Pet Valu Porter's Five Forces Analysis

From Overview to Strategy Blueprint

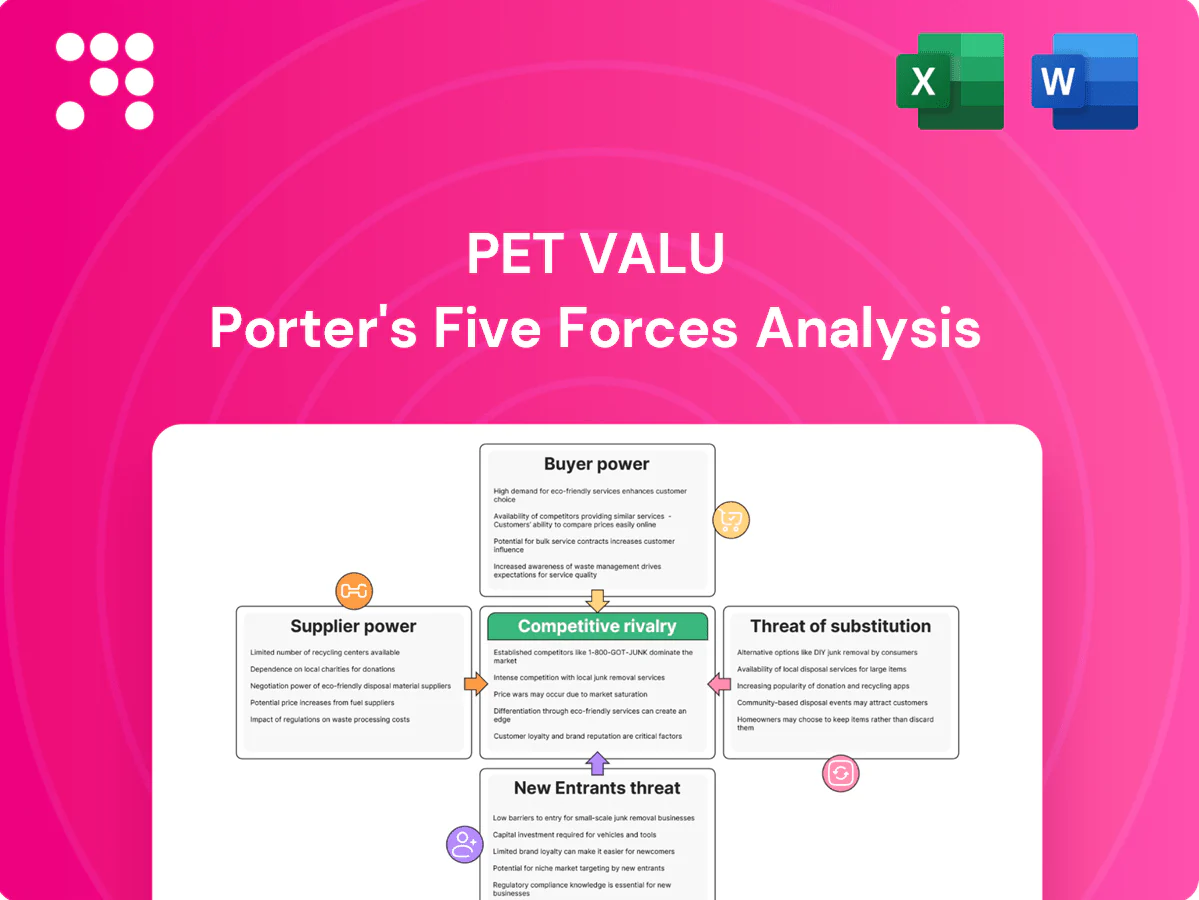

Pet Valu’s Porter's Five Forces snapshot highlights supplier leverage, buyer sensitivity, rival intensity and substitute threats shaping its retail pet segment, plus barriers to new entrants and regulatory pressures. This brief overview teases strategic implications and risk areas for investors and managers. The complete report reveals force-by-force ratings, visuals, and actionable recommendations. Unlock the full Porter's Five Forces Analysis to explore Pet Valu’s competitive dynamics in depth.

