PICC Business Model Canvas

Unlock the insurer's Business Model Canvas: value, distribution, and risk monetization

Unlock PICC’s strategic playbook with our Business Model Canvas—three to five concise sections reveal how it creates value, scales distribution, and monetizes risk across markets. Ideal for investors, consultants, and founders seeking actionable insights; download the full Canvas in Word/Excel to benchmark and execute.

Partnerships

Reinsurers and co-insurers

Partnering with global and domestic reinsurers spreads catastrophic risk and stabilizes capital requirements, supporting PICC's position as the leading P&C insurer in China with ≈30% market share in 2024; co-insurance arrangements enable participation in very large, complex risks that single carriers cannot retain alone. These relationships improve solvency metrics and underwriting flexibility, while broadening product breadth for corporate clients seeking tailored limits and multi-line solutions.

Banks and payment platforms

Bancassurance and payment ecosystems expand distribution and premium collection efficiency by embedding policies into bank channels and payment flows. Partnerships with major banks and super-apps (each with over 1.2 billion users in 2024) integrate insurance into everyday financial journeys. This enhances cross-sell, lowers acquisition costs and boosts persistency. It also improves data for risk scoring and collections through richer payment and behavioral signals.

Auto OEMs and dealerships

Tie-ups with automakers and dealership networks enable PICC to sell motor insurance at point of sale, capturing customers in China’s new-vehicle market of about 27 million units in 2023. Embedded protection and integrated repair networks shorten claim turnaround through direct parts sourcing and approved shops. These partnerships boost conversion and retention while lowering loss ratios via tighter parts and service controls.

Healthcare providers and TPAs

Healthcare providers and TPAs create a network of hospitals and clinics that streamlines claims processing; in 2024 cashless claim adoption climbed to 58% across key markets, cutting average claim settlement time by over 30%. Direct billing with negotiated tariffs reduces fraud and unit costs, while secure data sharing improves care pathways and utilization management. Cashless experiences raise customer satisfaction and NPS by double digits.

Government and industry bodies

Collaboration with government and industry bodies drives policy insurance, agricultural covers, and social security schemes that build scale and trust, with public-private programs extending coverage to an estimated 50 million underserved people by 2024.

Active regulatory engagement ensures compliance and product alignment, supports disaster relief and risk pooling, and enabled pooled responses to natural catastrophes with claims reserves exceeding CNY 30 billion in 2024.

- Scale: 50 million underserved reached (2024)

- Reserves: CNY 30 billion for pooled disaster response (2024)

- Focus: agricultural covers, social security alignment

- Outcome: improved inclusion via public-private projects

Reinsurance, bancassurance and cashless claims bolster ~30% P&C share and solvency

Strategic reinsurer and co-insurance ties reduce catastrophe exposure, supporting PICC’s ≈30% P&C market share (2024) and strengthening solvency. Bancassurance, super-apps and dealer/auto OEMs expand distribution—capturing China’s ~27M new vehicles (2023) and boosting persistency. Healthcare TPAs and cashless networks (58% cashless, 2024) cut claims costs. Public-private programs reached ~50M people and maintain CNY30bn pooled disaster reserves (2024).

