Deutsche Pfandbriefbank PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

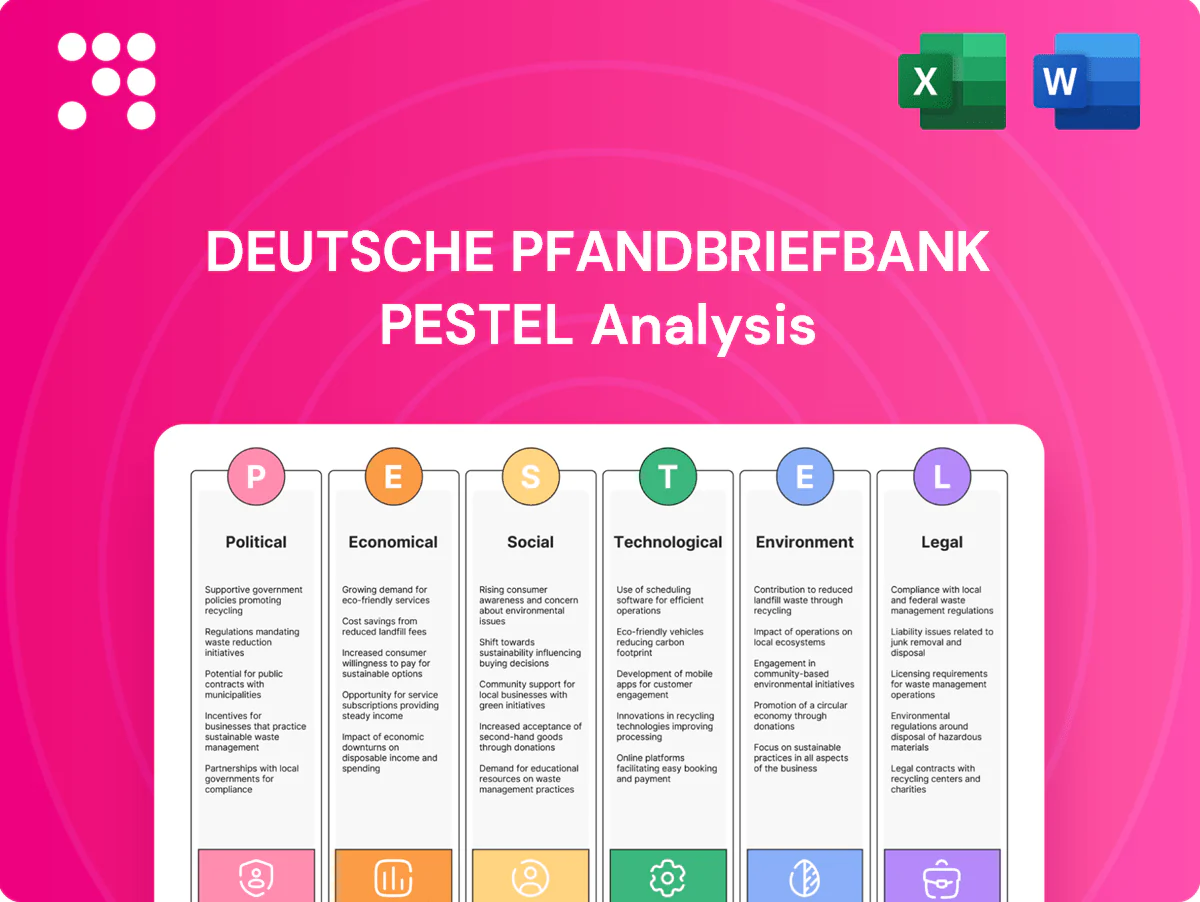

Unlock strategic clarity with our concise PESTLE Analysis of Deutsche Pfandbriefbank—spot how political regulation, economic cycles, social trends, technological shifts, and environmental and legal pressures shape its outlook. Ideal for investors, advisors, and strategists, this briefing highlights risks and opportunities you can act on today. Purchase the full report to access detailed data, actionable recommendations, and editable charts.

