Petco Health and Wellness Company Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Petco faces moderate supplier leverage, intense buyer price sensitivity, growing rivalry from online and specialty retailers, manageable threat of new entrants due to scale needs, and rising substitution from e-commerce and private-label brands; strategic moves around omnichannel and private labels matter. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed force ratings, data, and actionable recommendations.

Suppliers Bargaining Power

Concentrated branded pet food vendors

Major suppliers like Mars and Nestlé Purina command strong branded pull and in 2024 control roughly half of the US pet food market, enabling demands for slotting and favorable terms on flagship diets. Petco counters with broad assortment and category management programs to negotiate merchandising and promotions. Expansion of Petco private-label ranges reduces reliance on a few branded suppliers and improves margin leverage.

Private label and OEM partners

Private-label programs reduce Petco's input costs and reliance on national brands, supporting margin expansion as the company operated roughly 1,500 retail locations in 2024. Specialized OEMs supplying premium formulations can extract bargaining power through proprietary technical know-how and constrained capacity. Multisourcing and long-term contracts are used to stabilize supply and pricing. Strict quality control is essential to prevent costly recalls and brand damage.

Veterinary pharma and diagnostics suppliers

Prescription foods, flea/tick treatments and diagnostics are often regulated by FDA/EPA and come from limited-source, patent-protected suppliers, elevating supplier power through restricted distribution and compliance burdens. Petco’s ~1,600 in‑store vet clinics (2024) create volume leverage but must follow strict protocols, limiting switching. Diversifying branded and private‑label alternatives helps cushion pricing pressure.

Logistics, freight, and packaging inputs

Logistics, freight, and packaging cost volatility gives upstream suppliers leverage when capacity tightens; fuel spikes or port disruptions can compress Petco Health and Wellness margins and raise COGS. Contracted carriers, network optimization, and inventory planning are used to blunt shocks, while scale across ~1,500+ stores strengthens rate negotiations in peak seasons.

- Freight sensitivity: fuel/port risk

- Mitigants: contracted carriers, DCs, inventory

- Scale: ~1,500+ stores boosts negotiating power

Risk of supplier DTC and exclusive channels

Brands pushing DTC or exclusive retailer deals compress Petco margins by diverting SKUs; in 2024 Petco reinforced omnichannel reach across roughly 1,500 stores plus digital, leaning on high-margin services and data-driven merchandising to preserve assortment share. Exclusive co-developed SKUs and joint marketing with loyalty integration reduce supplier disintermediation.

- Omnichannel scale: ~1,500 stores + e‑commerce

- Services attachment: higher basket value vs pure retail

- Exclusive SKUs: supplier differentiation

- Loyalty integration: reduces channel leakage

Chains reduce supplier leverage; national brands still at ~50% market share

Major brands (Mars, Nestlé Purina) held ~50% of US pet food market in 2024, giving suppliers significant leverage on slotting and terms. Petco’s ~1,500 stores and ~1,600 in‑store vet clinics plus private‑label expansion and exclusive SKUs reduce supplier dependence. Regulated/patented products and logistics volatility retain pockets of high supplier power.

| Supplier type | Power | 2024 metric | Mitigant |

|---|---|---|---|

| National brands | High | ~50% market share | Private label, exclusives |

| Prescription/patented | Very high | Limited suppliers | Long contracts, vet volume |

| Logistics | Medium | Fuel/port risk | Contract carriers, DCs |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, substitutes, and entry barriers specific to Petco Health and Wellness Company, identifying disruptive threats, pricing pressure, and strategic advantages that shape its market position.

A concise Porter's Five Forces one-sheet for Petco that pinpoints retail pain points—supplier consolidation, buyer price sensitivity, substitute services, moderate new entrants and intense rivalry—so leaders can quickly prioritize cost, loyalty and differentiation strategies.

