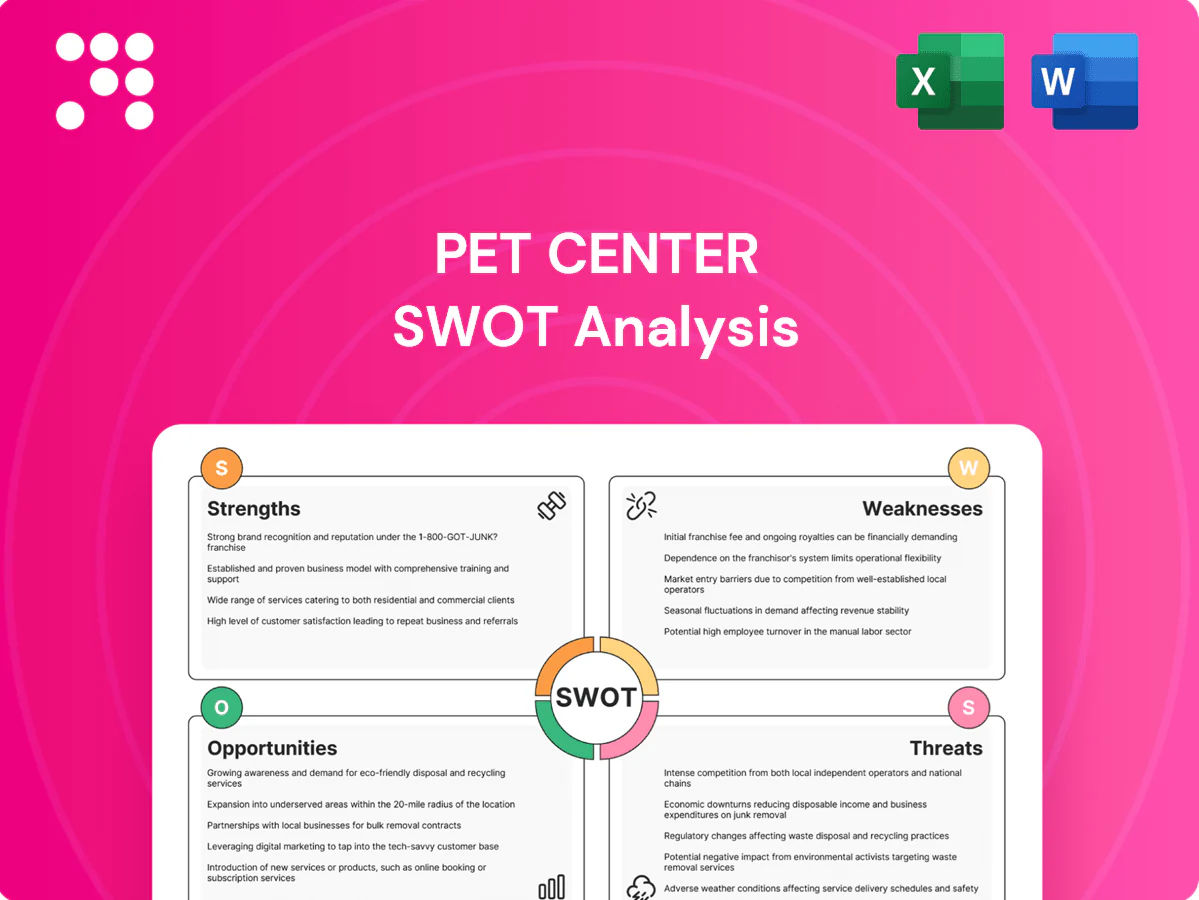

Pet Center SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Pet Center's SWOT reveals resilient brand strength, diversified product mix, and loyal customers, alongside margin pressure and supply-chain vulnerabilities. We outline opportunities—omnichannel expansion and pet wellness trends—and threats like fierce competition and regulatory shifts, with clear strategic options. Purchase the full SWOT analysis to access a professionally written, editable report and Excel tools for planning and investment.