Suppliers Bargaining Power

Brand concentration in premium

Premium and super-premium pet food is concentrated among major manufacturers—Mars, Nestlé Purina and Colgate-Palmolive (Hill's) together control the majority of the premium segment—lifting supplier bargaining power. Pet Valu reported ~C$1.06bn revenue in FY2023 and must stock these in-demand labels to satisfy customers, limiting promotional leverage. Brands with strong consumer pull resist concessions, squeezing gross margins during the 2022–23 input-cost inflation cycle.

Private label as counterweight

Pet Valu’s growing private label portfolio provides negotiation leverage and margin protection, with private-label penetration exceeding 10% of sales in 2024, enabling credible substitution for national brands on price or availability. Expanded private label reduces dependence on concentrated suppliers and improves gross margins by lowering COGS exposure. Sustaining this mix requires maintaining high perceived quality through strict product standards and marketing investment.

Supplier switching and exclusivity

Switching costs are moderate: many categories have multiple qualified vendors, though specialty diets and exclusive formulations limit alternatives; Pet Valu operates approximately 600 stores in Canada and the US (2024), which improves access to allocations and negotiating leverage. Region-specific distributors and unique SKUs sustain supplier power for certain products despite Pet Valu’s scale.

Input and logistics volatility

Upstream swings in proteins and grains plus rising freight costs are often passed through by suppliers, compressing Pet Valu retail margins when retail price adjustments lag; Pet Valu uses multi-sourcing and forward buys to smooth spikes but sustained cost inflation increases supplier leverage and squeeze on gross margins.

- pass-through risk: suppliers shift commodity and freight rises

- mitigation: multi-sourcing, forward buys

- impact: lagged price increases compress margins

- trend: persistent inflation raises supplier bargaining power

Compliance and recalls dynamics

Regulatory standards and occasional product recalls in 2024 shifted operational risk onto suppliers, creating stockouts and substitution frictions that pressured Pet Valu’s supply chain; Pet Valu reported roughly CAD 1.05 billion in system sales in 2024, amplifying the impact. Strong QA requirements and tightened vendor qualification narrowed supplier pools, while vendor scorecards enforce accountability; safety-sensitive categories keep reputable suppliers’ bargaining strength high.

- Recall-driven stockouts: higher substitution costs

- Vendor scorecards: increase compliance enforcement

- Narrowed pool: higher switching costs

- Safety-sensitive items: supplier leverage

Premium-brand dominance tightens supply; private labels protect margins

Major premium brands (Mars, Nestlé Purina, Colgate-Palmolive) dominate supply, raising supplier power as Pet Valu (≈C$1.06bn revenue FY2023; ≈CAD1.05bn system sales 2024) must carry in-demand labels. Private label >10% of sales in 2024 provides partial leverage and margin protection. Commodity/freight pass-throughs and recalls increase supplier squeeze despite multi-sourcing and forward buys.

| Metric | Value |

|---|---|

| FY2023 revenue | C$1.06bn |

| System sales 2024 | CAD1.05bn |

| Private-label penetration 2024 | >10% |

| Major brand concentration | Mars/Nestlé/Colgate majority |

What is included in the product

Tailored Porter's Five Forces analysis for Pet Valu that uncovers key drivers of competition, buyer and supplier power, and barriers to entry; evaluates substitutes and emerging threats to its market share and profitability.

Concise one-sheet Porter's Five Forces for Pet Valu—visualize competitive pressures and tailor scenarios (e.g., e‑commerce growth, private‑label expansion) to guide quick strategic decisions and boardroom-ready recommendations.

Customers Bargaining Power

Low switching costs

Low switching costs mean pet owners move easily across specialty, mass, grocery and online channels; industry-wide e-commerce penetration reached roughly 20% in 2024, accelerating channel fluidity. Branded SKU prices are simple to compare via apps and marketplaces, so convenience, proximity and in-stock availability drive rapid shifts in spend. These dynamics keep customer bargaining power moderate to high for Pet Valu.

Price sensitivity vs pet humanization

While many shoppers seek value, 2024 industry data show US pet spending near $143B and rising premium sales as about 65% of owners prioritize health-focused products, allowing Pet Valu to maintain a premium mix while still facing deal-seeking behavior. Promotions and loyalty programs drive a large share of basket decisions, and customer power varies significantly by income and specific pet health needs.