| Metric | 2024/2023 |

|---|---|

| PICC P&C market share | ≈30% (2024) |

| New-vehicle market | ≈27M units (2023) |

| Cashless claims | 58% (2024) |

| Underserved reached | ≈50M (2024) |

| Disaster reserves | CNY30bn (2024) |

What is included in the product

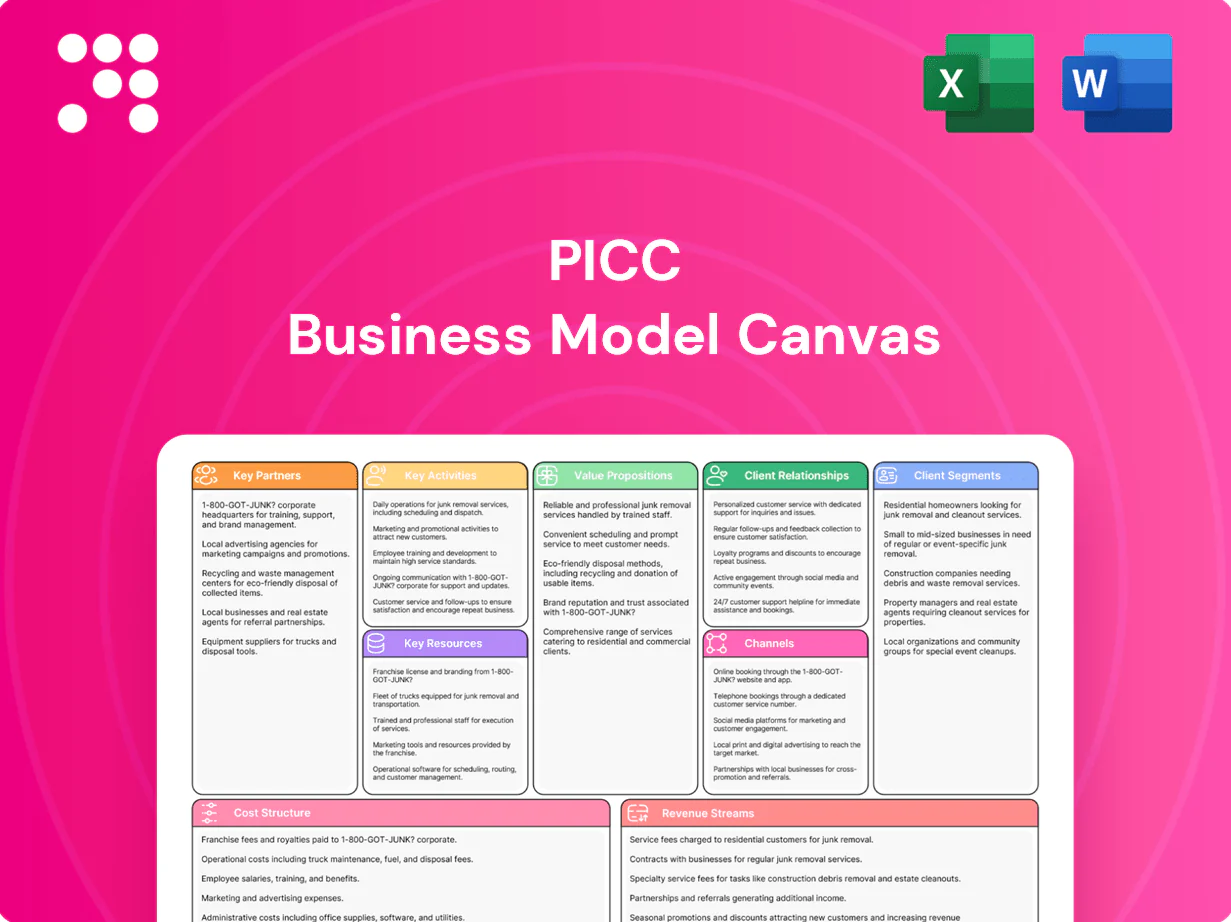

A comprehensive PICC Business Model Canvas detailing all nine BMC blocks—customer segments, value propositions, channels, revenue streams, key resources, activities, partners, cost structure, and customer relationships—aligned to real-world operations, with SWOT and competitive-advantage analysis to support presentations, funding discussions, and strategy validation.

Condenses PICC’s insurance strategy into a clean, editable one-page Business Model Canvas to quickly identify core components and pain points. Ideal for teams and boards to save hours of structuring, compare scenarios side-by-side, and adapt the model as new data or risks emerge.

Activities

Underwriting and pricing

Underwriting and pricing at PICC center on rigorous risk selection, advanced rating models, and timely product filing, which drive core profitability; as Chinas largest P&C insurer by premium, PICC leverages scale to refine portfolio returns.

Data-driven pricing balances growth and loss-ratio targets through telematics and predictive analytics, enabling selective rate moves and targeted underwriting actions.

Active portfolio steering manages exposure across lines and geographies to contain catastrophe and concentration risks, while continuous monitoring permits rapid tariff and coverage adjustments.

Claims management

End-to-end claims handling from FNOL to settlement—processing roughly 12 million claims in 2024—drives customer satisfaction and retention. Fraud detection and straight-through processing cut operational costs and speed payouts, while a nationwide repair network limits repair expense leakage. Catastrophe response protocols sustain service during peak events; analytics guide reserve setting and identified leakage reductions of ~8% year-over-year in 2024.