Customers Bargaining Power

Low switching costs and abundant alternatives

Low switching costs let pet owners move among Petco, PetSmart, Chewy, Amazon, mass and grocery channels; U.S. pet spending reached $136.8B in 2023 and Chewy reported about $8.45B in 2023 net sales, heightening buyer leverage via online price transparency. Petco counters with loyalty, subscriptions and Vital Care plans to increase stickiness. Same-day delivery and BOPIS further reduce convenience gaps.

Price sensitivity vs. premiumization

Macro pressures drive higher demand for value packs and promotions, yet Petco reported approximately $6.6 billion revenue in FY2024, reflecting resilience as humanization trends support premium foods and services that soften pure price sensitivity. Tailored in-store and digital recommendations raise average ticket and justify higher spend. Bundling products with grooming or vet care increases perceived value and loyalty.

Omnichannel expectations

Shoppers now expect seamless inventory visibility, same‑day delivery and easy returns, and failures accelerate churn to digital‑first rivals; Petco’s omnichannel model leverages 1,500+ stores as fulfillment hubs to cut last‑mile costs and speed service. Using stores for pickup and delivery improves margins and fulfillment KPIs, while auto‑ship and reminder programs (core to recurring revenue) materially boost customer lifetime value.

Information-rich consumers

Service-led differentiation reduces power

Service-led differentiation at Petco reduces customer bargaining power: grooming, training and in-clinic vet services create time savings and continuity of care, and in 2024 Petco reported ~1,600 vet locations and integrated services that increase stickiness. When services link to product plans and memberships, switching costs rise; Petco’s VIP/wellness programs (2.4M+ members in 2024) lock in frequency and boost lifetime value, lowering buyer leverage.

- Services tied to products raise switching costs

- Memberships/wellness plans: 2.4M+ members (2024)

- ~1,600 vet locations provide continuity

- Cross-sell increases customer LTV and reduces bargaining power

Price transparency raises buyer leverage; omnichannel, loyalty and services increase stickiness

Low switching costs and online price transparency (U.S. pet spend $136.8B in 2023; Chewy sales $8.45B 2023) increase buyer leverage, but Petco’s omnichannel, loyalty and services (≈1,500 stores; ~1,600 vet locations; revenue ~$7.5B FY2024; VIP 2.4M+ members) raise stickiness and reduce bargaining power.

