Persan SA Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Persan SA faces moderate supplier power, niche buyer segments, and evolving substitute threats that collectively shape its competitive stance. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Persan SA’s market pressures and strategic advantages in detail. Ready to move beyond the basics? Get the complete report now.

Suppliers Bargaining Power

Commodity chemical dependence

Core inputs like surfactants, enzymes, solvents and fragrances are sourced from large global chemical producers, tying Persán to a chemicals market where feedstock costs follow Brent crude (about $85/bbl in 2024) and palm/energy-linked commodity cycles. These cycles—with oil and palm price volatility—can compress margins; dual-sourcing lowers exposure but sudden spikes or shortages raise supplier leverage. Long-term contracts and hedging reduce but do not eliminate this input risk.

Specialty input concentration

Unique enzymes, biodegradable polymers and high-performance actives are concentrated among a few leaders (eg Novozymes, DSM), with the global specialty enzymes market ~USD 7.4B in 2024, limiting alternatives and raising switching costs and technical validation time (often 6–12 months). That concentration gives suppliers measurable pricing power on differentiated components, while co-development partnerships can trade lower price for prioritized innovation access.

Packaging and sustainability specs

Recycled plastics, paper-based and eco-label materials shrink the supplier pool; 2024 rPET feedstock tightness pushed premiums roughly 20%, raising input costs and qualification hurdles for Persan SA. Dependence on certified mills increases as 68% of EU buyers in 2024 prioritized eco-compliant suppliers. Long-term offtake deals secure volumes but can lock in higher margins and rigid terms.

Logistics and energy cost pass-through

Transport, warehousing and energy are material cost drivers for detergents; in Europe suppliers pass through spikes rapidly. Persán’s proximity to markets and process efficiency limit logistics spend but exposure remains given container freight and fuel volatility (container rates ~USD 2,000/FEU in 2024, EU diesel ~€1.60/l, industrial electricity ~€0.15/kWh in 2024). Onsite energy optimization eases but cannot offset systemic shocks.

- High pass-through: rapid supplier price adjustments in Europe

- 2024 markers: ~USD 2,000/FEU, €1.60/l diesel, €0.15/kWh electricity

- Persán mitigants: efficiency, proximity, onsite energy limits but residual exposure

Switching and formulation rigidity

Changing a critical ingredient forces reformulation, lab testing and regulatory re-approval, creating time and cost frictions that in 2024 left 72% of formulators reporting validation times over 3 months and average extra costs cited as six-figure impacts, favoring incumbent suppliers; high-volume SKUs face performance-drift risks that discourage frequent switches.

Supplier concentration boosts pricing; feedstock tracks Brent ~USD85/bbl

Supplier concentration on specialty actives and recycled inputs gives measurable pricing power; feedstock costs track Brent (~$85/bbl in 2024) and palm cycles, raising volatility; logistics/energy pass-through (container ~USD2,000/FEU, diesel €1.60/l, electricity €0.15/kWh) increases leverage; mitigants: dual-sourcing, hedging, long-term contracts and co-development.

| Item | 2024 metric | Impact |

|---|---|---|

| Brent | ~USD85/bbl | Feedstock-driven margin pressure |

| Specialty enzymes | Market USD7.4B | High switching cost |

| rPET premium | +20% | Input cost spike |

| Container | ~USD2,000/FEU | Logistics pass-through |

| Validation time | >3 months | Switching friction |

What is included in the product

Uncovers key drivers of competition for Persan SA—assessing supplier and buyer power, threat of new entrants, substitutes, and industry rivalry to reveal pricing, profitability, and market-entry risks. Tailored strategic insights identify disruptive threats and protective barriers for decision-making and investor materials.