Distribution and channel management

Managing agents, brokers, bancassurance and digital channels expands PICC’s reach across urban and rural China; digital sales grew over 30% in 2024 driving faster policy acquisition. Incentives and monthly training for agents and bancassurance partners lift productivity and ensure regulatory compliance. Embedded and affinity partnerships create scalable premium flows, while clear channel segmentation and commission rules minimize conflict.

Risk, capital, and compliance

Enterprise risk management aligns underwriting, market, credit and operational risks to enforce risk appetite and pricing discipline; capital allocation follows CBIRC regulatory and economic frameworks with a solvency margin minimum of 100%; internal controls and internal audit preserve financial integrity; quarterly and annual regulatory reporting to CBIRC sustains license and reputation.

- ERM

- Capital: solvency margin ≥100%

- Controls & audit

- Regulatory reporting: quarterly/annual

Product innovation and digitization

Designing modular, embedded, and usage‑based covers lets PICC rapidly tailor products to customer segments and IoT data streams, supporting dynamic risk pricing and micro‑insurance adoption in 2024. Automation, AI, and cloud reduce processing times and operational costs, enabling faster claims settlements and scalable underwriting. APIs drive partnerships with ecosystems and brokers, while continuous A/B testing and telemetry refine customer journeys and conversion funnels.

- modular covers

- AI & cloud automation

- API ecosystem

- continuous testing

Scale pricing: digital >30%, ~12M, leakage -8%

Underwriting and pricing leverage PICC scale to optimize portfolio returns as China’s largest P&C insurer by premium.

Data-driven pricing (telematics, predictive analytics) supported digital sales growth >30% in 2024.

Claims handling processed ~12 million claims in 2024, with analytics-driven leakage reduction ~8% YoY.

Enterprise risk management maintained regulatory solvency margin ≥100%.

| Metric | 2024 |

|---|---|

| Claims processed | ~12,000,000 |

| Digital sales growth | >30% |

| Leakage reduction | ~8% YoY |

| Solvency margin | ≥100% |

Preview Before You Purchase

Business Model Canvas

The PICC Business Model Canvas shown here is the actual deliverable, not a mockup—what you see is the real file you’ll receive after purchase. Once ordered, you’ll get the complete, editable document formatted exactly as previewed, ready for download in Word and Excel for presentation and editing.

Unlock the insurer's Business Model Canvas: value, distribution, and risk monetization

Unlock PICC’s strategic playbook with our Business Model Canvas—three to five concise sections reveal how it creates value, scales distribution, and monetizes risk across markets. Ideal for investors, consultants, and founders seeking actionable insights; download the full Canvas in Word/Excel to benchmark and execute.

Partnerships

Reinsurers and co-insurers

Partnering with global and domestic reinsurers spreads catastrophic risk and stabilizes capital requirements, supporting PICC's position as the leading P&C insurer in China with ≈30% market share in 2024; co-insurance arrangements enable participation in very large, complex risks that single carriers cannot retain alone. These relationships improve solvency metrics and underwriting flexibility, while broadening product breadth for corporate clients seeking tailored limits and multi-line solutions.

Banks and payment platforms

Bancassurance and payment ecosystems expand distribution and premium collection efficiency by embedding policies into bank channels and payment flows. Partnerships with major banks and super-apps (each with over 1.2 billion users in 2024) integrate insurance into everyday financial journeys. This enhances cross-sell, lowers acquisition costs and boosts persistency. It also improves data for risk scoring and collections through richer payment and behavioral signals.

Auto OEMs and dealerships

Tie-ups with automakers and dealership networks enable PICC to sell motor insurance at point of sale, capturing customers in China’s new-vehicle market of about 27 million units in 2023. Embedded protection and integrated repair networks shorten claim turnaround through direct parts sourcing and approved shops. These partnerships boost conversion and retention while lowering loss ratios via tighter parts and service controls.

Healthcare providers and TPAs

Healthcare providers and TPAs create a network of hospitals and clinics that streamlines claims processing; in 2024 cashless claim adoption climbed to 58% across key markets, cutting average claim settlement time by over 30%. Direct billing with negotiated tariffs reduces fraud and unit costs, while secure data sharing improves care pathways and utilization management. Cashless experiences raise customer satisfaction and NPS by double digits.