Omnichannel expectations

Shoppers now expect BOPIS, curbside, scheduled delivery and subscriptions, and with ecommerce at roughly 14% of retail sales in 2024 and a global cart abandonment rate around 69.8% (Baymard Institute 2023), friction in any channel quickly drives customers to marketplaces or rivals. Pet Valu’s omnichannel execution can blunt buyer power by raising convenience and stickiness, while weak execution increases consumers’ negotiating leverage.

Loyalty and community services

Loyalty points, grooming and self-serve wash at Pet Valu raise retention and cut price elasticity; 2024 Bond Loyalty data shows ~73% of consumers favor brands with rewards, boosting repeat visits and basket size. Community events and in-store pet expertise create perceived value beyond products, lowering buyer bargaining power; absent these services, customers push harder for discounts.

Product availability and special diets

Pet owners with prescription or specialty diets display low price elasticity but extreme sensitivity to availability; APPA estimated U.S. pet spending at about $144 billion in 2024, with specialty food share growing year-over-year. Stockouts drive immediate channel switching to clinics or online retailers, so breadth in specialty and vet-adjacent SKUs reduces buyer leverage. Refill predictability via subscriptions materially increases retention and margin stability.

- Availability sensitivity: high

- Price elasticity: low for special diets

- Stockouts → immediate switching

- SKU breadth reduces leverage

- Subscriptions lock demand

Premium pet demand and strong loyalty temper moderate-high customer bargaining power

Low switching costs and ~20% pet-industry e-commerce penetration in 2024 keep customer bargaining power moderate-high; price comparison apps and promotions intensify that leverage. US pet spending ≈ $144B in 2024 with 65% preferring health-focused/premium products, supporting a premium mix but sustaining deal-seeking. Loyalty (≈73% favor rewards) plus services/subscriptions reduce price sensitivity and stabilize retention.

| Metric | 2024 | Implication |

|---|---|---|

| E‑commerce | ~20% | Channel fluidity |

| US spend | $144B | Premium demand |

| Loyalty | ~73% | Higher retention |

Full Version Awaits

Pet Valu Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It is a complete Pet Valu Porter’s Five Forces analysis covering threat of new entrants, supplier and buyer power, competitive rivalry, and substitutes. The file is professionally formatted and ready for immediate download and use.

From Overview to Strategy Blueprint

Pet Valu’s Porter's Five Forces snapshot highlights supplier leverage, buyer sensitivity, rival intensity and substitute threats shaping its retail pet segment, plus barriers to new entrants and regulatory pressures. This brief overview teases strategic implications and risk areas for investors and managers. The complete report reveals force-by-force ratings, visuals, and actionable recommendations. Unlock the full Porter's Five Forces Analysis to explore Pet Valu’s competitive dynamics in depth.

Suppliers Bargaining Power

Brand concentration in premium

Premium and super-premium pet food is concentrated among major manufacturers—Mars, Nestlé Purina and Colgate-Palmolive (Hill's) together control the majority of the premium segment—lifting supplier bargaining power. Pet Valu reported ~C$1.06bn revenue in FY2023 and must stock these in-demand labels to satisfy customers, limiting promotional leverage. Brands with strong consumer pull resist concessions, squeezing gross margins during the 2022–23 input-cost inflation cycle.

Private label as counterweight

Pet Valu’s growing private label portfolio provides negotiation leverage and margin protection, with private-label penetration exceeding 10% of sales in 2024, enabling credible substitution for national brands on price or availability. Expanded private label reduces dependence on concentrated suppliers and improves gross margins by lowering COGS exposure. Sustaining this mix requires maintaining high perceived quality through strict product standards and marketing investment.

Supplier switching and exclusivity

Switching costs are moderate: many categories have multiple qualified vendors, though specialty diets and exclusive formulations limit alternatives; Pet Valu operates approximately 600 stores in Canada and the US (2024), which improves access to allocations and negotiating leverage. Region-specific distributors and unique SKUs sustain supplier power for certain products despite Pet Valu’s scale.