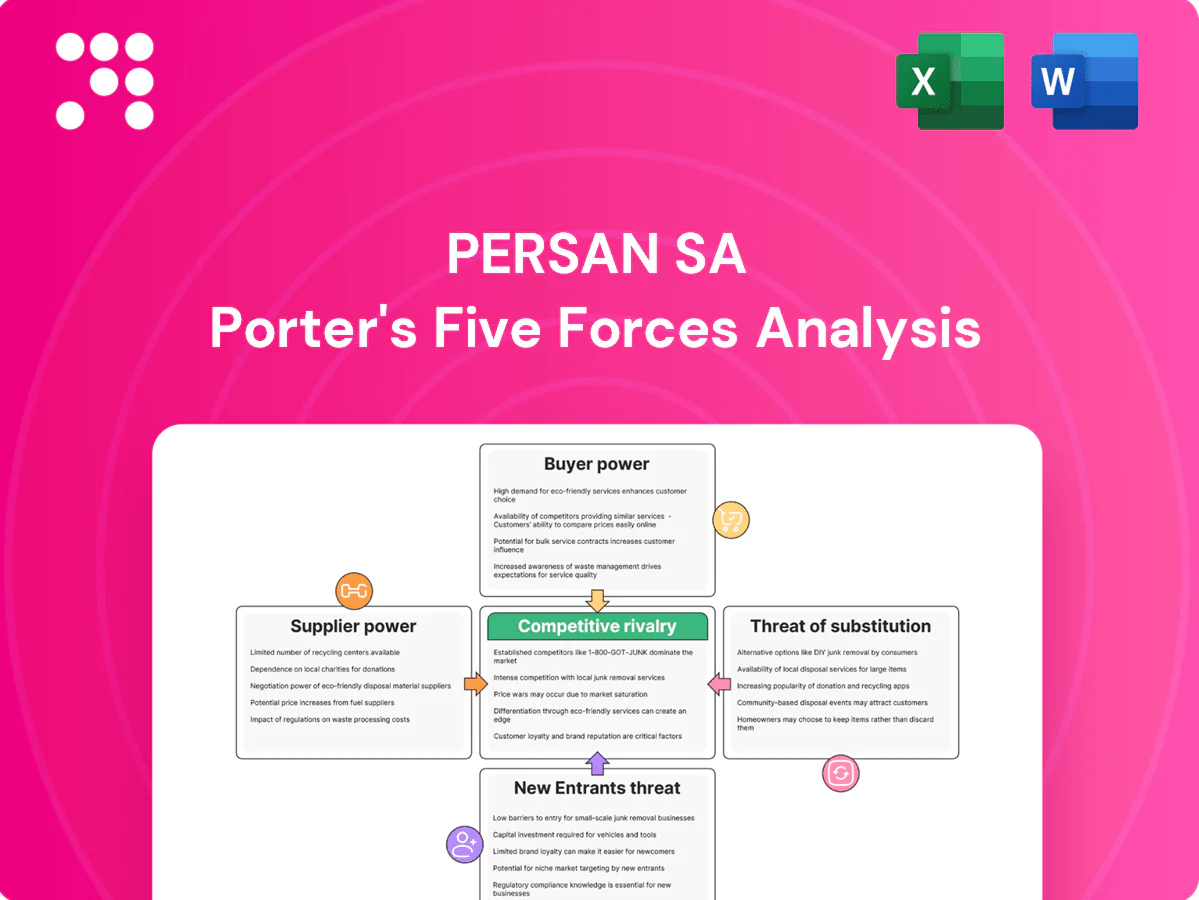

Clear one-sheet Porter's Five Forces for Persan SA—quickly pinpoint competitive pressure and relieve decision paralysis with a radar chart and customizable pressure levels for scenario testing.

Customers Bargaining Power

Retail giants and private labels

European hypermarkets and discounters (Aldi+Lidl ~13% EU grocery share in 2024) exert strong negotiating power and push private-label sourcing, forcing Persán into tight price talks.

Price cuts, slotting and promotional allowances—which can consume double-digit percentages of shelf supplier margin—intensify pressure on Persán’s margins.

Persán’s private-label capability secures volumes but at low pricing; maintaining scale and service levels is essential to preserve shelf presence.

High price sensitivity

Household cleaning is a frequent, low-involvement purchase with elastic demand; during 2022–24 inflation waves consumers increasingly traded down, lifting private-label penetration to roughly 30% in some EU markets in 2024 and pushing promotion incidence near 40%, which strengthens retailer leverage. Performance and eco-claims can differentiate Persan SA, but such claims are rapidly imitated, limiting pricing power.

B2B contract concentration

Large B2B contracts with key chains or multinational distributors drive volume dependence—Walmart alone recorded roughly 611 billion USD in net sales in FY2024, illustrating buyer scale and leverage over suppliers. Renewal cycles become critical negotiation points where price, terms and lead times are reset. Buyers increasingly press for bespoke specs and rapid innovation at minimal incremental cost, so diversifying geographies and channels reduces single-buyer risk.