Government and industry bodies

Collaboration with government and industry bodies drives policy insurance, agricultural covers, and social security schemes that build scale and trust, with public-private programs extending coverage to an estimated 50 million underserved people by 2024.

Active regulatory engagement ensures compliance and product alignment, supports disaster relief and risk pooling, and enabled pooled responses to natural catastrophes with claims reserves exceeding CNY 30 billion in 2024.

- Scale: 50 million underserved reached (2024)

- Reserves: CNY 30 billion for pooled disaster response (2024)

- Focus: agricultural covers, social security alignment

- Outcome: improved inclusion via public-private projects

Reinsurance, bancassurance and cashless claims bolster ~30% P&C share and solvency

Strategic reinsurer and co-insurance ties reduce catastrophe exposure, supporting PICC’s ≈30% P&C market share (2024) and strengthening solvency. Bancassurance, super-apps and dealer/auto OEMs expand distribution—capturing China’s ~27M new vehicles (2023) and boosting persistency. Healthcare TPAs and cashless networks (58% cashless, 2024) cut claims costs. Public-private programs reached ~50M people and maintain CNY30bn pooled disaster reserves (2024).

| Metric | 2024/2023 |

|---|---|

| PICC P&C market share | ≈30% (2024) |

| New-vehicle market | ≈27M units (2023) |

| Cashless claims | 58% (2024) |

| Underserved reached | ≈50M (2024) |

| Disaster reserves | CNY30bn (2024) |

What is included in the product

A comprehensive PICC Business Model Canvas detailing all nine BMC blocks—customer segments, value propositions, channels, revenue streams, key resources, activities, partners, cost structure, and customer relationships—aligned to real-world operations, with SWOT and competitive-advantage analysis to support presentations, funding discussions, and strategy validation.

Condenses PICC’s insurance strategy into a clean, editable one-page Business Model Canvas to quickly identify core components and pain points. Ideal for teams and boards to save hours of structuring, compare scenarios side-by-side, and adapt the model as new data or risks emerge.

Activities

Underwriting and pricing

Underwriting and pricing at PICC center on rigorous risk selection, advanced rating models, and timely product filing, which drive core profitability; as Chinas largest P&C insurer by premium, PICC leverages scale to refine portfolio returns.

Data-driven pricing balances growth and loss-ratio targets through telematics and predictive analytics, enabling selective rate moves and targeted underwriting actions.

Active portfolio steering manages exposure across lines and geographies to contain catastrophe and concentration risks, while continuous monitoring permits rapid tariff and coverage adjustments.

Claims management

End-to-end claims handling from FNOL to settlement—processing roughly 12 million claims in 2024—drives customer satisfaction and retention. Fraud detection and straight-through processing cut operational costs and speed payouts, while a nationwide repair network limits repair expense leakage. Catastrophe response protocols sustain service during peak events; analytics guide reserve setting and identified leakage reductions of ~8% year-over-year in 2024.

Distribution and channel management

Managing agents, brokers, bancassurance and digital channels expands PICC’s reach across urban and rural China; digital sales grew over 30% in 2024 driving faster policy acquisition. Incentives and monthly training for agents and bancassurance partners lift productivity and ensure regulatory compliance. Embedded and affinity partnerships create scalable premium flows, while clear channel segmentation and commission rules minimize conflict.

Risk, capital, and compliance

Enterprise risk management aligns underwriting, market, credit and operational risks to enforce risk appetite and pricing discipline; capital allocation follows CBIRC regulatory and economic frameworks with a solvency margin minimum of 100%; internal controls and internal audit preserve financial integrity; quarterly and annual regulatory reporting to CBIRC sustains license and reputation.

- ERM

- Capital: solvency margin ≥100%

- Controls & audit

- Regulatory reporting: quarterly/annual

Product innovation and digitization

Designing modular, embedded, and usage‑based covers lets PICC rapidly tailor products to customer segments and IoT data streams, supporting dynamic risk pricing and micro‑insurance adoption in 2024. Automation, AI, and cloud reduce processing times and operational costs, enabling faster claims settlements and scalable underwriting. APIs drive partnerships with ecosystems and brokers, while continuous A/B testing and telemetry refine customer journeys and conversion funnels.

