Phonero Porter's Five Forces Analysis

From Overview to Strategy Blueprint

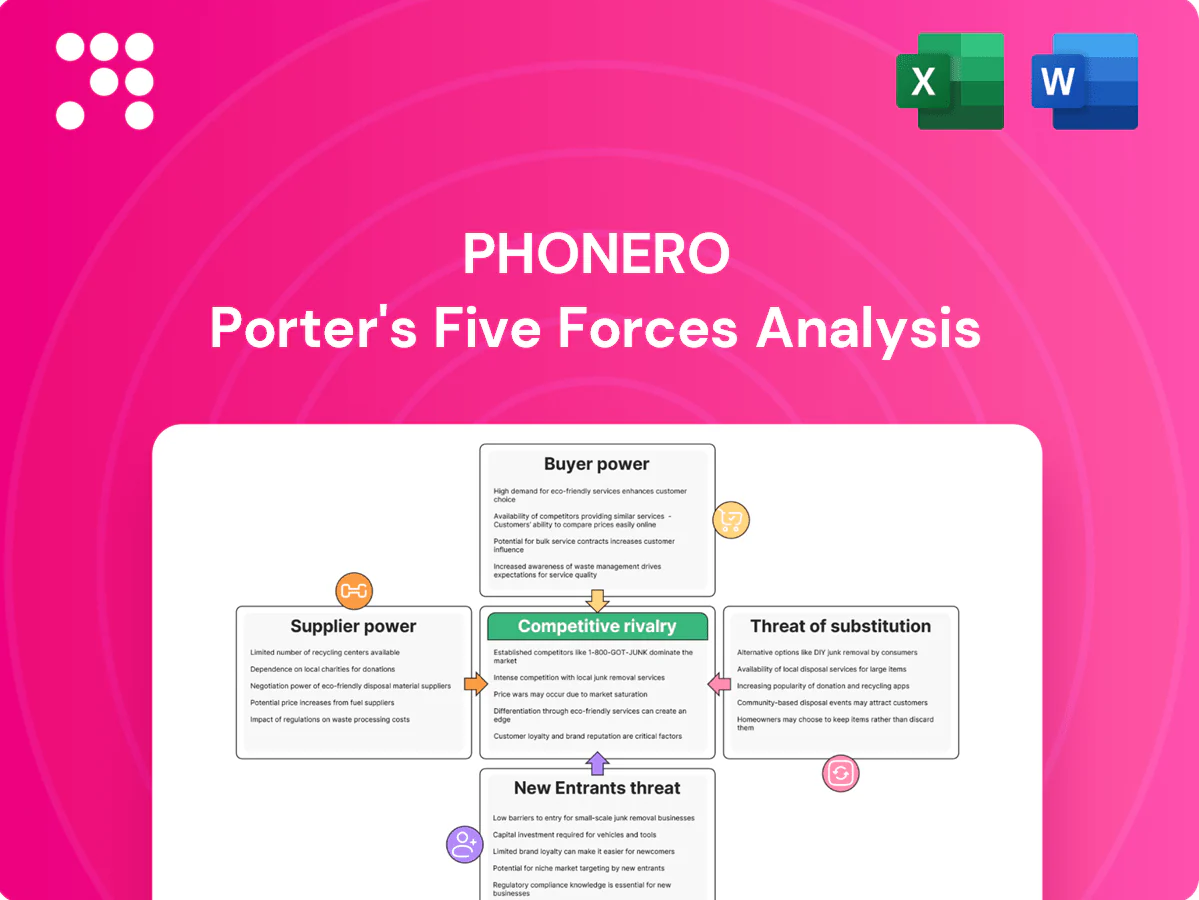

Phonero’s Porter's Five Forces snapshot highlights competitive rivalry, buyer and supplier power, entry barriers, and substitute threats, revealing strategic pressures shaping its margins. This brief overview teases key findings and tactical implications. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Concentrated network and spectrum owners

Phonero depends on a few Norwegian MNOs for radio access and spectrum, concentrating upstream bargaining power: Norway had three nationwide MNOs in 2024, limiting wholesale alternatives. Limited alternatives enable suppliers to dictate pricing and technical terms and long-term access and roaming agreements can lock in costs and features. Any supplier network changes can immediately ripple into service quality and SLA performance.

