Perdue Farms Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

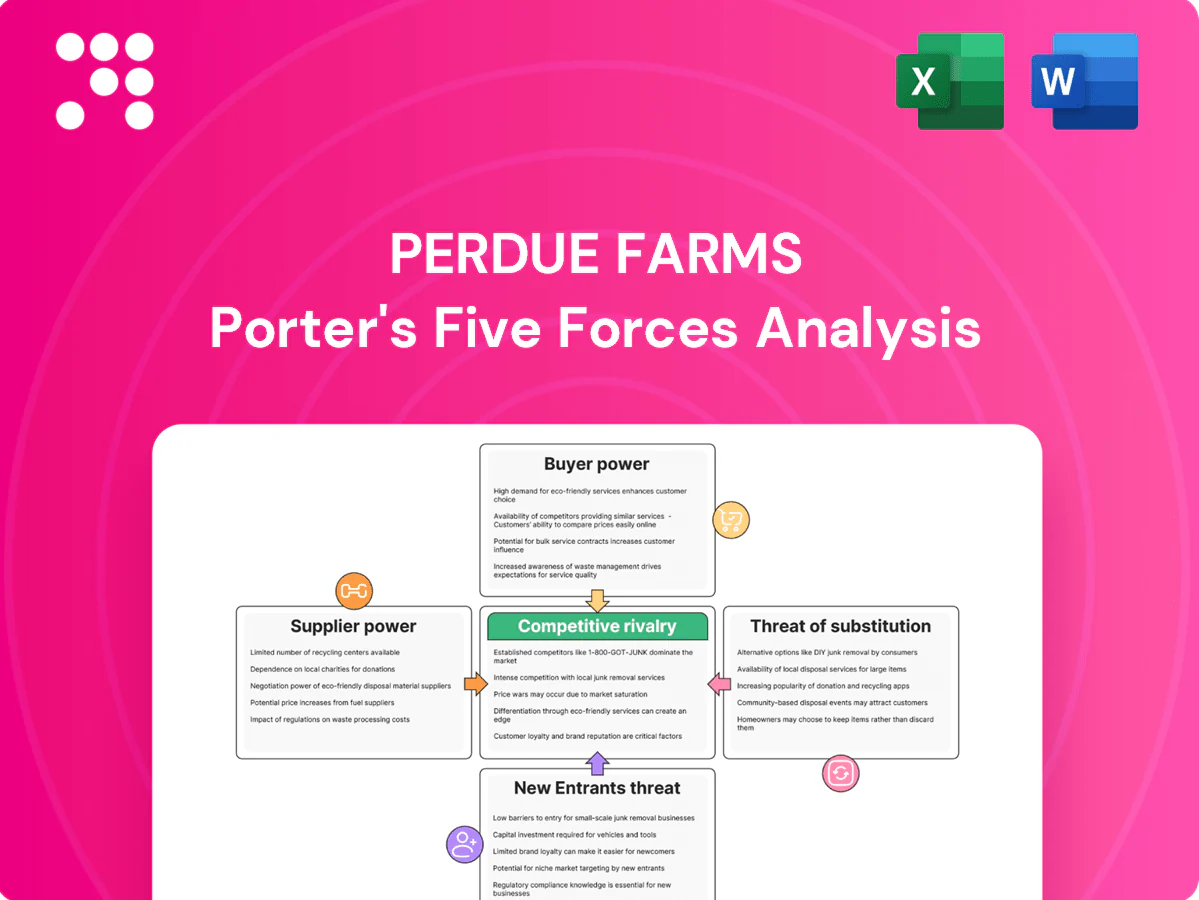

Perdue Farms faces intense competitive rivalry from integrated poultry processors, moderate supplier power from feed and labor markets, rising buyer power due to retailer consolidation, growing substitute threats from plant‑based proteins, and meaningful regulatory barriers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Perdue Farms’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertically integrated feed control

Perdue’s vertically integrated feed control—with in-house feed mills and direct grain sourcing—significantly reduces reliance on third-party suppliers and curbs supplier leverage, lowering switching costs and information asymmetry. Global corn and soy swings, which can move on the order of ±20% year-on-year, still transmit to costs. Hedging programs and long-term grain contracts mitigate but do not eliminate price shocks. Integration preserves margin resilience versus peers reliant on spot feed purchases.