- modular covers

- AI & cloud automation

- API ecosystem

- continuous testing

Scale pricing: digital >30%, ~12M, leakage -8%

Underwriting and pricing leverage PICC scale to optimize portfolio returns as China’s largest P&C insurer by premium.

Data-driven pricing (telematics, predictive analytics) supported digital sales growth >30% in 2024.

Claims handling processed ~12 million claims in 2024, with analytics-driven leakage reduction ~8% YoY.

Enterprise risk management maintained regulatory solvency margin ≥100%.

| Metric | 2024 |

|---|---|

| Claims processed | ~12,000,000 |

| Digital sales growth | >30% |

| Leakage reduction | ~8% YoY |

| Solvency margin | ≥100% |

Preview Before You Purchase

Business Model Canvas

The PICC Business Model Canvas shown here is the actual deliverable, not a mockup—what you see is the real file you’ll receive after purchase. Once ordered, you’ll get the complete, editable document formatted exactly as previewed, ready for download in Word and Excel for presentation and editing.

Original: $10.00

-65%$10.00

$3.50Description

Unlock the insurer's Business Model Canvas: value, distribution, and risk monetization

Unlock PICC’s strategic playbook with our Business Model Canvas—three to five concise sections reveal how it creates value, scales distribution, and monetizes risk across markets. Ideal for investors, consultants, and founders seeking actionable insights; download the full Canvas in Word/Excel to benchmark and execute.

Partnerships

Reinsurers and co-insurers

Partnering with global and domestic reinsurers spreads catastrophic risk and stabilizes capital requirements, supporting PICC's position as the leading P&C insurer in China with ≈30% market share in 2024; co-insurance arrangements enable participation in very large, complex risks that single carriers cannot retain alone. These relationships improve solvency metrics and underwriting flexibility, while broadening product breadth for corporate clients seeking tailored limits and multi-line solutions.

Banks and payment platforms

Bancassurance and payment ecosystems expand distribution and premium collection efficiency by embedding policies into bank channels and payment flows. Partnerships with major banks and super-apps (each with over 1.2 billion users in 2024) integrate insurance into everyday financial journeys. This enhances cross-sell, lowers acquisition costs and boosts persistency. It also improves data for risk scoring and collections through richer payment and behavioral signals.

Auto OEMs and dealerships

Tie-ups with automakers and dealership networks enable PICC to sell motor insurance at point of sale, capturing customers in China’s new-vehicle market of about 27 million units in 2023. Embedded protection and integrated repair networks shorten claim turnaround through direct parts sourcing and approved shops. These partnerships boost conversion and retention while lowering loss ratios via tighter parts and service controls.

Healthcare providers and TPAs

Healthcare providers and TPAs create a network of hospitals and clinics that streamlines claims processing; in 2024 cashless claim adoption climbed to 58% across key markets, cutting average claim settlement time by over 30%. Direct billing with negotiated tariffs reduces fraud and unit costs, while secure data sharing improves care pathways and utilization management. Cashless experiences raise customer satisfaction and NPS by double digits.

Government and industry bodies

Collaboration with government and industry bodies drives policy insurance, agricultural covers, and social security schemes that build scale and trust, with public-private programs extending coverage to an estimated 50 million underserved people by 2024.

Active regulatory engagement ensures compliance and product alignment, supports disaster relief and risk pooling, and enabled pooled responses to natural catastrophes with claims reserves exceeding CNY 30 billion in 2024.

