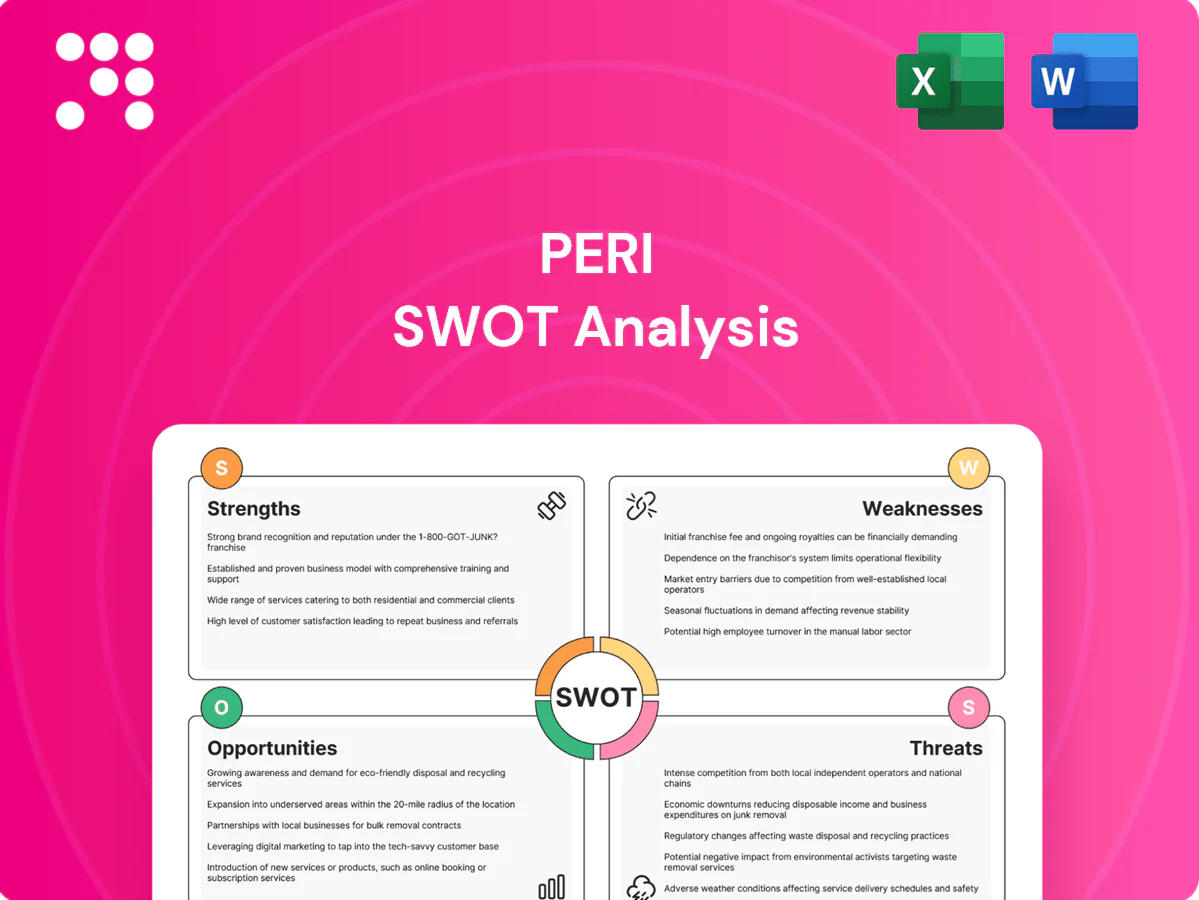

Peri SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Explore Peri’s strategic position with our concise SWOT preview—highlighting core strengths, market risks, and growth levers to inform your next move. Want the full, research-backed report with editable Word and Excel deliverables? Purchase the complete SWOT analysis to plan, pitch, or invest with confidence.

Strengths

Global brand and scale

PERI is a recognized leader in formwork and scaffolding across key construction markets and operates in over 60 countries with about 9,500 employees (2024). Its international footprint enables consistent service, rapid mobilization, and transfer of technical know‑how between projects. Global scale secures better procurement terms and equipment availability. This materially strengthens bid competitiveness and delivery reliability.

