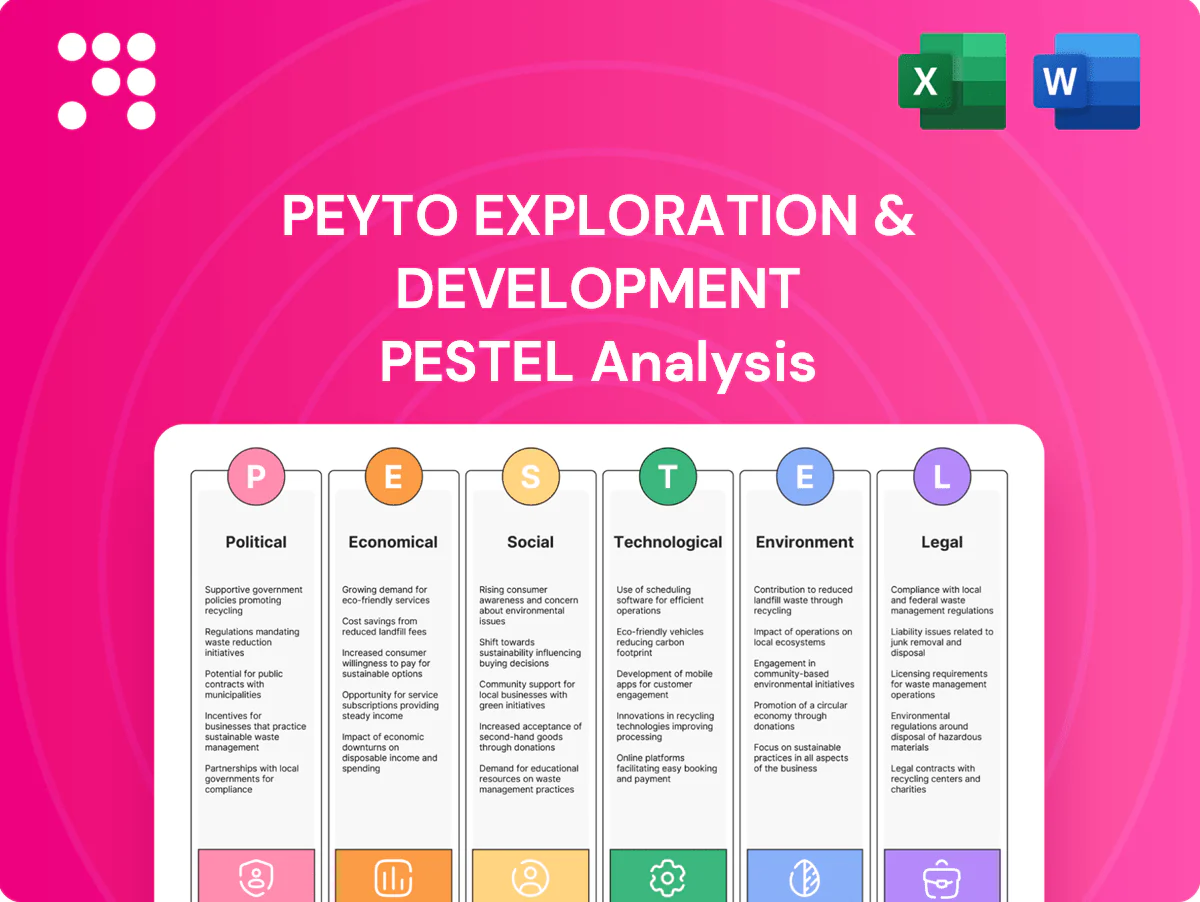

Peyto Exploration & Development PESTLE Analysis

Skip the Research. Get the Strategy.

Gain a strategic edge with our PESTLE analysis of Peyto Exploration & Development. In three to five concise sentences we map political, economic, social, technological, legal and environmental forces shaping growth and risk. Ideal for investors and strategists—download the full report for actionable insights now.

Political factors

Federal carbon pricing and emissions targets

Canada’s federal carbon price (about $65/t in 2023, legislated to rise to ~$170/t by 2030) and an oil & gas methane target of roughly 75% reduction by 2030 materially reshape Peyto’s operating cost curve and project screening. Policy stability or further tightening alters long‑term gas economics and compression CAPEX/OPEX assumptions. Management needs detailed abatement roadmaps to protect margins, while federal or provincial political shifts can accelerate timelines or increase stringency.