Input and logistics volatility

Upstream swings in proteins and grains plus rising freight costs are often passed through by suppliers, compressing Pet Valu retail margins when retail price adjustments lag; Pet Valu uses multi-sourcing and forward buys to smooth spikes but sustained cost inflation increases supplier leverage and squeeze on gross margins.

- pass-through risk: suppliers shift commodity and freight rises

- mitigation: multi-sourcing, forward buys

- impact: lagged price increases compress margins

- trend: persistent inflation raises supplier bargaining power

Compliance and recalls dynamics

Regulatory standards and occasional product recalls in 2024 shifted operational risk onto suppliers, creating stockouts and substitution frictions that pressured Pet Valu’s supply chain; Pet Valu reported roughly CAD 1.05 billion in system sales in 2024, amplifying the impact. Strong QA requirements and tightened vendor qualification narrowed supplier pools, while vendor scorecards enforce accountability; safety-sensitive categories keep reputable suppliers’ bargaining strength high.

- Recall-driven stockouts: higher substitution costs

- Vendor scorecards: increase compliance enforcement

- Narrowed pool: higher switching costs

- Safety-sensitive items: supplier leverage

Premium-brand dominance tightens supply; private labels protect margins

Major premium brands (Mars, Nestlé Purina, Colgate-Palmolive) dominate supply, raising supplier power as Pet Valu (≈C$1.06bn revenue FY2023; ≈CAD1.05bn system sales 2024) must carry in-demand labels. Private label >10% of sales in 2024 provides partial leverage and margin protection. Commodity/freight pass-throughs and recalls increase supplier squeeze despite multi-sourcing and forward buys.

| Metric | Value |

|---|---|

| FY2023 revenue | C$1.06bn |

| System sales 2024 | CAD1.05bn |

| Private-label penetration 2024 | >10% |

| Major brand concentration | Mars/Nestlé/Colgate majority |

What is included in the product

Tailored Porter's Five Forces analysis for Pet Valu that uncovers key drivers of competition, buyer and supplier power, and barriers to entry; evaluates substitutes and emerging threats to its market share and profitability.

Concise one-sheet Porter's Five Forces for Pet Valu—visualize competitive pressures and tailor scenarios (e.g., e‑commerce growth, private‑label expansion) to guide quick strategic decisions and boardroom-ready recommendations.

Customers Bargaining Power

Low switching costs

Low switching costs mean pet owners move easily across specialty, mass, grocery and online channels; industry-wide e-commerce penetration reached roughly 20% in 2024, accelerating channel fluidity. Branded SKU prices are simple to compare via apps and marketplaces, so convenience, proximity and in-stock availability drive rapid shifts in spend. These dynamics keep customer bargaining power moderate to high for Pet Valu.

Price sensitivity vs pet humanization

While many shoppers seek value, 2024 industry data show US pet spending near $143B and rising premium sales as about 65% of owners prioritize health-focused products, allowing Pet Valu to maintain a premium mix while still facing deal-seeking behavior. Promotions and loyalty programs drive a large share of basket decisions, and customer power varies significantly by income and specific pet health needs.

Omnichannel expectations

Shoppers now expect BOPIS, curbside, scheduled delivery and subscriptions, and with ecommerce at roughly 14% of retail sales in 2024 and a global cart abandonment rate around 69.8% (Baymard Institute 2023), friction in any channel quickly drives customers to marketplaces or rivals. Pet Valu’s omnichannel execution can blunt buyer power by raising convenience and stickiness, while weak execution increases consumers’ negotiating leverage.

Loyalty and community services

Loyalty points, grooming and self-serve wash at Pet Valu raise retention and cut price elasticity; 2024 Bond Loyalty data shows ~73% of consumers favor brands with rewards, boosting repeat visits and basket size. Community events and in-store pet expertise create perceived value beyond products, lowering buyer bargaining power; absent these services, customers push harder for discounts.

Product availability and special diets

Pet owners with prescription or specialty diets display low price elasticity but extreme sensitivity to availability; APPA estimated U.S. pet spending at about $144 billion in 2024, with specialty food share growing year-over-year. Stockouts drive immediate channel switching to clinics or online retailers, so breadth in specialty and vet-adjacent SKUs reduces buyer leverage. Refill predictability via subscriptions materially increases retention and margin stability.