Political factors

EU policy direction and banking supervision

As an ECB‑supervised institution, pbb is directly affected by EU banking union priorities and macro‑prudential tools; regulatory minima (CET1 4.5%) plus the 2.5% capital conservation buffer create a 7.0% common baseline capital need for banks in the euro area.

Shifts in counter‑cyclical buffer or systemic add‑ons can materially alter pbb’s lending capacity and covered‑bond issuance economics.

EU cohesion and energy‑transition programmes drive public‑sector financing demand that pbb targets, while political stability in Germany and core EU markets underpins Pfandbrief funding conditions and investor confidence.

Geopolitics, sanctions, and regional security

Heightened geopolitical tensions raise risk premiums and dent property investor sentiment. Sanctions — EU measures since 2014 and expanded after Russia’s 2022 invasion — can disrupt cross‑border transactions and tenant demand in logistics and office sectors. Rising defense and infrastructure priorities, highlighted by the NATO 2% of GDP guideline, may increase public‑sector financing needs. Political fragmentation can slow approvals for large projects and urban redevelopment.

Public infrastructure agendas

Government stimulus for transport, digital and social infrastructure underpins pbb’s public investment finance pipeline, with EU Recovery and Resilience Facility funding totalling €723.8bn supporting national programmes. Fiscal rules and federal-municipal budget debates determine the pace of project origination at municipalities. PPP frameworks and procurement policies shape risk allocation and bankability. Election cycles (four-year federal terms) can reprioritise sectors and timing of disbursements.

Housing and urban policy shifts

Rent controls, zoning reforms and housing subsidies materially affect residential cash flows and collateral values for Deutsche Pfandbriefbank, compressing yields in regulated markets and raising loss-given-default risk where rents lag inflation; office vacancy hit about 8% in Germany in 2024, heightening pressure for conversions and altering underwriting assumptions.

- Rent controls: lower cash yields

- Zoning/subsidies: mixed collateral impacts

- Office-to-resi: viability risk (2024 vacancy ~8%)

- Local heterogeneity: underwriting complexity

Transatlantic policy divergence

Transatlantic policy divergence—US rates at ~5.25–5.50% vs ECB deposit ~4.00% in 2024–25—raises funding and FX stress for pbb’s North American exposures, increasing hedging costs and prompting portfolio rebalancing.

Divergent climate and building codes (EU net-zero 2030/2050 targets vs US state-led standards) alter collateral standards and due diligence, while trade and visa shifts influence demand for office, retail and hospitality assets.

- policy/funding: higher US rates → costlier dollar funding

- fx: EUR/USD volatility affects NAV and hedging

- collateral: differing climate regulations change LTV and capex needs

- demand: visa/trade shifts impact occupational demand in CRE

ECB CET1 minima (7.0%) and RRF reshape bond supply amid higher US/EU rates

ECB supervision and CET1 minima (4.5% + 2.5% buffer = 7.0%) constrain pbb’s capital and covered‑bond issuance; counter‑cyclical buffers can tighten lending. EU RRF of €723.8bn and German stability boost public‑sector origination while geopolitical tensions and sanctions raise risk premia; German office vacancy ~8% (2024). US rates ~5.25–5.50% vs ECB ~4.0% increase hedging/funding costs.

| Metric | Value |

|---|---|

| CET1 baseline | 7.0% |

| EU RRF | €723.8bn |

| DE office vacancy (2024) | ~8% |

| Policy rates (US/EU 2024–25) | 5.25–5.50% / ~4.0% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Deutsche Pfandbriefbank, with data-backed insights on regional/regulatory dynamics, forward-looking scenario guidance, and actionable implications for executives, investors, and strategists—formatted for direct insertion into reports and plans.

A concise, visually segmented PESTLE summary for Deutsche Pfandbriefbank that clarifies regulatory, macroeconomic, and real estate market risks, ready to drop into presentations or planning sessions for quick team alignment and decision-making.