Handset and device ecosystem leverage

Global OEMs exert strong leverage: Apple reported roughly $205 billion in iPhone revenue for fiscal 2024, while Samsung remains the largest shipper, concentrating value and limiting device margin and customization for carriers. Enterprise contracts that mandate specific devices reduce Phonero’s purchasing flexibility. Volume rebates and handset subsidies skew toward large operators, and 2024 supply‑chain disruptions tended to prioritize bigger buyers, compressing options for mid‑sized providers.

UCaaS and cloud platform dependencies

Integration with Microsoft Teams, Zoom and other UC platforms creates reliance on third-party roadmaps, fee structures and certification cycles, raising supplier bargaining power. API access, certification and co-marketing terms can be costly and subject to platform policy changes that may disrupt bundled offers. Negotiating leverage improves materially as Phonero scales activated seats with enterprise customers.

Network equipment and tower providers

Vendors for core, security and OSS/BSS are concentrated and sticky, driving material switching costs for Phonero; 5G SA rollouts in 2023–24 forced synchronized core and RAN upgrades with vendor-dependent pricing. Tower and fiber contracts commonly include inflation- or CPI-linked escalators, and service credits seldom cover the commercial impact of outages.

- Concentration: few core/OSS/BSS suppliers

- Upgrade alignment: 4G→5G SA raises capex

- Escalators: inflation-linked tower/fiber fees

- Risk: service credits rarely offset outage losses

IoT module and eSIM suppliers

IoT growth ties Phonero closely to SIM/eSIM providers and module vendors because components are standardized but price-sensitive; global cellular IoT connections surpassed 3.1 billion in 2024, keeping downward price pressure. Certification per device and band adds months and often +5–12% unit cost. Global roaming partners shape IoT pricing footprints; suppliers gain leverage when enterprises demand multi-country profiles.

- Dependency: standardized, low-margin modules

- Cost impact: certification +5–12% per device

- Leverage: multi-country eSIM profiles raise supplier power

High supplier power: 3 nationwide MNOs push up access; IoT scale and cert add costs

Supplier power is high: three Norwegian nationwide MNOs in 2024 concentrate wholesale leverage, raising access and roaming costs. Global OEMs (Apple iPhone revenue ≈ $205B in fiscal 2024) and concentrated OSS/BSS vendors limit device margins and increase switching costs. IoT scale (3.1B cellular connections in 2024) pressures module pricing; certification adds +5–12% unit cost.

| Metric | 2024 Value |

|---|---|

| Norway nationwide MNOs | 3 |

| iPhone revenue (fiscal) | $205B |

| Cellular IoT connections | 3.1B |

| Certification cost | +5–12% |

What is included in the product

Tailored Porter's Five Forces for Phonero uncover competitive intensity, buyer/supplier leverage, threats from substitutes and entrants, and strategic levers to protect margins.

Clear one-sheet Porter's Five Forces for Phonero—instantly visualize competitive pressure with a spider chart and customizable force levels, ready to drop into decks or Excel dashboards to simplify strategic decisions and reduce analysis time.

Customers Bargaining Power

Corporate RFP scale and sophistication

Enterprise customers run rigorous tenders, benchmark tariffs, and demand customization, negotiating term discounts, pooled data arrangements and SLA penalties that compress margins for Phonero.

Low switching costs via portability

Number portability in the EEA is typically completed within one working day in 2024, and widespread eSIM support on modern handsets has made carrier migration nearly instant. Standardized mobile bundles across voice, data and streaming make offers directly comparable, compressing price differentiation. Shorter contract terms (many plans now 12 months or less) raise churn risk, forcing Phonero to invest in service and feature-based retention beyond price.