Strengths

Nationwide store footprint

Wide nationwide footprint boosts brand visibility and convenience, reaching part of the roughly 90.5 million US households that own pets. Dense store presence enables rapid fulfillment and click-and-collect services, shortening delivery times and improving conversion. Localized assortments align with regional preferences, while stores serve as service hubs that drive repeat visits and loyalty.

Omnichannel integration

Omnichannel integration lets Pet Center link strong e-commerce and stores for seamless journeys—browse online, pick up in-store, or book services digitally—cutting friction via unified inventory and payments; US e-commerce was 15.7% of retail in 2023 and the global pet care market was about $232B in 2023, enabling data-driven targeted marketing across channels.

Full-service pet ecosystem

Integrated veterinary clinics, grooming, and adoption create a one-stop experience that lifts visit frequency and retention; the US pet market was estimated at about $143 billion in 2024, with services capturing a growing share. Services drive higher lifetime value—average annual spend per pet rises when bundled care is offered—and cross-selling between products and services typically increases basket size by double-digit percentages. Adoption initiatives boost community ties and measurable brand goodwill, often translating to higher local store traffic and repeat purchases.

Comprehensive product assortment

Comprehensive assortment covers food, toys and accessories across dogs, cats and small animals, aligning with a US pet market of 136.8 billion in 2023 (APPA), capturing core demand and upsell opportunities. Deep SKU depth supports budget and premium shoppers and multiple species, improving basket size. Reliable in-stock levels build trust and repeat visits; strong vendor ties enable promotions and exclusives.

- Market size: 136.8B (US, 2023)

- Multi-category SKUs: budget to premium

- In-stock = higher repeat visits

- Vendor deals = exclusives & promos

Strong brand recognition

Leader positioning increases top-of-mind awareness, supporting customer retention in a US pet market with $136.8B in spending (APPA, 2022). Consistent service standards reinforce trust and repeat visits, while marketing scale reduces customer acquisition cost per unit. Brand strength enables selective premium pricing in higher-margin categories.

- Leader positioning: higher recall

- Service standards: stronger retention

- Marketing scale: lower CAC

- Brand power: premium pricing

Nationwide pet retail scale: 90.5M households, omnichannel commerce and service-driven loyalty

Extensive nationwide footprint reaches ~90.5M US pet-owning households, enabling fast fulfillment and click-and-collect. Omnichannel integration and unified inventory drive conversion; e-commerce was 15.7% of retail in 2023. Services (vet/grooming/adoption) increase visit frequency and lifetime value. Broad SKU depth and vendor exclusives support premium pricing and repeat purchases.

| Metric | Value |

|---|---|

| US pet households | ~90.5M |

| US pet market | $136.8B (2023); $143B (2024 est.) |

| E‑commerce share | 15.7% (2023) |

What is included in the product

Delivers a strategic overview of Pet Center’s internal capabilities and external market forces, outlining strengths, weaknesses, opportunities, and threats to inform strategic decisions.

Provides a concise Pet Center SWOT matrix that highlights key pain points and priorities for rapid mitigation and resource allocation. Editable format enables quick scenario updates so frontline teams and executives can act on changing risks and opportunities.

Weaknesses

High operating cost base

Large store and clinic networks drive heavy fixed costs; U.S. pet industry spending was $136.8B in 2023 and veterinary services alone totaled about $35.6B, highlighting capital intensity. Rent, staffing and vet equipment compress margins, and utilization swings quickly hit profitability, so strict cost discipline is essential in downturns.

Service quality consistency

Standardizing veterinary and grooming outcomes across locations is difficult and risks variability that can erode trust and online reviews; with the US pet industry at $136.8 billion in 2022 (APPA), services are a material revenue driver. Training and compliance add measurable overhead—often cited as 4–6% of operating costs—and recurring certification needs raise fixed costs. Talent shortages remain acute, with surveys indicating roughly half of clinics reporting staffing gaps, constraining capacity and expansion.