| Metric | Value |

|---|---|

| Stores | ≈1,500 |

| Vet locations | ~1,600 |

| FY2024 revenue | ~$7.5B |

| VIP members | 2.4M+ |

Same Document Delivered

Petco Health and Wellness Company Porter's Five Forces Analysis

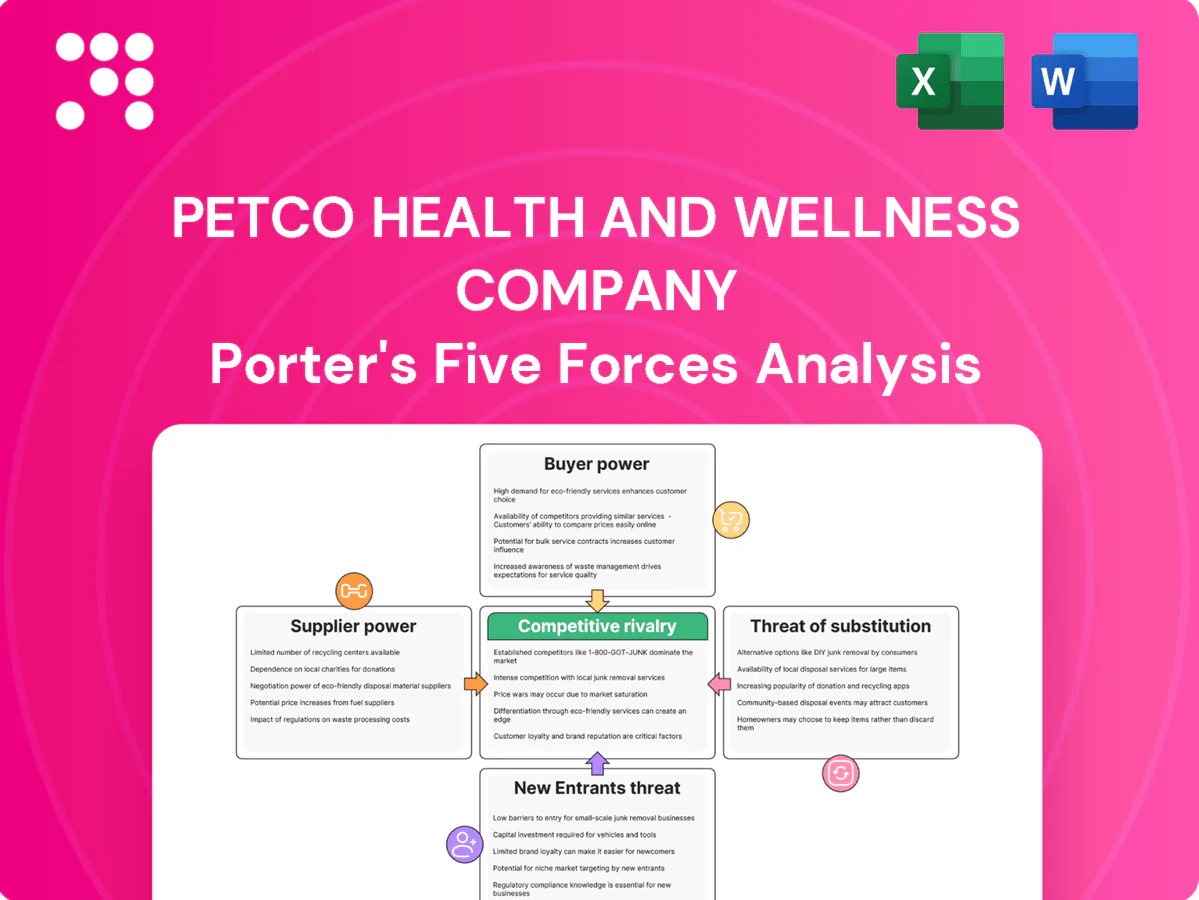

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. Petco's Porter’s Five Forces analysis finds high competitive rivalry from national chains and e-commerce, moderate buyer power due to brand loyalty and services, low supplier power, moderate threat of new entrants given scale and capital needs, and moderate threat of substitutes from vet clinics and online retail. This file is ready for immediate use.

Don't Miss the Bigger Picture

Petco faces moderate supplier leverage, intense buyer price sensitivity, growing rivalry from online and specialty retailers, manageable threat of new entrants due to scale needs, and rising substitution from e-commerce and private-label brands; strategic moves around omnichannel and private labels matter. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed force ratings, data, and actionable recommendations.

Suppliers Bargaining Power

Concentrated branded pet food vendors

Major suppliers like Mars and Nestlé Purina command strong branded pull and in 2024 control roughly half of the US pet food market, enabling demands for slotting and favorable terms on flagship diets. Petco counters with broad assortment and category management programs to negotiate merchandising and promotions. Expansion of Petco private-label ranges reduces reliance on a few branded suppliers and improves margin leverage.

Private label and OEM partners

Private-label programs reduce Petco's input costs and reliance on national brands, supporting margin expansion as the company operated roughly 1,500 retail locations in 2024. Specialized OEMs supplying premium formulations can extract bargaining power through proprietary technical know-how and constrained capacity. Multisourcing and long-term contracts are used to stabilize supply and pricing. Strict quality control is essential to prevent costly recalls and brand damage.

Veterinary pharma and diagnostics suppliers

Prescription foods, flea/tick treatments and diagnostics are often regulated by FDA/EPA and come from limited-source, patent-protected suppliers, elevating supplier power through restricted distribution and compliance burdens. Petco’s ~1,600 in‑store vet clinics (2024) create volume leverage but must follow strict protocols, limiting switching. Diversifying branded and private‑label alternatives helps cushion pricing pressure.