- Availability sensitivity: high

- Price elasticity: low for special diets

- Stockouts → immediate switching

- SKU breadth reduces leverage

- Subscriptions lock demand

Premium pet demand and strong loyalty temper moderate-high customer bargaining power

Low switching costs and ~20% pet-industry e-commerce penetration in 2024 keep customer bargaining power moderate-high; price comparison apps and promotions intensify that leverage. US pet spending ≈ $144B in 2024 with 65% preferring health-focused/premium products, supporting a premium mix but sustaining deal-seeking. Loyalty (≈73% favor rewards) plus services/subscriptions reduce price sensitivity and stabilize retention.

| Metric | 2024 | Implication |

|---|---|---|

| E‑commerce | ~20% | Channel fluidity |

| US spend | $144B | Premium demand |

| Loyalty | ~73% | Higher retention |

Full Version Awaits

Pet Valu Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It is a complete Pet Valu Porter’s Five Forces analysis covering threat of new entrants, supplier and buyer power, competitive rivalry, and substitutes. The file is professionally formatted and ready for immediate download and use.

Description

From Overview to Strategy Blueprint

Pet Valu’s Porter's Five Forces snapshot highlights supplier leverage, buyer sensitivity, rival intensity and substitute threats shaping its retail pet segment, plus barriers to new entrants and regulatory pressures. This brief overview teases strategic implications and risk areas for investors and managers. The complete report reveals force-by-force ratings, visuals, and actionable recommendations. Unlock the full Porter's Five Forces Analysis to explore Pet Valu’s competitive dynamics in depth.

Suppliers Bargaining Power

Brand concentration in premium

Premium and super-premium pet food is concentrated among major manufacturers—Mars, Nestlé Purina and Colgate-Palmolive (Hill's) together control the majority of the premium segment—lifting supplier bargaining power. Pet Valu reported ~C$1.06bn revenue in FY2023 and must stock these in-demand labels to satisfy customers, limiting promotional leverage. Brands with strong consumer pull resist concessions, squeezing gross margins during the 2022–23 input-cost inflation cycle.

Private label as counterweight

Pet Valu’s growing private label portfolio provides negotiation leverage and margin protection, with private-label penetration exceeding 10% of sales in 2024, enabling credible substitution for national brands on price or availability. Expanded private label reduces dependence on concentrated suppliers and improves gross margins by lowering COGS exposure. Sustaining this mix requires maintaining high perceived quality through strict product standards and marketing investment.

Supplier switching and exclusivity

Switching costs are moderate: many categories have multiple qualified vendors, though specialty diets and exclusive formulations limit alternatives; Pet Valu operates approximately 600 stores in Canada and the US (2024), which improves access to allocations and negotiating leverage. Region-specific distributors and unique SKUs sustain supplier power for certain products despite Pet Valu’s scale.

Input and logistics volatility

Upstream swings in proteins and grains plus rising freight costs are often passed through by suppliers, compressing Pet Valu retail margins when retail price adjustments lag; Pet Valu uses multi-sourcing and forward buys to smooth spikes but sustained cost inflation increases supplier leverage and squeeze on gross margins.

- pass-through risk: suppliers shift commodity and freight rises

- mitigation: multi-sourcing, forward buys

- impact: lagged price increases compress margins

- trend: persistent inflation raises supplier bargaining power

Compliance and recalls dynamics

Regulatory standards and occasional product recalls in 2024 shifted operational risk onto suppliers, creating stockouts and substitution frictions that pressured Pet Valu’s supply chain; Pet Valu reported roughly CAD 1.05 billion in system sales in 2024, amplifying the impact. Strong QA requirements and tightened vendor qualification narrowed supplier pools, while vendor scorecards enforce accountability; safety-sensitive categories keep reputable suppliers’ bargaining strength high.