Diverse input base, limited concentration

Inputs span breeders/genetics, vaccines, packaging, equipment and energy, diluting any single supplier’s power. In 2024 some niches (grandparent-stock genetics, specialty packaging) remain concentrated to roughly 3–5 key suppliers, creating episodic leverage. Perdue uses dual-sourcing and approved-vendor lists spanning hundreds of suppliers to negotiate terms. Strict compliance and quality specs constrain rapid supplier substitution.

Contract grower dynamics

Perdue’s contract growers—about 4,000 family farms—provide labor, housing and bird care but rely on integrator‑supplied chicks and feed, limiting bargaining power; Perdue’s reported 2024 revenue was roughly $7.5 billion, concentrating leverage with the integrator. Performance‑based pay, often 20–30% of grower income, aligns incentives but consolidates negotiation clout with Perdue. Local labor and housing shortages create bottlenecks that reduce short‑term supply flexibility.

Energy and logistics exposure

Perdue’s processing plants are energy- and cold-chain-intensive, making utility and diesel suppliers potent cost drivers; US retail diesel averaged about 3.80 USD/gal in 2024, and regional utility monopolies limit switching. Efficiency upgrades and renewables PPAs can cut exposure—corporate buyers report 10–20% energy savings from retrofits. Tight truckload capacity in 2024 pushed national spot rates up ~25%, pressuring freight costs.

- Energy intensity: cold storage dependence

- Diesel volatility: ~3.80 USD/gal (2024)

- Utility market power: regional monopolies

- Mitigants: efficiency, renewables PPAs

- Logistics: +25% spot rate pressure (2024)

Biosecurity and compliance inputs

Bargaining power of suppliers for biosecurity and compliance inputs is elevated as disease prevention drives reliance on specialized sanitation, PPE and veterinary supplies; USDA reported over 58 million birds affected by HPAI in 2022–23, underscoring demand spikes. During outbreaks, limited approved vendors can exert pricing power, while inventory buffering and qualifying alternates mitigate exposure; regulatory shifts can temporarily tighten supplier pools.

- Specialized inputs concentrated among few vendors

- HPAI impact: >58 million birds 2022–23

- Inventory buffering lowers supply risk

- Regulatory changes can raise supplier leverage

Vertical-integrator tightens supplier power despite ±20% feed swings

Perdue’s vertical feed integration and 4,000 contract growers concentrate purchasing power with the integrator, limiting supplier leverage despite global corn/soy volatility (~±20% y/y). Key niches remain concentrated (3–5 vendors), HPAI shocks (>58M birds 2022–23) and 2024 diesel ~$3.80/gal raise episodic supplier power; hedges, long‑term contracts and dual‑sourcing mitigate risk.

| Metric | 2024 / recent |

|---|---|

| Revenue | $7.5B |

| Diesel | $3.80/gal |

| Freight spot change | +25% |

| HPAI impact | >58M birds (2022–23) |

| Supplier concentration | 3–5 key vendors |

What is included in the product

Tailored Porter's Five Forces analysis for Perdue Farms uncovering competitive drivers, supplier and buyer power, substitute threats, and entry barriers that shape pricing and profitability. Includes strategic commentary on disruptive forces and market dynamics to inform investor materials, strategy decks, or academic projects.

A concise Porter's Five Forces snapshot for Perdue Farms that highlights supplier, buyer, entrant, substitute, and competitive pressures—perfect for swiftly identifying strategic pain points and prioritizing responses.

Customers Bargaining Power

Consolidated retail channels

Large grocers, club stores and mass retailers — e.g., Walmart (FY2024 revenue $611.3B), Kroger (FY2024 $137.9B) and Costco (FY2024 $256B) — command volume and shelf access, boosting bargaining power. They extract price concessions, promotional funding and stringent service levels. Growing private label penetration further increases buyer leverage, though Perdue’s branded and differentiated lines help moderate price pressure.