Digital channel transparency

E-commerce transparency (global online retail ~22.3% of sales in 2024) makes price and review visibility pervasive, enabling easy comparison and shrinking room for premium pricing for Persan SA.

Private labels and challenger brands, growing share in grocery and apparel channels, use targeted ads to undercut prices and capture margin-sensitive buyers.

Retailers using data-driven assortments and dynamic pricing increase buyer power, compressing Persan SA margins absent strong brand equity.

- e-commerce-share-2024: 22.3%

- reviews-influence-high: >90% buyers

- private-label-pressure: rising share in grocery/apparel

- retailer-data-dynamic-pricing

ESG and compliance demands

Retailers impose stringent sustainability, traceability and packaging requirements that raise supplier costs and narrow sourcing options, giving buyers stronger leverage in price and terms. Compliance often becomes a market-access ticket—EU CSRD extended reporting to roughly 50,000 companies in 2024—shifting value capture toward retailers. Certifications and lifecycle metrics are now table stakes, compressing supplier margins.

- Increased supplier costs and fewer sourcing options

- Compliance = market access (CSRD ~50,000 firms in 2024)

- Certifications and LCA metrics are mandatory

Discounters, private-labels and promos compress margins as e-commerce 22.3%

European hypermarkets and discounters (Aldi+Lidl ~13% EU grocery share in 2024) and large chains (Walmart net sales ~611bn USD FY2024) drive strong buyer leverage, pushing private-label sourcing and deep promo/slotting discounts. Private-label penetration reached ~30% in some EU markets in 2024 and promotion incidence neared 40%, compressing Persán margins. E-commerce (22.3% of retail sales 2024) and reviews (>90% influence) further reduce pricing power.

| Metric | 2024 Value | Implication |

|---|---|---|

| Discounters share (EU) | ~13% | Higher private-label pressure |

| Private-label penetration | ~30% (some markets) | Lower ASPs |

| Promo incidence | ~40% | Margin erosion |

| E-commerce | 22.3% | Price transparency |

Same Document Delivered

Persan SA Porter's Five Forces Analysis

This preview shows the exact Persan SA Porter’s Five Forces analysis you’ll receive upon purchase—no placeholders or samples. The file is the complete, professionally formatted document, ready for immediate download and use. What you see here is precisely the deliverable accessible instantly after payment.

Go Beyond the Preview—Access the Full Strategic Report

Persan SA faces moderate supplier power, niche buyer segments, and evolving substitute threats that collectively shape its competitive stance. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Persan SA’s market pressures and strategic advantages in detail. Ready to move beyond the basics? Get the complete report now.

Suppliers Bargaining Power

Commodity chemical dependence

Core inputs like surfactants, enzymes, solvents and fragrances are sourced from large global chemical producers, tying Persán to a chemicals market where feedstock costs follow Brent crude (about $85/bbl in 2024) and palm/energy-linked commodity cycles. These cycles—with oil and palm price volatility—can compress margins; dual-sourcing lowers exposure but sudden spikes or shortages raise supplier leverage. Long-term contracts and hedging reduce but do not eliminate this input risk.

Specialty input concentration

Unique enzymes, biodegradable polymers and high-performance actives are concentrated among a few leaders (eg Novozymes, DSM), with the global specialty enzymes market ~USD 7.4B in 2024, limiting alternatives and raising switching costs and technical validation time (often 6–12 months). That concentration gives suppliers measurable pricing power on differentiated components, while co-development partnerships can trade lower price for prioritized innovation access.

Packaging and sustainability specs

Recycled plastics, paper-based and eco-label materials shrink the supplier pool; 2024 rPET feedstock tightness pushed premiums roughly 20%, raising input costs and qualification hurdles for Persan SA. Dependence on certified mills increases as 68% of EU buyers in 2024 prioritized eco-compliant suppliers. Long-term offtake deals secure volumes but can lock in higher margins and rigid terms.

Logistics and energy cost pass-through

Transport, warehousing and energy are material cost drivers for detergents; in Europe suppliers pass through spikes rapidly. Persán’s proximity to markets and process efficiency limit logistics spend but exposure remains given container freight and fuel volatility (container rates ~USD 2,000/FEU in 2024, EU diesel ~€1.60/l, industrial electricity ~€0.15/kWh in 2024). Onsite energy optimization eases but cannot offset systemic shocks.