Demand for integrated UC and security

Clients now demand seamless mobile-UC integration, compliance and zero-trust features, with a 2024 industry survey showing over 50% of buyers make integration a purchase prerequisite. Deals are lost despite competitive pricing if vendors fail integration or API deliverables. Buyers increasingly insist on managed services and 24/7 support without large premiums and require tailored reporting and APIs as mandatory contract items.

Service quality and coverage expectations

Business customers demand consistent nationwide coverage, reliable VoLTE/VoWiFi and strong indoor performance; SLA breaches in 2024 commonly trigger service credits or contractual exit rights and erode trust fast in B2B segments.

- Buyers validate claims via drive tests and crowd data

- SLA credits or exit clauses enforce bargaining power

- Any outage can rapidly damage reputation and sales

Multi-year bundling leverage

Enterprises trade multi-year terms (typically 24–36 months) for deeper discounts and device subsidies, with providers offering up to 30% off list pricing on large deals in 2024.

Buyers demand price protection and upgrade paths across the contract life and often condition IoT and UC cross-selling on blended rates to keep effective ARPU stable.

About 64% of large buyers in 2024 required sustainability commitments or reporting as part of procurement criteria, increasing negotiation leverage.

- term-length: 24–36 months

- max-discount: up to 30% (2024)

- cross-sell: blended-rate conditions

- sustainability-demand: ~64% (2024)

Enterprise buyers exert leverage: 1-day portability, up to 30% discounts

Enterprise buyers exert strong bargaining power: rigorous tenders, one-day number portability (EEA, 2024), short contracts and up to 30% discounts on multi-year deals (24–36 months) compress margins. >50% require mobile‑UC integration; ~64% demand sustainability reporting. SLAs, drive‑test verification and blended-rate cross-sell terms shift leverage to customers.

| Metric | 2024 | Impact |

|---|---|---|

| Number portability | 1 working day | High |

| Max discount | Up to 30% | High |

| Integration requirement | >50% | High |

| Sustainability demand | ~64% | Medium‑High |

| Typical term | 24–36 months | Raises churn risk |

Full Version Awaits

Phonero Porter's Five Forces Analysis

This preview shows the exact Phonero Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted and ready for download and use the moment you buy. You're viewing the final deliverable, identical to the instant-access document provided on payment.

From Overview to Strategy Blueprint

Phonero’s Porter's Five Forces snapshot highlights competitive rivalry, buyer and supplier power, entry barriers, and substitute threats, revealing strategic pressures shaping its margins. This brief overview teases key findings and tactical implications. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Concentrated network and spectrum owners

Phonero depends on a few Norwegian MNOs for radio access and spectrum, concentrating upstream bargaining power: Norway had three nationwide MNOs in 2024, limiting wholesale alternatives. Limited alternatives enable suppliers to dictate pricing and technical terms and long-term access and roaming agreements can lock in costs and features. Any supplier network changes can immediately ripple into service quality and SLA performance.

Handset and device ecosystem leverage

Global OEMs exert strong leverage: Apple reported roughly $205 billion in iPhone revenue for fiscal 2024, while Samsung remains the largest shipper, concentrating value and limiting device margin and customization for carriers. Enterprise contracts that mandate specific devices reduce Phonero’s purchasing flexibility. Volume rebates and handset subsidies skew toward large operators, and 2024 supply‑chain disruptions tended to prioritize bigger buyers, compressing options for mid‑sized providers.

UCaaS and cloud platform dependencies

Integration with Microsoft Teams, Zoom and other UC platforms creates reliance on third-party roadmaps, fee structures and certification cycles, raising supplier bargaining power. API access, certification and co-marketing terms can be costly and subject to platform policy changes that may disrupt bundled offers. Negotiating leverage improves materially as Phonero scales activated seats with enterprise customers.