Inventory complexity

Managing tens of thousands of SKUs (Chewy lists ~200,000 products) across channels raises obsolescence risk, especially as pet food shelf life is typically 12–18 months. Heavy pet food drives logistics costs and lifts freight share of COGS, while forecast errors produce ~10% OOS or markdown-driven margin erosion. Cold-chain and prescription items add regulatory and temperature-control constraints and higher per-unit handling costs.

Exposure to domestic macro cycles

Reliance on Brazilian consumer spending makes Pet Center sensitive to domestic cycles, with discretionary segments such as accessories showing higher elasticity and sharper sales swings during downturns.

High inflationary episodes compress margins by raising input costs while dampening demand; BRL volatility further transmits to retail prices for imported pet food and supplies.

- High consumer sensitivity

- Accessories = elastic demand

- Inflation squeezes margins

- Currency risk on imports

Digital experience gaps vs. pure-plays

Online marketplaces deliver broader selection and lower prices, pressuring Pet Center on assortment and margin; average e-commerce conversion was about 2.5% in 2024 (Statista), so slow feature rollout from legacy systems directly hits sales. Delivery speed and shipping cost remain battlegrounds as consumers prioritize fast, low-cost fulfillment, and cart conversion falls without continuous optimization.

- Selection/pricing pressure

- Delivery cost/speed competitiveness

- Legacy IT hinders feature speed

- Low conversion risk ~2.5%

High fixed costs, staffing gaps and SKU complexity are squeezing pet retail margins

Large fixed costs from stores/clinics (U.S. pet spend $136.8B 2023; vet $35.6B) compress margins and magnify utilization swings. Standardizing clinical/grooming quality and filling staffing gaps (~50% clinics report shortages) raise operating overhead. SKU complexity (Chewy ~200k SKUs) drives ~10% obsolescence/OOS; e-commerce conversion ~2.5% slows growth amid delivery/cost pressure and BRL/import volatility.

| Metric | Value |

|---|---|

| U.S. pet spend (2023) | $136.8B |

| Veterinary services (2023) | $35.6B |

| Clinic staffing gap | ~50% |

| SKU breadth (peer) | ~200,000 |

| Obsolescence/OOS | ~10% |

| E‑commerce conversion (2024) | ~2.5% |

Same Document Delivered

Pet Center SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete structure and findings for Pet Center. Purchase unlocks the editable, full-length version for immediate download after checkout.

Elevate Your Analysis with the Complete SWOT Report

Pet Center's SWOT reveals resilient brand strength, diversified product mix, and loyal customers, alongside margin pressure and supply-chain vulnerabilities. We outline opportunities—omnichannel expansion and pet wellness trends—and threats like fierce competition and regulatory shifts, with clear strategic options. Purchase the full SWOT analysis to access a professionally written, editable report and Excel tools for planning and investment.

Strengths

Nationwide store footprint

Wide nationwide footprint boosts brand visibility and convenience, reaching part of the roughly 90.5 million US households that own pets. Dense store presence enables rapid fulfillment and click-and-collect services, shortening delivery times and improving conversion. Localized assortments align with regional preferences, while stores serve as service hubs that drive repeat visits and loyalty.

Omnichannel integration

Omnichannel integration lets Pet Center link strong e-commerce and stores for seamless journeys—browse online, pick up in-store, or book services digitally—cutting friction via unified inventory and payments; US e-commerce was 15.7% of retail in 2023 and the global pet care market was about $232B in 2023, enabling data-driven targeted marketing across channels.

Full-service pet ecosystem

Integrated veterinary clinics, grooming, and adoption create a one-stop experience that lifts visit frequency and retention; the US pet market was estimated at about $143 billion in 2024, with services capturing a growing share. Services drive higher lifetime value—average annual spend per pet rises when bundled care is offered—and cross-selling between products and services typically increases basket size by double-digit percentages. Adoption initiatives boost community ties and measurable brand goodwill, often translating to higher local store traffic and repeat purchases.

