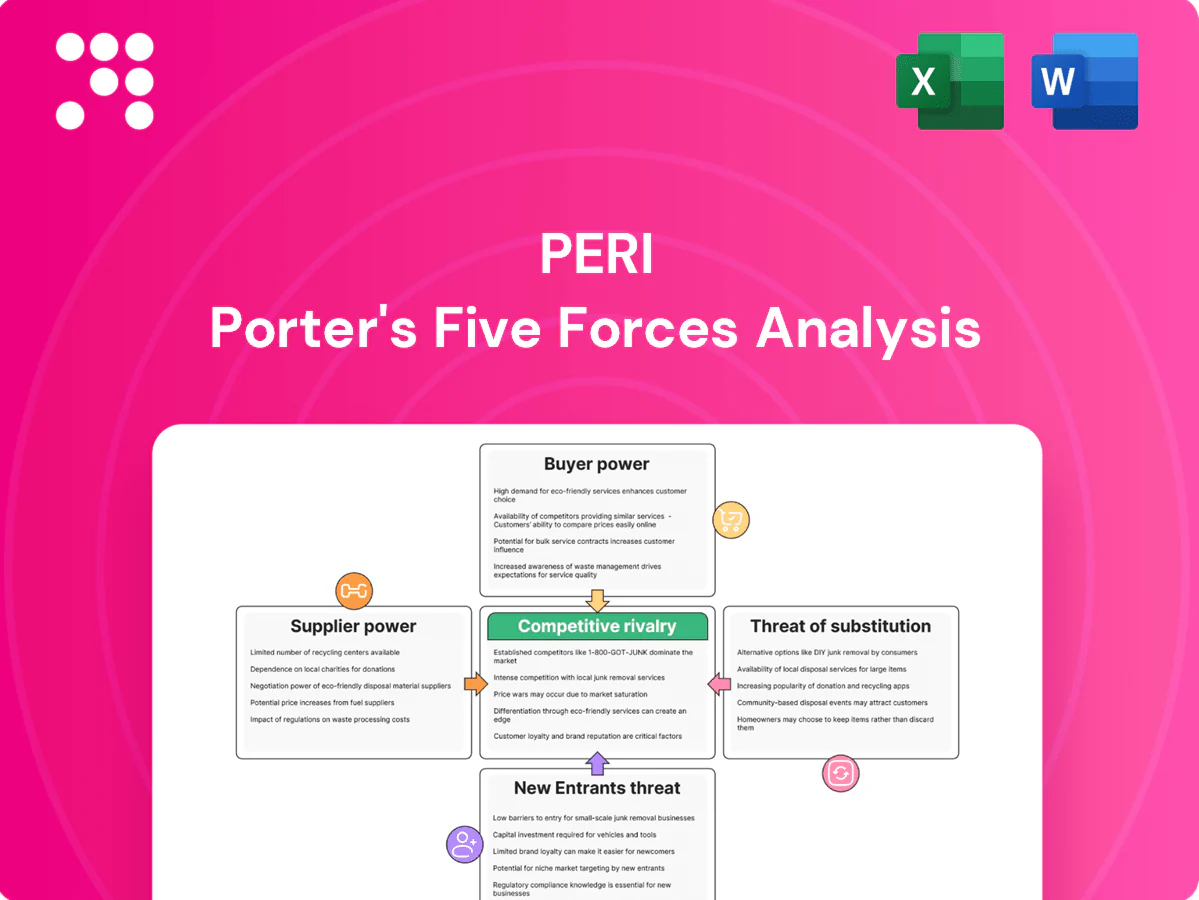

Peri Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Peri faces varied industry pressures—supplier bargaining, buyer demands, substitute threats, entrant risk, and rival rivalry—that shape margins and growth prospects. This snapshot highlights key friction points and strategic levers Peri can use to defend or expand its position. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals and actionable strategy.