Economic factors

Interest rate cycle and CRE valuations

Interest rate levels directly drive cap rates, DSCRs and refinancing risk across office, retail, logistics and residential, pressuring valuations and borrower servicing capacity.

Rapid repricing tightens LTV cushions and can elevate Stage 2/3 loan migration, while stabilization or cuts typically revive transaction volumes and fee income.

With the ECB deposit rate at 4.00% and 5y EUR swaps near 3.7% (July 2025), higher hedging costs and basis dynamics weigh on net interest margin.

Macro growth and labor markets

GDP growth drives tenant demand and rent trajectories: Germany expanded about 0.6% in 2024, euro area ~0.7% and the US ~2.5% in 2024, so weak growth hits office and retail harder than logistics and residential. Employment remained tight (Germany unemployment ~3.4% in 2024), supporting household formation but pushing construction costs up ~6% YoY, while Pfandbriefbank’s US and core‑EU exposures increase cyclicality.

Inflation and construction inputs

Construction cost inflation (Baupreisindex up about 5% y/y in 2024) erodes project feasibility and borrower equity cushions, raising loan-to-cost risks for Deutsche Pfandbriefbank. Higher operating costs cut NOI, notably for energy-inefficient assets. German CPI ~2.5% (2024) shapes rent indexation and real returns, while ECB policy rate ~4.00% (mid‑2025) feeds through to funding spreads and loan pricing.

Funding market conditions

Covered bond and unsecured markets set Pfandbriefbank’s funding cost and lending appetite; the European covered‑bond market exceeded €1.2 trillion in 2024, anchoring benchmarks and pricing. Spread volatility in 2024–25 compressed originations and pushed lenders toward lower‑risk assets. Investor demand for Pfandbriefe depends on credit perception and collateral quality, while narrow liquidity windows dictate issuance timing and portfolio growth.

- Market size: >€1.2 trillion (covered bonds, 2024)

- Effect: spreads → slower originations, safer product mix

- Driver: investor focus on credit & collateral quality

- Timing: issuance governed by liquidity windows

Sectoral divergences within CRE

Logistics (vacancy ~3.5% in 2024) and residential (price growth ~4% in 2024) have shown resilience, while offices face structural headwinds (German office vacancy ~7.5% in 2024). Retail is bifurcated: prime assets stable, secondary under pressure; hospitality is cyclical with RevPAR recovery ~+18% YoY into 2024 as travel rebounds. Sector mix and geography therefore materially drive risk‑adjusted returns and provisioning.

- Logistics: low vacancy ~3.5% (2024)

- Residential: price growth ~4% (2024)

- Offices: vacancy ~7.5% (2024)

- Hospitality: RevPAR +18% YoY (2024)

ECB CET1 minima (7.0%) and RRF reshape bond supply amid higher US/EU rates

Higher ECB rates (deposit 4.00% mid‑2025) and 5y swaps ~3.7% raise funding and hedging costs, compressing NIMs and originations. Weak GDP (Germany 0.6% 2024) and construction inflation (~5% y/y) squeeze valuations and LTV cushions; sector mix (office vacancy 7.5% vs logistics 3.5%) drives provisioning.

| Metric | 2024/25 |

|---|---|

| ECB deposit rate | 4.00% (mid‑2025) |

| 5y EUR swap | ~3.7% (Jul 2025) |

| Germany GDP | 0.6% (2024) |

| Construction inflation | ~5% y/y (2024) |

Preview Before You Purchase

Deutsche Pfandbriefbank PESTLE Analysis

This Deutsche Pfandbriefbank PESTLE Analysis is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, structure, and insights shown in the preview are identical to the file you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured product.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our concise PESTLE Analysis of Deutsche Pfandbriefbank—spot how political regulation, economic cycles, social trends, technological shifts, and environmental and legal pressures shape its outlook. Ideal for investors, advisors, and strategists, this briefing highlights risks and opportunities you can act on today. Purchase the full report to access detailed data, actionable recommendations, and editable charts.