- High pass-through: rapid supplier price adjustments in Europe

- 2024 markers: ~USD 2,000/FEU, €1.60/l diesel, €0.15/kWh electricity

- Persán mitigants: efficiency, proximity, onsite energy limits but residual exposure

Switching and formulation rigidity

Changing a critical ingredient forces reformulation, lab testing and regulatory re-approval, creating time and cost frictions that in 2024 left 72% of formulators reporting validation times over 3 months and average extra costs cited as six-figure impacts, favoring incumbent suppliers; high-volume SKUs face performance-drift risks that discourage frequent switches.

Supplier concentration boosts pricing; feedstock tracks Brent ~USD85/bbl

Supplier concentration on specialty actives and recycled inputs gives measurable pricing power; feedstock costs track Brent (~$85/bbl in 2024) and palm cycles, raising volatility; logistics/energy pass-through (container ~USD2,000/FEU, diesel €1.60/l, electricity €0.15/kWh) increases leverage; mitigants: dual-sourcing, hedging, long-term contracts and co-development.

| Item | 2024 metric | Impact |

|---|---|---|

| Brent | ~USD85/bbl | Feedstock-driven margin pressure |

| Specialty enzymes | Market USD7.4B | High switching cost |

| rPET premium | +20% | Input cost spike |

| Container | ~USD2,000/FEU | Logistics pass-through |

| Validation time | >3 months | Switching friction |

What is included in the product

Uncovers key drivers of competition for Persan SA—assessing supplier and buyer power, threat of new entrants, substitutes, and industry rivalry to reveal pricing, profitability, and market-entry risks. Tailored strategic insights identify disruptive threats and protective barriers for decision-making and investor materials.

Clear one-sheet Porter's Five Forces for Persan SA—quickly pinpoint competitive pressure and relieve decision paralysis with a radar chart and customizable pressure levels for scenario testing.

Customers Bargaining Power

Retail giants and private labels

European hypermarkets and discounters (Aldi+Lidl ~13% EU grocery share in 2024) exert strong negotiating power and push private-label sourcing, forcing Persán into tight price talks.

Price cuts, slotting and promotional allowances—which can consume double-digit percentages of shelf supplier margin—intensify pressure on Persán’s margins.

Persán’s private-label capability secures volumes but at low pricing; maintaining scale and service levels is essential to preserve shelf presence.

High price sensitivity

Household cleaning is a frequent, low-involvement purchase with elastic demand; during 2022–24 inflation waves consumers increasingly traded down, lifting private-label penetration to roughly 30% in some EU markets in 2024 and pushing promotion incidence near 40%, which strengthens retailer leverage. Performance and eco-claims can differentiate Persan SA, but such claims are rapidly imitated, limiting pricing power.

B2B contract concentration

Large B2B contracts with key chains or multinational distributors drive volume dependence—Walmart alone recorded roughly 611 billion USD in net sales in FY2024, illustrating buyer scale and leverage over suppliers. Renewal cycles become critical negotiation points where price, terms and lead times are reset. Buyers increasingly press for bespoke specs and rapid innovation at minimal incremental cost, so diversifying geographies and channels reduces single-buyer risk.

Digital channel transparency

E-commerce transparency (global online retail ~22.3% of sales in 2024) makes price and review visibility pervasive, enabling easy comparison and shrinking room for premium pricing for Persan SA.

Private labels and challenger brands, growing share in grocery and apparel channels, use targeted ads to undercut prices and capture margin-sensitive buyers.

Retailers using data-driven assortments and dynamic pricing increase buyer power, compressing Persan SA margins absent strong brand equity.

- e-commerce-share-2024: 22.3%

- reviews-influence-high: >90% buyers

- private-label-pressure: rising share in grocery/apparel

- retailer-data-dynamic-pricing

ESG and compliance demands

Retailers impose stringent sustainability, traceability and packaging requirements that raise supplier costs and narrow sourcing options, giving buyers stronger leverage in price and terms. Compliance often becomes a market-access ticket—EU CSRD extended reporting to roughly 50,000 companies in 2024—shifting value capture toward retailers. Certifications and lifecycle metrics are now table stakes, compressing supplier margins.