- Recall-driven stockouts: higher substitution costs

- Vendor scorecards: increase compliance enforcement

- Narrowed pool: higher switching costs

- Safety-sensitive items: supplier leverage

Premium-brand dominance tightens supply; private labels protect margins

Major premium brands (Mars, Nestlé Purina, Colgate-Palmolive) dominate supply, raising supplier power as Pet Valu (≈C$1.06bn revenue FY2023; ≈CAD1.05bn system sales 2024) must carry in-demand labels. Private label >10% of sales in 2024 provides partial leverage and margin protection. Commodity/freight pass-throughs and recalls increase supplier squeeze despite multi-sourcing and forward buys.

| Metric | Value |

|---|---|

| FY2023 revenue | C$1.06bn |

| System sales 2024 | CAD1.05bn |

| Private-label penetration 2024 | >10% |

| Major brand concentration | Mars/Nestlé/Colgate majority |

What is included in the product

Tailored Porter's Five Forces analysis for Pet Valu that uncovers key drivers of competition, buyer and supplier power, and barriers to entry; evaluates substitutes and emerging threats to its market share and profitability.

Concise one-sheet Porter's Five Forces for Pet Valu—visualize competitive pressures and tailor scenarios (e.g., e‑commerce growth, private‑label expansion) to guide quick strategic decisions and boardroom-ready recommendations.

Customers Bargaining Power

Low switching costs

Low switching costs mean pet owners move easily across specialty, mass, grocery and online channels; industry-wide e-commerce penetration reached roughly 20% in 2024, accelerating channel fluidity. Branded SKU prices are simple to compare via apps and marketplaces, so convenience, proximity and in-stock availability drive rapid shifts in spend. These dynamics keep customer bargaining power moderate to high for Pet Valu.

Price sensitivity vs pet humanization

While many shoppers seek value, 2024 industry data show US pet spending near $143B and rising premium sales as about 65% of owners prioritize health-focused products, allowing Pet Valu to maintain a premium mix while still facing deal-seeking behavior. Promotions and loyalty programs drive a large share of basket decisions, and customer power varies significantly by income and specific pet health needs.

Omnichannel expectations

Shoppers now expect BOPIS, curbside, scheduled delivery and subscriptions, and with ecommerce at roughly 14% of retail sales in 2024 and a global cart abandonment rate around 69.8% (Baymard Institute 2023), friction in any channel quickly drives customers to marketplaces or rivals. Pet Valu’s omnichannel execution can blunt buyer power by raising convenience and stickiness, while weak execution increases consumers’ negotiating leverage.

Loyalty and community services

Loyalty points, grooming and self-serve wash at Pet Valu raise retention and cut price elasticity; 2024 Bond Loyalty data shows ~73% of consumers favor brands with rewards, boosting repeat visits and basket size. Community events and in-store pet expertise create perceived value beyond products, lowering buyer bargaining power; absent these services, customers push harder for discounts.

Product availability and special diets

Pet owners with prescription or specialty diets display low price elasticity but extreme sensitivity to availability; APPA estimated U.S. pet spending at about $144 billion in 2024, with specialty food share growing year-over-year. Stockouts drive immediate channel switching to clinics or online retailers, so breadth in specialty and vet-adjacent SKUs reduces buyer leverage. Refill predictability via subscriptions materially increases retention and margin stability.

- Availability sensitivity: high

- Price elasticity: low for special diets

- Stockouts → immediate switching

- SKU breadth reduces leverage

- Subscriptions lock demand

Premium pet demand and strong loyalty temper moderate-high customer bargaining power

Low switching costs and ~20% pet-industry e-commerce penetration in 2024 keep customer bargaining power moderate-high; price comparison apps and promotions intensify that leverage. US pet spending ≈ $144B in 2024 with 65% preferring health-focused/premium products, supporting a premium mix but sustaining deal-seeking. Loyalty (≈73% favor rewards) plus services/subscriptions reduce price sensitivity and stabilize retention.

| Metric | 2024 | Implication |

|---|---|---|

| E‑commerce | ~20% | Channel fluidity |

| US spend | $144B | Premium demand |

| Loyalty | ~73% | Higher retention |

Full Version Awaits

Pet Valu Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It is a complete Pet Valu Porter’s Five Forces analysis covering threat of new entrants, supplier and buyer power, competitive rivalry, and substitutes. The file is professionally formatted and ready for immediate download and use.