Political factors

EU policy direction and banking supervision

As an ECB‑supervised institution, pbb is directly affected by EU banking union priorities and macro‑prudential tools; regulatory minima (CET1 4.5%) plus the 2.5% capital conservation buffer create a 7.0% common baseline capital need for banks in the euro area.

Shifts in counter‑cyclical buffer or systemic add‑ons can materially alter pbb’s lending capacity and covered‑bond issuance economics.

EU cohesion and energy‑transition programmes drive public‑sector financing demand that pbb targets, while political stability in Germany and core EU markets underpins Pfandbrief funding conditions and investor confidence.

Geopolitics, sanctions, and regional security

Heightened geopolitical tensions raise risk premiums and dent property investor sentiment. Sanctions — EU measures since 2014 and expanded after Russia’s 2022 invasion — can disrupt cross‑border transactions and tenant demand in logistics and office sectors. Rising defense and infrastructure priorities, highlighted by the NATO 2% of GDP guideline, may increase public‑sector financing needs. Political fragmentation can slow approvals for large projects and urban redevelopment.

Public infrastructure agendas

Government stimulus for transport, digital and social infrastructure underpins pbb’s public investment finance pipeline, with EU Recovery and Resilience Facility funding totalling €723.8bn supporting national programmes. Fiscal rules and federal-municipal budget debates determine the pace of project origination at municipalities. PPP frameworks and procurement policies shape risk allocation and bankability. Election cycles (four-year federal terms) can reprioritise sectors and timing of disbursements.

Housing and urban policy shifts

Rent controls, zoning reforms and housing subsidies materially affect residential cash flows and collateral values for Deutsche Pfandbriefbank, compressing yields in regulated markets and raising loss-given-default risk where rents lag inflation; office vacancy hit about 8% in Germany in 2024, heightening pressure for conversions and altering underwriting assumptions.

- Rent controls: lower cash yields

- Zoning/subsidies: mixed collateral impacts

- Office-to-resi: viability risk (2024 vacancy ~8%)

- Local heterogeneity: underwriting complexity

Transatlantic policy divergence

Transatlantic policy divergence—US rates at ~5.25–5.50% vs ECB deposit ~4.00% in 2024–25—raises funding and FX stress for pbb’s North American exposures, increasing hedging costs and prompting portfolio rebalancing.

Divergent climate and building codes (EU net-zero 2030/2050 targets vs US state-led standards) alter collateral standards and due diligence, while trade and visa shifts influence demand for office, retail and hospitality assets.

- policy/funding: higher US rates → costlier dollar funding

- fx: EUR/USD volatility affects NAV and hedging

- collateral: differing climate regulations change LTV and capex needs

- demand: visa/trade shifts impact occupational demand in CRE

ECB CET1 minima (7.0%) and RRF reshape bond supply amid higher US/EU rates

ECB supervision and CET1 minima (4.5% + 2.5% buffer = 7.0%) constrain pbb’s capital and covered‑bond issuance; counter‑cyclical buffers can tighten lending. EU RRF of €723.8bn and German stability boost public‑sector origination while geopolitical tensions and sanctions raise risk premia; German office vacancy ~8% (2024). US rates ~5.25–5.50% vs ECB ~4.0% increase hedging/funding costs.

| Metric | Value |

|---|---|

| CET1 baseline | 7.0% |

| EU RRF | €723.8bn |

| DE office vacancy (2024) | ~8% |

| Policy rates (US/EU 2024–25) | 5.25–5.50% / ~4.0% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Deutsche Pfandbriefbank, with data-backed insights on regional/regulatory dynamics, forward-looking scenario guidance, and actionable implications for executives, investors, and strategists—formatted for direct insertion into reports and plans.

