensing dependencies

Third-party courseware, simulations and vendor certifications are often must-have inputs for Perdoceo programs, and the global e-learning market exceeded 300 billion in 2023 with ~9% CAGR, reflecting heavy supplier influence. Vendor-specific content refresh cycles force periodic upgrades and add costs. Proprietary curricula reduce dependence but still require external licenses to meet industry standards. Bundled pricing models compress negotiation leverage.

Accreditation and compliance bodies

Regional and national accreditors and regulators function as quasi-suppliers of market access for Perdoceo, since accreditation status directly determines eligibility for federal student aid and the size of the enrollment funnel.

Compliance changes in 2024 have continued to force costly system and process updates, raising operating risk and capex needs for reporting and academic controls.

Limited alternative accrediting pathways heighten these bodies' bargaining power despite non-commercial motives, meaning regulatory decisions can quickly affect revenue streams tied to federal aid.

- Accreditation impact

- Federal aid dependency

- Compliance-driven costs

- Limited alternatives

Marketing channels and lead generators

Digital ad platforms and select affiliates control access to the majority of student leads, with auction-based channels accounting for over 60% of recruitment spend and CPCs rising roughly 15% in 2024; privacy changes (ID deprecations) have further pushed acquisition costs higher. Diversifying to organic, referral and employer pathways reduces dependency but typically requires 6–12 months to scale. Performance-based contracts can align incentives but may concentrate 20–50% of volume in a few channels, increasing supplier power.

- >60% recruitment spend via auctioned digital channels (2024)

- CPC +15% YoY (2024)

- Organic/referral ramp 6–12 months

- Performance contracts can concentrate 20–50% of volume

High supplier concentration and faculty scarcity squeeze online education margins

Supplier concentration: top‑3 cloud 66% / LMS ~60% (2024). Faculty scarcity: adjuncts ~70% of teaching staff; wage pressure +4% (2023–24). Content/vendors: global e‑learning >$300B (2023), ~9% CAGR. Recruitment: auctioned channels >60% spend; CPC +15% (2024). Accreditation controls federal aid access, raising switching costs.

| Metric | 2024 value |

|---|---|

| Top‑3 cloud share | 66% |

| LMS share | ~60% |

| Adjuncts | 70% |

| CPC YoY | +15% |

What is included in the product

Concise Porter's Five Forces analysis for Perdoceo Education, revealing competitive intensity, buyer/supplier leverage, threat of substitutes and entrants, plus strategic implications for pricing, margins and growth.

A concise one-sheet Porter's Five Forces for Perdoceo Education that highlights competitive pressures, regulatory risk, and supplier/buyer leverage—ready to drop into decks or reports to speed strategic decision-making and relieve analysis bottlenecks.

Customers Bargaining Power

Price-sensitive adult learners

Working adults weigh Perdoceo tuition against measurable employability gains, with 50% of surveyed adult learners in 2024 naming cost as their primary decision factor, creating strong price pressure. Online comparison tools and transparent outcome data heighten sensitivity by exposing ROI differences across programs. Scholarships and transfer-credit policies materially shift enrollment choices, while flexible pacing and modality act as non-price bargaining levers.

Low switching costs online

Low switching costs let students move programs between terms with modest friction, contributing to an estimated annual churn near 25% in online adult education providers in 2024. Uneven credit transfer policies reduce stickiness for many Perdoceo students, while trial courses and stackable credentials have grown adoption, enabling exits after short modules. Reputation and enhanced student support remain key retention levers, materially affecting enrollment stability.

Outcome-driven decision-making

Buyers now prioritize placement rates, licensure pass rates and ROI, with 72% of prospective students in 2024 citing employment outcomes as their top selection criterion; poor outcomes shift demand rapidly to competitors. Publishing outcomes data has improved transparency but raises regulatory and reputational accountability as seen in increased scrutiny of for-profit providers. Strategic employer partnerships (e.g., credentialing agreements) validate value propositions and materially reduce buyer bargaining power.

Alternative financing expectations

Students increasingly expect scholarships, flexible payment plans and employer tuition assistance; about 6 million students received Pell Grants in 2024, which lowers immediate out-of-pocket cost but increases regulatory and outcome scrutiny for providers. Income-aligned repayment and micro-payment models boost buyer leverage, while faster, easier aid processing becomes a differentiator in enrollment decisions.

- Expectations: scholarships, payment plans, employer aid

- Federal aid: ~6M Pell recipients (2024) → scrutiny

- Payment models: income-aligned, micro-payments increase leverage

- Ops: aid-processing speed = competitive factor

Information-rich comparisons

Ratings, reviews and program-ranking sites give Perdoceo buyers direct leverage by making outcomes and complaints visible; transparent pricing and syllabus access allow fast apples-to-apples checks. Negative sentiment can cascade on social and review platforms, increasing pressure for discounts or program enhancements. Strong, responsive student services and clear outcome reporting reduce raw price sensitivity by preserving perceived value.

- Reviews amplify buyer leverage

- Transparent pricing enables comparisons

- Service responsiveness mitigates discount pressure

Buyers press price & outcomes: 50% cost, 72% outcome

Buyers exert strong price and outcome pressure: 50% cite cost as top factor and 72% prioritize employment outcomes in 2024. Low switching costs drive ~25% annual churn among online adult learners, raising retention spend. ~6M Pell recipients amplify regulatory scrutiny while employer tuition and flexible payment models reduce buyer price leverage.

| Metric | 2024 | Impact |

|---|---|---|

| Cost priority | 50% | ↑ Price pressure |

| Outcome focus | 72% | ↑ Reputation risk |

| Churn | 25% | ↑ Retention cost |

| Pell recipients | 6M | ↑ Scrutiny |

Preview the Actual Deliverable

Perdoceo Education Porter's Five Forces Analysis

This preview shows the exact Perdoceo Education Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready to use. No mockups, no placeholders: the file displayed here is the deliverable available for instant download upon payment. Use it as-is for strategic planning, valuation inputs, or client presentations.