- Increased supplier costs and fewer sourcing options

- Compliance = market access (CSRD ~50,000 firms in 2024)

- Certifications and LCA metrics are mandatory

Discounters, private-labels and promos compress margins as e-commerce 22.3%

European hypermarkets and discounters (Aldi+Lidl ~13% EU grocery share in 2024) and large chains (Walmart net sales ~611bn USD FY2024) drive strong buyer leverage, pushing private-label sourcing and deep promo/slotting discounts. Private-label penetration reached ~30% in some EU markets in 2024 and promotion incidence neared 40%, compressing Persán margins. E-commerce (22.3% of retail sales 2024) and reviews (>90% influence) further reduce pricing power.

| Metric | 2024 Value | Implication |

|---|---|---|

| Discounters share (EU) | ~13% | Higher private-label pressure |

| Private-label penetration | ~30% (some markets) | Lower ASPs |

| Promo incidence | ~40% | Margin erosion |

| E-commerce | 22.3% | Price transparency |

Same Document Delivered

Persan SA Porter's Five Forces Analysis

This preview shows the exact Persan SA Porter’s Five Forces analysis you’ll receive upon purchase—no placeholders or samples. The file is the complete, professionally formatted document, ready for immediate download and use. What you see here is precisely the deliverable accessible instantly after payment.

Description

Go Beyond the Preview—Access the Full Strategic Report

Persan SA faces moderate supplier power, niche buyer segments, and evolving substitute threats that collectively shape its competitive stance. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Persan SA’s market pressures and strategic advantages in detail. Ready to move beyond the basics? Get the complete report now.

Suppliers Bargaining Power

Commodity chemical dependence

Core inputs like surfactants, enzymes, solvents and fragrances are sourced from large global chemical producers, tying Persán to a chemicals market where feedstock costs follow Brent crude (about $85/bbl in 2024) and palm/energy-linked commodity cycles. These cycles—with oil and palm price volatility—can compress margins; dual-sourcing lowers exposure but sudden spikes or shortages raise supplier leverage. Long-term contracts and hedging reduce but do not eliminate this input risk.

Specialty input concentration

Unique enzymes, biodegradable polymers and high-performance actives are concentrated among a few leaders (eg Novozymes, DSM), with the global specialty enzymes market ~USD 7.4B in 2024, limiting alternatives and raising switching costs and technical validation time (often 6–12 months). That concentration gives suppliers measurable pricing power on differentiated components, while co-development partnerships can trade lower price for prioritized innovation access.

Packaging and sustainability specs

Recycled plastics, paper-based and eco-label materials shrink the supplier pool; 2024 rPET feedstock tightness pushed premiums roughly 20%, raising input costs and qualification hurdles for Persan SA. Dependence on certified mills increases as 68% of EU buyers in 2024 prioritized eco-compliant suppliers. Long-term offtake deals secure volumes but can lock in higher margins and rigid terms.

Logistics and energy cost pass-through

Transport, warehousing and energy are material cost drivers for detergents; in Europe suppliers pass through spikes rapidly. Persán’s proximity to markets and process efficiency limit logistics spend but exposure remains given container freight and fuel volatility (container rates ~USD 2,000/FEU in 2024, EU diesel ~€1.60/l, industrial electricity ~€0.15/kWh in 2024). Onsite energy optimization eases but cannot offset systemic shocks.

- High pass-through: rapid supplier price adjustments in Europe

- 2024 markers: ~USD 2,000/FEU, €1.60/l diesel, €0.15/kWh electricity

- Persán mitigants: efficiency, proximity, onsite energy limits but residual exposure

Switching and formulation rigidity

Changing a critical ingredient forces reformulation, lab testing and regulatory re-approval, creating time and cost frictions that in 2024 left 72% of formulators reporting validation times over 3 months and average extra costs cited as six-figure impacts, favoring incumbent suppliers; high-volume SKUs face performance-drift risks that discourage frequent switches.