Foodservice and QSR scale

Distributors and national QSRs buy Perdue-scale poultry in bulk to strict, standardized specs, concentrating buyer power and forcing price concessions. Multi-year RFPs and bid cycles typically span 3–5 years, compressing supplier margins and locking volumes. Operational reliability and end-to-end traceability are table stakes for continued contracts. Rapid menu shifts can reallocate volumes in weeks, quickly pressuring pricing and capacity planning.

Low switching costs

Chicken cuts are highly standardized so buyers can switch among qualified processors; US broiler production was about 50 billion pounds in 2024 (USDA), underscoring abundant supply and buyer options. Certifications like organic or ABF create some stickiness—organic represented roughly 4% of retail chicken volume in 2024—but are replicable by competitors. Service reliability and fill rates become key differentiators, while price remains the primary decision driver in commodity SKUs.

Demand for value-add

Buyers increasingly demand marinated, fully cooked and convenience offerings to lift category margins; value-add products make direct price comparisons harder and can weaken buyer price power, but they raise expectations for service, shelf-life and continuous innovation. Co-development secures accounts through customized solutions while increasing vendor accountability for quality and supply consistency.

- Value-add reduces price transparency

- Raises service/innovation burden

- Co-development strengthens ties, raises vendor risk

ESG and traceability requirements

- ESG-driven specs

- Audit/data cost shift

- Premium placement reward

- Delisting/penalties risk

Retailer and QSR scale, 50B lb broiler supply and 4% organic share squeeze suppliers

Large retailers (Walmart FY2024 $611.3B; Kroger FY2024 $137.9B; Costco FY2024 $256B) and QSRs exert strong price and service pressure; private label growth and 50B lb US broiler supply (USDA 2024) increase buyer leverage. Value-add and certifications (organic ~4% retail chicken 2024) reduce pure price transparency but raise service and compliance burdens, with audits shifting costs to suppliers.

| Metric | 2024 |

|---|---|

| Major retailer revenue | WMT $611.3B; Kroger $137.9B; Costco $256B |

| US broiler supply | ~50B lb |

| Organic share | ~4% |

Full Version Awaits

Perdue Farms Porter's Five Forces Analysis

This Perdue Farms Porter's Five Forces Analysis preview is the exact, fully formatted document you'll receive immediately after purchase, not a sample or placeholder. It contains the full competitive assessment, implications and concise conclusions ready for download and use. No mockups or edits are required—what you see is what you get.

Go Beyond the Preview—Access the Full Strategic Report

Perdue Farms faces intense competitive rivalry from integrated poultry processors, moderate supplier power from feed and labor markets, rising buyer power due to retailer consolidation, growing substitute threats from plant‑based proteins, and meaningful regulatory barriers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Perdue Farms’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertically integrated feed control

Perdue’s vertically integrated feed control—with in-house feed mills and direct grain sourcing—significantly reduces reliance on third-party suppliers and curbs supplier leverage, lowering switching costs and information asymmetry. Global corn and soy swings, which can move on the order of ±20% year-on-year, still transmit to costs. Hedging programs and long-term grain contracts mitigate but do not eliminate price shocks. Integration preserves margin resilience versus peers reliant on spot feed purchases.

Diverse input base, limited concentration

Inputs span breeders/genetics, vaccines, packaging, equipment and energy, diluting any single supplier’s power. In 2024 some niches (grandparent-stock genetics, specialty packaging) remain concentrated to roughly 3–5 key suppliers, creating episodic leverage. Perdue uses dual-sourcing and approved-vendor lists spanning hundreds of suppliers to negotiate terms. Strict compliance and quality specs constrain rapid supplier substitution.

Contract grower dynamics

Perdue’s contract growers—about 4,000 family farms—provide labor, housing and bird care but rely on integrator‑supplied chicks and feed, limiting bargaining power; Perdue’s reported 2024 revenue was roughly $7.5 billion, concentrating leverage with the integrator. Performance‑based pay, often 20–30% of grower income, aligns incentives but consolidates negotiation clout with Perdue. Local labor and housing shortages create bottlenecks that reduce short‑term supply flexibility.