Logistics, freight, and packaging inputs

Logistics, freight, and packaging cost volatility gives upstream suppliers leverage when capacity tightens; fuel spikes or port disruptions can compress Petco Health and Wellness margins and raise COGS. Contracted carriers, network optimization, and inventory planning are used to blunt shocks, while scale across ~1,500+ stores strengthens rate negotiations in peak seasons.

- Freight sensitivity: fuel/port risk

- Mitigants: contracted carriers, DCs, inventory

- Scale: ~1,500+ stores boosts negotiating power

Risk of supplier DTC and exclusive channels

Brands pushing DTC or exclusive retailer deals compress Petco margins by diverting SKUs; in 2024 Petco reinforced omnichannel reach across roughly 1,500 stores plus digital, leaning on high-margin services and data-driven merchandising to preserve assortment share. Exclusive co-developed SKUs and joint marketing with loyalty integration reduce supplier disintermediation.

- Omnichannel scale: ~1,500 stores + e‑commerce

- Services attachment: higher basket value vs pure retail

- Exclusive SKUs: supplier differentiation

- Loyalty integration: reduces channel leakage

Chains reduce supplier leverage; national brands still at ~50% market share

Major brands (Mars, Nestlé Purina) held ~50% of US pet food market in 2024, giving suppliers significant leverage on slotting and terms. Petco’s ~1,500 stores and ~1,600 in‑store vet clinics plus private‑label expansion and exclusive SKUs reduce supplier dependence. Regulated/patented products and logistics volatility retain pockets of high supplier power.

| Supplier type | Power | 2024 metric | Mitigant |

|---|---|---|---|

| National brands | High | ~50% market share | Private label, exclusives |

| Prescription/patented | Very high | Limited suppliers | Long contracts, vet volume |

| Logistics | Medium | Fuel/port risk | Contract carriers, DCs |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, substitutes, and entry barriers specific to Petco Health and Wellness Company, identifying disruptive threats, pricing pressure, and strategic advantages that shape its market position.

A concise Porter's Five Forces one-sheet for Petco that pinpoints retail pain points—supplier consolidation, buyer price sensitivity, substitute services, moderate new entrants and intense rivalry—so leaders can quickly prioritize cost, loyalty and differentiation strategies.

Customers Bargaining Power

Low switching costs and abundant alternatives

Low switching costs let pet owners move among Petco, PetSmart, Chewy, Amazon, mass and grocery channels; U.S. pet spending reached $136.8B in 2023 and Chewy reported about $8.45B in 2023 net sales, heightening buyer leverage via online price transparency. Petco counters with loyalty, subscriptions and Vital Care plans to increase stickiness. Same-day delivery and BOPIS further reduce convenience gaps.

Price sensitivity vs. premiumization

Macro pressures drive higher demand for value packs and promotions, yet Petco reported approximately $6.6 billion revenue in FY2024, reflecting resilience as humanization trends support premium foods and services that soften pure price sensitivity. Tailored in-store and digital recommendations raise average ticket and justify higher spend. Bundling products with grooming or vet care increases perceived value and loyalty.

Omnichannel expectations

Shoppers now expect seamless inventory visibility, same‑day delivery and easy returns, and failures accelerate churn to digital‑first rivals; Petco’s omnichannel model leverages 1,500+ stores as fulfillment hubs to cut last‑mile costs and speed service. Using stores for pickup and delivery improves margins and fulfillment KPIs, while auto‑ship and reminder programs (core to recurring revenue) materially boost customer lifetime value.

Information-rich consumers

Service-led differentiation reduces power

Service-led differentiation at Petco reduces customer bargaining power: grooming, training and in-clinic vet services create time savings and continuity of care, and in 2024 Petco reported ~1,600 vet locations and integrated services that increase stickiness. When services link to product plans and memberships, switching costs rise; Petco’s VIP/wellness programs (2.4M+ members in 2024) lock in frequency and boost lifetime value, lowering buyer leverage.