Suppliers Bargaining Power

Commodity input exposure

PERI depends heavily on steel, aluminum and timber, exposing margins to commodity price volatility as input cost spikes allow suppliers to pass through increases rapidly. Hedging programs and multi-year supply contracts reduce short-term exposure but do not eliminate margin pressure during sharp commodity moves. Diversified global sourcing dilutes individual supplier leverage and supports procurement flexibility.

Specialized components

Custom extrusions, high-strength alloys and engineered connectors come from a narrow supplier base, concentrating bargaining power; certification and qualification typically take 6–12 months and can cost >$250,000, raising switching costs. In 2024 lead times for specialty alloys increased ~15% vs 2023, strengthening niche suppliers’ leverage. Dual-sourcing and in-house engineering can cut supplier dependency and mitigate risk.

Logistics and lead times

Bulky PERI systems need reliable freight, warehousing and JIT availability; sea freight lead times averaged ~45 days in 2023, amplifying supplier leverage when ports congest. Port disruptions in 2023–24 raised container delays and spot freight volatility, strengthening logistics providers’ bargaining power. PERI’s presence in 90+ countries and reported ~€1.9bn revenue in 2023, plus its owned fleet and regional hubs with inventory buffers, mitigate but do not eliminate spikes in logistics leverage.

Quality and safety standards

Strict compliance, traceability, and safety certifications limit acceptable suppliers, elevating supplier bargaining power; 2024 industry surveys reported ~62% of buyers requiring third-party safety certifications. Fewer qualified vendors can command better terms and price premia. Audits and supplier-development programs (used by ~74% of large buyers in 2024) broaden the pool, yet maintaining standards constrains rapid switching.

- Compliance limits supplier pool

- Audits & development expand options

- Fewer certified vendors = stronger supplier terms

ESG and regulatory constraints

- CSRD effective 2024: tighter disclosure

- Supplier ESG compliance increases negotiating leverage

- PERI scale eases access but cannot eliminate supply constraints

Supplier squeeze: steel +18%, alloy +15%, €1.9bn scale

PERI faces medium-high supplier power: commodity-driven inputs (steel +18% YoY in 2024) and specialty-alloy lead times +15% strengthen suppliers, while multi-year contracts, hedges and €1.9bn 2023 scale mitigate but do not eliminate risk.

| Metric | 2023 | 2024 |

|---|---|---|

| Revenue | €1.9bn | — |

| Steel price YoY | — | +18% |

| Alloy lead times | — | +15% |

What is included in the product

Peri-specific Porter's Five Forces analysis identifying competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and rivalry—highlighting disruptive trends, entry barriers, pricing influence, and strategic implications for Peri’s market positioning.

A concise one-sheet Porter's Five Forces snapshot that highlights competitive pressures, enables scenario toggles, and exports clean visuals for decks—turning complex strategic analysis into quick, actionable guidance for decision-makers.

Customers Bargaining Power

Large contractor concentration

Global EPCs and major contractors in 2024 run competitive tenders for multi-country programs worth billions, leveraging scale to demand discounts, strict SLAs and flexible rental terms; probe discounts commonly shift procurement margins and can compress supplier pricing power. Bundling multi-country volumes amplifies buyer leverage across regions. PERI offsets this by offering engineering value-add, bespoke solutions and a global support network to protect margins and retain contracts.

Rental vs. purchase optionality

Customers toggle between buying and renting based on project cycles, heightening price sensitivity and prompting tougher term negotiations. High-utilization periods force rate concessions as clients press for lower short-term costs. PERI mitigates this pressure through superior availability, high-quality fleet maintenance, and advanced project planning that secures longer-term contracts and reduces idle time.

Multi-sourcing to rivals

Clients can switch among PERI, Doka, ULMA, MEVA, Layher and others, and in 2024 comparable commodity systems continue to intensify price competition across projects. Approved vendor lists and standardized procurement mean substitution can occur within days to weeks, pressuring margins. Proprietary systems and tight design integration, however, lower churn by creating higher switching costs for complex projects.