A concise, visually segmented PESTLE summary for Deutsche Pfandbriefbank that clarifies regulatory, macroeconomic, and real estate market risks, ready to drop into presentations or planning sessions for quick team alignment and decision-making.

Economic factors

Interest rate cycle and CRE valuations

Interest rate levels directly drive cap rates, DSCRs and refinancing risk across office, retail, logistics and residential, pressuring valuations and borrower servicing capacity.

Rapid repricing tightens LTV cushions and can elevate Stage 2/3 loan migration, while stabilization or cuts typically revive transaction volumes and fee income.

With the ECB deposit rate at 4.00% and 5y EUR swaps near 3.7% (July 2025), higher hedging costs and basis dynamics weigh on net interest margin.

Macro growth and labor markets

GDP growth drives tenant demand and rent trajectories: Germany expanded about 0.6% in 2024, euro area ~0.7% and the US ~2.5% in 2024, so weak growth hits office and retail harder than logistics and residential. Employment remained tight (Germany unemployment ~3.4% in 2024), supporting household formation but pushing construction costs up ~6% YoY, while Pfandbriefbank’s US and core‑EU exposures increase cyclicality.

Inflation and construction inputs

Construction cost inflation (Baupreisindex up about 5% y/y in 2024) erodes project feasibility and borrower equity cushions, raising loan-to-cost risks for Deutsche Pfandbriefbank. Higher operating costs cut NOI, notably for energy-inefficient assets. German CPI ~2.5% (2024) shapes rent indexation and real returns, while ECB policy rate ~4.00% (mid‑2025) feeds through to funding spreads and loan pricing.

Funding market conditions

Covered bond and unsecured markets set Pfandbriefbank’s funding cost and lending appetite; the European covered‑bond market exceeded €1.2 trillion in 2024, anchoring benchmarks and pricing. Spread volatility in 2024–25 compressed originations and pushed lenders toward lower‑risk assets. Investor demand for Pfandbriefe depends on credit perception and collateral quality, while narrow liquidity windows dictate issuance timing and portfolio growth.

- Market size: >€1.2 trillion (covered bonds, 2024)

- Effect: spreads → slower originations, safer product mix

- Driver: investor focus on credit & collateral quality

- Timing: issuance governed by liquidity windows

Sectoral divergences within CRE

Logistics (vacancy ~3.5% in 2024) and residential (price growth ~4% in 2024) have shown resilience, while offices face structural headwinds (German office vacancy ~7.5% in 2024). Retail is bifurcated: prime assets stable, secondary under pressure; hospitality is cyclical with RevPAR recovery ~+18% YoY into 2024 as travel rebounds. Sector mix and geography therefore materially drive risk‑adjusted returns and provisioning.

- Logistics: low vacancy ~3.5% (2024)

- Residential: price growth ~4% (2024)

- Offices: vacancy ~7.5% (2024)

- Hospitality: RevPAR +18% YoY (2024)

ECB CET1 minima (7.0%) and RRF reshape bond supply amid higher US/EU rates

Higher ECB rates (deposit 4.00% mid‑2025) and 5y swaps ~3.7% raise funding and hedging costs, compressing NIMs and originations. Weak GDP (Germany 0.6% 2024) and construction inflation (~5% y/y) squeeze valuations and LTV cushions; sector mix (office vacancy 7.5% vs logistics 3.5%) drives provisioning.

| Metric | 2024/25 |

|---|---|

| ECB deposit rate | 4.00% (mid‑2025) |

| 5y EUR swap | ~3.7% (Jul 2025) |

| Germany GDP | 0.6% (2024) |

| Construction inflation | ~5% y/y (2024) |

Preview Before You Purchase

Deutsche Pfandbriefbank PESTLE Analysis

This Deutsche Pfandbriefbank PESTLE Analysis is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, structure, and insights shown in the preview are identical to the file you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured product.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our concise PESTLE Analysis of Deutsche Pfandbriefbank—spot how political regulation, economic cycles, social trends, technological shifts, and environmental and legal pressures shape its outlook. Ideal for investors, advisors, and strategists, this briefing highlights risks and opportunities you can act on today. Purchase the full report to access detailed data, actionable recommendations, and editable charts.