Alberta resource governance and royalty stance

Alberta’s Modernized Royalty Framework, implemented in 2016, and the province’s pro-development stance support stronger netbacks and encourage multi-year Deep Basin drilling programs for producers like Peyto. Royalty formulas (gas royalty bands roughly 5–36%) directly affect after-tax returns and capital allocation. Any provincial royalty review or new gas/liquids incentives would likely shift capex priorities. Periodic provincial–federal tensions create regulatory uncertainty windows that can slow permitting and spending.

Pipeline takeaway and interprovincial approvals

Capacity on the NGTL system, roughly 17 Bcf/d, and access to export hubs such as LNG Canada (14 mtpa ≈ 2.1 Bcf/d) are politically sensitive; interprovincial approvals and Indigenous consultations can dictate expansions or constraints. Improved takeaway narrows AECO differentials and boosts Peyto’s realized pricing, while delays increase basis risk and reliance on seasonal storage.

Indigenous relations and benefit agreements

Strong Nation-to-Nation relations are central to project certainty for Peyto in Alberta; the province had 258,640 Indigenous people in 2021, shaping local expectations. Participation, employment and environmental stewardship demands are rising, and constructive engagement lowers political and reputational risk. Missteps have led to permit delays and opposition on energy projects.

- Nation-to-Nation ties reduce delays; rising participation expectations

North American energy security and LNG strategy

North American political support for LNG exports, notably LNG Canada’s 14 mtpa terminal, strengthens long-term gas demand and underpins Peyto’s export-linked pricing prospects; continental alignment with US market dynamics and policy boosts competitiveness versus global suppliers. Geopolitical framing of gas as a transition fuel post-2024 further supports investment and price realization.

- National/provincial backing: LNG Canada 14 mtpa

- US alignment: continental market integration improves access

- Geopolitics: transition-fuel narrative raises valuation

Carbon to ~170/t and methane cuts raise gas costs; export access intact

Federal carbon price ~$65/t (2023), rising to ~170/t by 2030, plus a ~75% methane cut by 2030, materially raises Peyto’s operating costs and CAPEX for abatement. Alberta’s royalty bands (~5–36% gas) and pro-development stance support netbacks but periodic reviews create uncertainty. NGTL capacity ~16–17 Bcf/d and LNG Canada 14 mtpa underpin export access; Indigenous engagement remains critical.

| Metric | Value |

|---|---|

| Federal carbon price (2023) | $65/t |

| 2030 target | $170/t |

| Methane reduction target | ~75% by 2030 |

| NGTL capacity | 16–17 Bcf/d |

| LNG Canada | 14 mtpa |

What is included in the product

Analyzes how Political, Economic, Social, Technological, Environmental and Legal forces—including Alberta/Canada energy policy, gas price cycles, ESG and emissions rules, pipeline capacity, decarbonization technologies and local stakeholder dynamics—uniquely shape Peyto Exploration & Development, delivering data-backed, forward-looking insights to support strategic planning, risk management and investor communications.

Condensed PESTLE of Peyto Exploration & Development, visually segmented and written in plain language to speed stakeholder alignment, support external risk discussions, and drop directly into presentations or planning packs.

Economic factors

AECO price volatility and basis differentials

AECO has shown sharp swings driven by local supply-demand imbalances and frequent pipeline maintenance, with basis widening notably in 2023–24 when AECO traded as much as C$1.50–2.50/GJ below Henry Hub during constrained months. Basis to hubs like Henry Hub (Henry Hub averaged about US$2.85/MMBtu in 2024 per EIA) directly reduces realized prices and increases hedging needs. Diversifying markets and firm transport contracts can smooth cash flows and hedge basis risk. Prolonged weak basis compresses funds from operations and raises capital efficiency thresholds for new wells.

Condensate demand for oil sands diluent

Liquids-rich gas boosts Peyto revenue via condensate sales, which become more valuable when oil sands activity is strong—Canadian oil sands output was about 3.3 million b/d in 2024, underpinning robust diluent demand. Strong diluent pricing in 2024–2025 supported Deep Basin well economics, while oil sands throughput downturns compress condensate premiums. Balancing gas and liquids exposure mitigates cycle risk for Peyto.