Energy and logistics exposure

Perdue’s processing plants are energy- and cold-chain-intensive, making utility and diesel suppliers potent cost drivers; US retail diesel averaged about 3.80 USD/gal in 2024, and regional utility monopolies limit switching. Efficiency upgrades and renewables PPAs can cut exposure—corporate buyers report 10–20% energy savings from retrofits. Tight truckload capacity in 2024 pushed national spot rates up ~25%, pressuring freight costs.

- Energy intensity: cold storage dependence

- Diesel volatility: ~3.80 USD/gal (2024)

- Utility market power: regional monopolies

- Mitigants: efficiency, renewables PPAs

- Logistics: +25% spot rate pressure (2024)

Biosecurity and compliance inputs

Bargaining power of suppliers for biosecurity and compliance inputs is elevated as disease prevention drives reliance on specialized sanitation, PPE and veterinary supplies; USDA reported over 58 million birds affected by HPAI in 2022–23, underscoring demand spikes. During outbreaks, limited approved vendors can exert pricing power, while inventory buffering and qualifying alternates mitigate exposure; regulatory shifts can temporarily tighten supplier pools.

- Specialized inputs concentrated among few vendors

- HPAI impact: >58 million birds 2022–23

- Inventory buffering lowers supply risk

- Regulatory changes can raise supplier leverage

Vertical-integrator tightens supplier power despite ±20% feed swings

Perdue’s vertical feed integration and 4,000 contract growers concentrate purchasing power with the integrator, limiting supplier leverage despite global corn/soy volatility (~±20% y/y). Key niches remain concentrated (3–5 vendors), HPAI shocks (>58M birds 2022–23) and 2024 diesel ~$3.80/gal raise episodic supplier power; hedges, long‑term contracts and dual‑sourcing mitigate risk.

| Metric | 2024 / recent |

|---|---|

| Revenue | $7.5B |

| Diesel | $3.80/gal |

| Freight spot change | +25% |

| HPAI impact | >58M birds (2022–23) |

| Supplier concentration | 3–5 key vendors |

What is included in the product

Tailored Porter's Five Forces analysis for Perdue Farms uncovering competitive drivers, supplier and buyer power, substitute threats, and entry barriers that shape pricing and profitability. Includes strategic commentary on disruptive forces and market dynamics to inform investor materials, strategy decks, or academic projects.

A concise Porter's Five Forces snapshot for Perdue Farms that highlights supplier, buyer, entrant, substitute, and competitive pressures—perfect for swiftly identifying strategic pain points and prioritizing responses.

Customers Bargaining Power

Consolidated retail channels

Large grocers, club stores and mass retailers — e.g., Walmart (FY2024 revenue $611.3B), Kroger (FY2024 $137.9B) and Costco (FY2024 $256B) — command volume and shelf access, boosting bargaining power. They extract price concessions, promotional funding and stringent service levels. Growing private label penetration further increases buyer leverage, though Perdue’s branded and differentiated lines help moderate price pressure.

Foodservice and QSR scale

Distributors and national QSRs buy Perdue-scale poultry in bulk to strict, standardized specs, concentrating buyer power and forcing price concessions. Multi-year RFPs and bid cycles typically span 3–5 years, compressing supplier margins and locking volumes. Operational reliability and end-to-end traceability are table stakes for continued contracts. Rapid menu shifts can reallocate volumes in weeks, quickly pressuring pricing and capacity planning.

Low switching costs

Chicken cuts are highly standardized so buyers can switch among qualified processors; US broiler production was about 50 billion pounds in 2024 (USDA), underscoring abundant supply and buyer options. Certifications like organic or ABF create some stickiness—organic represented roughly 4% of retail chicken volume in 2024—but are replicable by competitors. Service reliability and fill rates become key differentiators, while price remains the primary decision driver in commodity SKUs.

Demand for value-add

Buyers increasingly demand marinated, fully cooked and convenience offerings to lift category margins; value-add products make direct price comparisons harder and can weaken buyer price power, but they raise expectations for service, shelf-life and continuous innovation. Co-development secures accounts through customized solutions while increasing vendor accountability for quality and supply consistency.