Diversified revenue model

Peri benefits from a diversified revenue model—product sales, rentals, and engineering services—that smooths cyclical demand and stabilizes cash flow. Rentals deliver recurring revenue and longer customer engagement, while engineering support increases value beyond hardware and raises switching costs. This mix enhances margin resilience and improves asset utilization across project cycles.

Engineering expertise and safety

Peri's engineering expertise—backed by a global footprint in over 60 countries and roughly 9,000 employees—optimizes concrete cycles and boosts labor productivity through modular design. Proven safety systems and training reduce jobsite risk and delays, de‑risking complex projects and making Peri a preferred partner for Tier‑1 contractors. This enables premium pricing and strong repeat business, supporting reported 2023 sales near €1.6bn.

Comprehensive solutions portfolio

Peri offers a full range of formwork, scaffolding, shoring and accessories covering residential projects to mega‑infrastructure, enabling project continuity across scales. System interoperability speeds setup and can cut assembly time by up to 30%, reducing on‑site errors. Standardized components materially lower total cost of ownership, often by ~15–20% versus bespoke solutions, while one‑stop coverage simplifies procurement and logistics.

- Coverage: end‑to‑end solutions for small to mega projects

- Efficiency: up to 30% faster setup

- Cost: ~15–20% lower TCO through standardization

- Procurement: single‑vendor sourcing reduces lead times

Track record on large projects

Peri's 50+ years of experience on bridges, tunnels, high‑rises and industrial plants validates operational reliability and constructability know‑how; client references tangibly reduce perceived tender risk and shorten decision cycles. Proven logistics and planning scale to tight timelines, supporting bids for complex, higher‑margin projects.

- 50+ years proven portfolio

- References lower client award risk

- Logistics scale to fast schedules

Global formwork & scaffolding leader: 60+ countries, €1.6bn sales, 30% faster setup

PERI is a global leader in formwork and scaffolding operating in 60+ countries with ~9,500 employees (2024) and 2023 sales ≈€1.6bn. Diversified revenue—product sales, rentals, engineering—drives recurring cash flow and higher utilization. Engineering and standardized systems cut assembly time up to 30% and lower TCO ~15–20%, supporting premium pricing and repeat business.

| Metric | Value |

|---|---|

| Countries | 60+ |

| Employees (2024) | ~9,500 |

| 2023 Sales | ≈€1.6bn |

| Setup time | Up to 30% faster |

| Estimated TCO reduction | ~15–20% |

What is included in the product

Provides a concise SWOT analysis of Peri’s internal capabilities and external market factors, highlighting strengths, weaknesses, opportunities, and threats that shape its strategic outlook and competitive position.

Provides a focused Peri SWOT matrix that pinpoints core pain points and recommended responses for rapid strategic alignment. Editable format enables swift updates to reflect shifting priorities and accelerate stakeholder buy-in.

Weaknesses

Exposure to construction cycles

Revenue is closely tied to new-build and infrastructure activity, so downturns or funding pauses can quickly reduce Peri utilization and sales. EU construction output contracted in 2023 and IMF/WB forecasts showed only tepid recovery into 2024, making regional slumps hard to offset despite Peri's global reach. Cash flows can become volatile during macro stress as project delays and payment timing shift.

Capital‑intensive rental fleet

Maintaining and refreshing large fleets ties up capital and can represent over 30% of a rental firm's asset base. Idle equipment and depreciation squeeze margins during slow construction cycles, eroding EBITDA. Logistics and maintenance add fixed costs, so asset turns must exceed roughly 1.5–2.0x annually to sustain returns.

Price competition and commoditization

Basic formwork and scaffolding face low‑cost rivals as commoditization rises; in construction, global output exceeded USD 11 trillion in 2023, fueling price‑centric supply chains. Tendering often prioritizes lowest price over differentiation, pushing providers to bid aggressively. Discounting has eroded margins in certain segments and regions, sometimes by double‑digit percentage points. Clear value communication and lifecycle‑cost arguments are needed to offset lowest‑bid dynamics.