- Services tied to products raise switching costs

- Memberships/wellness plans: 2.4M+ members (2024)

- ~1,600 vet locations provide continuity

- Cross-sell increases customer LTV and reduces bargaining power

Price transparency raises buyer leverage; omnichannel, loyalty and services increase stickiness

Low switching costs and online price transparency (U.S. pet spend $136.8B in 2023; Chewy sales $8.45B 2023) increase buyer leverage, but Petco’s omnichannel, loyalty and services (≈1,500 stores; ~1,600 vet locations; revenue ~$7.5B FY2024; VIP 2.4M+ members) raise stickiness and reduce bargaining power.

| Metric | Value |

|---|---|

| Stores | ≈1,500 |

| Vet locations | ~1,600 |

| FY2024 revenue | ~$7.5B |

| VIP members | 2.4M+ |

Same Document Delivered

Petco Health and Wellness Company Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. Petco's Porter’s Five Forces analysis finds high competitive rivalry from national chains and e-commerce, moderate buyer power due to brand loyalty and services, low supplier power, moderate threat of new entrants given scale and capital needs, and moderate threat of substitutes from vet clinics and online retail. This file is ready for immediate use.

Description

Don't Miss the Bigger Picture

Petco faces moderate supplier leverage, intense buyer price sensitivity, growing rivalry from online and specialty retailers, manageable threat of new entrants due to scale needs, and rising substitution from e-commerce and private-label brands; strategic moves around omnichannel and private labels matter. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed force ratings, data, and actionable recommendations.

Suppliers Bargaining Power

Concentrated branded pet food vendors

Major suppliers like Mars and Nestlé Purina command strong branded pull and in 2024 control roughly half of the US pet food market, enabling demands for slotting and favorable terms on flagship diets. Petco counters with broad assortment and category management programs to negotiate merchandising and promotions. Expansion of Petco private-label ranges reduces reliance on a few branded suppliers and improves margin leverage.

Private label and OEM partners

Private-label programs reduce Petco's input costs and reliance on national brands, supporting margin expansion as the company operated roughly 1,500 retail locations in 2024. Specialized OEMs supplying premium formulations can extract bargaining power through proprietary technical know-how and constrained capacity. Multisourcing and long-term contracts are used to stabilize supply and pricing. Strict quality control is essential to prevent costly recalls and brand damage.

Veterinary pharma and diagnostics suppliers

Prescription foods, flea/tick treatments and diagnostics are often regulated by FDA/EPA and come from limited-source, patent-protected suppliers, elevating supplier power through restricted distribution and compliance burdens. Petco’s ~1,600 in‑store vet clinics (2024) create volume leverage but must follow strict protocols, limiting switching. Diversifying branded and private‑label alternatives helps cushion pricing pressure.

Logistics, freight, and packaging inputs

Logistics, freight, and packaging cost volatility gives upstream suppliers leverage when capacity tightens; fuel spikes or port disruptions can compress Petco Health and Wellness margins and raise COGS. Contracted carriers, network optimization, and inventory planning are used to blunt shocks, while scale across ~1,500+ stores strengthens rate negotiations in peak seasons.

- Freight sensitivity: fuel/port risk

- Mitigants: contracted carriers, DCs, inventory

- Scale: ~1,500+ stores boosts negotiating power

Risk of supplier DTC and exclusive channels

Brands pushing DTC or exclusive retailer deals compress Petco margins by diverting SKUs; in 2024 Petco reinforced omnichannel reach across roughly 1,500 stores plus digital, leaning on high-margin services and data-driven merchandising to preserve assortment share. Exclusive co-developed SKUs and joint marketing with loyalty integration reduce supplier disintermediation.