- Value-add reduces price transparency

- Raises service/innovation burden

- Co-development strengthens ties, raises vendor risk

ESG and traceability requirements

- ESG-driven specs

- Audit/data cost shift

- Premium placement reward

- Delisting/penalties risk

Retailer and QSR scale, 50B lb broiler supply and 4% organic share squeeze suppliers

Large retailers (Walmart FY2024 $611.3B; Kroger FY2024 $137.9B; Costco FY2024 $256B) and QSRs exert strong price and service pressure; private label growth and 50B lb US broiler supply (USDA 2024) increase buyer leverage. Value-add and certifications (organic ~4% retail chicken 2024) reduce pure price transparency but raise service and compliance burdens, with audits shifting costs to suppliers.

| Metric | 2024 |

|---|---|

| Major retailer revenue | WMT $611.3B; Kroger $137.9B; Costco $256B |

| US broiler supply | ~50B lb |

| Organic share | ~4% |

Full Version Awaits

Perdue Farms Porter's Five Forces Analysis

This Perdue Farms Porter's Five Forces Analysis preview is the exact, fully formatted document you'll receive immediately after purchase, not a sample or placeholder. It contains the full competitive assessment, implications and concise conclusions ready for download and use. No mockups or edits are required—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Perdue Farms faces intense competitive rivalry from integrated poultry processors, moderate supplier power from feed and labor markets, rising buyer power due to retailer consolidation, growing substitute threats from plant‑based proteins, and meaningful regulatory barriers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Perdue Farms’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertically integrated feed control

Perdue’s vertically integrated feed control—with in-house feed mills and direct grain sourcing—significantly reduces reliance on third-party suppliers and curbs supplier leverage, lowering switching costs and information asymmetry. Global corn and soy swings, which can move on the order of ±20% year-on-year, still transmit to costs. Hedging programs and long-term grain contracts mitigate but do not eliminate price shocks. Integration preserves margin resilience versus peers reliant on spot feed purchases.

Diverse input base, limited concentration

Inputs span breeders/genetics, vaccines, packaging, equipment and energy, diluting any single supplier’s power. In 2024 some niches (grandparent-stock genetics, specialty packaging) remain concentrated to roughly 3–5 key suppliers, creating episodic leverage. Perdue uses dual-sourcing and approved-vendor lists spanning hundreds of suppliers to negotiate terms. Strict compliance and quality specs constrain rapid supplier substitution.

Contract grower dynamics

Perdue’s contract growers—about 4,000 family farms—provide labor, housing and bird care but rely on integrator‑supplied chicks and feed, limiting bargaining power; Perdue’s reported 2024 revenue was roughly $7.5 billion, concentrating leverage with the integrator. Performance‑based pay, often 20–30% of grower income, aligns incentives but consolidates negotiation clout with Perdue. Local labor and housing shortages create bottlenecks that reduce short‑term supply flexibility.

Energy and logistics exposure

Perdue’s processing plants are energy- and cold-chain-intensive, making utility and diesel suppliers potent cost drivers; US retail diesel averaged about 3.80 USD/gal in 2024, and regional utility monopolies limit switching. Efficiency upgrades and renewables PPAs can cut exposure—corporate buyers report 10–20% energy savings from retrofits. Tight truckload capacity in 2024 pushed national spot rates up ~25%, pressuring freight costs.

- Energy intensity: cold storage dependence

- Diesel volatility: ~3.80 USD/gal (2024)

- Utility market power: regional monopolies

- Mitigants: efficiency, renewables PPAs

- Logistics: +25% spot rate pressure (2024)

Biosecurity and compliance inputs

Bargaining power of suppliers for biosecurity and compliance inputs is elevated as disease prevention drives reliance on specialized sanitation, PPE and veterinary supplies; USDA reported over 58 million birds affected by HPAI in 2022–23, underscoring demand spikes. During outbreaks, limited approved vendors can exert pricing power, while inventory buffering and qualifying alternates mitigate exposure; regulatory shifts can temporarily tighten supplier pools.