Service cost inflation and labor availability

Rising basin activity lifts service costs—rig dayrates, pressure‑pumping and tubing demand—compressing Peyto’s margins unless offset by productivity; Canada’s CPI averaged about 2.9% in 2024 (StatsCan). Scheduling and long‑term vendor partnerships have been used to secure capacity and pricing. Tight labour markets (Canada unemployment ~5.4% in 2024) can extend timelines and increase non‑productive time.

Interest rates, FX, and capital access

Higher rates elevate borrowing costs and hurdle rates; Bank of Canada policy rate at 5.00% (mid‑2025) raises financing costs for Peyto and increases required project IRRs. CAD/USD ~0.74 (mid‑2025) shifts equipment/material costs and links condensate receipts to USD pricing. Peyto's strong balance sheet and hedge book support resilient investment, while gas market and ESG sentiment pressure equity valuation.

- Rate: BoC 5.00%

- FX: CAD/USD ~0.74

- Commodity: Henry Hub ~3 USD/MMBtu (2024 avg)

- Balance: hedges/strong balance sheet bolster cyclicality

Global LNG buildout and North American supply

New global LNG buildout and rising U.S. exports (about 13 Bcf/d of U.S. liquefaction capacity by 2024) can tighten North American balances and lift Henry Hub/AECO prices; storage and weather continue to add seasonal volatility. U.S. shale responsiveness and rising well productivity set marginal supply costs, while Peyto’s low-cost Montney model preserves margins in tight markets and sustains cash flow in weaker cycles.

- US LNG capacity ~13 Bcf/d (2024)

- Storage/weather = seasonal price swings

- Shale productivity defines marginal cost

- Peyto = low-cost, resilient producer

Carbon to ~170/t and methane cuts raise gas costs; export access intact

AECO volatility and C$ basis risk (Henry Hub ~US$2.85/MMBtu 2024) compresses realized prices; BoC rate 5.00% raises financing costs and IRRs. Liquids upside tied to oil sands ~3.3 mb/d (2024) and CAD/USD ~0.74 (mid‑2025). Service inflation (CPI 2.9%, unemployment 5.4%) and US LNG ~13 Bcf/d shape margins; Peyto’s low‑cost Montney model and hedges support resilience.

| Metric | Value |

|---|---|

| BoC Rate | 5.00% |

| Henry Hub (2024) | US$2.85/MMBtu |

| CAD/USD | 0.74 |

| US LNG (2024) | 13 Bcf/d |

Same Document Delivered

Peyto Exploration & Development PESTLE Analysis

The Peyto Exploration & Development PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment. No placeholders or teasers—this is the real, final file.

Skip the Research. Get the Strategy.

Gain a strategic edge with our PESTLE analysis of Peyto Exploration & Development. In three to five concise sentences we map political, economic, social, technological, legal and environmental forces shaping growth and risk. Ideal for investors and strategists—download the full report for actionable insights now.

Political factors

Federal carbon pricing and emissions targets

Canada’s federal carbon price (about $65/t in 2023, legislated to rise to ~$170/t by 2030) and an oil & gas methane target of roughly 75% reduction by 2030 materially reshape Peyto’s operating cost curve and project screening. Policy stability or further tightening alters long‑term gas economics and compression CAPEX/OPEX assumptions. Management needs detailed abatement roadmaps to protect margins, while federal or provincial political shifts can accelerate timelines or increase stringency.

Alberta resource governance and royalty stance

Alberta’s Modernized Royalty Framework, implemented in 2016, and the province’s pro-development stance support stronger netbacks and encourage multi-year Deep Basin drilling programs for producers like Peyto. Royalty formulas (gas royalty bands roughly 5–36%) directly affect after-tax returns and capital allocation. Any provincial royalty review or new gas/liquids incentives would likely shift capex priorities. Periodic provincial–federal tensions create regulatory uncertainty windows that can slow permitting and spending.

Pipeline takeaway and interprovincial approvals

Capacity on the NGTL system, roughly 17 Bcf/d, and access to export hubs such as LNG Canada (14 mtpa ≈ 2.1 Bcf/d) are politically sensitive; interprovincial approvals and Indigenous consultations can dictate expansions or constraints. Improved takeaway narrows AECO differentials and boosts Peyto’s realized pricing, while delays increase basis risk and reliance on seasonal storage.

Indigenous relations and benefit agreements

Strong Nation-to-Nation relations are central to project certainty for Peyto in Alberta; the province had 258,640 Indigenous people in 2021, shaping local expectations. Participation, employment and environmental stewardship demands are rising, and constructive engagement lowers political and reputational risk. Missteps have led to permit delays and opposition on energy projects.