Total cost of ownership focus

Buyers prioritize total cost of ownership, weighing setup speed, safety, reusability, and engineering support; 2024 case studies report up to 30% cycle-time reductions that often outweigh higher sticker prices. Data access, BIM integration, and on-site service materially lower perceived deployment risk and reduce buyer leverage. Weak proof points and sparse ROI evidence increase buyer negotiation power.

- setup speed

- safety & reusability

- engineering support

- up to 30% cycle-time savings (2024 case studies)

- BIM/data integration reduces perceived risk

Project-based demand volatility

Lumpy project awards give buyers timing leverage; large bids concentrated in quarters let clients demand concessions. During downturns contractors typically face rate reductions of 5–20% and payment terms extending from ~30 to 60–90 days. In booms availability outweighs price as utilizations often exceed 90%, and PERI’s fleet scale blunts but does not erase these buyer-power swings.

- Timing leverage: concentrated awards increase buyer bargaining

- Downturn impact: rate cuts 5–20% and payment terms to 60–90 days

- Boom dynamics: >90% utilization shifts power toward suppliers despite PERI’s fleet scale

Large EPC tenders compress supplier margins; booms restore supplier leverage

In 2024 large EPCs use billion-dollar multi-country tenders to extract discounts, strict SLAs and flexible rental terms, compressing supplier margins. Buyers switch among PERI, Doka, ULMA, MEVA and Layher within weeks, raising price sensitivity, though PERI’s engineering services and global support raise switching costs on complex jobs. Downturns drive 5–20% rate cuts and payment terms from ~30 to 60–90 days; booms (>90% utilization) shift leverage back to suppliers.

| Metric | 2024 value | Buyer impact |

|---|---|---|

| Tender size | Multi-country, $bn programs | High leverage |

| Rate cuts (downturn) | 5–20% | Margin compression |

| Payment terms | ~30 → 60–90 days | Cash flow pressure |

| Cycle-time savings | Up to 30% | Reduces price sensitivity |

| Utilization (booms) | >90% | Supplier leverage |

Same Document Delivered

Peri Porter's Five Forces Analysis

This Peri Porter's Five Forces analysis evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers to clarify industry dynamics. This preview is the exact document you'll receive upon purchase—fully formatted and ready to download. No mockups or samples: what you see is the final deliverable. Instant access after payment, ready for immediate use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Peri faces varied industry pressures—supplier bargaining, buyer demands, substitute threats, entrant risk, and rival rivalry—that shape margins and growth prospects. This snapshot highlights key friction points and strategic levers Peri can use to defend or expand its position. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals and actionable strategy.

Suppliers Bargaining Power

Commodity input exposure

PERI depends heavily on steel, aluminum and timber, exposing margins to commodity price volatility as input cost spikes allow suppliers to pass through increases rapidly. Hedging programs and multi-year supply contracts reduce short-term exposure but do not eliminate margin pressure during sharp commodity moves. Diversified global sourcing dilutes individual supplier leverage and supports procurement flexibility.

Specialized components

Custom extrusions, high-strength alloys and engineered connectors come from a narrow supplier base, concentrating bargaining power; certification and qualification typically take 6–12 months and can cost >$250,000, raising switching costs. In 2024 lead times for specialty alloys increased ~15% vs 2023, strengthening niche suppliers’ leverage. Dual-sourcing and in-house engineering can cut supplier dependency and mitigate risk.

Logistics and lead times

Bulky PERI systems need reliable freight, warehousing and JIT availability; sea freight lead times averaged ~45 days in 2023, amplifying supplier leverage when ports congest. Port disruptions in 2023–24 raised container delays and spot freight volatility, strengthening logistics providers’ bargaining power. PERI’s presence in 90+ countries and reported ~€1.9bn revenue in 2023, plus its owned fleet and regional hubs with inventory buffers, mitigate but do not eliminate spikes in logistics leverage.