Project execution risk

Project execution risk: design‑to‑deliver lead times and changing site conditions frequently shift mid‑project, driving misestimates that trigger change orders, delays and cost overruns; Flyvbjerg et al. report median cost overruns around 28% on large projects. HSE incidents remain disruptive—OSHA notes the construction Fatal Four cause roughly half of industry deaths—while complex logistics amplify coordination risk.

- Design changes → change orders, delays, cost overruns (~28% median)

- Site condition volatility → schedule slippage

- HSE incidents → operational stoppages (Fatal Four ≈50% of deaths)

- Complex logistics → higher coordination failure risk

Dependence on skilled engineers

Specialist design and site support drive Peri’s value proposition, but dependency on skilled engineers exposes delivery risk; ManpowerGroup’s 2024 Talent Shortage Survey found 69% of employers struggle to fill technical roles, amplifying recruitment pressure.

High training lead times—commonly 6–12 months for field engineers—plus attrition impede capacity growth, while sector wage inflation (notably elevated in 2023–24) raises operating costs and margin pressure.

- Talent shortage: ManpowerGroup 2024 — 69% difficulty filling technical roles

- Training lead time: 6–12 months for field engineers

- Attrition limits scalability and service quality

- Wage inflation in 2023–24 increased operating cost pressure

Construction cyclicality: global market >USD 11tn; fleets > 30%; turns > 1.5–2.0x

Peri is cyclical—revenue tied to new builds; EU 2023 contraction and global construction >USD11tn (2023) risk utilization and cash flow volatility. Large fleets consume >30% of rental assets; idle kit and depreciation cut EBITDA unless asset turns exceed ~1.5–2.0x. Commoditization pressures margins; tendering drove double‑digit margin erosion in some regions. Skilled‑staff gaps (Manpower 2024: 69%) and 6–12m training slow scaling.

| Metric | Value |

|---|---|

| Global construction 2023 | USD 11+ tn |

| Fleet share of assets | >30% |

| Required asset turns | 1.5–2.0x |

| Median cost overrun | ~28% |

| Technical hiring difficulty | 69% (Manpower 2024) |

| Training lead time | 6–12 months |

Preview Before You Purchase

Peri SWOT Analysis

This is the actual Peri SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete structure and findings. Purchase unlocks the full, editable version ready for download.

Go Beyond the Preview—Access the Full Strategic Report

Explore Peri’s strategic position with our concise SWOT preview—highlighting core strengths, market risks, and growth levers to inform your next move. Want the full, research-backed report with editable Word and Excel deliverables? Purchase the complete SWOT analysis to plan, pitch, or invest with confidence.

Strengths

Global brand and scale

PERI is a recognized leader in formwork and scaffolding across key construction markets and operates in over 60 countries with about 9,500 employees (2024). Its international footprint enables consistent service, rapid mobilization, and transfer of technical know‑how between projects. Global scale secures better procurement terms and equipment availability. This materially strengthens bid competitiveness and delivery reliability.

Diversified revenue model

Peri benefits from a diversified revenue model—product sales, rentals, and engineering services—that smooths cyclical demand and stabilizes cash flow. Rentals deliver recurring revenue and longer customer engagement, while engineering support increases value beyond hardware and raises switching costs. This mix enhances margin resilience and improves asset utilization across project cycles.

Engineering expertise and safety

Peri's engineering expertise—backed by a global footprint in over 60 countries and roughly 9,000 employees—optimizes concrete cycles and boosts labor productivity through modular design. Proven safety systems and training reduce jobsite risk and delays, de‑risking complex projects and making Peri a preferred partner for Tier‑1 contractors. This enables premium pricing and strong repeat business, supporting reported 2023 sales near €1.6bn.

Comprehensive solutions portfolio

Peri offers a full range of formwork, scaffolding, shoring and accessories covering residential projects to mega‑infrastructure, enabling project continuity across scales. System interoperability speeds setup and can cut assembly time by up to 30%, reducing on‑site errors. Standardized components materially lower total cost of ownership, often by ~15–20% versus bespoke solutions, while one‑stop coverage simplifies procurement and logistics.