- Nation-to-Nation ties reduce delays; rising participation expectations

North American energy security and LNG strategy

North American political support for LNG exports, notably LNG Canada’s 14 mtpa terminal, strengthens long-term gas demand and underpins Peyto’s export-linked pricing prospects; continental alignment with US market dynamics and policy boosts competitiveness versus global suppliers. Geopolitical framing of gas as a transition fuel post-2024 further supports investment and price realization.

- National/provincial backing: LNG Canada 14 mtpa

- US alignment: continental market integration improves access

- Geopolitics: transition-fuel narrative raises valuation

Carbon to ~170/t and methane cuts raise gas costs; export access intact

Federal carbon price ~$65/t (2023), rising to ~170/t by 2030, plus a ~75% methane cut by 2030, materially raises Peyto’s operating costs and CAPEX for abatement. Alberta’s royalty bands (~5–36% gas) and pro-development stance support netbacks but periodic reviews create uncertainty. NGTL capacity ~16–17 Bcf/d and LNG Canada 14 mtpa underpin export access; Indigenous engagement remains critical.

| Metric | Value |

|---|---|

| Federal carbon price (2023) | $65/t |

| 2030 target | $170/t |

| Methane reduction target | ~75% by 2030 |

| NGTL capacity | 16–17 Bcf/d |

| LNG Canada | 14 mtpa |

What is included in the product

Analyzes how Political, Economic, Social, Technological, Environmental and Legal forces—including Alberta/Canada energy policy, gas price cycles, ESG and emissions rules, pipeline capacity, decarbonization technologies and local stakeholder dynamics—uniquely shape Peyto Exploration & Development, delivering data-backed, forward-looking insights to support strategic planning, risk management and investor communications.

Condensed PESTLE of Peyto Exploration & Development, visually segmented and written in plain language to speed stakeholder alignment, support external risk discussions, and drop directly into presentations or planning packs.

Economic factors

AECO price volatility and basis differentials

AECO has shown sharp swings driven by local supply-demand imbalances and frequent pipeline maintenance, with basis widening notably in 2023–24 when AECO traded as much as C$1.50–2.50/GJ below Henry Hub during constrained months. Basis to hubs like Henry Hub (Henry Hub averaged about US$2.85/MMBtu in 2024 per EIA) directly reduces realized prices and increases hedging needs. Diversifying markets and firm transport contracts can smooth cash flows and hedge basis risk. Prolonged weak basis compresses funds from operations and raises capital efficiency thresholds for new wells.

Condensate demand for oil sands diluent

Liquids-rich gas boosts Peyto revenue via condensate sales, which become more valuable when oil sands activity is strong—Canadian oil sands output was about 3.3 million b/d in 2024, underpinning robust diluent demand. Strong diluent pricing in 2024–2025 supported Deep Basin well economics, while oil sands throughput downturns compress condensate premiums. Balancing gas and liquids exposure mitigates cycle risk for Peyto.

Service cost inflation and labor availability

Rising basin activity lifts service costs—rig dayrates, pressure‑pumping and tubing demand—compressing Peyto’s margins unless offset by productivity; Canada’s CPI averaged about 2.9% in 2024 (StatsCan). Scheduling and long‑term vendor partnerships have been used to secure capacity and pricing. Tight labour markets (Canada unemployment ~5.4% in 2024) can extend timelines and increase non‑productive time.

Interest rates, FX, and capital access

Higher rates elevate borrowing costs and hurdle rates; Bank of Canada policy rate at 5.00% (mid‑2025) raises financing costs for Peyto and increases required project IRRs. CAD/USD ~0.74 (mid‑2025) shifts equipment/material costs and links condensate receipts to USD pricing. Peyto's strong balance sheet and hedge book support resilient investment, while gas market and ESG sentiment pressure equity valuation.

- Rate: BoC 5.00%

- FX: CAD/USD ~0.74

- Commodity: Henry Hub ~3 USD/MMBtu (2024 avg)

- Balance: hedges/strong balance sheet bolster cyclicality

Global LNG buildout and North American supply

New global LNG buildout and rising U.S. exports (about 13 Bcf/d of U.S. liquefaction capacity by 2024) can tighten North American balances and lift Henry Hub/AECO prices; storage and weather continue to add seasonal volatility. U.S. shale responsiveness and rising well productivity set marginal supply costs, while Peyto’s low-cost Montney model preserves margins in tight markets and sustains cash flow in weaker cycles.