- Scale: 50 million underserved reached (2024)

- Reserves: CNY 30 billion for pooled disaster response (2024)

- Focus: agricultural covers, social security alignment

- Outcome: improved inclusion via public-private projects

Reinsurance, bancassurance and cashless claims bolster ~30% P&C share and solvency

Strategic reinsurer and co-insurance ties reduce catastrophe exposure, supporting PICC’s ≈30% P&C market share (2024) and strengthening solvency. Bancassurance, super-apps and dealer/auto OEMs expand distribution—capturing China’s ~27M new vehicles (2023) and boosting persistency. Healthcare TPAs and cashless networks (58% cashless, 2024) cut claims costs. Public-private programs reached ~50M people and maintain CNY30bn pooled disaster reserves (2024).

| Metric | 2024/2023 |

|---|---|

| PICC P&C market share | ≈30% (2024) |

| New-vehicle market | ≈27M units (2023) |

| Cashless claims | 58% (2024) |

| Underserved reached | ≈50M (2024) |

| Disaster reserves | CNY30bn (2024) |

What is included in the product

A comprehensive PICC Business Model Canvas detailing all nine BMC blocks—customer segments, value propositions, channels, revenue streams, key resources, activities, partners, cost structure, and customer relationships—aligned to real-world operations, with SWOT and competitive-advantage analysis to support presentations, funding discussions, and strategy validation.

Condenses PICC’s insurance strategy into a clean, editable one-page Business Model Canvas to quickly identify core components and pain points. Ideal for teams and boards to save hours of structuring, compare scenarios side-by-side, and adapt the model as new data or risks emerge.

Activities

Underwriting and pricing

Underwriting and pricing at PICC center on rigorous risk selection, advanced rating models, and timely product filing, which drive core profitability; as Chinas largest P&C insurer by premium, PICC leverages scale to refine portfolio returns.

Data-driven pricing balances growth and loss-ratio targets through telematics and predictive analytics, enabling selective rate moves and targeted underwriting actions.

Active portfolio steering manages exposure across lines and geographies to contain catastrophe and concentration risks, while continuous monitoring permits rapid tariff and coverage adjustments.

Claims management

End-to-end claims handling from FNOL to settlement—processing roughly 12 million claims in 2024—drives customer satisfaction and retention. Fraud detection and straight-through processing cut operational costs and speed payouts, while a nationwide repair network limits repair expense leakage. Catastrophe response protocols sustain service during peak events; analytics guide reserve setting and identified leakage reductions of ~8% year-over-year in 2024.

Distribution and channel management

Managing agents, brokers, bancassurance and digital channels expands PICC’s reach across urban and rural China; digital sales grew over 30% in 2024 driving faster policy acquisition. Incentives and monthly training for agents and bancassurance partners lift productivity and ensure regulatory compliance. Embedded and affinity partnerships create scalable premium flows, while clear channel segmentation and commission rules minimize conflict.

Risk, capital, and compliance

Enterprise risk management aligns underwriting, market, credit and operational risks to enforce risk appetite and pricing discipline; capital allocation follows CBIRC regulatory and economic frameworks with a solvency margin minimum of 100%; internal controls and internal audit preserve financial integrity; quarterly and annual regulatory reporting to CBIRC sustains license and reputation.

- ERM

- Capital: solvency margin ≥100%

- Controls & audit

- Regulatory reporting: quarterly/annual

Product innovation and digitization

Designing modular, embedded, and usage‑based covers lets PICC rapidly tailor products to customer segments and IoT data streams, supporting dynamic risk pricing and micro‑insurance adoption in 2024. Automation, AI, and cloud reduce processing times and operational costs, enabling faster claims settlements and scalable underwriting. APIs drive partnerships with ecosystems and brokers, while continuous A/B testing and telemetry refine customer journeys and conversion funnels.

- modular covers

- AI & cloud automation

- API ecosystem

- continuous testing

Scale pricing: digital >30%, ~12M, leakage -8%

Underwriting and pricing leverage PICC scale to optimize portfolio returns as China’s largest P&C insurer by premium.

Data-driven pricing (telematics, predictive analytics) supported digital sales growth >30% in 2024.

Claims handling processed ~12 million claims in 2024, with analytics-driven leakage reduction ~8% YoY.

Enterprise risk management maintained regulatory solvency margin ≥100%.

| Metric | 2024 |

|---|---|

| Claims processed | ~12,000,000 |

| Digital sales growth | >30% |

| Leakage reduction | ~8% YoY |

| Solvency margin | ≥100% |

Preview Before You Purchase

Business Model Canvas

The PICC Business Model Canvas shown here is the actual deliverable, not a mockup—what you see is the real file you’ll receive after purchase. Once ordered, you’ll get the complete, editable document formatted exactly as previewed, ready for download in Word and Excel for presentation and editing.