Quality and safety standards

Strict compliance, traceability, and safety certifications limit acceptable suppliers, elevating supplier bargaining power; 2024 industry surveys reported ~62% of buyers requiring third-party safety certifications. Fewer qualified vendors can command better terms and price premia. Audits and supplier-development programs (used by ~74% of large buyers in 2024) broaden the pool, yet maintaining standards constrains rapid switching.

- Compliance limits supplier pool

- Audits & development expand options

- Fewer certified vendors = stronger supplier terms

ESG and regulatory constraints

- CSRD effective 2024: tighter disclosure

- Supplier ESG compliance increases negotiating leverage

- PERI scale eases access but cannot eliminate supply constraints

Supplier squeeze: steel +18%, alloy +15%, €1.9bn scale

PERI faces medium-high supplier power: commodity-driven inputs (steel +18% YoY in 2024) and specialty-alloy lead times +15% strengthen suppliers, while multi-year contracts, hedges and €1.9bn 2023 scale mitigate but do not eliminate risk.

| Metric | 2023 | 2024 |

|---|---|---|

| Revenue | €1.9bn | — |

| Steel price YoY | — | +18% |

| Alloy lead times | — | +15% |

What is included in the product

Peri-specific Porter's Five Forces analysis identifying competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and rivalry—highlighting disruptive trends, entry barriers, pricing influence, and strategic implications for Peri’s market positioning.

A concise one-sheet Porter's Five Forces snapshot that highlights competitive pressures, enables scenario toggles, and exports clean visuals for decks—turning complex strategic analysis into quick, actionable guidance for decision-makers.

Customers Bargaining Power

Large contractor concentration

Global EPCs and major contractors in 2024 run competitive tenders for multi-country programs worth billions, leveraging scale to demand discounts, strict SLAs and flexible rental terms; probe discounts commonly shift procurement margins and can compress supplier pricing power. Bundling multi-country volumes amplifies buyer leverage across regions. PERI offsets this by offering engineering value-add, bespoke solutions and a global support network to protect margins and retain contracts.

Rental vs. purchase optionality

Customers toggle between buying and renting based on project cycles, heightening price sensitivity and prompting tougher term negotiations. High-utilization periods force rate concessions as clients press for lower short-term costs. PERI mitigates this pressure through superior availability, high-quality fleet maintenance, and advanced project planning that secures longer-term contracts and reduces idle time.

Multi-sourcing to rivals

Clients can switch among PERI, Doka, ULMA, MEVA, Layher and others, and in 2024 comparable commodity systems continue to intensify price competition across projects. Approved vendor lists and standardized procurement mean substitution can occur within days to weeks, pressuring margins. Proprietary systems and tight design integration, however, lower churn by creating higher switching costs for complex projects.

Total cost of ownership focus

Buyers prioritize total cost of ownership, weighing setup speed, safety, reusability, and engineering support; 2024 case studies report up to 30% cycle-time reductions that often outweigh higher sticker prices. Data access, BIM integration, and on-site service materially lower perceived deployment risk and reduce buyer leverage. Weak proof points and sparse ROI evidence increase buyer negotiation power.

- setup speed

- safety & reusability

- engineering support

- up to 30% cycle-time savings (2024 case studies)

- BIM/data integration reduces perceived risk

Project-based demand volatility

Lumpy project awards give buyers timing leverage; large bids concentrated in quarters let clients demand concessions. During downturns contractors typically face rate reductions of 5–20% and payment terms extending from ~30 to 60–90 days. In booms availability outweighs price as utilizations often exceed 90%, and PERI’s fleet scale blunts but does not erase these buyer-power swings.