Network equipment and tower providers

Vendors for core, security and OSS/BSS are concentrated and sticky, driving material switching costs for Phonero; 5G SA rollouts in 2023–24 forced synchronized core and RAN upgrades with vendor-dependent pricing. Tower and fiber contracts commonly include inflation- or CPI-linked escalators, and service credits seldom cover the commercial impact of outages.

- Concentration: few core/OSS/BSS suppliers

- Upgrade alignment: 4G→5G SA raises capex

- Escalators: inflation-linked tower/fiber fees

- Risk: service credits rarely offset outage losses

IoT module and eSIM suppliers

IoT growth ties Phonero closely to SIM/eSIM providers and module vendors because components are standardized but price-sensitive; global cellular IoT connections surpassed 3.1 billion in 2024, keeping downward price pressure. Certification per device and band adds months and often +5–12% unit cost. Global roaming partners shape IoT pricing footprints; suppliers gain leverage when enterprises demand multi-country profiles.

- Dependency: standardized, low-margin modules

- Cost impact: certification +5–12% per device

- Leverage: multi-country eSIM profiles raise supplier power

High supplier power: 3 nationwide MNOs push up access; IoT scale and cert add costs

Supplier power is high: three Norwegian nationwide MNOs in 2024 concentrate wholesale leverage, raising access and roaming costs. Global OEMs (Apple iPhone revenue ≈ $205B in fiscal 2024) and concentrated OSS/BSS vendors limit device margins and increase switching costs. IoT scale (3.1B cellular connections in 2024) pressures module pricing; certification adds +5–12% unit cost.

| Metric | 2024 Value |

|---|---|

| Norway nationwide MNOs | 3 |

| iPhone revenue (fiscal) | $205B |

| Cellular IoT connections | 3.1B |

| Certification cost | +5–12% |

What is included in the product

Tailored Porter's Five Forces for Phonero uncover competitive intensity, buyer/supplier leverage, threats from substitutes and entrants, and strategic levers to protect margins.

Clear one-sheet Porter's Five Forces for Phonero—instantly visualize competitive pressure with a spider chart and customizable force levels, ready to drop into decks or Excel dashboards to simplify strategic decisions and reduce analysis time.

Customers Bargaining Power

Corporate RFP scale and sophistication

Enterprise customers run rigorous tenders, benchmark tariffs, and demand customization, negotiating term discounts, pooled data arrangements and SLA penalties that compress margins for Phonero.

Low switching costs via portability

Number portability in the EEA is typically completed within one working day in 2024, and widespread eSIM support on modern handsets has made carrier migration nearly instant. Standardized mobile bundles across voice, data and streaming make offers directly comparable, compressing price differentiation. Shorter contract terms (many plans now 12 months or less) raise churn risk, forcing Phonero to invest in service and feature-based retention beyond price.

Demand for integrated UC and security

Clients now demand seamless mobile-UC integration, compliance and zero-trust features, with a 2024 industry survey showing over 50% of buyers make integration a purchase prerequisite. Deals are lost despite competitive pricing if vendors fail integration or API deliverables. Buyers increasingly insist on managed services and 24/7 support without large premiums and require tailored reporting and APIs as mandatory contract items.

Service quality and coverage expectations

Business customers demand consistent nationwide coverage, reliable VoLTE/VoWiFi and strong indoor performance; SLA breaches in 2024 commonly trigger service credits or contractual exit rights and erode trust fast in B2B segments.

- Buyers validate claims via drive tests and crowd data

- SLA credits or exit clauses enforce bargaining power

- Any outage can rapidly damage reputation and sales

Multi-year bundling leverage

Enterprises trade multi-year terms (typically 24–36 months) for deeper discounts and device subsidies, with providers offering up to 30% off list pricing on large deals in 2024.

Buyers demand price protection and upgrade paths across the contract life and often condition IoT and UC cross-selling on blended rates to keep effective ARPU stable.