- US LNG capacity ~13 Bcf/d (2024)

- Storage/weather = seasonal price swings

- Shale productivity defines marginal cost

- Peyto = low-cost, resilient producer

Carbon to ~170/t and methane cuts raise gas costs; export access intact

AECO volatility and C$ basis risk (Henry Hub ~US$2.85/MMBtu 2024) compresses realized prices; BoC rate 5.00% raises financing costs and IRRs. Liquids upside tied to oil sands ~3.3 mb/d (2024) and CAD/USD ~0.74 (mid‑2025). Service inflation (CPI 2.9%, unemployment 5.4%) and US LNG ~13 Bcf/d shape margins; Peyto’s low‑cost Montney model and hedges support resilience.

| Metric | Value |

|---|---|

| BoC Rate | 5.00% |

| Henry Hub (2024) | US$2.85/MMBtu |

| CAD/USD | 0.74 |

| US LNG (2024) | 13 Bcf/d |

Same Document Delivered

Peyto Exploration & Development PESTLE Analysis

The Peyto Exploration & Development PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment. No placeholders or teasers—this is the real, final file.

Description

Skip the Research. Get the Strategy.

Gain a strategic edge with our PESTLE analysis of Peyto Exploration & Development. In three to five concise sentences we map political, economic, social, technological, legal and environmental forces shaping growth and risk. Ideal for investors and strategists—download the full report for actionable insights now.

Political factors

Federal carbon pricing and emissions targets

Canada’s federal carbon price (about $65/t in 2023, legislated to rise to ~$170/t by 2030) and an oil & gas methane target of roughly 75% reduction by 2030 materially reshape Peyto’s operating cost curve and project screening. Policy stability or further tightening alters long‑term gas economics and compression CAPEX/OPEX assumptions. Management needs detailed abatement roadmaps to protect margins, while federal or provincial political shifts can accelerate timelines or increase stringency.

Alberta resource governance and royalty stance

Alberta’s Modernized Royalty Framework, implemented in 2016, and the province’s pro-development stance support stronger netbacks and encourage multi-year Deep Basin drilling programs for producers like Peyto. Royalty formulas (gas royalty bands roughly 5–36%) directly affect after-tax returns and capital allocation. Any provincial royalty review or new gas/liquids incentives would likely shift capex priorities. Periodic provincial–federal tensions create regulatory uncertainty windows that can slow permitting and spending.

Pipeline takeaway and interprovincial approvals

Capacity on the NGTL system, roughly 17 Bcf/d, and access to export hubs such as LNG Canada (14 mtpa ≈ 2.1 Bcf/d) are politically sensitive; interprovincial approvals and Indigenous consultations can dictate expansions or constraints. Improved takeaway narrows AECO differentials and boosts Peyto’s realized pricing, while delays increase basis risk and reliance on seasonal storage.

Indigenous relations and benefit agreements

Strong Nation-to-Nation relations are central to project certainty for Peyto in Alberta; the province had 258,640 Indigenous people in 2021, shaping local expectations. Participation, employment and environmental stewardship demands are rising, and constructive engagement lowers political and reputational risk. Missteps have led to permit delays and opposition on energy projects.

- Nation-to-Nation ties reduce delays; rising participation expectations

North American energy security and LNG strategy

North American political support for LNG exports, notably LNG Canada’s 14 mtpa terminal, strengthens long-term gas demand and underpins Peyto’s export-linked pricing prospects; continental alignment with US market dynamics and policy boosts competitiveness versus global suppliers. Geopolitical framing of gas as a transition fuel post-2024 further supports investment and price realization.

- National/provincial backing: LNG Canada 14 mtpa

- US alignment: continental market integration improves access

- Geopolitics: transition-fuel narrative raises valuation

Carbon to ~170/t and methane cuts raise gas costs; export access intact

Federal carbon price ~$65/t (2023), rising to ~170/t by 2030, plus a ~75% methane cut by 2030, materially raises Peyto’s operating costs and CAPEX for abatement. Alberta’s royalty bands (~5–36% gas) and pro-development stance support netbacks but periodic reviews create uncertainty. NGTL capacity ~16–17 Bcf/d and LNG Canada 14 mtpa underpin export access; Indigenous engagement remains critical.

| Metric | Value |

|---|---|

| Federal carbon price (2023) | $65/t |

| 2030 target | $170/t |

| Methane reduction target | ~75% by 2030 |

| NGTL capacity | 16–17 Bcf/d |

| LNG Canada | 14 mtpa |

What is included in the product

Analyzes how Political, Economic, Social, Technological, Environmental and Legal forces—including Alberta/Canada energy policy, gas price cycles, ESG and emissions rules, pipeline capacity, decarbonization technologies and local stakeholder dynamics—uniquely shape Peyto Exploration & Development, delivering data-backed, forward-looking insights to support strategic planning, risk management and investor communications.