- Specialized inputs concentrated among few vendors

- HPAI impact: >58 million birds 2022–23

- Inventory buffering lowers supply risk

- Regulatory changes can raise supplier leverage

Vertical-integrator tightens supplier power despite ±20% feed swings

Perdue’s vertical feed integration and 4,000 contract growers concentrate purchasing power with the integrator, limiting supplier leverage despite global corn/soy volatility (~±20% y/y). Key niches remain concentrated (3–5 vendors), HPAI shocks (>58M birds 2022–23) and 2024 diesel ~$3.80/gal raise episodic supplier power; hedges, long‑term contracts and dual‑sourcing mitigate risk.

| Metric | 2024 / recent |

|---|---|

| Revenue | $7.5B |

| Diesel | $3.80/gal |

| Freight spot change | +25% |

| HPAI impact | >58M birds (2022–23) |

| Supplier concentration | 3–5 key vendors |

What is included in the product

Tailored Porter's Five Forces analysis for Perdue Farms uncovering competitive drivers, supplier and buyer power, substitute threats, and entry barriers that shape pricing and profitability. Includes strategic commentary on disruptive forces and market dynamics to inform investor materials, strategy decks, or academic projects.

A concise Porter's Five Forces snapshot for Perdue Farms that highlights supplier, buyer, entrant, substitute, and competitive pressures—perfect for swiftly identifying strategic pain points and prioritizing responses.

Customers Bargaining Power

Consolidated retail channels

Large grocers, club stores and mass retailers — e.g., Walmart (FY2024 revenue $611.3B), Kroger (FY2024 $137.9B) and Costco (FY2024 $256B) — command volume and shelf access, boosting bargaining power. They extract price concessions, promotional funding and stringent service levels. Growing private label penetration further increases buyer leverage, though Perdue’s branded and differentiated lines help moderate price pressure.

Foodservice and QSR scale

Distributors and national QSRs buy Perdue-scale poultry in bulk to strict, standardized specs, concentrating buyer power and forcing price concessions. Multi-year RFPs and bid cycles typically span 3–5 years, compressing supplier margins and locking volumes. Operational reliability and end-to-end traceability are table stakes for continued contracts. Rapid menu shifts can reallocate volumes in weeks, quickly pressuring pricing and capacity planning.

Low switching costs

Chicken cuts are highly standardized so buyers can switch among qualified processors; US broiler production was about 50 billion pounds in 2024 (USDA), underscoring abundant supply and buyer options. Certifications like organic or ABF create some stickiness—organic represented roughly 4% of retail chicken volume in 2024—but are replicable by competitors. Service reliability and fill rates become key differentiators, while price remains the primary decision driver in commodity SKUs.

Demand for value-add

Buyers increasingly demand marinated, fully cooked and convenience offerings to lift category margins; value-add products make direct price comparisons harder and can weaken buyer price power, but they raise expectations for service, shelf-life and continuous innovation. Co-development secures accounts through customized solutions while increasing vendor accountability for quality and supply consistency.

- Value-add reduces price transparency

- Raises service/innovation burden

- Co-development strengthens ties, raises vendor risk

ESG and traceability requirements

- ESG-driven specs

- Audit/data cost shift

- Premium placement reward

- Delisting/penalties risk

Retailer and QSR scale, 50B lb broiler supply and 4% organic share squeeze suppliers

Large retailers (Walmart FY2024 $611.3B; Kroger FY2024 $137.9B; Costco FY2024 $256B) and QSRs exert strong price and service pressure; private label growth and 50B lb US broiler supply (USDA 2024) increase buyer leverage. Value-add and certifications (organic ~4% retail chicken 2024) reduce pure price transparency but raise service and compliance burdens, with audits shifting costs to suppliers.

| Metric | 2024 |

|---|---|

| Major retailer revenue | WMT $611.3B; Kroger $137.9B; Costco $256B |

| US broiler supply | ~50B lb |

| Organic share | ~4% |

Full Version Awaits

Perdue Farms Porter's Five Forces Analysis

This Perdue Farms Porter's Five Forces Analysis preview is the exact, fully formatted document you'll receive immediately after purchase, not a sample or placeholder. It contains the full competitive assessment, implications and concise conclusions ready for download and use. No mockups or edits are required—what you see is what you get.