About 64% of large buyers in 2024 required sustainability commitments or reporting as part of procurement criteria, increasing negotiation leverage.

- term-length: 24–36 months

- max-discount: up to 30% (2024)

- cross-sell: blended-rate conditions

- sustainability-demand: ~64% (2024)

Enterprise buyers exert leverage: 1-day portability, up to 30% discounts

Enterprise buyers exert strong bargaining power: rigorous tenders, one-day number portability (EEA, 2024), short contracts and up to 30% discounts on multi-year deals (24–36 months) compress margins. >50% require mobile‑UC integration; ~64% demand sustainability reporting. SLAs, drive‑test verification and blended-rate cross-sell terms shift leverage to customers.

| Metric | 2024 | Impact |

|---|---|---|

| Number portability | 1 working day | High |

| Max discount | Up to 30% | High |

| Integration requirement | >50% | High |

| Sustainability demand | ~64% | Medium‑High |

| Typical term | 24–36 months | Raises churn risk |

Full Version Awaits

Phonero Porter's Five Forces Analysis

This preview shows the exact Phonero Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted and ready for download and use the moment you buy. You're viewing the final deliverable, identical to the instant-access document provided on payment.

Description

From Overview to Strategy Blueprint

Phonero’s Porter's Five Forces snapshot highlights competitive rivalry, buyer and supplier power, entry barriers, and substitute threats, revealing strategic pressures shaping its margins. This brief overview teases key findings and tactical implications. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Concentrated network and spectrum owners

Phonero depends on a few Norwegian MNOs for radio access and spectrum, concentrating upstream bargaining power: Norway had three nationwide MNOs in 2024, limiting wholesale alternatives. Limited alternatives enable suppliers to dictate pricing and technical terms and long-term access and roaming agreements can lock in costs and features. Any supplier network changes can immediately ripple into service quality and SLA performance.

Handset and device ecosystem leverage

Global OEMs exert strong leverage: Apple reported roughly $205 billion in iPhone revenue for fiscal 2024, while Samsung remains the largest shipper, concentrating value and limiting device margin and customization for carriers. Enterprise contracts that mandate specific devices reduce Phonero’s purchasing flexibility. Volume rebates and handset subsidies skew toward large operators, and 2024 supply‑chain disruptions tended to prioritize bigger buyers, compressing options for mid‑sized providers.

UCaaS and cloud platform dependencies

Integration with Microsoft Teams, Zoom and other UC platforms creates reliance on third-party roadmaps, fee structures and certification cycles, raising supplier bargaining power. API access, certification and co-marketing terms can be costly and subject to platform policy changes that may disrupt bundled offers. Negotiating leverage improves materially as Phonero scales activated seats with enterprise customers.

Network equipment and tower providers

Vendors for core, security and OSS/BSS are concentrated and sticky, driving material switching costs for Phonero; 5G SA rollouts in 2023–24 forced synchronized core and RAN upgrades with vendor-dependent pricing. Tower and fiber contracts commonly include inflation- or CPI-linked escalators, and service credits seldom cover the commercial impact of outages.

- Concentration: few core/OSS/BSS suppliers

- Upgrade alignment: 4G→5G SA raises capex

- Escalators: inflation-linked tower/fiber fees

- Risk: service credits rarely offset outage losses

IoT module and eSIM suppliers

IoT growth ties Phonero closely to SIM/eSIM providers and module vendors because components are standardized but price-sensitive; global cellular IoT connections surpassed 3.1 billion in 2024, keeping downward price pressure. Certification per device and band adds months and often +5–12% unit cost. Global roaming partners shape IoT pricing footprints; suppliers gain leverage when enterprises demand multi-country profiles.