- Coverage: end‑to‑end solutions for small to mega projects

- Efficiency: up to 30% faster setup

- Cost: ~15–20% lower TCO through standardization

- Procurement: single‑vendor sourcing reduces lead times

Track record on large projects

Peri's 50+ years of experience on bridges, tunnels, high‑rises and industrial plants validates operational reliability and constructability know‑how; client references tangibly reduce perceived tender risk and shorten decision cycles. Proven logistics and planning scale to tight timelines, supporting bids for complex, higher‑margin projects.

- 50+ years proven portfolio

- References lower client award risk

- Logistics scale to fast schedules

Global formwork & scaffolding leader: 60+ countries, €1.6bn sales, 30% faster setup

PERI is a global leader in formwork and scaffolding operating in 60+ countries with ~9,500 employees (2024) and 2023 sales ≈€1.6bn. Diversified revenue—product sales, rentals, engineering—drives recurring cash flow and higher utilization. Engineering and standardized systems cut assembly time up to 30% and lower TCO ~15–20%, supporting premium pricing and repeat business.

| Metric | Value |

|---|---|

| Countries | 60+ |

| Employees (2024) | ~9,500 |

| 2023 Sales | ≈€1.6bn |

| Setup time | Up to 30% faster |

| Estimated TCO reduction | ~15–20% |

What is included in the product

Provides a concise SWOT analysis of Peri’s internal capabilities and external market factors, highlighting strengths, weaknesses, opportunities, and threats that shape its strategic outlook and competitive position.

Provides a focused Peri SWOT matrix that pinpoints core pain points and recommended responses for rapid strategic alignment. Editable format enables swift updates to reflect shifting priorities and accelerate stakeholder buy-in.

Weaknesses

Exposure to construction cycles

Revenue is closely tied to new-build and infrastructure activity, so downturns or funding pauses can quickly reduce Peri utilization and sales. EU construction output contracted in 2023 and IMF/WB forecasts showed only tepid recovery into 2024, making regional slumps hard to offset despite Peri's global reach. Cash flows can become volatile during macro stress as project delays and payment timing shift.

Capital‑intensive rental fleet

Maintaining and refreshing large fleets ties up capital and can represent over 30% of a rental firm's asset base. Idle equipment and depreciation squeeze margins during slow construction cycles, eroding EBITDA. Logistics and maintenance add fixed costs, so asset turns must exceed roughly 1.5–2.0x annually to sustain returns.

Price competition and commoditization

Basic formwork and scaffolding face low‑cost rivals as commoditization rises; in construction, global output exceeded USD 11 trillion in 2023, fueling price‑centric supply chains. Tendering often prioritizes lowest price over differentiation, pushing providers to bid aggressively. Discounting has eroded margins in certain segments and regions, sometimes by double‑digit percentage points. Clear value communication and lifecycle‑cost arguments are needed to offset lowest‑bid dynamics.

Project execution risk

Project execution risk: design‑to‑deliver lead times and changing site conditions frequently shift mid‑project, driving misestimates that trigger change orders, delays and cost overruns; Flyvbjerg et al. report median cost overruns around 28% on large projects. HSE incidents remain disruptive—OSHA notes the construction Fatal Four cause roughly half of industry deaths—while complex logistics amplify coordination risk.

- Design changes → change orders, delays, cost overruns (~28% median)

- Site condition volatility → schedule slippage

- HSE incidents → operational stoppages (Fatal Four ≈50% of deaths)

- Complex logistics → higher coordination failure risk

Dependence on skilled engineers

Specialist design and site support drive Peri’s value proposition, but dependency on skilled engineers exposes delivery risk; ManpowerGroup’s 2024 Talent Shortage Survey found 69% of employers struggle to fill technical roles, amplifying recruitment pressure.

High training lead times—commonly 6–12 months for field engineers—plus attrition impede capacity growth, while sector wage inflation (notably elevated in 2023–24) raises operating costs and margin pressure.