Comprehensive product assortment

Comprehensive assortment covers food, toys and accessories across dogs, cats and small animals, aligning with a US pet market of 136.8 billion in 2023 (APPA), capturing core demand and upsell opportunities. Deep SKU depth supports budget and premium shoppers and multiple species, improving basket size. Reliable in-stock levels build trust and repeat visits; strong vendor ties enable promotions and exclusives.

- Market size: 136.8B (US, 2023)

- Multi-category SKUs: budget to premium

- In-stock = higher repeat visits

- Vendor deals = exclusives & promos

Strong brand recognition

Leader positioning increases top-of-mind awareness, supporting customer retention in a US pet market with $136.8B in spending (APPA, 2022). Consistent service standards reinforce trust and repeat visits, while marketing scale reduces customer acquisition cost per unit. Brand strength enables selective premium pricing in higher-margin categories.

- Leader positioning: higher recall

- Service standards: stronger retention

- Marketing scale: lower CAC

- Brand power: premium pricing

Nationwide pet retail scale: 90.5M households, omnichannel commerce and service-driven loyalty

Extensive nationwide footprint reaches ~90.5M US pet-owning households, enabling fast fulfillment and click-and-collect. Omnichannel integration and unified inventory drive conversion; e-commerce was 15.7% of retail in 2023. Services (vet/grooming/adoption) increase visit frequency and lifetime value. Broad SKU depth and vendor exclusives support premium pricing and repeat purchases.

| Metric | Value |

|---|---|

| US pet households | ~90.5M |

| US pet market | $136.8B (2023); $143B (2024 est.) |

| E‑commerce share | 15.7% (2023) |

What is included in the product

Delivers a strategic overview of Pet Center’s internal capabilities and external market forces, outlining strengths, weaknesses, opportunities, and threats to inform strategic decisions.

Provides a concise Pet Center SWOT matrix that highlights key pain points and priorities for rapid mitigation and resource allocation. Editable format enables quick scenario updates so frontline teams and executives can act on changing risks and opportunities.

Weaknesses

High operating cost base

Large store and clinic networks drive heavy fixed costs; U.S. pet industry spending was $136.8B in 2023 and veterinary services alone totaled about $35.6B, highlighting capital intensity. Rent, staffing and vet equipment compress margins, and utilization swings quickly hit profitability, so strict cost discipline is essential in downturns.

Service quality consistency

Standardizing veterinary and grooming outcomes across locations is difficult and risks variability that can erode trust and online reviews; with the US pet industry at $136.8 billion in 2022 (APPA), services are a material revenue driver. Training and compliance add measurable overhead—often cited as 4–6% of operating costs—and recurring certification needs raise fixed costs. Talent shortages remain acute, with surveys indicating roughly half of clinics reporting staffing gaps, constraining capacity and expansion.

Inventory complexity

Managing tens of thousands of SKUs (Chewy lists ~200,000 products) across channels raises obsolescence risk, especially as pet food shelf life is typically 12–18 months. Heavy pet food drives logistics costs and lifts freight share of COGS, while forecast errors produce ~10% OOS or markdown-driven margin erosion. Cold-chain and prescription items add regulatory and temperature-control constraints and higher per-unit handling costs.

Exposure to domestic macro cycles

Reliance on Brazilian consumer spending makes Pet Center sensitive to domestic cycles, with discretionary segments such as accessories showing higher elasticity and sharper sales swings during downturns.

High inflationary episodes compress margins by raising input costs while dampening demand; BRL volatility further transmits to retail prices for imported pet food and supplies.

- High consumer sensitivity

- Accessories = elastic demand

- Inflation squeezes margins

- Currency risk on imports

Digital experience gaps vs. pure-plays

Online marketplaces deliver broader selection and lower prices, pressuring Pet Center on assortment and margin; average e-commerce conversion was about 2.5% in 2024 (Statista), so slow feature rollout from legacy systems directly hits sales. Delivery speed and shipping cost remain battlegrounds as consumers prioritize fast, low-cost fulfillment, and cart conversion falls without continuous optimization.