- Dependency: standardized, low-margin modules

- Cost impact: certification +5–12% per device

- Leverage: multi-country eSIM profiles raise supplier power

High supplier power: 3 nationwide MNOs push up access; IoT scale and cert add costs

Supplier power is high: three Norwegian nationwide MNOs in 2024 concentrate wholesale leverage, raising access and roaming costs. Global OEMs (Apple iPhone revenue ≈ $205B in fiscal 2024) and concentrated OSS/BSS vendors limit device margins and increase switching costs. IoT scale (3.1B cellular connections in 2024) pressures module pricing; certification adds +5–12% unit cost.

| Metric | 2024 Value |

|---|---|

| Norway nationwide MNOs | 3 |

| iPhone revenue (fiscal) | $205B |

| Cellular IoT connections | 3.1B |

| Certification cost | +5–12% |

What is included in the product

Tailored Porter's Five Forces for Phonero uncover competitive intensity, buyer/supplier leverage, threats from substitutes and entrants, and strategic levers to protect margins.

Clear one-sheet Porter's Five Forces for Phonero—instantly visualize competitive pressure with a spider chart and customizable force levels, ready to drop into decks or Excel dashboards to simplify strategic decisions and reduce analysis time.

Customers Bargaining Power

Corporate RFP scale and sophistication

Enterprise customers run rigorous tenders, benchmark tariffs, and demand customization, negotiating term discounts, pooled data arrangements and SLA penalties that compress margins for Phonero.

Low switching costs via portability

Number portability in the EEA is typically completed within one working day in 2024, and widespread eSIM support on modern handsets has made carrier migration nearly instant. Standardized mobile bundles across voice, data and streaming make offers directly comparable, compressing price differentiation. Shorter contract terms (many plans now 12 months or less) raise churn risk, forcing Phonero to invest in service and feature-based retention beyond price.

Demand for integrated UC and security

Clients now demand seamless mobile-UC integration, compliance and zero-trust features, with a 2024 industry survey showing over 50% of buyers make integration a purchase prerequisite. Deals are lost despite competitive pricing if vendors fail integration or API deliverables. Buyers increasingly insist on managed services and 24/7 support without large premiums and require tailored reporting and APIs as mandatory contract items.

Service quality and coverage expectations

Business customers demand consistent nationwide coverage, reliable VoLTE/VoWiFi and strong indoor performance; SLA breaches in 2024 commonly trigger service credits or contractual exit rights and erode trust fast in B2B segments.

- Buyers validate claims via drive tests and crowd data

- SLA credits or exit clauses enforce bargaining power

- Any outage can rapidly damage reputation and sales

Multi-year bundling leverage

Enterprises trade multi-year terms (typically 24–36 months) for deeper discounts and device subsidies, with providers offering up to 30% off list pricing on large deals in 2024.

Buyers demand price protection and upgrade paths across the contract life and often condition IoT and UC cross-selling on blended rates to keep effective ARPU stable.

About 64% of large buyers in 2024 required sustainability commitments or reporting as part of procurement criteria, increasing negotiation leverage.

- term-length: 24–36 months

- max-discount: up to 30% (2024)

- cross-sell: blended-rate conditions

- sustainability-demand: ~64% (2024)

Enterprise buyers exert leverage: 1-day portability, up to 30% discounts

Enterprise buyers exert strong bargaining power: rigorous tenders, one-day number portability (EEA, 2024), short contracts and up to 30% discounts on multi-year deals (24–36 months) compress margins. >50% require mobile‑UC integration; ~64% demand sustainability reporting. SLAs, drive‑test verification and blended-rate cross-sell terms shift leverage to customers.

| Metric | 2024 | Impact |

|---|---|---|

| Number portability | 1 working day | High |

| Max discount | Up to 30% | High |

| Integration requirement | >50% | High |

| Sustainability demand | ~64% | Medium‑High |

| Typical term | 24–36 months | Raises churn risk |

Full Version Awaits

Phonero Porter's Five Forces Analysis

This preview shows the exact Phonero Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted and ready for download and use the moment you buy. You're viewing the final deliverable, identical to the instant-access document provided on payment.