- Talent shortage: ManpowerGroup 2024 — 69% difficulty filling technical roles

- Training lead time: 6–12 months for field engineers

- Attrition limits scalability and service quality

- Wage inflation in 2023–24 increased operating cost pressure

Construction cyclicality: global market >USD 11tn; fleets > 30%; turns > 1.5–2.0x

Peri is cyclical—revenue tied to new builds; EU 2023 contraction and global construction >USD11tn (2023) risk utilization and cash flow volatility. Large fleets consume >30% of rental assets; idle kit and depreciation cut EBITDA unless asset turns exceed ~1.5–2.0x. Commoditization pressures margins; tendering drove double‑digit margin erosion in some regions. Skilled‑staff gaps (Manpower 2024: 69%) and 6–12m training slow scaling.

| Metric | Value |

|---|---|

| Global construction 2023 | USD 11+ tn |

| Fleet share of assets | >30% |

| Required asset turns | 1.5–2.0x |

| Median cost overrun | ~28% |

| Technical hiring difficulty | 69% (Manpower 2024) |

| Training lead time | 6–12 months |

Preview Before You Purchase

Peri SWOT Analysis

This is the actual Peri SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete structure and findings. Purchase unlocks the full, editable version ready for download.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Explore Peri’s strategic position with our concise SWOT preview—highlighting core strengths, market risks, and growth levers to inform your next move. Want the full, research-backed report with editable Word and Excel deliverables? Purchase the complete SWOT analysis to plan, pitch, or invest with confidence.

Strengths

Global brand and scale

PERI is a recognized leader in formwork and scaffolding across key construction markets and operates in over 60 countries with about 9,500 employees (2024). Its international footprint enables consistent service, rapid mobilization, and transfer of technical know‑how between projects. Global scale secures better procurement terms and equipment availability. This materially strengthens bid competitiveness and delivery reliability.

Diversified revenue model

Peri benefits from a diversified revenue model—product sales, rentals, and engineering services—that smooths cyclical demand and stabilizes cash flow. Rentals deliver recurring revenue and longer customer engagement, while engineering support increases value beyond hardware and raises switching costs. This mix enhances margin resilience and improves asset utilization across project cycles.

Engineering expertise and safety

Peri's engineering expertise—backed by a global footprint in over 60 countries and roughly 9,000 employees—optimizes concrete cycles and boosts labor productivity through modular design. Proven safety systems and training reduce jobsite risk and delays, de‑risking complex projects and making Peri a preferred partner for Tier‑1 contractors. This enables premium pricing and strong repeat business, supporting reported 2023 sales near €1.6bn.

Comprehensive solutions portfolio

Peri offers a full range of formwork, scaffolding, shoring and accessories covering residential projects to mega‑infrastructure, enabling project continuity across scales. System interoperability speeds setup and can cut assembly time by up to 30%, reducing on‑site errors. Standardized components materially lower total cost of ownership, often by ~15–20% versus bespoke solutions, while one‑stop coverage simplifies procurement and logistics.

- Coverage: end‑to‑end solutions for small to mega projects

- Efficiency: up to 30% faster setup

- Cost: ~15–20% lower TCO through standardization

- Procurement: single‑vendor sourcing reduces lead times

Track record on large projects

Peri's 50+ years of experience on bridges, tunnels, high‑rises and industrial plants validates operational reliability and constructability know‑how; client references tangibly reduce perceived tender risk and shorten decision cycles. Proven logistics and planning scale to tight timelines, supporting bids for complex, higher‑margin projects.

- 50+ years proven portfolio

- References lower client award risk

- Logistics scale to fast schedules

Global formwork & scaffolding leader: 60+ countries, €1.6bn sales, 30% faster setup

PERI is a global leader in formwork and scaffolding operating in 60+ countries with ~9,500 employees (2024) and 2023 sales ≈€1.6bn. Diversified revenue—product sales, rentals, engineering—drives recurring cash flow and higher utilization. Engineering and standardized systems cut assembly time up to 30% and lower TCO ~15–20%, supporting premium pricing and repeat business.

| Metric | Value |

|---|---|

| Countries | 60+ |

| Employees (2024) | ~9,500 |

| 2023 Sales | ≈€1.6bn |

| Setup time | Up to 30% faster |

| Estimated TCO reduction | ~15–20% |

What is included in the product

Provides a concise SWOT analysis of Peri’s internal capabilities and external market factors, highlighting strengths, weaknesses, opportunities, and threats that shape its strategic outlook and competitive position.