- Selection/pricing pressure

- Delivery cost/speed competitiveness

- Legacy IT hinders feature speed

- Low conversion risk ~2.5%

High fixed costs, staffing gaps and SKU complexity are squeezing pet retail margins

Large fixed costs from stores/clinics (U.S. pet spend $136.8B 2023; vet $35.6B) compress margins and magnify utilization swings. Standardizing clinical/grooming quality and filling staffing gaps (~50% clinics report shortages) raise operating overhead. SKU complexity (Chewy ~200k SKUs) drives ~10% obsolescence/OOS; e-commerce conversion ~2.5% slows growth amid delivery/cost pressure and BRL/import volatility.

| Metric | Value |

|---|---|

| U.S. pet spend (2023) | $136.8B |

| Veterinary services (2023) | $35.6B |

| Clinic staffing gap | ~50% |

| SKU breadth (peer) | ~200,000 |

| Obsolescence/OOS | ~10% |

| E‑commerce conversion (2024) | ~2.5% |

Same Document Delivered

Pet Center SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete structure and findings for Pet Center. Purchase unlocks the editable, full-length version for immediate download after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

Pet Center's SWOT reveals resilient brand strength, diversified product mix, and loyal customers, alongside margin pressure and supply-chain vulnerabilities. We outline opportunities—omnichannel expansion and pet wellness trends—and threats like fierce competition and regulatory shifts, with clear strategic options. Purchase the full SWOT analysis to access a professionally written, editable report and Excel tools for planning and investment.

Strengths

Nationwide store footprint

Wide nationwide footprint boosts brand visibility and convenience, reaching part of the roughly 90.5 million US households that own pets. Dense store presence enables rapid fulfillment and click-and-collect services, shortening delivery times and improving conversion. Localized assortments align with regional preferences, while stores serve as service hubs that drive repeat visits and loyalty.

Omnichannel integration

Omnichannel integration lets Pet Center link strong e-commerce and stores for seamless journeys—browse online, pick up in-store, or book services digitally—cutting friction via unified inventory and payments; US e-commerce was 15.7% of retail in 2023 and the global pet care market was about $232B in 2023, enabling data-driven targeted marketing across channels.

Full-service pet ecosystem

Integrated veterinary clinics, grooming, and adoption create a one-stop experience that lifts visit frequency and retention; the US pet market was estimated at about $143 billion in 2024, with services capturing a growing share. Services drive higher lifetime value—average annual spend per pet rises when bundled care is offered—and cross-selling between products and services typically increases basket size by double-digit percentages. Adoption initiatives boost community ties and measurable brand goodwill, often translating to higher local store traffic and repeat purchases.

Comprehensive product assortment

Comprehensive assortment covers food, toys and accessories across dogs, cats and small animals, aligning with a US pet market of 136.8 billion in 2023 (APPA), capturing core demand and upsell opportunities. Deep SKU depth supports budget and premium shoppers and multiple species, improving basket size. Reliable in-stock levels build trust and repeat visits; strong vendor ties enable promotions and exclusives.

- Market size: 136.8B (US, 2023)

- Multi-category SKUs: budget to premium

- In-stock = higher repeat visits

- Vendor deals = exclusives & promos

Strong brand recognition

Leader positioning increases top-of-mind awareness, supporting customer retention in a US pet market with $136.8B in spending (APPA, 2022). Consistent service standards reinforce trust and repeat visits, while marketing scale reduces customer acquisition cost per unit. Brand strength enables selective premium pricing in higher-margin categories.