- Timing leverage: concentrated awards increase buyer bargaining

- Downturn impact: rate cuts 5–20% and payment terms to 60–90 days

- Boom dynamics: >90% utilization shifts power toward suppliers despite PERI’s fleet scale

Large EPC tenders compress supplier margins; booms restore supplier leverage

In 2024 large EPCs use billion-dollar multi-country tenders to extract discounts, strict SLAs and flexible rental terms, compressing supplier margins. Buyers switch among PERI, Doka, ULMA, MEVA and Layher within weeks, raising price sensitivity, though PERI’s engineering services and global support raise switching costs on complex jobs. Downturns drive 5–20% rate cuts and payment terms from ~30 to 60–90 days; booms (>90% utilization) shift leverage back to suppliers.

| Metric | 2024 value | Buyer impact |

|---|---|---|

| Tender size | Multi-country, $bn programs | High leverage |

| Rate cuts (downturn) | 5–20% | Margin compression |

| Payment terms | ~30 → 60–90 days | Cash flow pressure |

| Cycle-time savings | Up to 30% | Reduces price sensitivity |

| Utilization (booms) | >90% | Supplier leverage |

Same Document Delivered

Peri Porter's Five Forces Analysis

This Peri Porter's Five Forces analysis evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers to clarify industry dynamics. This preview is the exact document you'll receive upon purchase—fully formatted and ready to download. No mockups or samples: what you see is the final deliverable. Instant access after payment, ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Peri faces varied industry pressures—supplier bargaining, buyer demands, substitute threats, entrant risk, and rival rivalry—that shape margins and growth prospects. This snapshot highlights key friction points and strategic levers Peri can use to defend or expand its position. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals and actionable strategy.

Suppliers Bargaining Power

Commodity input exposure

PERI depends heavily on steel, aluminum and timber, exposing margins to commodity price volatility as input cost spikes allow suppliers to pass through increases rapidly. Hedging programs and multi-year supply contracts reduce short-term exposure but do not eliminate margin pressure during sharp commodity moves. Diversified global sourcing dilutes individual supplier leverage and supports procurement flexibility.

Specialized components

Custom extrusions, high-strength alloys and engineered connectors come from a narrow supplier base, concentrating bargaining power; certification and qualification typically take 6–12 months and can cost >$250,000, raising switching costs. In 2024 lead times for specialty alloys increased ~15% vs 2023, strengthening niche suppliers’ leverage. Dual-sourcing and in-house engineering can cut supplier dependency and mitigate risk.

Logistics and lead times

Bulky PERI systems need reliable freight, warehousing and JIT availability; sea freight lead times averaged ~45 days in 2023, amplifying supplier leverage when ports congest. Port disruptions in 2023–24 raised container delays and spot freight volatility, strengthening logistics providers’ bargaining power. PERI’s presence in 90+ countries and reported ~€1.9bn revenue in 2023, plus its owned fleet and regional hubs with inventory buffers, mitigate but do not eliminate spikes in logistics leverage.

Quality and safety standards

Strict compliance, traceability, and safety certifications limit acceptable suppliers, elevating supplier bargaining power; 2024 industry surveys reported ~62% of buyers requiring third-party safety certifications. Fewer qualified vendors can command better terms and price premia. Audits and supplier-development programs (used by ~74% of large buyers in 2024) broaden the pool, yet maintaining standards constrains rapid switching.

- Compliance limits supplier pool

- Audits & development expand options

- Fewer certified vendors = stronger supplier terms

ESG and regulatory constraints

- CSRD effective 2024: tighter disclosure

- Supplier ESG compliance increases negotiating leverage

- PERI scale eases access but cannot eliminate supply constraints

Supplier squeeze: steel +18%, alloy +15%, €1.9bn scale

PERI faces medium-high supplier power: commodity-driven inputs (steel +18% YoY in 2024) and specialty-alloy lead times +15% strengthen suppliers, while multi-year contracts, hedges and €1.9bn 2023 scale mitigate but do not eliminate risk.

| Metric | 2023 | 2024 |

|---|---|---|

| Revenue | €1.9bn | — |

| Steel price YoY | — | +18% |

| Alloy lead times | — | +15% |

What is included in the product

Peri-specific Porter's Five Forces analysis identifying competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and rivalry—highlighting disruptive trends, entry barriers, pricing influence, and strategic implications for Peri’s market positioning.