Provides a focused Peri SWOT matrix that pinpoints core pain points and recommended responses for rapid strategic alignment. Editable format enables swift updates to reflect shifting priorities and accelerate stakeholder buy-in.

Weaknesses

Exposure to construction cycles

Revenue is closely tied to new-build and infrastructure activity, so downturns or funding pauses can quickly reduce Peri utilization and sales. EU construction output contracted in 2023 and IMF/WB forecasts showed only tepid recovery into 2024, making regional slumps hard to offset despite Peri's global reach. Cash flows can become volatile during macro stress as project delays and payment timing shift.

Capital‑intensive rental fleet

Maintaining and refreshing large fleets ties up capital and can represent over 30% of a rental firm's asset base. Idle equipment and depreciation squeeze margins during slow construction cycles, eroding EBITDA. Logistics and maintenance add fixed costs, so asset turns must exceed roughly 1.5–2.0x annually to sustain returns.

Price competition and commoditization

Basic formwork and scaffolding face low‑cost rivals as commoditization rises; in construction, global output exceeded USD 11 trillion in 2023, fueling price‑centric supply chains. Tendering often prioritizes lowest price over differentiation, pushing providers to bid aggressively. Discounting has eroded margins in certain segments and regions, sometimes by double‑digit percentage points. Clear value communication and lifecycle‑cost arguments are needed to offset lowest‑bid dynamics.

Project execution risk

Project execution risk: design‑to‑deliver lead times and changing site conditions frequently shift mid‑project, driving misestimates that trigger change orders, delays and cost overruns; Flyvbjerg et al. report median cost overruns around 28% on large projects. HSE incidents remain disruptive—OSHA notes the construction Fatal Four cause roughly half of industry deaths—while complex logistics amplify coordination risk.

- Design changes → change orders, delays, cost overruns (~28% median)

- Site condition volatility → schedule slippage

- HSE incidents → operational stoppages (Fatal Four ≈50% of deaths)

- Complex logistics → higher coordination failure risk

Dependence on skilled engineers

Specialist design and site support drive Peri’s value proposition, but dependency on skilled engineers exposes delivery risk; ManpowerGroup’s 2024 Talent Shortage Survey found 69% of employers struggle to fill technical roles, amplifying recruitment pressure.

High training lead times—commonly 6–12 months for field engineers—plus attrition impede capacity growth, while sector wage inflation (notably elevated in 2023–24) raises operating costs and margin pressure.

- Talent shortage: ManpowerGroup 2024 — 69% difficulty filling technical roles

- Training lead time: 6–12 months for field engineers

- Attrition limits scalability and service quality

- Wage inflation in 2023–24 increased operating cost pressure

Construction cyclicality: global market >USD 11tn; fleets > 30%; turns > 1.5–2.0x

Peri is cyclical—revenue tied to new builds; EU 2023 contraction and global construction >USD11tn (2023) risk utilization and cash flow volatility. Large fleets consume >30% of rental assets; idle kit and depreciation cut EBITDA unless asset turns exceed ~1.5–2.0x. Commoditization pressures margins; tendering drove double‑digit margin erosion in some regions. Skilled‑staff gaps (Manpower 2024: 69%) and 6–12m training slow scaling.

| Metric | Value |

|---|---|

| Global construction 2023 | USD 11+ tn |

| Fleet share of assets | >30% |

| Required asset turns | 1.5–2.0x |

| Median cost overrun | ~28% |

| Technical hiring difficulty | 69% (Manpower 2024) |

| Training lead time | 6–12 months |

Preview Before You Purchase

Peri SWOT Analysis

This is the actual Peri SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete structure and findings. Purchase unlocks the full, editable version ready for download.