- Leader positioning: higher recall

- Service standards: stronger retention

- Marketing scale: lower CAC

- Brand power: premium pricing

Nationwide pet retail scale: 90.5M households, omnichannel commerce and service-driven loyalty

Extensive nationwide footprint reaches ~90.5M US pet-owning households, enabling fast fulfillment and click-and-collect. Omnichannel integration and unified inventory drive conversion; e-commerce was 15.7% of retail in 2023. Services (vet/grooming/adoption) increase visit frequency and lifetime value. Broad SKU depth and vendor exclusives support premium pricing and repeat purchases.

| Metric | Value |

|---|---|

| US pet households | ~90.5M |

| US pet market | $136.8B (2023); $143B (2024 est.) |

| E‑commerce share | 15.7% (2023) |

What is included in the product

Delivers a strategic overview of Pet Center’s internal capabilities and external market forces, outlining strengths, weaknesses, opportunities, and threats to inform strategic decisions.

Provides a concise Pet Center SWOT matrix that highlights key pain points and priorities for rapid mitigation and resource allocation. Editable format enables quick scenario updates so frontline teams and executives can act on changing risks and opportunities.

Weaknesses

High operating cost base

Large store and clinic networks drive heavy fixed costs; U.S. pet industry spending was $136.8B in 2023 and veterinary services alone totaled about $35.6B, highlighting capital intensity. Rent, staffing and vet equipment compress margins, and utilization swings quickly hit profitability, so strict cost discipline is essential in downturns.

Service quality consistency

Standardizing veterinary and grooming outcomes across locations is difficult and risks variability that can erode trust and online reviews; with the US pet industry at $136.8 billion in 2022 (APPA), services are a material revenue driver. Training and compliance add measurable overhead—often cited as 4–6% of operating costs—and recurring certification needs raise fixed costs. Talent shortages remain acute, with surveys indicating roughly half of clinics reporting staffing gaps, constraining capacity and expansion.

Inventory complexity

Managing tens of thousands of SKUs (Chewy lists ~200,000 products) across channels raises obsolescence risk, especially as pet food shelf life is typically 12–18 months. Heavy pet food drives logistics costs and lifts freight share of COGS, while forecast errors produce ~10% OOS or markdown-driven margin erosion. Cold-chain and prescription items add regulatory and temperature-control constraints and higher per-unit handling costs.

Exposure to domestic macro cycles

Reliance on Brazilian consumer spending makes Pet Center sensitive to domestic cycles, with discretionary segments such as accessories showing higher elasticity and sharper sales swings during downturns.

High inflationary episodes compress margins by raising input costs while dampening demand; BRL volatility further transmits to retail prices for imported pet food and supplies.

- High consumer sensitivity

- Accessories = elastic demand

- Inflation squeezes margins

- Currency risk on imports

Digital experience gaps vs. pure-plays

Online marketplaces deliver broader selection and lower prices, pressuring Pet Center on assortment and margin; average e-commerce conversion was about 2.5% in 2024 (Statista), so slow feature rollout from legacy systems directly hits sales. Delivery speed and shipping cost remain battlegrounds as consumers prioritize fast, low-cost fulfillment, and cart conversion falls without continuous optimization.

- Selection/pricing pressure

- Delivery cost/speed competitiveness

- Legacy IT hinders feature speed

- Low conversion risk ~2.5%

High fixed costs, staffing gaps and SKU complexity are squeezing pet retail margins

Large fixed costs from stores/clinics (U.S. pet spend $136.8B 2023; vet $35.6B) compress margins and magnify utilization swings. Standardizing clinical/grooming quality and filling staffing gaps (~50% clinics report shortages) raise operating overhead. SKU complexity (Chewy ~200k SKUs) drives ~10% obsolescence/OOS; e-commerce conversion ~2.5% slows growth amid delivery/cost pressure and BRL/import volatility.

| Metric | Value |

|---|---|

| U.S. pet spend (2023) | $136.8B |

| Veterinary services (2023) | $35.6B |

| Clinic staffing gap | ~50% |

| SKU breadth (peer) | ~200,000 |

| Obsolescence/OOS | ~10% |

| E‑commerce conversion (2024) | ~2.5% |

Same Document Delivered

Pet Center SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete structure and findings for Pet Center. Purchase unlocks the editable, full-length version for immediate download after checkout.