A concise one-sheet Porter's Five Forces snapshot that highlights competitive pressures, enables scenario toggles, and exports clean visuals for decks—turning complex strategic analysis into quick, actionable guidance for decision-makers.

Customers Bargaining Power

Large contractor concentration

Global EPCs and major contractors in 2024 run competitive tenders for multi-country programs worth billions, leveraging scale to demand discounts, strict SLAs and flexible rental terms; probe discounts commonly shift procurement margins and can compress supplier pricing power. Bundling multi-country volumes amplifies buyer leverage across regions. PERI offsets this by offering engineering value-add, bespoke solutions and a global support network to protect margins and retain contracts.

Rental vs. purchase optionality

Customers toggle between buying and renting based on project cycles, heightening price sensitivity and prompting tougher term negotiations. High-utilization periods force rate concessions as clients press for lower short-term costs. PERI mitigates this pressure through superior availability, high-quality fleet maintenance, and advanced project planning that secures longer-term contracts and reduces idle time.

Multi-sourcing to rivals

Clients can switch among PERI, Doka, ULMA, MEVA, Layher and others, and in 2024 comparable commodity systems continue to intensify price competition across projects. Approved vendor lists and standardized procurement mean substitution can occur within days to weeks, pressuring margins. Proprietary systems and tight design integration, however, lower churn by creating higher switching costs for complex projects.

Total cost of ownership focus

Buyers prioritize total cost of ownership, weighing setup speed, safety, reusability, and engineering support; 2024 case studies report up to 30% cycle-time reductions that often outweigh higher sticker prices. Data access, BIM integration, and on-site service materially lower perceived deployment risk and reduce buyer leverage. Weak proof points and sparse ROI evidence increase buyer negotiation power.

- setup speed

- safety & reusability

- engineering support

- up to 30% cycle-time savings (2024 case studies)

- BIM/data integration reduces perceived risk

Project-based demand volatility

Lumpy project awards give buyers timing leverage; large bids concentrated in quarters let clients demand concessions. During downturns contractors typically face rate reductions of 5–20% and payment terms extending from ~30 to 60–90 days. In booms availability outweighs price as utilizations often exceed 90%, and PERI’s fleet scale blunts but does not erase these buyer-power swings.

- Timing leverage: concentrated awards increase buyer bargaining

- Downturn impact: rate cuts 5–20% and payment terms to 60–90 days

- Boom dynamics: >90% utilization shifts power toward suppliers despite PERI’s fleet scale

Large EPC tenders compress supplier margins; booms restore supplier leverage

In 2024 large EPCs use billion-dollar multi-country tenders to extract discounts, strict SLAs and flexible rental terms, compressing supplier margins. Buyers switch among PERI, Doka, ULMA, MEVA and Layher within weeks, raising price sensitivity, though PERI’s engineering services and global support raise switching costs on complex jobs. Downturns drive 5–20% rate cuts and payment terms from ~30 to 60–90 days; booms (>90% utilization) shift leverage back to suppliers.

| Metric | 2024 value | Buyer impact |

|---|---|---|

| Tender size | Multi-country, $bn programs | High leverage |

| Rate cuts (downturn) | 5–20% | Margin compression |

| Payment terms | ~30 → 60–90 days | Cash flow pressure |

| Cycle-time savings | Up to 30% | Reduces price sensitivity |

| Utilization (booms) | >90% | Supplier leverage |

Same Document Delivered

Peri Porter's Five Forces Analysis

This Peri Porter's Five Forces analysis evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers to clarify industry dynamics. This preview is the exact document you'll receive upon purchase—fully formatted and ready to download. No mockups or samples: what you see is the final deliverable. Instant access after payment, ready for immediate use.