Political factors

EU policy direction and banking supervision

As an ECB‑supervised institution, pbb is directly affected by EU banking union priorities and macro‑prudential tools; regulatory minima (CET1 4.5%) plus the 2.5% capital conservation buffer create a 7.0% common baseline capital need for banks in the euro area.

Shifts in counter‑cyclical buffer or systemic add‑ons can materially alter pbb’s lending capacity and covered‑bond issuance economics.

EU cohesion and energy‑transition programmes drive public‑sector financing demand that pbb targets, while political stability in Germany and core EU markets underpins Pfandbrief funding conditions and investor confidence.

Geopolitics, sanctions, and regional security

Heightened geopolitical tensions raise risk premiums and dent property investor sentiment. Sanctions — EU measures since 2014 and expanded after Russia’s 2022 invasion — can disrupt cross‑border transactions and tenant demand in logistics and office sectors. Rising defense and infrastructure priorities, highlighted by the NATO 2% of GDP guideline, may increase public‑sector financing needs. Political fragmentation can slow approvals for large projects and urban redevelopment.

Public infrastructure agendas

Government stimulus for transport, digital and social infrastructure underpins pbb’s public investment finance pipeline, with EU Recovery and Resilience Facility funding totalling €723.8bn supporting national programmes. Fiscal rules and federal-municipal budget debates determine the pace of project origination at municipalities. PPP frameworks and procurement policies shape risk allocation and bankability. Election cycles (four-year federal terms) can reprioritise sectors and timing of disbursements.

Housing and urban policy shifts

Rent controls, zoning reforms and housing subsidies materially affect residential cash flows and collateral values for Deutsche Pfandbriefbank, compressing yields in regulated markets and raising loss-given-default risk where rents lag inflation; office vacancy hit about 8% in Germany in 2024, heightening pressure for conversions and altering underwriting assumptions.

- Rent controls: lower cash yields

- Zoning/subsidies: mixed collateral impacts

- Office-to-resi: viability risk (2024 vacancy ~8%)

- Local heterogeneity: underwriting complexity

Transatlantic policy divergence

Transatlantic policy divergence—US rates at ~5.25–5.50% vs ECB deposit ~4.00% in 2024–25—raises funding and FX stress for pbb’s North American exposures, increasing hedging costs and prompting portfolio rebalancing.

Divergent climate and building codes (EU net-zero 2030/2050 targets vs US state-led standards) alter collateral standards and due diligence, while trade and visa shifts influence demand for office, retail and hospitality assets.

- policy/funding: higher US rates → costlier dollar funding

- fx: EUR/USD volatility affects NAV and hedging

- collateral: differing climate regulations change LTV and capex needs

- demand: visa/trade shifts impact occupational demand in CRE

ECB CET1 minima (7.0%) and RRF reshape bond supply amid higher US/EU rates

ECB supervision and CET1 minima (4.5% + 2.5% buffer = 7.0%) constrain pbb’s capital and covered‑bond issuance; counter‑cyclical buffers can tighten lending. EU RRF of €723.8bn and German stability boost public‑sector origination while geopolitical tensions and sanctions raise risk premia; German office vacancy ~8% (2024). US rates ~5.25–5.50% vs ECB ~4.0% increase hedging/funding costs.

| Metric | Value |

|---|---|

| CET1 baseline | 7.0% |

| EU RRF | €723.8bn |

| DE office vacancy (2024) | ~8% |

| Policy rates (US/EU 2024–25) | 5.25–5.50% / ~4.0% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Deutsche Pfandbriefbank, with data-backed insights on regional/regulatory dynamics, forward-looking scenario guidance, and actionable implications for executives, investors, and strategists—formatted for direct insertion into reports and plans.