Supplier concentration boosts pricing; feedstock tracks Brent ~USD85/bbl

Supplier concentration on specialty actives and recycled inputs gives measurable pricing power; feedstock costs track Brent (~$85/bbl in 2024) and palm cycles, raising volatility; logistics/energy pass-through (container ~USD2,000/FEU, diesel €1.60/l, electricity €0.15/kWh) increases leverage; mitigants: dual-sourcing, hedging, long-term contracts and co-development.

| Item | 2024 metric | Impact |

|---|---|---|

| Brent | ~USD85/bbl | Feedstock-driven margin pressure |

| Specialty enzymes | Market USD7.4B | High switching cost |

| rPET premium | +20% | Input cost spike |

| Container | ~USD2,000/FEU | Logistics pass-through |

| Validation time | >3 months | Switching friction |

What is included in the product

Uncovers key drivers of competition for Persan SA—assessing supplier and buyer power, threat of new entrants, substitutes, and industry rivalry to reveal pricing, profitability, and market-entry risks. Tailored strategic insights identify disruptive threats and protective barriers for decision-making and investor materials.

Clear one-sheet Porter's Five Forces for Persan SA—quickly pinpoint competitive pressure and relieve decision paralysis with a radar chart and customizable pressure levels for scenario testing.

Customers Bargaining Power

Retail giants and private labels

European hypermarkets and discounters (Aldi+Lidl ~13% EU grocery share in 2024) exert strong negotiating power and push private-label sourcing, forcing Persán into tight price talks.

Price cuts, slotting and promotional allowances—which can consume double-digit percentages of shelf supplier margin—intensify pressure on Persán’s margins.

Persán’s private-label capability secures volumes but at low pricing; maintaining scale and service levels is essential to preserve shelf presence.

High price sensitivity

Household cleaning is a frequent, low-involvement purchase with elastic demand; during 2022–24 inflation waves consumers increasingly traded down, lifting private-label penetration to roughly 30% in some EU markets in 2024 and pushing promotion incidence near 40%, which strengthens retailer leverage. Performance and eco-claims can differentiate Persan SA, but such claims are rapidly imitated, limiting pricing power.

B2B contract concentration

Large B2B contracts with key chains or multinational distributors drive volume dependence—Walmart alone recorded roughly 611 billion USD in net sales in FY2024, illustrating buyer scale and leverage over suppliers. Renewal cycles become critical negotiation points where price, terms and lead times are reset. Buyers increasingly press for bespoke specs and rapid innovation at minimal incremental cost, so diversifying geographies and channels reduces single-buyer risk.

Digital channel transparency

E-commerce transparency (global online retail ~22.3% of sales in 2024) makes price and review visibility pervasive, enabling easy comparison and shrinking room for premium pricing for Persan SA.

Private labels and challenger brands, growing share in grocery and apparel channels, use targeted ads to undercut prices and capture margin-sensitive buyers.

Retailers using data-driven assortments and dynamic pricing increase buyer power, compressing Persan SA margins absent strong brand equity.

- e-commerce-share-2024: 22.3%

- reviews-influence-high: >90% buyers

- private-label-pressure: rising share in grocery/apparel

- retailer-data-dynamic-pricing

ESG and compliance demands

Retailers impose stringent sustainability, traceability and packaging requirements that raise supplier costs and narrow sourcing options, giving buyers stronger leverage in price and terms. Compliance often becomes a market-access ticket—EU CSRD extended reporting to roughly 50,000 companies in 2024—shifting value capture toward retailers. Certifications and lifecycle metrics are now table stakes, compressing supplier margins.

- Increased supplier costs and fewer sourcing options

- Compliance = market access (CSRD ~50,000 firms in 2024)

- Certifications and LCA metrics are mandatory

Discounters, private-labels and promos compress margins as e-commerce 22.3%

European hypermarkets and discounters (Aldi+Lidl ~13% EU grocery share in 2024) and large chains (Walmart net sales ~611bn USD FY2024) drive strong buyer leverage, pushing private-label sourcing and deep promo/slotting discounts. Private-label penetration reached ~30% in some EU markets in 2024 and promotion incidence neared 40%, compressing Persán margins. E-commerce (22.3% of retail sales 2024) and reviews (>90% influence) further reduce pricing power.

| Metric | 2024 Value | Implication |

|---|---|---|

| Discounters share (EU) | ~13% | Higher private-label pressure |

| Private-label penetration | ~30% (some markets) | Lower ASPs |

| Promo incidence | ~40% | Margin erosion |

| E-commerce | 22.3% | Price transparency |

Same Document Delivered

Persan SA Porter's Five Forces Analysis

This preview shows the exact Persan SA Porter’s Five Forces analysis you’ll receive upon purchase—no placeholders or samples. The file is the complete, professionally formatted document, ready for immediate download and use. What you see here is precisely the deliverable accessible instantly after payment.