Condensed PESTLE of Peyto Exploration & Development, visually segmented and written in plain language to speed stakeholder alignment, support external risk discussions, and drop directly into presentations or planning packs.

Economic factors

AECO price volatility and basis differentials

AECO has shown sharp swings driven by local supply-demand imbalances and frequent pipeline maintenance, with basis widening notably in 2023–24 when AECO traded as much as C$1.50–2.50/GJ below Henry Hub during constrained months. Basis to hubs like Henry Hub (Henry Hub averaged about US$2.85/MMBtu in 2024 per EIA) directly reduces realized prices and increases hedging needs. Diversifying markets and firm transport contracts can smooth cash flows and hedge basis risk. Prolonged weak basis compresses funds from operations and raises capital efficiency thresholds for new wells.

Condensate demand for oil sands diluent

Liquids-rich gas boosts Peyto revenue via condensate sales, which become more valuable when oil sands activity is strong—Canadian oil sands output was about 3.3 million b/d in 2024, underpinning robust diluent demand. Strong diluent pricing in 2024–2025 supported Deep Basin well economics, while oil sands throughput downturns compress condensate premiums. Balancing gas and liquids exposure mitigates cycle risk for Peyto.

Service cost inflation and labor availability

Rising basin activity lifts service costs—rig dayrates, pressure‑pumping and tubing demand—compressing Peyto’s margins unless offset by productivity; Canada’s CPI averaged about 2.9% in 2024 (StatsCan). Scheduling and long‑term vendor partnerships have been used to secure capacity and pricing. Tight labour markets (Canada unemployment ~5.4% in 2024) can extend timelines and increase non‑productive time.

Interest rates, FX, and capital access

Higher rates elevate borrowing costs and hurdle rates; Bank of Canada policy rate at 5.00% (mid‑2025) raises financing costs for Peyto and increases required project IRRs. CAD/USD ~0.74 (mid‑2025) shifts equipment/material costs and links condensate receipts to USD pricing. Peyto's strong balance sheet and hedge book support resilient investment, while gas market and ESG sentiment pressure equity valuation.

- Rate: BoC 5.00%

- FX: CAD/USD ~0.74

- Commodity: Henry Hub ~3 USD/MMBtu (2024 avg)

- Balance: hedges/strong balance sheet bolster cyclicality

Global LNG buildout and North American supply

New global LNG buildout and rising U.S. exports (about 13 Bcf/d of U.S. liquefaction capacity by 2024) can tighten North American balances and lift Henry Hub/AECO prices; storage and weather continue to add seasonal volatility. U.S. shale responsiveness and rising well productivity set marginal supply costs, while Peyto’s low-cost Montney model preserves margins in tight markets and sustains cash flow in weaker cycles.

- US LNG capacity ~13 Bcf/d (2024)

- Storage/weather = seasonal price swings

- Shale productivity defines marginal cost

- Peyto = low-cost, resilient producer

Carbon to ~170/t and methane cuts raise gas costs; export access intact

AECO volatility and C$ basis risk (Henry Hub ~US$2.85/MMBtu 2024) compresses realized prices; BoC rate 5.00% raises financing costs and IRRs. Liquids upside tied to oil sands ~3.3 mb/d (2024) and CAD/USD ~0.74 (mid‑2025). Service inflation (CPI 2.9%, unemployment 5.4%) and US LNG ~13 Bcf/d shape margins; Peyto’s low‑cost Montney model and hedges support resilience.

| Metric | Value |

|---|---|

| BoC Rate | 5.00% |

| Henry Hub (2024) | US$2.85/MMBtu |

| CAD/USD | 0.74 |

| US LNG (2024) | 13 Bcf/d |

Same Document Delivered

Peyto Exploration & Development PESTLE Analysis

The Peyto Exploration & Development PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment. No placeholders or teasers—this is the real, final file.