A concise, visually segmented PESTLE summary for Deutsche Pfandbriefbank that clarifies regulatory, macroeconomic, and real estate market risks, ready to drop into presentations or planning sessions for quick team alignment and decision-making.

Economic factors

Interest rate cycle and CRE valuations

Interest rate levels directly drive cap rates, DSCRs and refinancing risk across office, retail, logistics and residential, pressuring valuations and borrower servicing capacity.

Rapid repricing tightens LTV cushions and can elevate Stage 2/3 loan migration, while stabilization or cuts typically revive transaction volumes and fee income.

With the ECB deposit rate at 4.00% and 5y EUR swaps near 3.7% (July 2025), higher hedging costs and basis dynamics weigh on net interest margin.

Macro growth and labor markets

GDP growth drives tenant demand and rent trajectories: Germany expanded about 0.6% in 2024, euro area ~0.7% and the US ~2.5% in 2024, so weak growth hits office and retail harder than logistics and residential. Employment remained tight (Germany unemployment ~3.4% in 2024), supporting household formation but pushing construction costs up ~6% YoY, while Pfandbriefbank’s US and core‑EU exposures increase cyclicality.

Inflation and construction inputs

Construction cost inflation (Baupreisindex up about 5% y/y in 2024) erodes project feasibility and borrower equity cushions, raising loan-to-cost risks for Deutsche Pfandbriefbank. Higher operating costs cut NOI, notably for energy-inefficient assets. German CPI ~2.5% (2024) shapes rent indexation and real returns, while ECB policy rate ~4.00% (mid‑2025) feeds through to funding spreads and loan pricing.

Funding market conditions

Covered bond and unsecured markets set Pfandbriefbank’s funding cost and lending appetite; the European covered‑bond market exceeded €1.2 trillion in 2024, anchoring benchmarks and pricing. Spread volatility in 2024–25 compressed originations and pushed lenders toward lower‑risk assets. Investor demand for Pfandbriefe depends on credit perception and collateral quality, while narrow liquidity windows dictate issuance timing and portfolio growth.

- Market size: >€1.2 trillion (covered bonds, 2024)

- Effect: spreads → slower originations, safer product mix

- Driver: investor focus on credit & collateral quality

- Timing: issuance governed by liquidity windows

Sectoral divergences within CRE

Logistics (vacancy ~3.5% in 2024) and residential (price growth ~4% in 2024) have shown resilience, while offices face structural headwinds (German office vacancy ~7.5% in 2024). Retail is bifurcated: prime assets stable, secondary under pressure; hospitality is cyclical with RevPAR recovery ~+18% YoY into 2024 as travel rebounds. Sector mix and geography therefore materially drive risk‑adjusted returns and provisioning.

- Logistics: low vacancy ~3.5% (2024)

- Residential: price growth ~4% (2024)

- Offices: vacancy ~7.5% (2024)

- Hospitality: RevPAR +18% YoY (2024)

ECB CET1 minima (7.0%) and RRF reshape bond supply amid higher US/EU rates

Higher ECB rates (deposit 4.00% mid‑2025) and 5y swaps ~3.7% raise funding and hedging costs, compressing NIMs and originations. Weak GDP (Germany 0.6% 2024) and construction inflation (~5% y/y) squeeze valuations and LTV cushions; sector mix (office vacancy 7.5% vs logistics 3.5%) drives provisioning.

| Metric | 2024/25 |

|---|---|

| ECB deposit rate | 4.00% (mid‑2025) |

| 5y EUR swap | ~3.7% (Jul 2025) |

| Germany GDP | 0.6% (2024) |

| Construction inflation | ~5% y/y (2024) |

Preview Before You Purchase

Deutsche Pfandbriefbank PESTLE Analysis

This Deutsche Pfandbriefbank PESTLE Analysis is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, structure, and insights shown in the preview are identical to the file you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured product.