- Omnichannel scale: ~1,500 stores + e‑commerce

- Services attachment: higher basket value vs pure retail

- Exclusive SKUs: supplier differentiation

- Loyalty integration: reduces channel leakage

Chains reduce supplier leverage; national brands still at ~50% market share

Major brands (Mars, Nestlé Purina) held ~50% of US pet food market in 2024, giving suppliers significant leverage on slotting and terms. Petco’s ~1,500 stores and ~1,600 in‑store vet clinics plus private‑label expansion and exclusive SKUs reduce supplier dependence. Regulated/patented products and logistics volatility retain pockets of high supplier power.

| Supplier type | Power | 2024 metric | Mitigant |

|---|---|---|---|

| National brands | High | ~50% market share | Private label, exclusives |

| Prescription/patented | Very high | Limited suppliers | Long contracts, vet volume |

| Logistics | Medium | Fuel/port risk | Contract carriers, DCs |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, substitutes, and entry barriers specific to Petco Health and Wellness Company, identifying disruptive threats, pricing pressure, and strategic advantages that shape its market position.

A concise Porter's Five Forces one-sheet for Petco that pinpoints retail pain points—supplier consolidation, buyer price sensitivity, substitute services, moderate new entrants and intense rivalry—so leaders can quickly prioritize cost, loyalty and differentiation strategies.

Customers Bargaining Power

Low switching costs and abundant alternatives

Low switching costs let pet owners move among Petco, PetSmart, Chewy, Amazon, mass and grocery channels; U.S. pet spending reached $136.8B in 2023 and Chewy reported about $8.45B in 2023 net sales, heightening buyer leverage via online price transparency. Petco counters with loyalty, subscriptions and Vital Care plans to increase stickiness. Same-day delivery and BOPIS further reduce convenience gaps.

Price sensitivity vs. premiumization

Macro pressures drive higher demand for value packs and promotions, yet Petco reported approximately $6.6 billion revenue in FY2024, reflecting resilience as humanization trends support premium foods and services that soften pure price sensitivity. Tailored in-store and digital recommendations raise average ticket and justify higher spend. Bundling products with grooming or vet care increases perceived value and loyalty.

Omnichannel expectations

Shoppers now expect seamless inventory visibility, same‑day delivery and easy returns, and failures accelerate churn to digital‑first rivals; Petco’s omnichannel model leverages 1,500+ stores as fulfillment hubs to cut last‑mile costs and speed service. Using stores for pickup and delivery improves margins and fulfillment KPIs, while auto‑ship and reminder programs (core to recurring revenue) materially boost customer lifetime value.

Information-rich consumers

Service-led differentiation reduces power

Service-led differentiation at Petco reduces customer bargaining power: grooming, training and in-clinic vet services create time savings and continuity of care, and in 2024 Petco reported ~1,600 vet locations and integrated services that increase stickiness. When services link to product plans and memberships, switching costs rise; Petco’s VIP/wellness programs (2.4M+ members in 2024) lock in frequency and boost lifetime value, lowering buyer leverage.

- Services tied to products raise switching costs

- Memberships/wellness plans: 2.4M+ members (2024)

- ~1,600 vet locations provide continuity

- Cross-sell increases customer LTV and reduces bargaining power

Price transparency raises buyer leverage; omnichannel, loyalty and services increase stickiness

Low switching costs and online price transparency (U.S. pet spend $136.8B in 2023; Chewy sales $8.45B 2023) increase buyer leverage, but Petco’s omnichannel, loyalty and services (≈1,500 stores; ~1,600 vet locations; revenue ~$7.5B FY2024; VIP 2.4M+ members) raise stickiness and reduce bargaining power.

| Metric | Value |

|---|---|

| Stores | ≈1,500 |

| Vet locations | ~1,600 |

| FY2024 revenue | ~$7.5B |

| VIP members | 2.4M+ |

Same Document Delivered

Petco Health and Wellness Company Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. Petco's Porter’s Five Forces analysis finds high competitive rivalry from national chains and e-commerce, moderate buyer power due to brand loyalty and services, low supplier power, moderate threat of new entrants given scale and capital needs, and moderate threat of substitutes from vet clinics and online retail. This file is ready for immediate use.